Bubble Wrap maker Sealed Air surges on report of buyout talks

Introduction & Market Context

Alfa Sigma presented its third-quarter 2025 results on October 23, showcasing revenue growth in a challenging cost environment. The company reported an 8% year-over-year revenue increase to $2.39 billion, primarily driven by selective price actions across its markets. However, rising raw material costs, particularly in turkey and other protein categories, put pressure on margins, resulting in a 9% decline in EBITDA compared to the same period last year.

The company operates in a complex global market with varying regional dynamics, facing headwinds from increased input costs while implementing strategic growth initiatives in areas like snacks and sustainability. The presentation highlighted both achievements and challenges across its diverse geographical footprint.

Quarterly Performance Highlights

Alfa Sigma delivered mixed results for Q3 2025, with strong revenue performance offset by margin compression. The company maintained relatively stable sales volumes at 463 kilotons, just slightly below the 465 kilotons reported in Q3 2024, demonstrating resilience in consumer demand despite pricing actions.

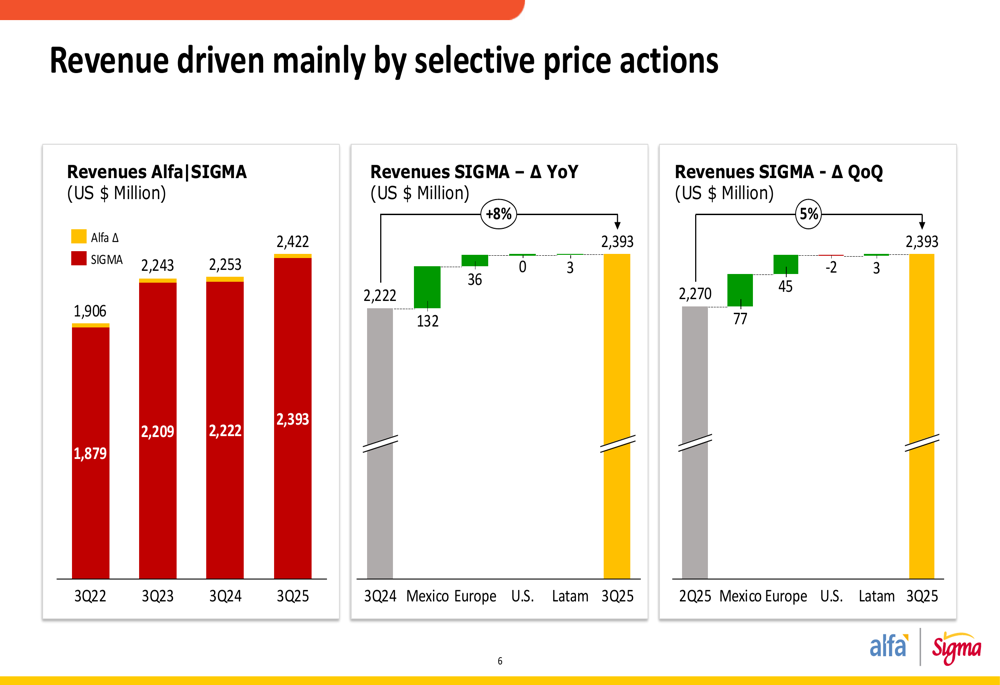

As shown in the following chart of quarterly revenue growth:

Revenue reached $2.39 billion in Q3 2025, representing an 8% increase year-over-year. This growth was primarily driven by Mexico (+$132 million) and Europe (+$36 million), while the U.S. remained flat and Latin America contributed a modest $3 million increase.

