Oklo stock tumbles as Financial Times scrutinizes valuation

Introduction & Market Context

Alfa Sigma presented its Q2 2025 earnings results on July 24, highlighting the completion of its corporate transformation into a pure-play packaged food business. The company reported strong EBITDA performance, though results were significantly boosted by insurance reimbursements related to flood damage at its Torrente facility in Spain.

The presentation revealed that Alfa shares began trading as a dedicated food business on April 7, following the spin-off of Alfa’s share ownership in Alpek on October 24, 2024, with shareholders receiving shares on April 4, 2025. The company’s Global Industry Classification Standard (GICS) has changed to "Consumer Staples," aligning with its new focus, and preparations are underway to change Alfa’s name and ticker.

As shown in the following transformation overview:

Quarterly Performance Highlights

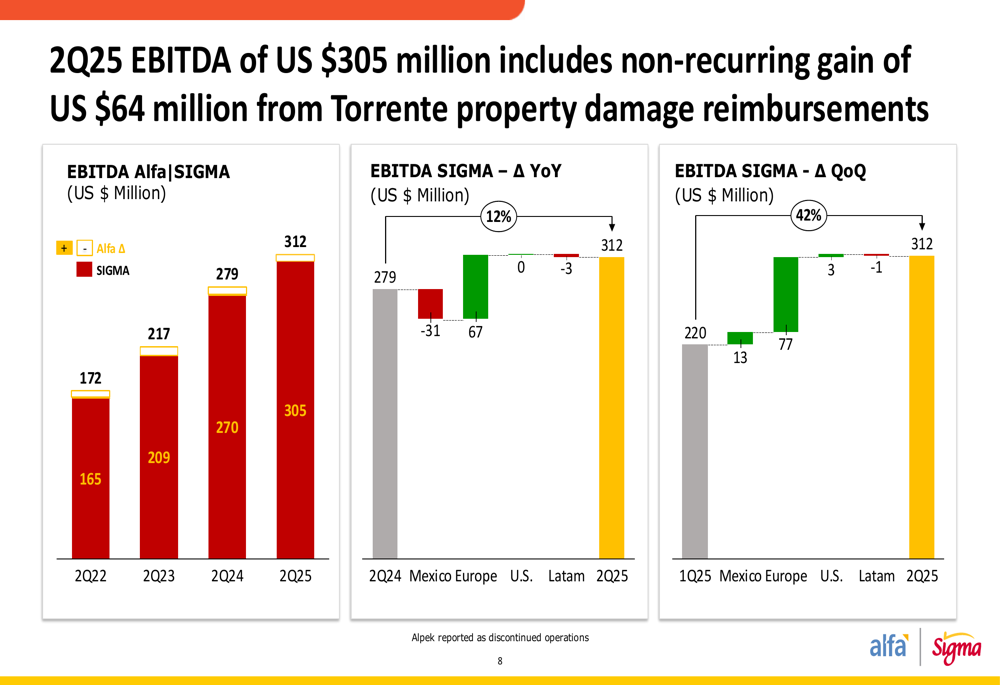

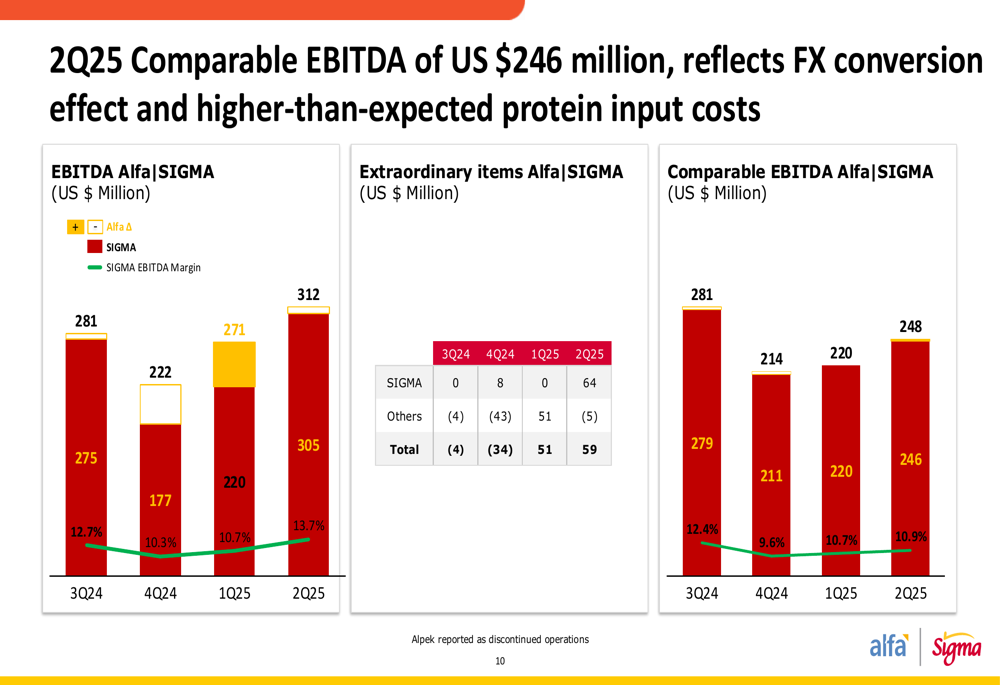

Alfa Sigma reported Q2 2025 EBITDA of $305 million, which includes a non-recurring gain of $64 million from Torrente property damage reimbursements. Year-to-date EBITDA reached $576 million. The company’s performance varied significantly by region, with challenges in Mexico offset by strength in Europe.

The regional breakdown of performance shows:

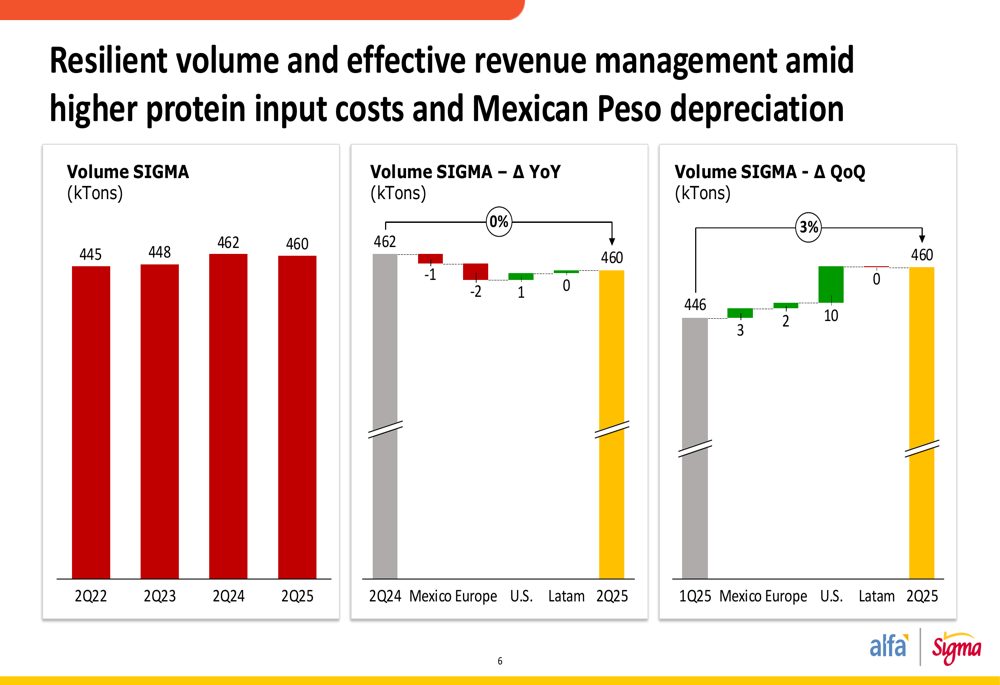

Volume remained resilient at 460 kTons in Q2 2025, showing only a slight decrease from 462 kTons in Q2 2024, despite facing headwinds from higher protein input costs and Mexican Peso depreciation. The quarterly volume increased by 14 kTons compared to Q1 2025, with the U.S. contributing the largest gain of 10 kTons.

