CME glitch; U.S. dollar on pace for weekly fall; Tokyo CPI - what’s moving markets

Algonquin Power & Utilities Corp (NYSE:AQN) reported a substantial decline in earnings for the second quarter of 2025, with net earnings dropping 90% year-over-year, according to the company's earnings presentation delivered on August 8, 2025. Despite the significant decrease, management highlighted strategic initiatives including new rate case filings and leadership appointments as part of its transformation efforts.

Quarterly Performance Highlights

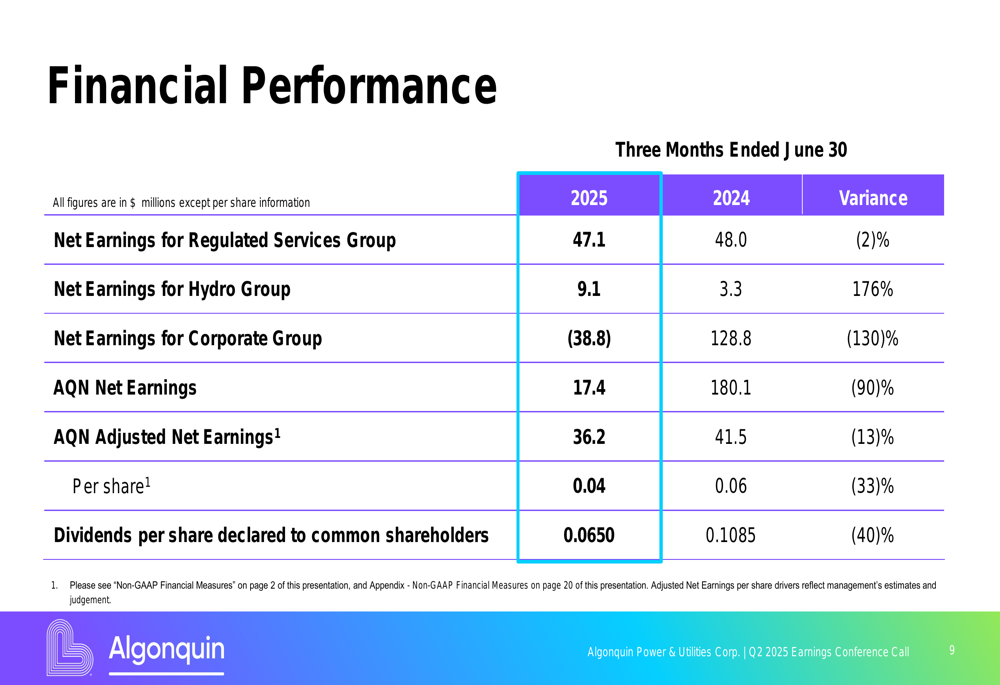

Algonquin's Q2 2025 results showed a dramatic shift from both the previous quarter and year-over-year comparisons. The company reported net earnings of $17.4 million, down 90% from $180.1 million in Q2 2024. Adjusted net earnings, which exclude certain one-time items, came in at $36.2 million, representing a 13% decrease from $41.5 million in the same period last year.

As shown in the following financial performance summary:

On a per-share basis, adjusted net earnings were $0.04, down 33% from $0.06 in Q2 2024. The company also reduced its quarterly dividend to $0.0650 per share, a 40% decrease from $0.1085 in the prior year, reflecting ongoing financial restructuring efforts.

The results represent a significant reversal from Q1 2025, when Algonquin had reported an EPS of $0.14, exceeding market expectations by 55.6%. The stock was trading at $5.92 at the previous close, with premarket activity showing a 1.35% increase to $6.00, suggesting investors may have anticipated even worse results.

Detailed Financial Analysis

The earnings decline was primarily driven by the Corporate Group segment, which posted a loss of $38.8 million compared to earnings of $128.8 million in Q2 2024, representing a 130% negative swing. The Regulated Services Group saw a modest 2% decrease to $47.1 million, while the Hydro Group was a bright spot with earnings of $9.1 million, up 176% from $3.3 million in the prior year.

