Intel stock extends gains after report of possible U.S. government stake

Introduction & Market Context

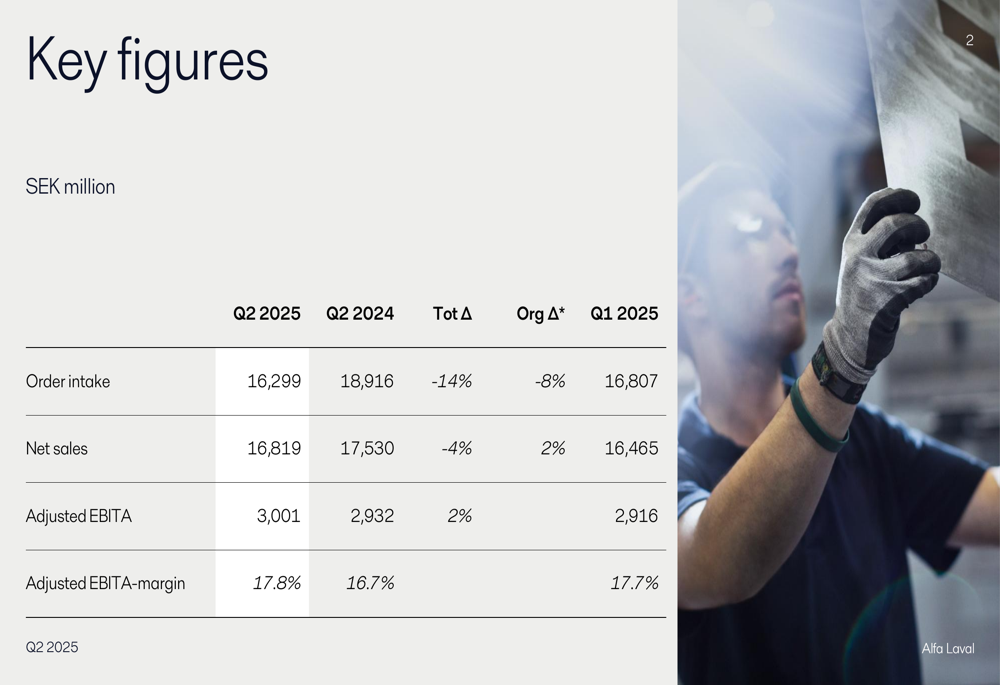

Alfa Laval AB (STO:ALFA) released its second quarter 2025 results on July 21, showing improved profitability despite declining revenues and order intake. The company’s stock closed at 421.2 SEK on the reporting day, down 0.71% from the previous close, reflecting mixed investor sentiment about the results.

The industrial equipment manufacturer demonstrated resilience in a challenging market environment, with its adjusted EBITA margin expanding to 17.8% from 16.7% in the same quarter last year. This improvement came despite a 4.1% decline in sales and a more substantial 13.8% drop in order intake.

Quarterly Performance Highlights

Alfa Laval reported Q2 2025 sales of 16,819 million SEK, representing a 4.1% decline compared to the same period last year. However, organic growth was positive at 2.3%, with currency effects (-6.5%) accounting for the overall decline. The company’s adjusted EBITA reached 3,001 million SEK, up from 2,932 million SEK in Q2 2024.

As shown in the following chart of key financial figures:

Earnings per share improved to 4.87 SEK, up from 4.08 SEK in Q2 2024, representing a 19.4% increase. This performance marks a continued improvement from Q1 2025, when the company reported EPS of 4.82 SEK.