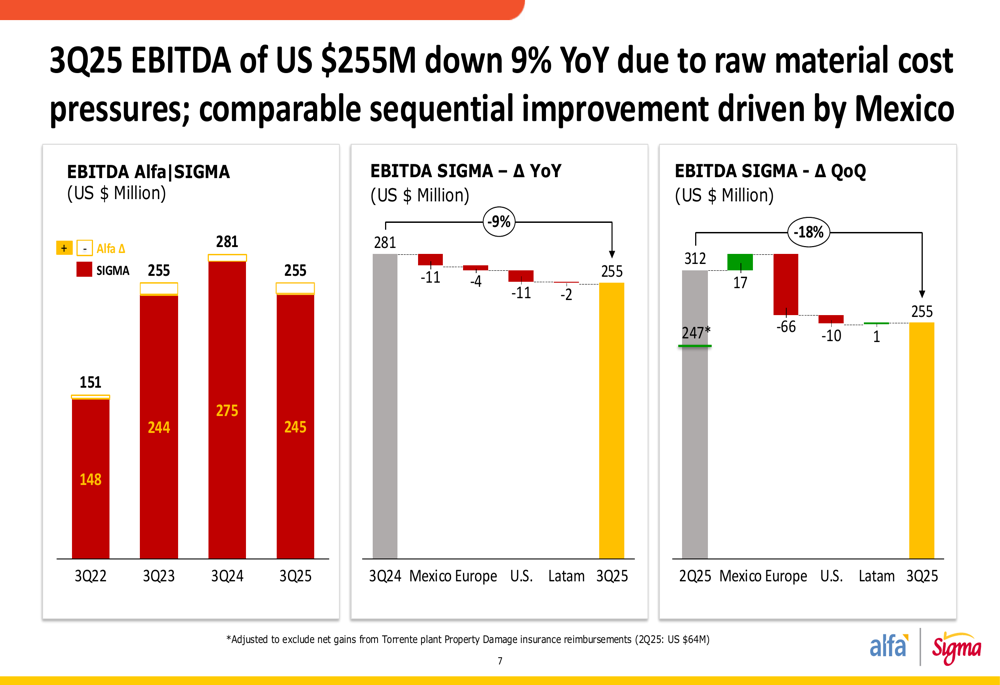

However, EBITDA performance showed a different story:

EBITDA declined 9% year-over-year to $245 million in Q3 2025, down from $275 million in Q3 2024. All regions experienced EBITDA contraction, with Mexico down $11 million, the U.S. down $11 million, Europe down $4 million, and Latin America down $2 million compared to the previous year.

The company’s EBITDA margin has been on a downward trend, as illustrated in this chart:

The overall EBITDA margin decreased to 10.6% in Q3 2025 from 12.7% in Q3 2024, reflecting the impact of higher input costs across all regions.

Regional Performance Analysis

Alfa Sigma’s performance varied significantly across its geographic segments, with each region facing unique challenges and opportunities.

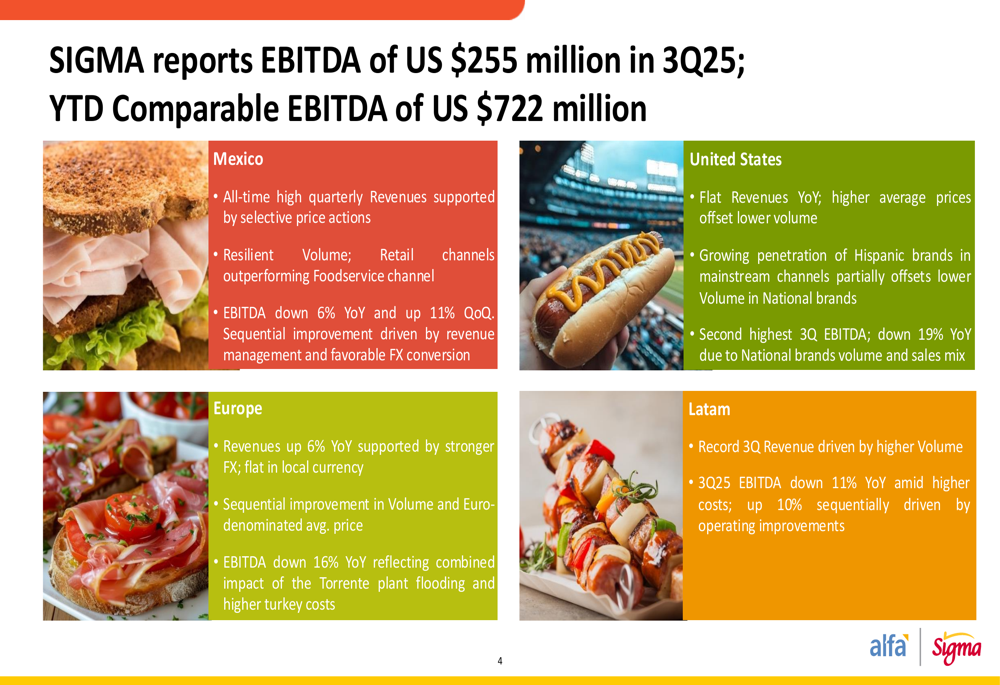

The regional breakdown of performance shows distinct patterns:

In Mexico, the company achieved all-time high quarterly revenues supported by selective price actions. Retail channels outperformed the foodservice channel, with EBITDA down 6% year-over-year but up 11% quarter-over-quarter, showing sequential improvement.

The United States segment reported flat revenues year-over-year, with higher average prices offsetting lower volumes. The company noted growing penetration of Hispanic brands in mainstream channels, which partially offset lower volume in National brands. However, EBITDA was down 19% year-over-year due to National brands volume declines and unfavorable sales mix.