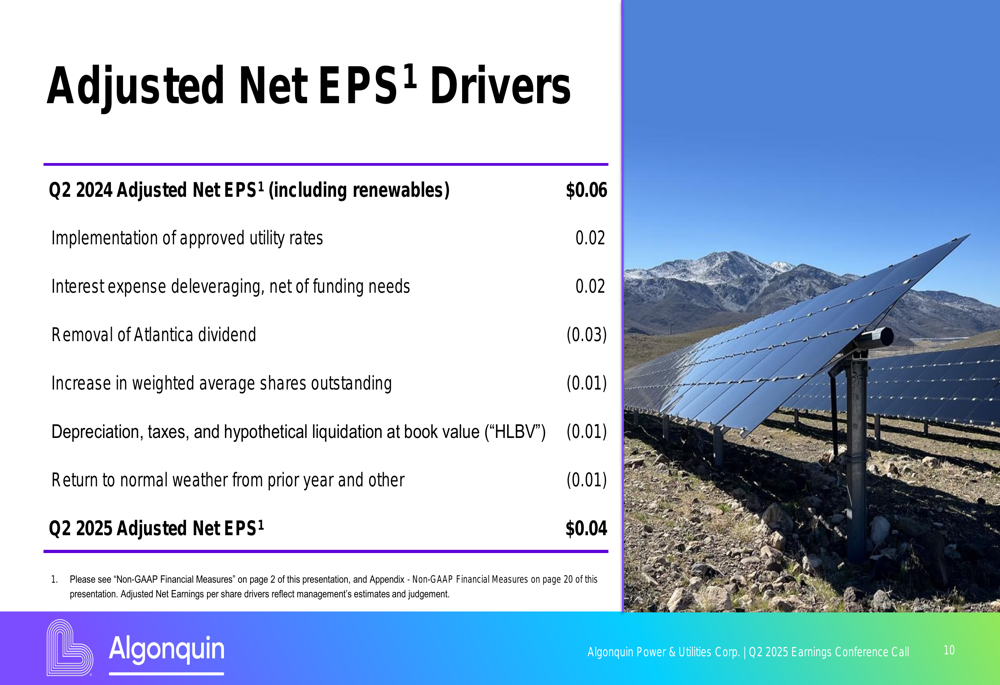

The following chart breaks down the key drivers affecting the company's adjusted earnings per share:

Implementation of approved utility rates and interest expense deleveraging each contributed $0.02 positively to EPS, while the removal of Atlantica dividend reduced EPS by $0.03. Other factors including increased shares outstanding, higher depreciation, and weather normalization collectively reduced EPS by another $0.03.

The company's balance sheet shows total debt of $6.3 billion, with various adjustments including $700 million in equity credit from hybrids and $300 million from Empire securitization.