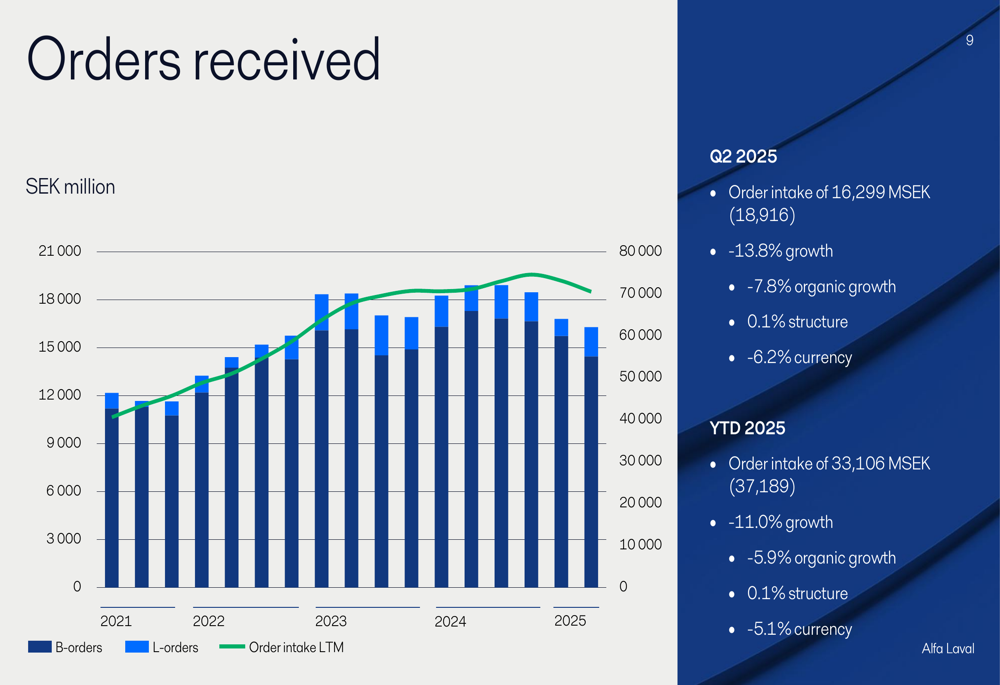

The company’s order intake declined significantly to 16,299 million SEK, down 14% from Q2 2024, with organic decline of 8%. This represents a sequential decline from Q1 2025’s order intake of 16,807 million SEK, potentially signaling challenges ahead.

The following chart illustrates the order intake trends:

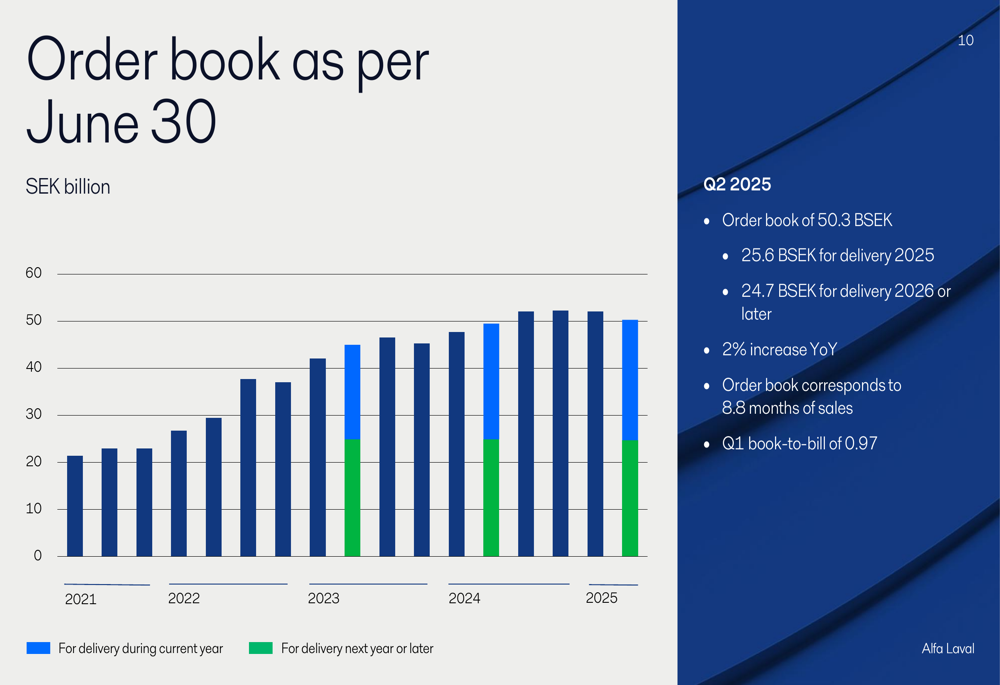

Despite the order decline, Alfa Laval’s order book remains strong at 50.3 billion SEK, representing a 2% increase year-over-year and equivalent to 8.8 months of sales. The Q1 book-to-bill ratio was 0.97, indicating that new orders are slightly below current sales levels.

