Hedge funds cut NFLX, keep big bets on MSFT, AMZN, add NVDA

Introduction & Market Context

Alight Inc (NYSE:ALIT) released its second quarter 2025 earnings presentation on August 5, revealing a mixed financial picture that triggered a significant market reaction. The company’s stock plummeted 18.13% following the announcement, closing at $5.14, as investors responded to a substantial $983 million goodwill impairment charge that overshadowed operational improvements. The HR and benefits administration provider reported declining revenue but improved margins and free cash flow generation.

Quarterly Performance Highlights

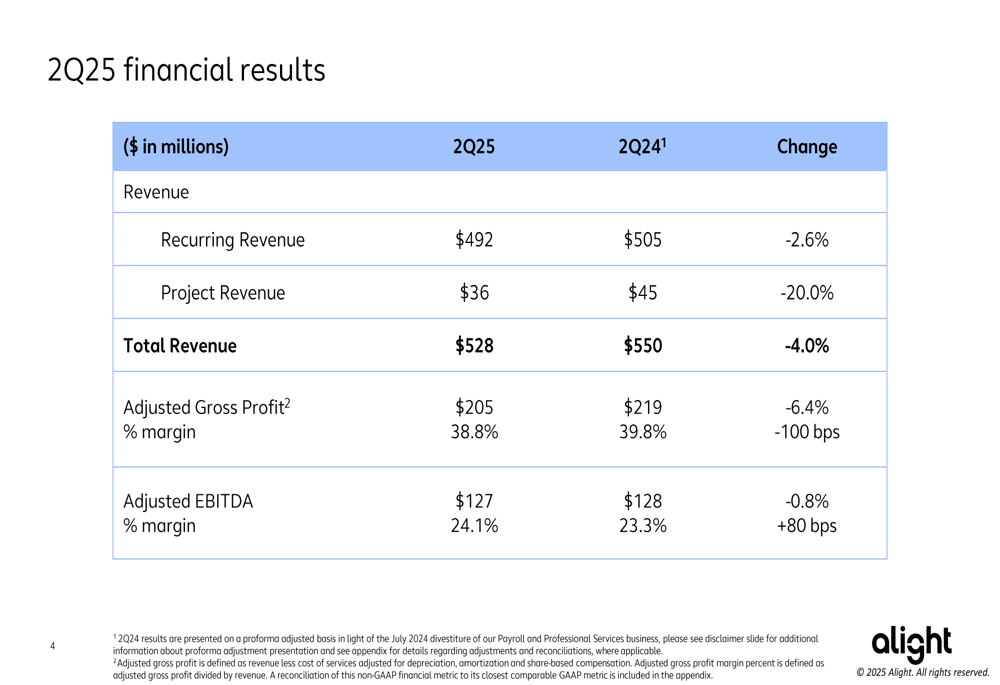

Alight’s Q2 2025 financial results showed total revenue of $528 million, representing a 4.0% year-over-year decline. Recurring revenue, which constituted 93.2% of the total at $492 million, decreased by 2.6% compared to the same period last year. Project revenue saw a more significant drop of 20.0%, coming in at $36 million.

Despite the revenue decline, the company demonstrated margin improvement with Adjusted EBITDA of $127 million, only slightly below the prior year’s $128 million. The Adjusted EBITDA margin expanded by 80 basis points to 24.1%, reflecting enhanced operational efficiency.

