Bullish indicating open at $55-$60, IPO prices at $37

Executive Summary

Alight Inc (NYSE:ALIT) released its first quarter 2025 earnings presentation on May 8, revealing a 3.5% year-over-year revenue decline to $548 million, with adjusted EBITDA falling 9.9% to $118 million. Despite these challenges, the company highlighted that 92% of its projected full-year revenue is already under contract, and nearly 80% of clients are now leveraging its AI capabilities, up from 62% at the end of 2024.

The company maintained its quarterly dividend of $0.04 per share while repurchasing $20 million of shares during the quarter. Management reaffirmed its full-year 2025 guidance, projecting revenue between $2,318 million and $2,388 million, representing a range of -1.5% to 1.5% growth.

Quarterly Performance Highlights

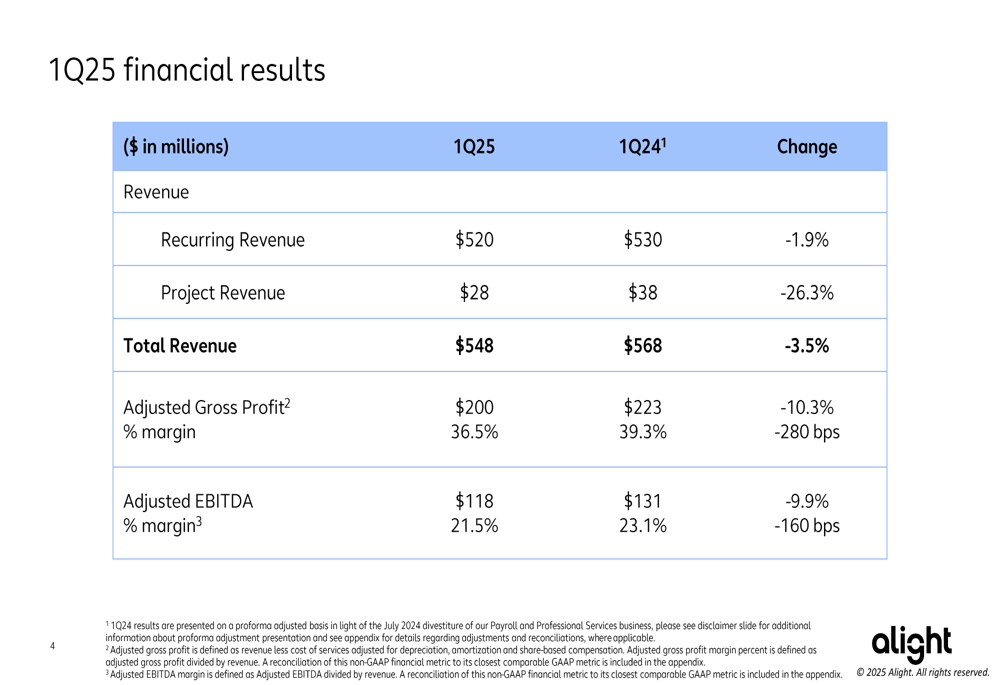

Alight’s Q1 2025 financial results showed mixed performance across key metrics. Recurring revenue, which now comprises 94.9% of total revenue, reached $520 million, down 1.9% from the prior year. Project revenue saw a steeper decline of 26.3%, falling to $28 million.

As shown in the following financial results table:

Profitability metrics also faced pressure, with adjusted gross profit declining 10.3% to $200 million, resulting in a margin contraction of 280 basis points to 36.5%. Similarly, adjusted EBITDA margin fell 160 basis points to 21.5%.

The company noted that these year-over-year comparisons are presented on a proforma adjusted basis to account for the divestiture of the Payroll and Professional Services business in July 2024.