Divisional Performance Analysis

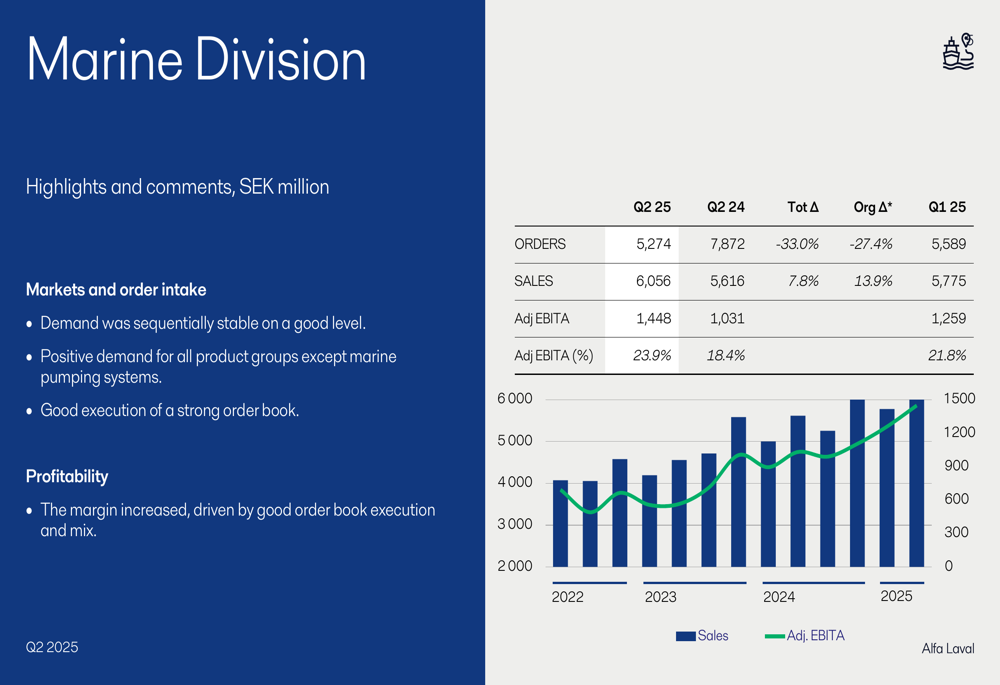

Alfa Laval’s three divisions showed markedly different performance patterns in Q2 2025, with Marine standing out as the strongest performer.

The Marine division demonstrated impressive margin improvement, with adjusted EBITA margin rising to 23.9% from 18.4% in Q2 2024. Sales increased by 7.8% to 6,056 million SEK, though order intake fell sharply by 33% to 5,274 million SEK. According to the presentation, the margin increase was "driven by good order book execution and mix."

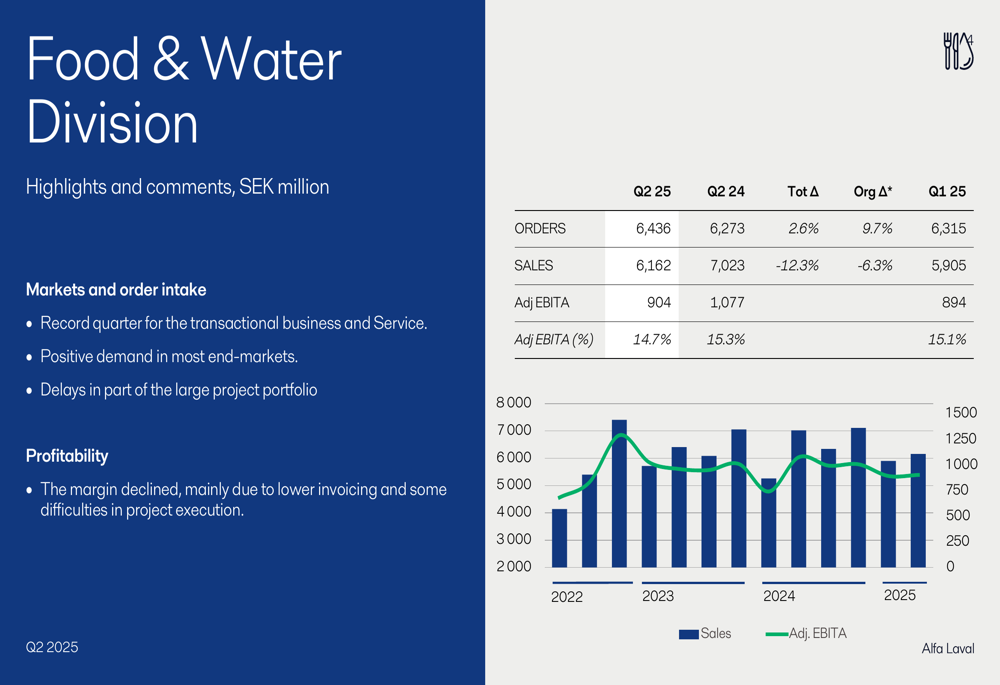

The Food & Water division faced challenges with sales declining 12.3% to 6,162 million SEK, while order intake increased 2.6% to 6,436 million SEK. The division’s adjusted EBITA margin decreased to 14.7% from 15.3%, with the company citing "margin decline mainly due to lower invoicing and difficulties in project execution."