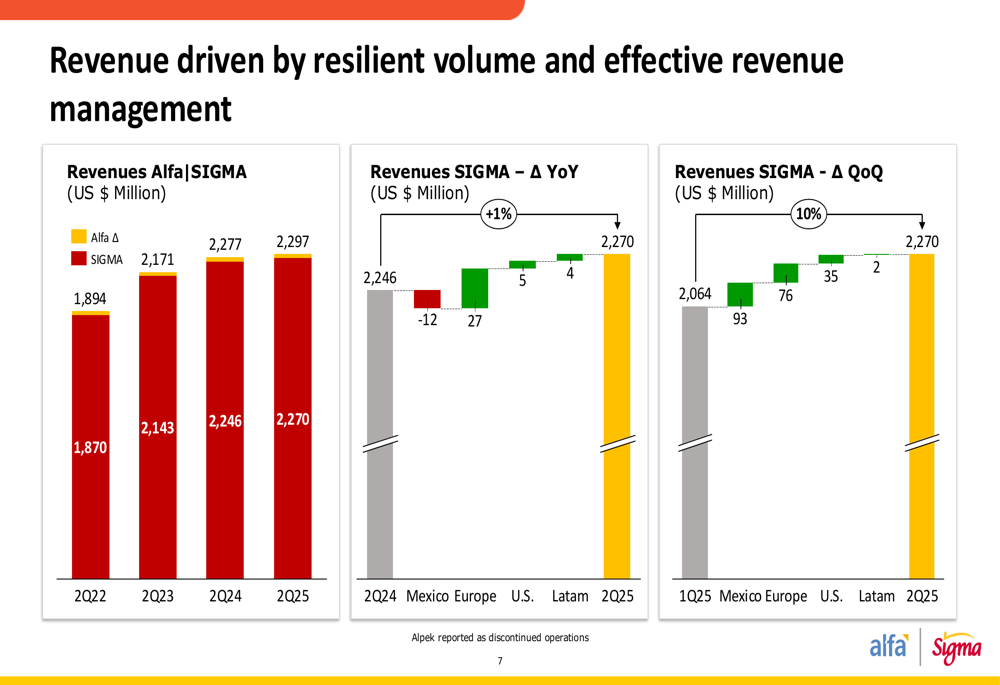

Revenue performance was similarly stable, reaching $2,297 million in Q2 2025, a 1% increase year-over-year. The quarter-on-quarter improvement was more substantial at 10%, with Mexico and Europe leading the growth.

Detailed Financial Analysis

The company’s EBITDA performance shows significant improvement, with Q2 2025 EBITDA of $305 million representing a 13% increase from the $270 million reported in Q2 2024. However, it’s important to note that this includes the $64 million non-recurring gain from insurance reimbursements related to the Torrente facility damage.