Revenue Drivers and Business Outlook

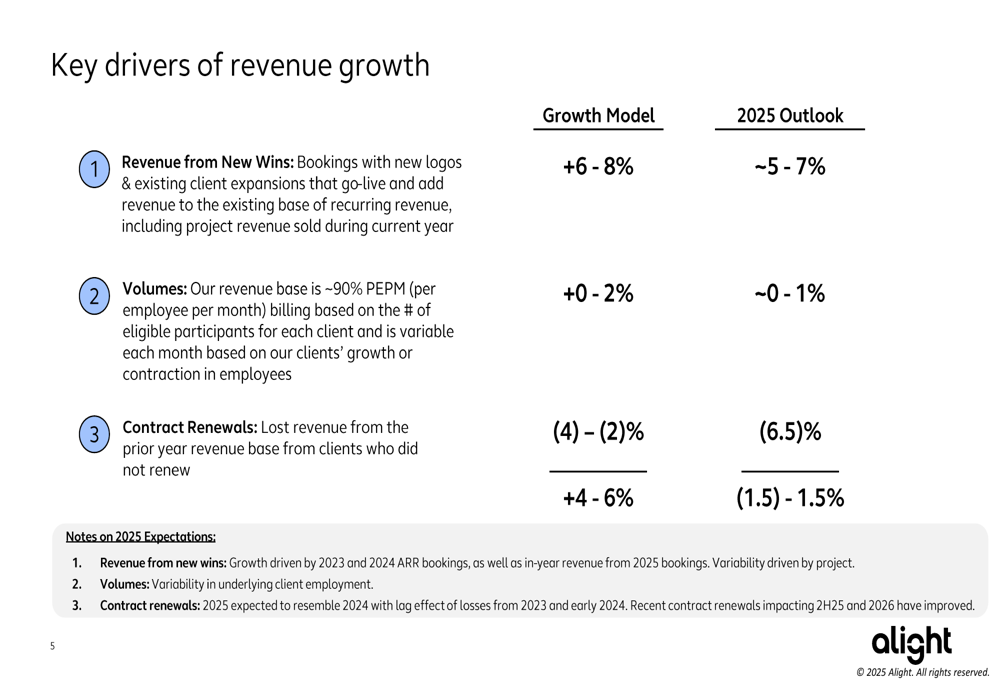

Alight’s presentation broke down the key drivers affecting its revenue growth trajectory, highlighting both structural challenges and opportunities. Contract renewals are expected to create a 6.5% headwind to growth in 2025, significantly more negative than the company’s long-term growth model projection of -2% to -4%.

The following slide details these growth drivers:

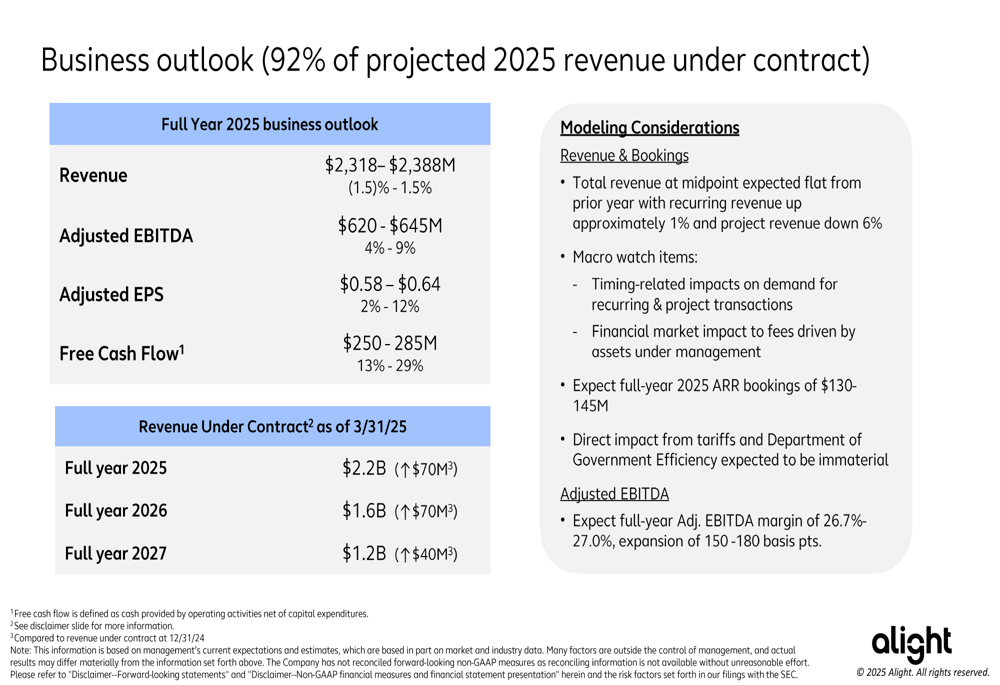

Despite these challenges, Alight maintains a positive outlook for 2025, with 92% of its projected revenue already under contract. The company’s business outlook shows expectations for modest adjusted EBITDA growth of 4-9% and free cash flow growth of 13-29% for the full year.

As illustrated in this comprehensive business outlook:

The company’s revenue under contract has increased across multiple years, with full-year 2025 contracted revenue up by $70 million to $2.2 billion, and 2026 contracted revenue also increasing by $70 million to $1.6 billion.

AI Strategy and Client Adoption

A central theme in Alight’s presentation was its accelerating AI strategy. The company reported that nearly 80% of clients are now leveraging its AI capabilities, a significant increase from 62% at the end of 2024. This rapid adoption rate suggests the company’s technology investments are gaining traction in the market.

Strategic highlights from the quarter include new wins or expanded relationships with major clients including US Foods, Markel (NYSE:MKL), and Delek. The company also launched a self-service reporting platform for Leaves, with AI insights integration planned for the current quarter.

The following strategic highlights slide details these developments:

The company’s focus on AI capabilities appears to be a key differentiator in client retention and expansion efforts, potentially offsetting some of the revenue pressure from contract renewals.

Capital Structure and Shareholder Returns

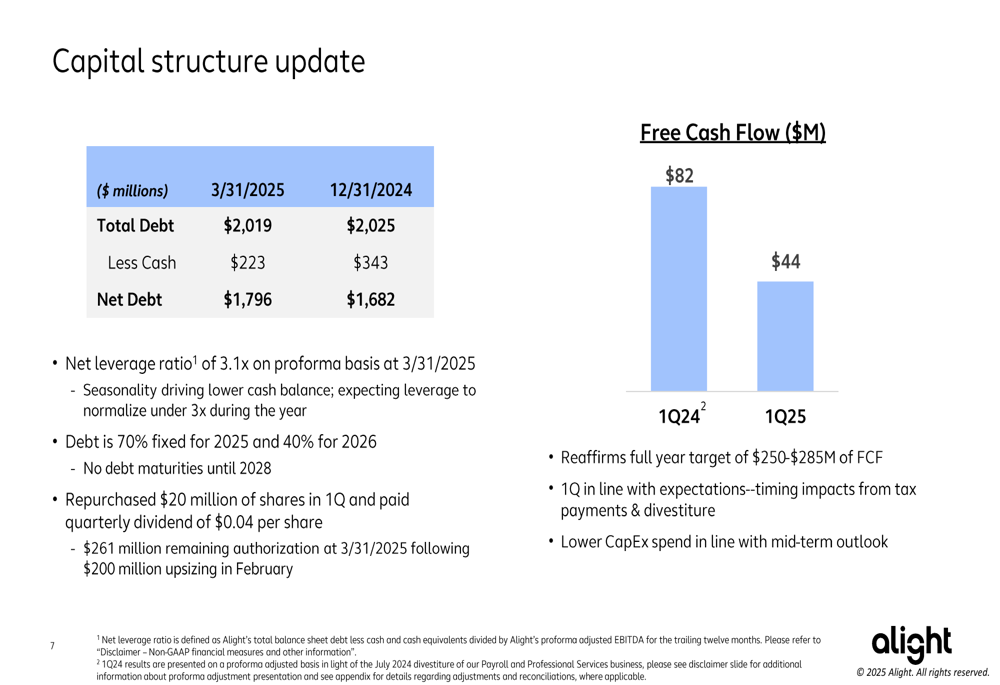

Alight’s capital structure showed some seasonal fluctuations, with net debt increasing to $1,796 million as of March 31, 2025, compared to $1,682 million at the end of 2024. The company’s net leverage ratio stood at 3.1x on a proforma basis.

