These are top 10 stocks traded on the Robinhood UK platform in July

Introduction & Market Context

Alerus Financial Corp (NASDAQ:ALRS) released its first quarter 2025 investor presentation on April 29, highlighting strong financial performance across its diversified business segments. The commercial wealth bank and national retirement plan provider reported significant improvements in key metrics, with adjusted earnings per share jumping 25% quarter-over-quarter following the successful integration of HMN Financial (HMNF).

The results mark Alerus’s first full quarter with HMNF fully integrated, providing what management described as a "strong tailwind" for the company’s performance. Despite the positive quarterly results, Alerus’s stock closed at $17.76 on April 28, 2025, with a slight increase of 0.23% on the day, suggesting investors may still be assessing the long-term impact of the company’s recent strategic moves.

Quarterly Performance Highlights

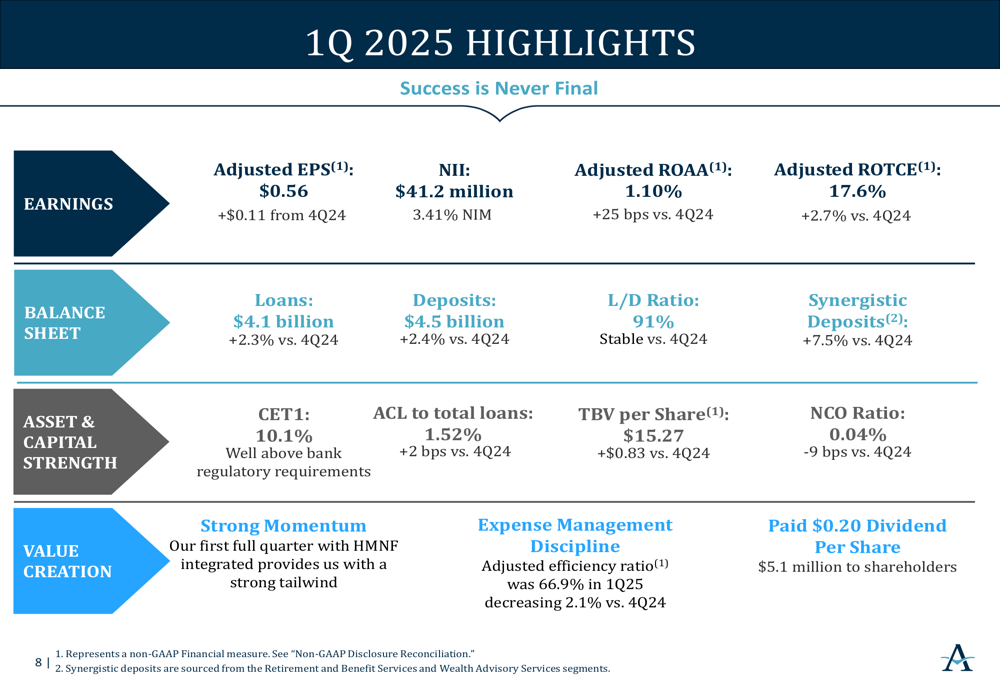

Alerus reported adjusted earnings per share of $0.56 for Q1 2025, representing a $0.11 or 25% increase from the $0.44 reported in Q4 2024. This performance was driven by robust net interest income growth and improved operational efficiency.

As shown in the following comprehensive overview of Q1 2025 results:

Key financial metrics showed notable improvement, with net interest income reaching $41.2 million and net interest margin expanding to 3.41%, a 21 basis point increase from the previous quarter. The company’s adjusted return on average assets (ROAA) improved to 1.10%, up 25 basis points from Q4 2024, while adjusted return on tangible common equity (ROTCE) reached 17.6%, an increase of 2.7 percentage points.

Balance sheet growth remained solid, with loans increasing by $93 million (2.3%) to $4.1 billion and deposits growing by $107 million (2.4%) to $4.5 billion compared to the end of 2024. The loan-to-deposit ratio remained stable at 91%, reflecting balanced growth across both sides of the balance sheet.

The detailed income statement further illustrates the company’s financial performance:

Detailed Financial Analysis

Alerus’s business model continues to benefit from its diversified revenue streams, with net interest income representing 51.8% of total revenue, followed by retirement and benefits services (26.6%), wealth advisory (11.1%), and banking fees and other revenue (10.5%).