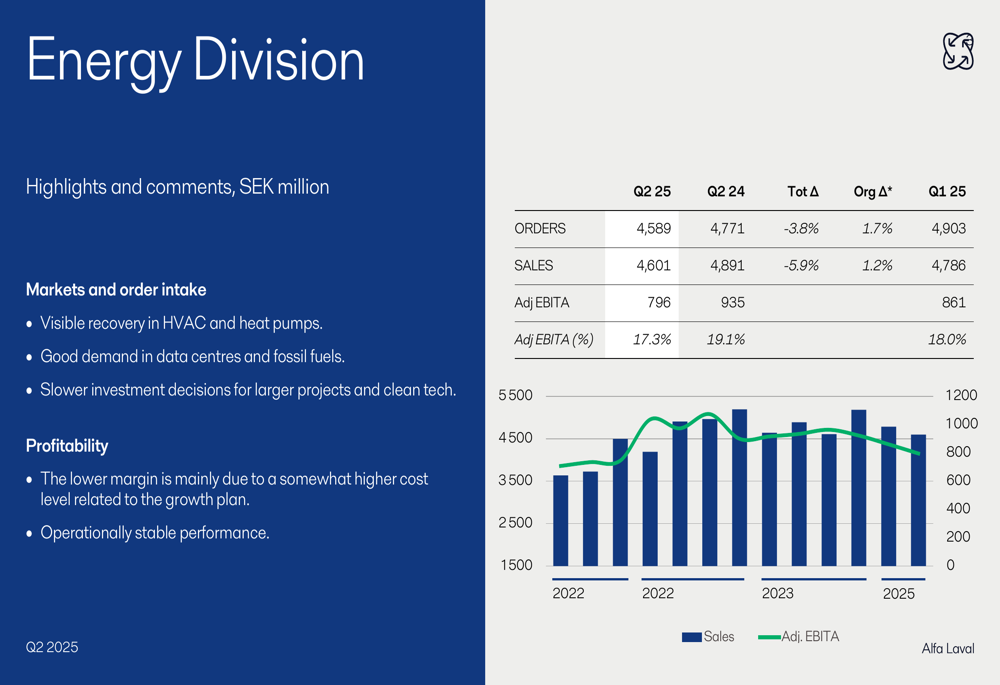

The Energy division reported a 5.9% sales decline to 4,601 million SEK and a 3.8% order decline to 4,589 million SEK. Its adjusted EBITA margin fell to 17.3% from 19.1% in Q2 2024. The presentation noted "visible recovery in HVAC and heat pumps" but also "lower margin mainly due to higher cost levels related to the growth plan."

Service orders continued to be a bright spot for Alfa Laval, with the following breakdown of service order contributions from each division:

Financial Position and Outlook

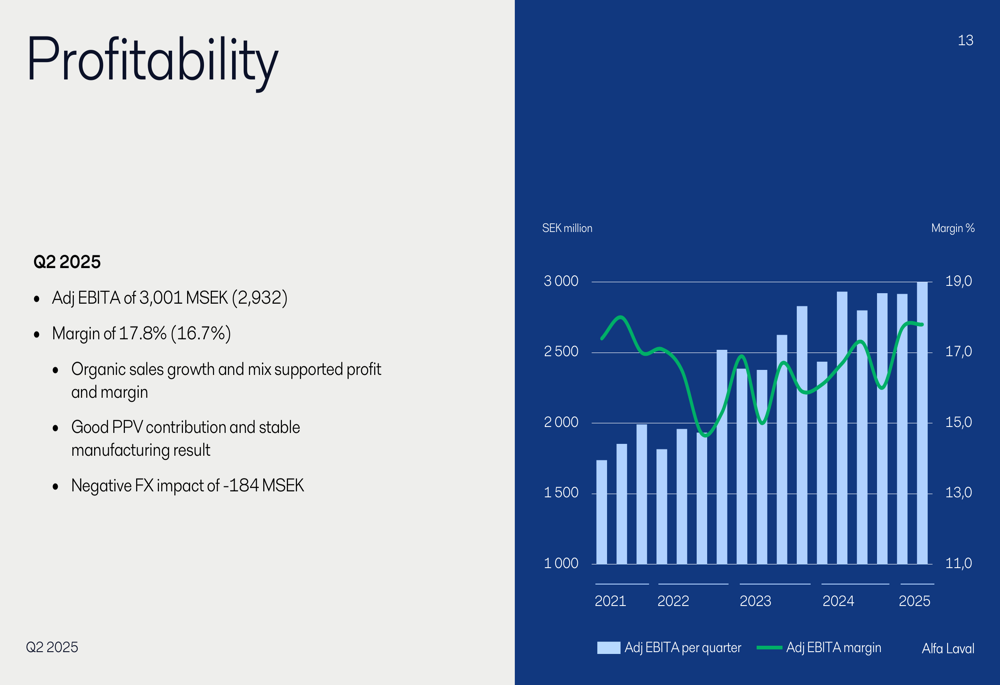

Alfa Laval’s profitability improved in Q2 2025, with the adjusted EBITA margin reaching 17.8%, up from 16.7% in Q2 2024. The company attributed this improvement to organic sales growth, favorable mix, good price/cost management, and stable manufacturing results, despite a negative FX impact of 184 million SEK.