In Europe, revenues increased 6% year-over-year in USD terms, supported by stronger foreign exchange rates, but remained flat in local currency. The region showed sequential improvement in volume and Euro-denominated average prices. EBITDA declined 16% year-over-year, reflecting the combined impact of the Torrente plant flooding and higher turkey costs.

Latin America achieved record third-quarter revenue driven by higher volume, but EBITDA was down 11% year-over-year amid higher costs. The region did show a 10% sequential improvement in EBITDA, driven by operational enhancements.

Financial Position & Outlook

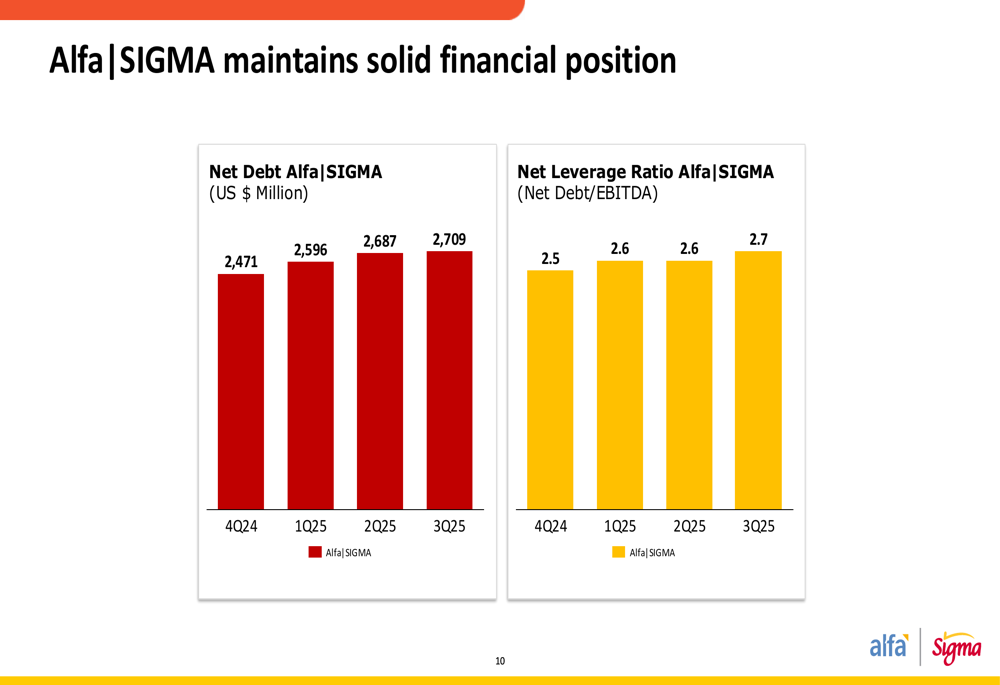

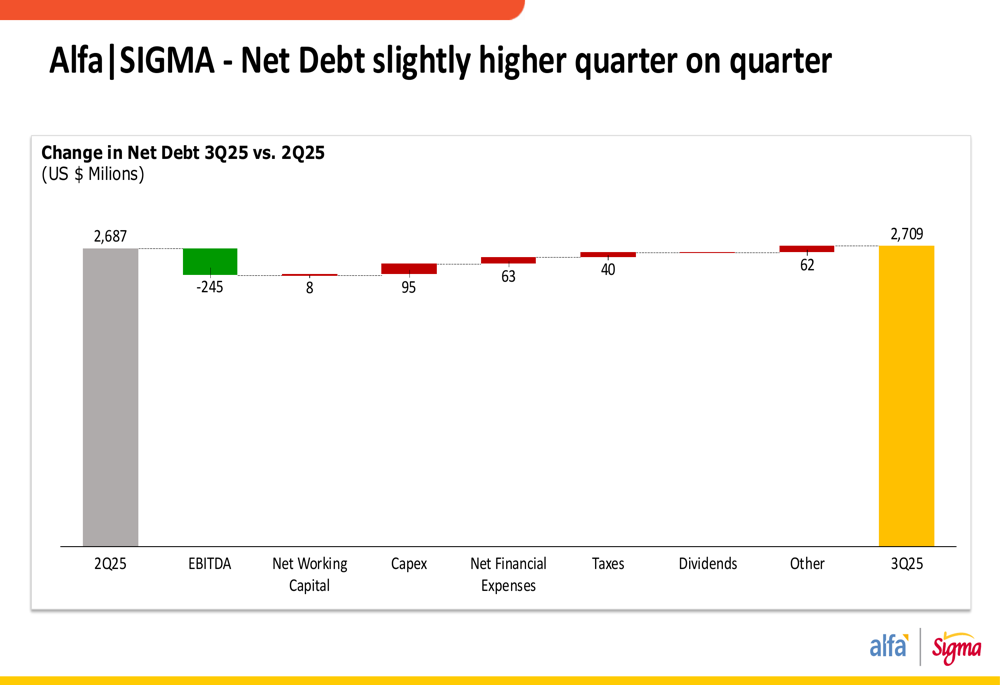

Alfa Sigma’s net debt increased slightly to $2.71 billion in Q3 2025, up from $2.69 billion in the previous quarter. This resulted in a net leverage ratio of 2.7x, compared to 2.6x in Q2 2025.