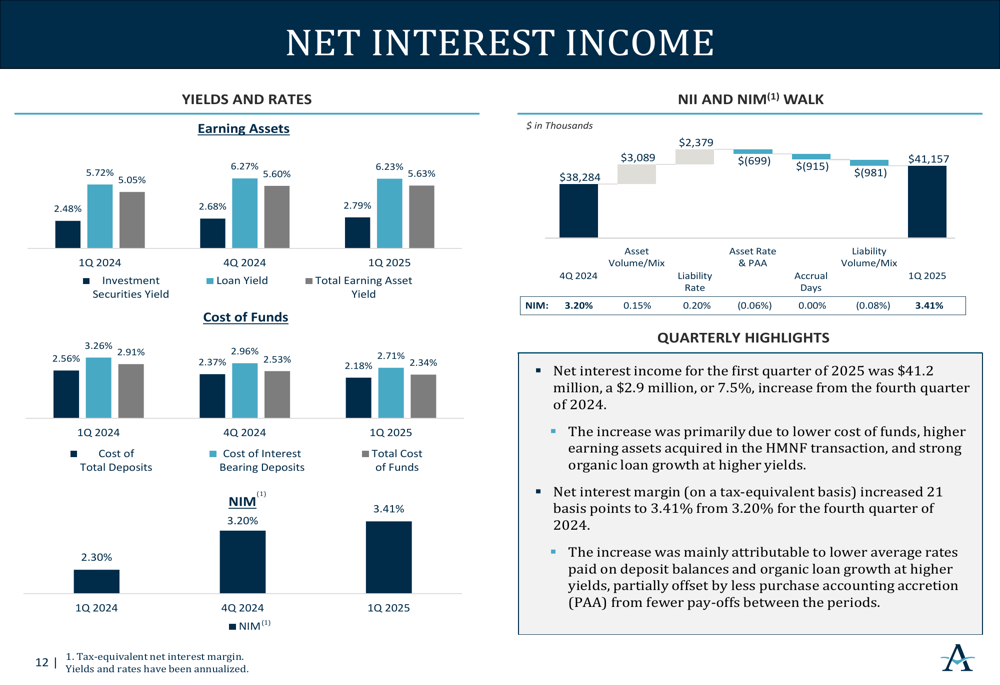

The loan portfolio shows a balanced mix across various segments, with commercial real estate representing the largest portion:

On the funding side, the deposit base remains well-diversified, with money market and savings accounts comprising the largest segment at 32.3%, followed by interest-bearing demand deposits at 28.6%, and non-interest bearing deposits at 19.8%. Notably, synergistic deposits—those generated from the company’s wealth management and retirement services businesses—grew by 7.5% quarter-over-quarter and now represent 23.3% of total deposits.

The following chart provides a detailed breakdown of the deposit characteristics:

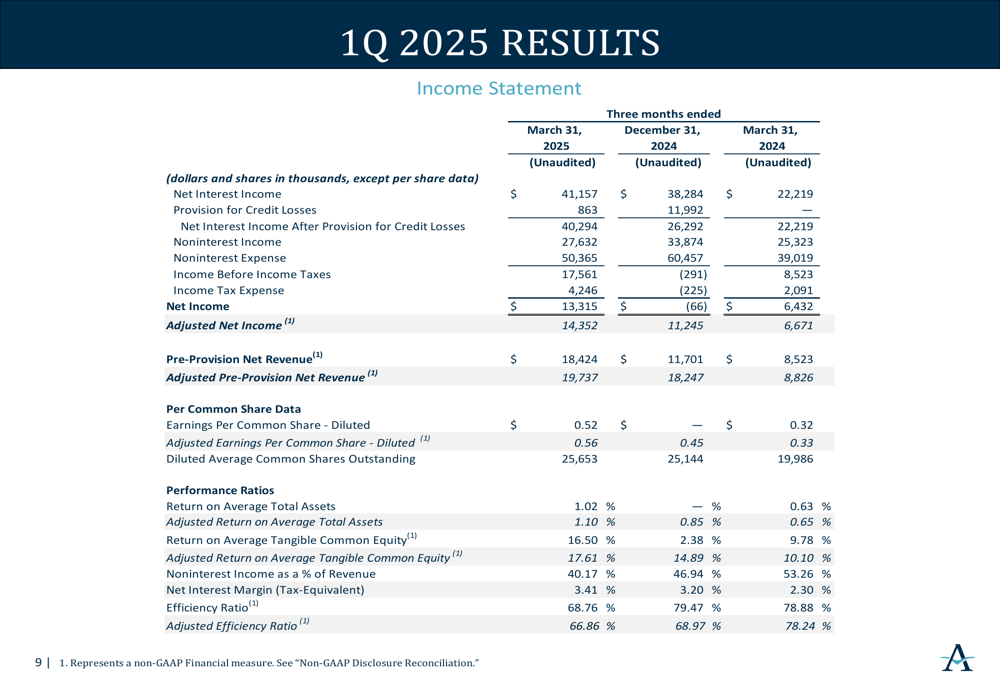

Net interest income showed significant improvement, increasing by 7.5% quarter-over-quarter and 85.2% year-over-year to $41.2 million. This growth was driven by the expansion of net interest margin to 3.41%, up from 3.20% in Q4 2024, reflecting the company’s ability to manage its interest rate spread effectively in the current rate environment.

Non-interest income decreased by 18.4% quarter-over-quarter but increased by 9.1% year-over-year to $27.6 million. The quarterly decline was primarily due to seasonal factors and the normalization of certain fee income streams following the HMNF integration.

On the expense side, Alerus demonstrated improved cost discipline, with the adjusted efficiency ratio decreasing to 66.9% in Q1 2025, down 2.1 percentage points from Q4 2024. Non-interest expense decreased by 16.7% quarter-over-quarter but increased by 29.1% year-over-year, reflecting the impact of the HMNF acquisition.

Strategic Initiatives & Outlook

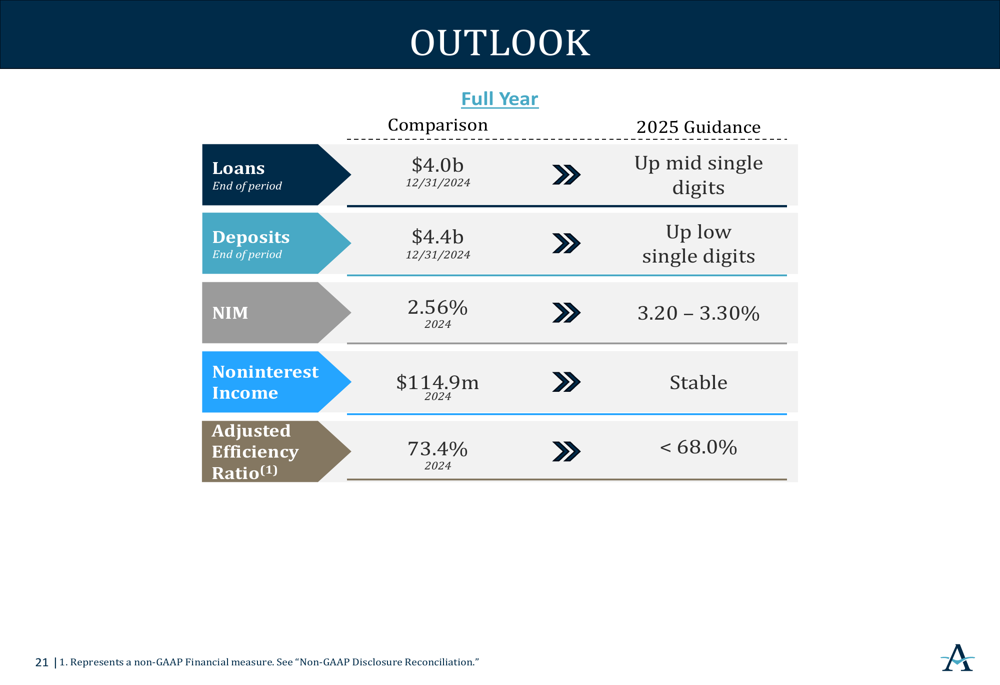

Looking ahead, Alerus provided a positive outlook for the full year 2025, projecting continued growth across key metrics:

The company expects mid-single-digit loan growth and low single-digit deposit growth for the full year. Net interest margin is projected to remain between 3.20% and 3.30%, while non-interest income is expected to remain stable. Management also anticipates further improvement in operational efficiency, with the adjusted efficiency ratio projected to be below 68.0%.