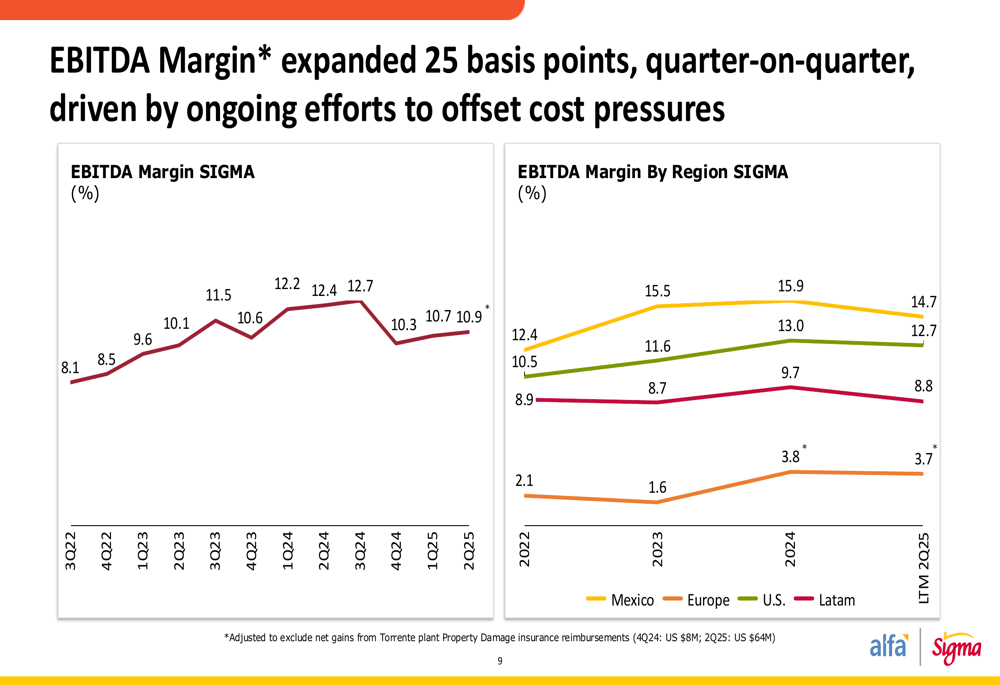

EBITDA margin expansion continued, with a 25 basis points increase quarter-on-quarter, driven by ongoing efforts to offset cost pressures. The margin trends by region show significant variations, with Europe demonstrating the strongest profitability at 15.5% for the last twelve months ending Q2 2025.

When excluding extraordinary items, the comparable EBITDA for Q2 2025 was $246 million, reflecting the impact of FX conversion effects and higher-than-expected protein input costs.

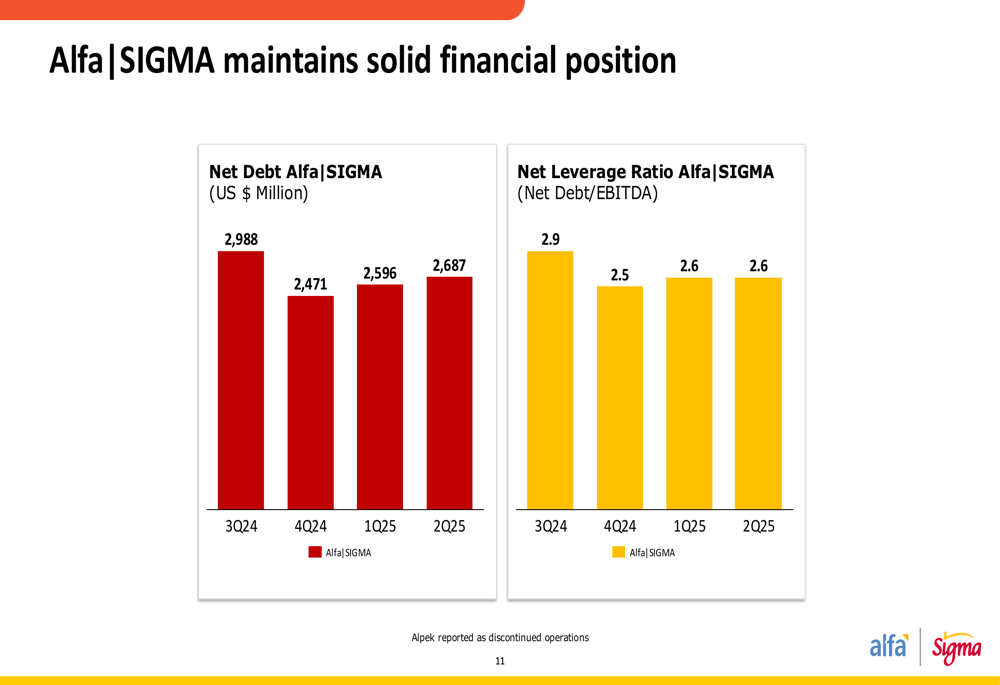

The company maintained a solid financial position with net debt of $2,687 million at the end of Q2 2025, resulting in a net leverage ratio of 2.6x, unchanged from the previous quarter.

The quarter-on-quarter increase in net debt from $2,596 million in Q1 2025 to $2,687 million in Q2 2025 was primarily driven by dividend payments of $84 million, capital expenditures of $61 million, and financial expenses of $64 million, partially offset by the strong EBITDA generation.