The following capital structure update provides additional details:

Free cash flow for Q1 2025 was $44 million, down from $82 million in the prior year period. However, management reaffirmed its full-year target of $250-$285 million, attributing the Q1 performance to timing impacts from tax payments and the previous divestiture.

On the positive side, Alight successfully repriced its $2 billion term loan, which is expected to generate interest savings of approximately $10 million on an annualized basis. The company has no debt maturities until 2028, with 70% of its debt fixed for 2025 and 40% for 2026.

Alight continued its shareholder return program, paying a quarterly dividend of $0.04 per share and repurchasing $20 million of shares during the quarter. The company has $261 million remaining in its share repurchase authorization.

Forward-Looking Statements

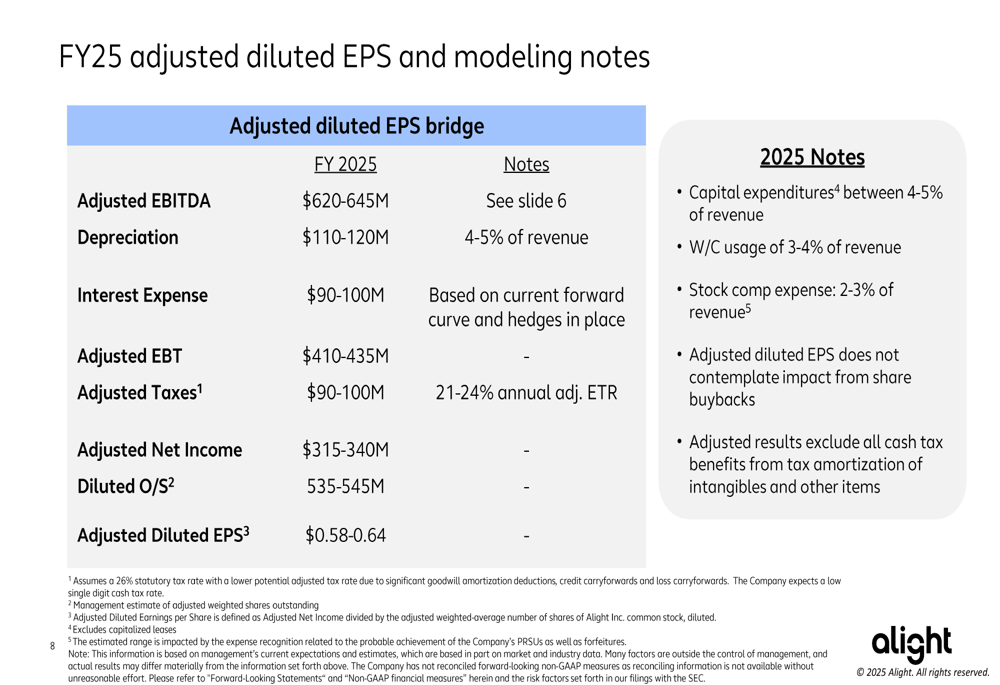

Looking ahead, Alight provided a detailed bridge for its full-year 2025 adjusted diluted EPS guidance of $0.58-$0.64, representing growth of 2-12% year-over-year:

This outlook is supported by the company’s high percentage of contracted revenue and ongoing strategic initiatives. However, investors should note the challenges presented by negative contract renewal impacts and the continued decline in project-based revenue.

Compared to the company’s Q3 2024 performance, where revenue declined by a more modest 0.5% year-over-year, the Q1 2025 results show an accelerating revenue decline. However, the shift toward recurring revenue continues to strengthen, now representing 94.9% of total revenue compared to 91% reported in Q3 2024.

As Alight navigates these challenges, its focus on AI capabilities and high percentage of contracted revenue provide some stability amid market uncertainties. Investors will likely watch closely for signs of stabilization in the company’s revenue trajectory and improvement in margin performance in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.