Alerus continues to focus on its strategic initiatives, including organic growth, becoming an employer of choice, pursuing strategic acquisitions, and improving productivity and efficiency. The company’s diversified business model, combining banking, retirement and benefits, and wealth advisory services, provides multiple growth avenues and revenue diversification.

The key takeaways from the presentation highlight the company’s strong start to 2025:

Capital Position & Shareholder Returns

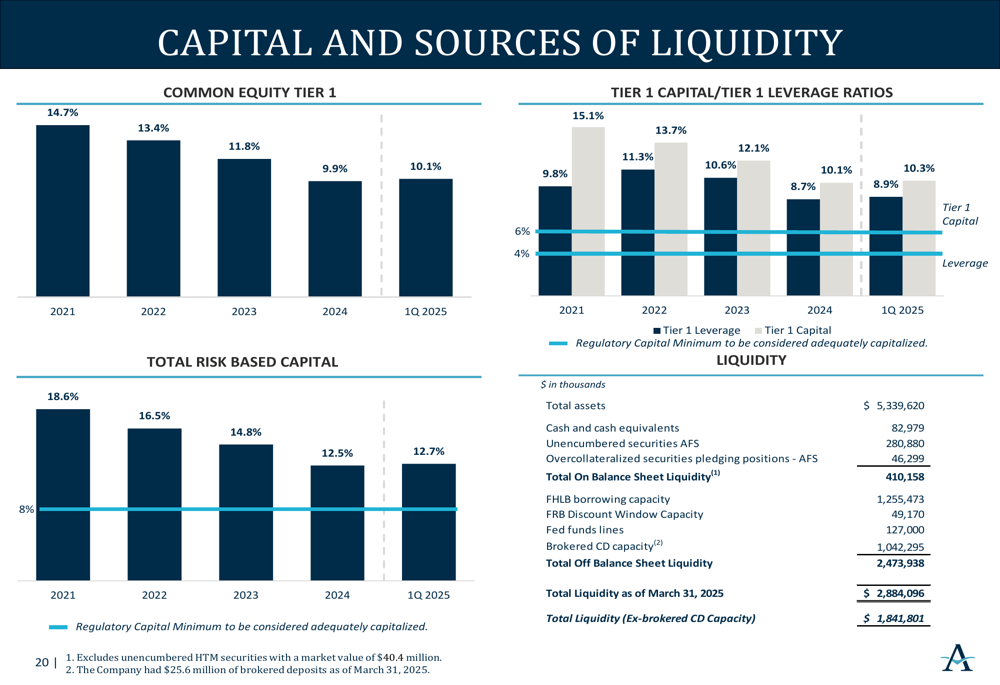

Alerus maintains a strong capital position, with a Common Equity Tier 1 (CET1) ratio of 10.1%, well above regulatory requirements. The company’s allowance for credit losses to total loans stands at 1.52%, reflecting prudent risk management in the current economic environment.

Tangible book value per share increased to $15.27, up $0.83 or 5.7% from the previous quarter, demonstrating continued value creation for shareholders. During the quarter, Alerus returned $5.1 million to shareholders through dividends, paying $0.20 per share.

Asset quality remains solid, with the net charge-off ratio decreasing to 0.04% in Q1 2025, down 9 basis points from the previous quarter. This improvement reflects the company’s disciplined underwriting standards and effective credit risk management.

Conclusion

Alerus’s Q1 2025 results demonstrate the company’s ability to execute on its strategic initiatives and deliver improved financial performance following the integration of HMN Financial. The diversified business model continues to provide resilience and multiple growth avenues, while the strong capital position supports future expansion opportunities.

While the stock price has not yet fully reflected the improved performance, the company’s focus on long-term value creation through balanced growth, operational efficiency, and disciplined capital management positions it well for continued success in 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.