Strategic Initiatives

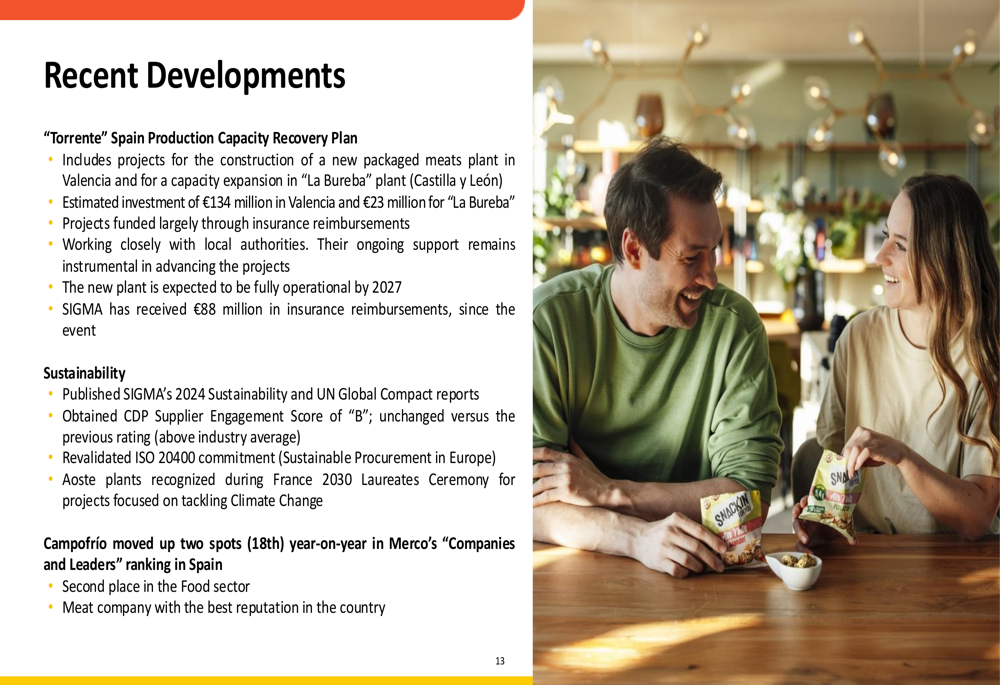

Alfa Sigma outlined its recovery plan for the Torrente facility in Spain, which includes a €134 million investment for a new packaged meats plant in Valencia and a €23 million investment for capacity expansion in the "La Bureba" plant in Castilla y León. The new Valencia plant is expected to be operational by 2027. To date, the company has received €88 million in insurance reimbursements related to the flood damage.

The company also highlighted its sustainability efforts, including the publication of its 2024 Sustainability and UN Global Compact reports, and obtaining a CDP Supplier Engagement Score of "B". Additionally, Campofrío moved up two spots to 18th place in Merco’s "Companies and Leaders" ranking in Spain.

Forward-Looking Statements

Looking ahead, Alfa Sigma faces several challenges, including volatile raw material prices. The presentation included detailed charts showing the trends in pork ham prices in the U.S. and Europe, as well as poultry and dairy raw material prices in the U.S., highlighting the cost pressures the company continues to navigate.

Currency fluctuations also remain a factor, with the Mexican Peso and Euro exchange rates against the U.S. Dollar potentially impacting the company’s financial results going forward.

The company’s focus on effective revenue management and margin expansion suggests a strategic emphasis on profitability amid these challenges. With the corporate transformation now complete, Alfa Sigma is positioned as a dedicated packaged food business with operations across multiple regions, though regional performance variations indicate both opportunities and challenges ahead.

The ongoing recovery efforts in Spain, including significant investments in new production capacity, demonstrate the company’s commitment to long-term growth despite short-term setbacks. As the company moves forward with its rebranding and continues to adapt to changing market conditions, investors will be watching closely to see if the underlying performance can match the headline numbers that were boosted by non-recurring items in Q2 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.