The following chart illustrates the company’s net debt evolution:

The increase in net debt was primarily driven by capital expenditures, financial expenses, taxes, and dividend payments, partially offset by EBITDA generation, as shown in this waterfall chart:

On a positive note, the company reported refinancing a bank loan 26 months before maturity at a lower spread. The loan is denominated in both USD and MXN, with maturities in 2027 and 2032. Additionally, the Board approved a cash dividend of $35 million, demonstrating confidence in the company’s cash generation capabilities despite current challenges.

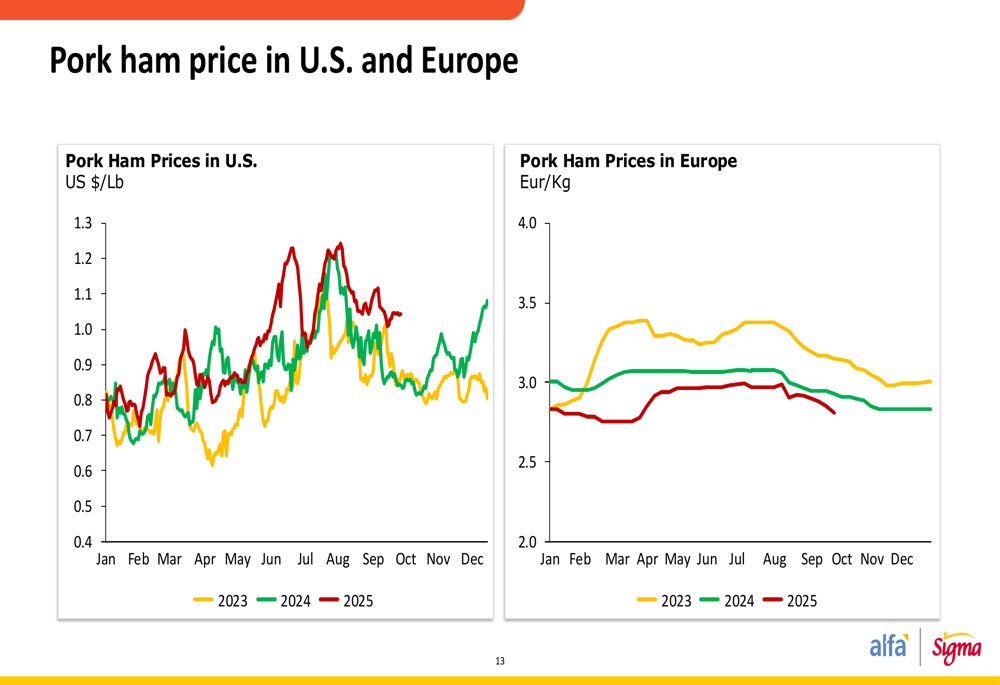

Raw material cost pressures remain a key concern, as evidenced by the rising prices of key inputs:

Pork ham prices have shown significant volatility in both the U.S. and European markets, while poultry raw materials have also experienced upward price trends, particularly turkey breast in Europe, which has impacted the company’s margins.

Strategic Initiatives & Recent Developments

Despite margin pressures, Alfa Sigma continues to invest in growth initiatives and operational improvements. The company’s snacks business unit in Mexico now exceeds 1 million units sold per month, with plans to launch in its first U.S. city in Q4 2025.

The company highlighted progress at SIGMA’s global center of excellence called STUDIO, which has developed 46 physical prototypes and established 11 innovation commitments. This focus on innovation is part of the company’s strategy to differentiate its products in competitive markets.

Sustainability remains a priority, with the company surpassing its 80% goal of raw materials sourced from suppliers with sustainability practices (achieving 81%). Additional environmental initiatives include replacing 95% of fossil fuel-generated energy with biomass in Ecuador and installing 1,520 solar panels at the Imperial site in Belgium. These efforts contributed to an improved S&P CSA rating of 41.

Looking ahead, Alfa Sigma faces continued challenges from raw material cost pressures but appears positioned to leverage its diverse geographical presence and product portfolio to navigate the current environment. The company’s focus on innovation, sustainability, and selective pricing actions suggests a balanced approach to managing growth and profitability in a challenging global market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.