The following chart illustrates the profitability trends:

The company’s financial position strengthened, with net debt excluding leases decreasing to 4,625 million SEK from 7,718 million SEK in Q2 2024. The net debt to EBITDA ratio improved to 0.34 from 0.62, indicating increased financial flexibility.

Free cash flow declined to 1,483 million SEK from 2,014 million SEK in Q2 2024, primarily due to a 711 million SEK increase in working capital. Capital expenditures for the quarter were 676 million SEK, slightly lower than the 741 million SEK spent in Q2 2024.

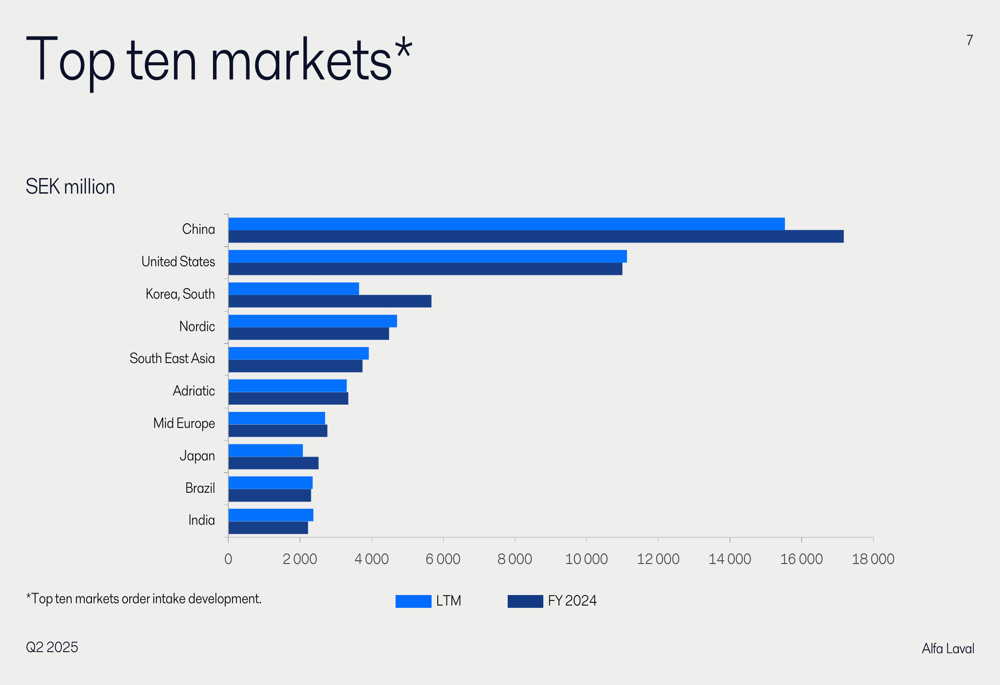

Alfa Laval’s geographical presence remains diverse, with China, the United States, and South Korea representing the top markets by order intake:

Forward-Looking Statements

Looking ahead, Alfa Laval provided a cautiously optimistic outlook for Q3 2025, stating: "We expect demand in the third quarter to be somewhat higher compared to the second quarter." This suggests a potential stabilization or modest improvement in order intake.

For Q3 2025, the company expects capital expenditures of approximately 0.7 billion SEK, with PPA amortization of around 125 million SEK and a tax rate between 24-26%. For the full year 2025, capital expenditures are estimated at 2.5-3.0 billion SEK.

The divergent performance across divisions presents both opportunities and challenges for Alfa Laval. The Marine division’s strong margin performance demonstrates the company’s ability to execute effectively in favorable market conditions, while the challenges in Food & Water and Energy divisions highlight areas requiring management attention.

While the overall order decline is concerning, Alfa Laval’s improved profitability, strong order book, and healthy financial position provide a solid foundation for navigating the current market environment. Investors will be watching closely to see if the anticipated demand improvement in Q3 materializes and whether the company can maintain its margin expansion while returning to order and revenue growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.