Strategic Initiatives

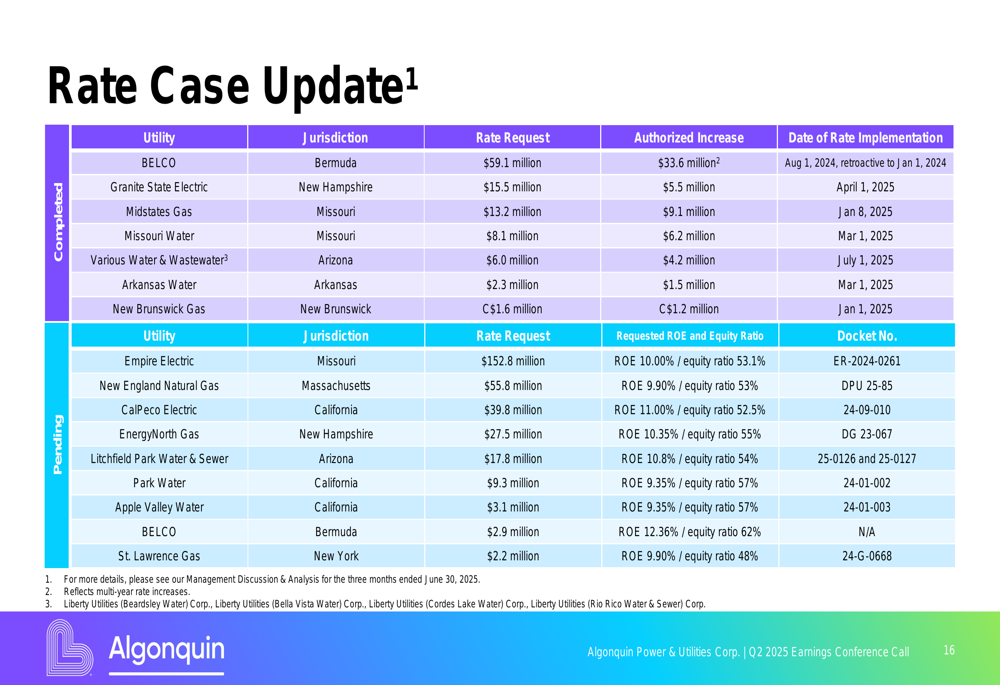

Algonquin highlighted several strategic initiatives aimed at stabilizing performance and positioning for future growth. The company announced new rate case filings in Massachusetts and Arizona, while also noting an approved settlement agreement in Arizona and a filed settlement agreement in New Hampshire.

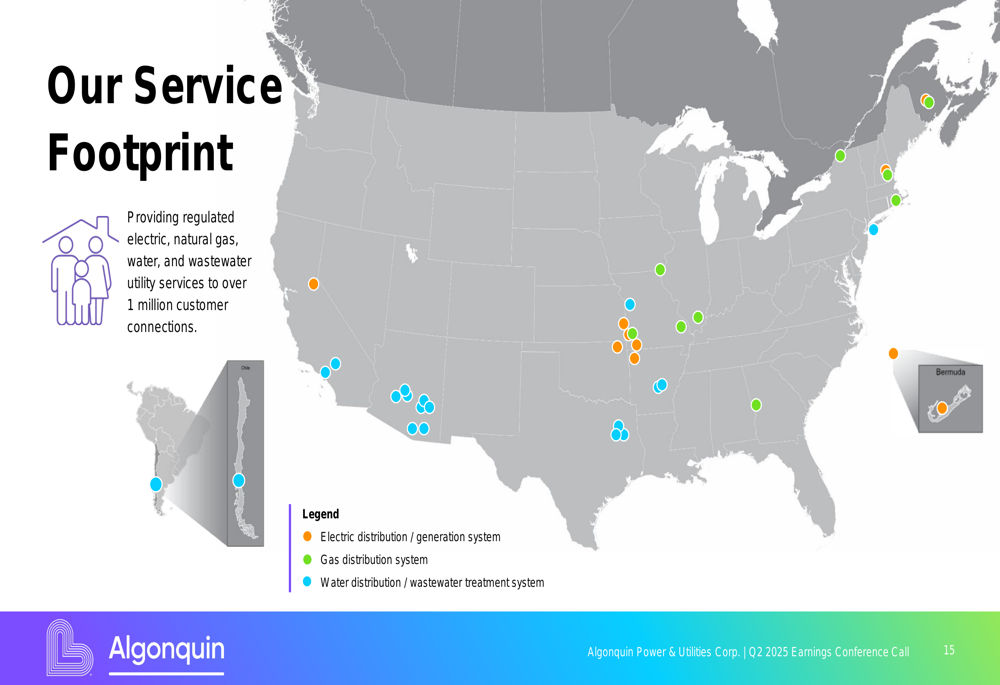

The company's utility operations span multiple jurisdictions across North America, as illustrated in this service footprint map:

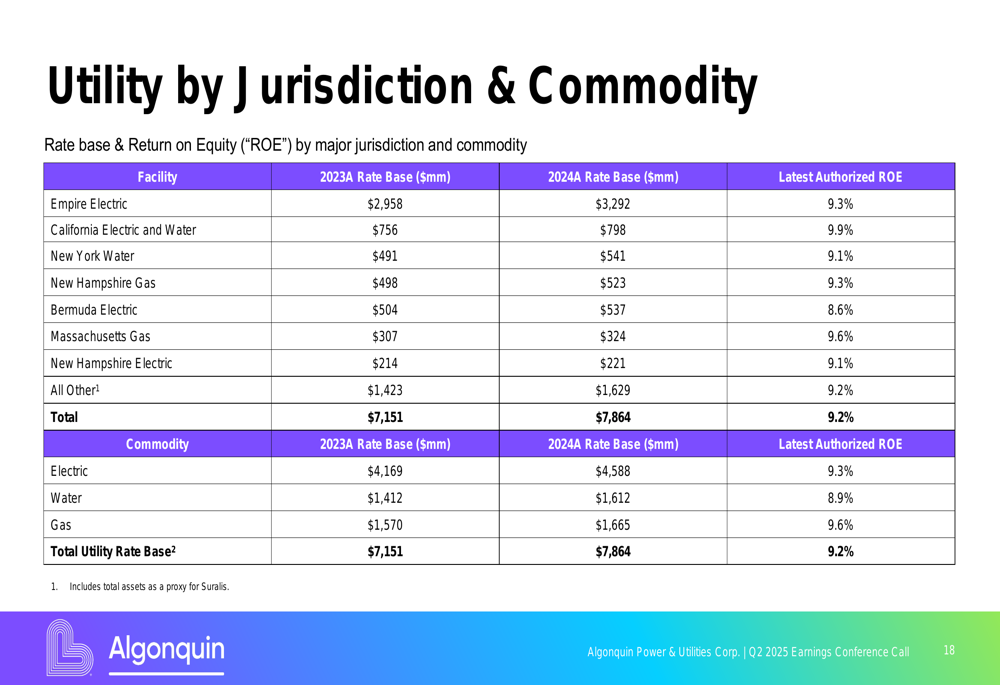

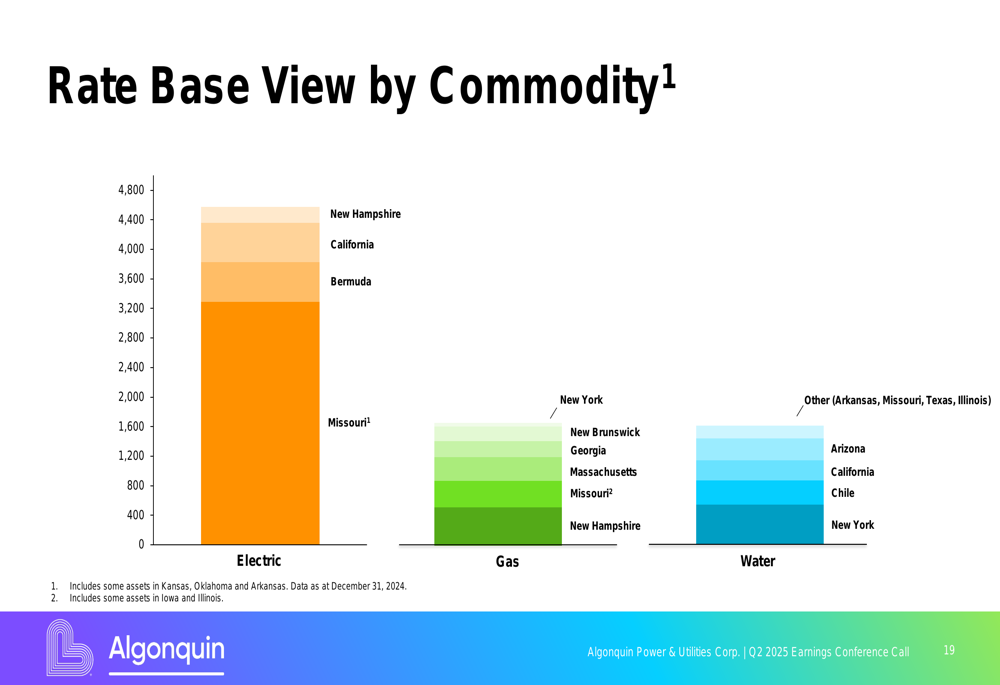

Algonquin's regulated utility business maintains a rate base of $7.86 billion, distributed across electric (58.3%), gas (21.2%), and water (20.5%) services. The company provided a detailed breakdown of its rate base by jurisdiction and commodity:

The company's rate base by commodity shows diversification across multiple jurisdictions, with electric services concentrated in Empire, California, and Bermuda, while gas and water services are spread across multiple regions:

Forward-Looking Statements

Despite the challenging quarter, management emphasized its focus on executing a three-year financial outlook and business plan. The company has strengthened its executive team with new appointments, including Rod West as CEO, Brian Chin as Interim CFO and VP of Investor Relations, and Sarah MacDonald as Chief Transformation Officer.

The company continues to pursue rate case approvals across its service territories, with several pending cases representing significant potential revenue increases:

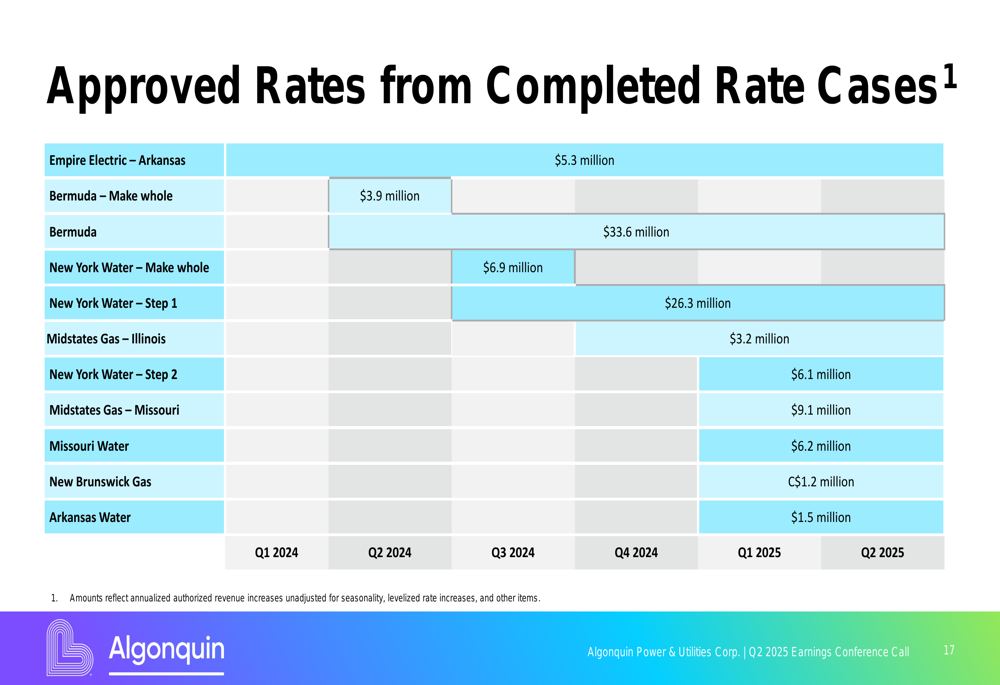

Algonquin has already secured several rate approvals in 2024, including a $33.6 million increase in Bermuda and various other rate implementations across its service territories:

Market Context

The significant earnings decline comes at a challenging time for Algonquin, which had positioned itself as becoming a "premium utility" during its Q1 2025 earnings call. The stock is currently trading below its 52-week high of $6.24 but remains above its 52-week low of $4.19, suggesting investors maintain cautious optimism about the company's transformation efforts.

With a market capitalization of approximately $4.4 billion and 767.9 million shares outstanding, Algonquin faces the challenge of convincing investors that its strategic pivot and rate case initiatives will translate into improved financial performance in upcoming quarters. The company's reduced dividend of $0.26 per share annually (down from the previous level) further underscores the financial pressures it faces as it works to stabilize operations and return to growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.