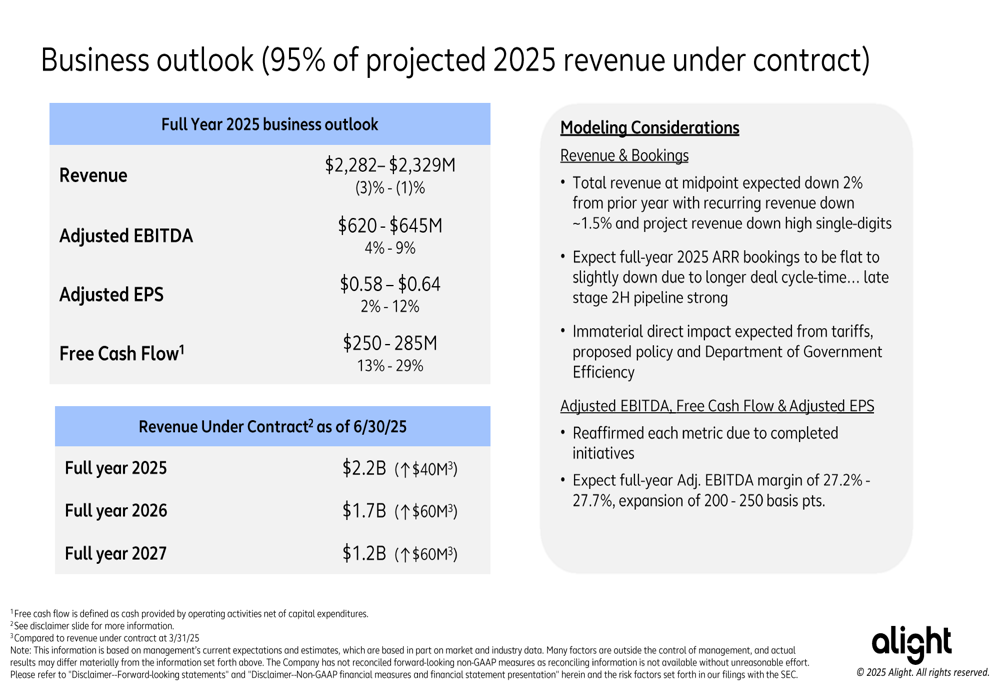

The company highlighted several strategic achievements in the quarter, including new wins and expanded relationships with companies like Thermo Fisher Scientific (NYSE:TMO). Management emphasized that 95% of projected full-year revenue is already under contract, providing visibility for the remainder of 2025.

Detailed Financial Analysis

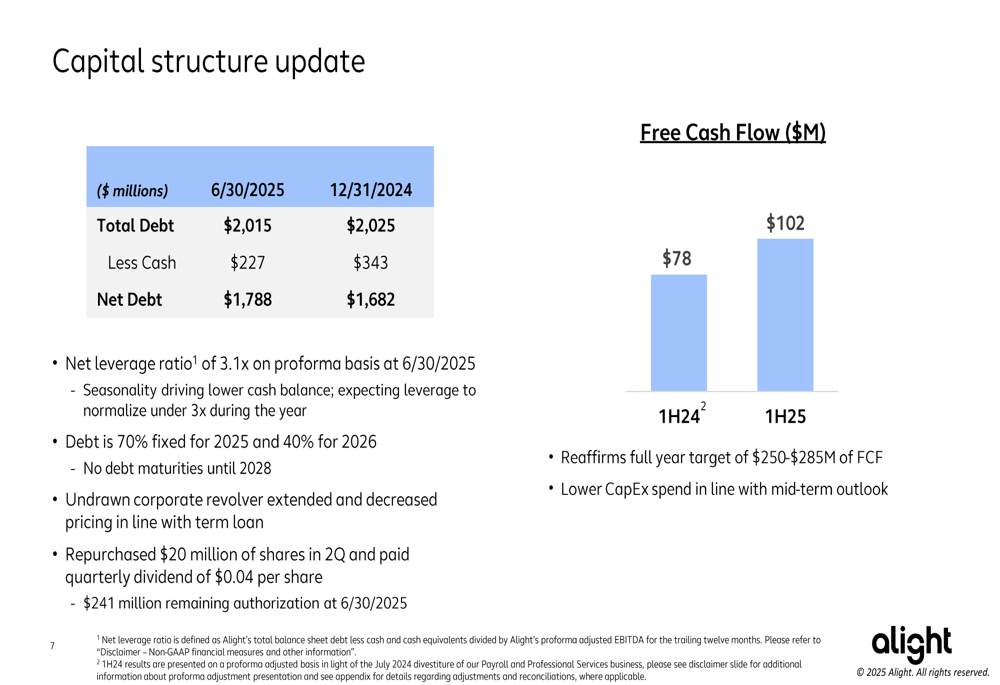

Alight’s adjusted gross profit for the quarter was $205 million, down 6.4% year-over-year, with the margin contracting by 100 basis points to 38.8%. However, the company’s cash flow performance showed significant improvement, with free cash flow for the first half of 2025 increasing by over 30% year-over-year to $102 million.

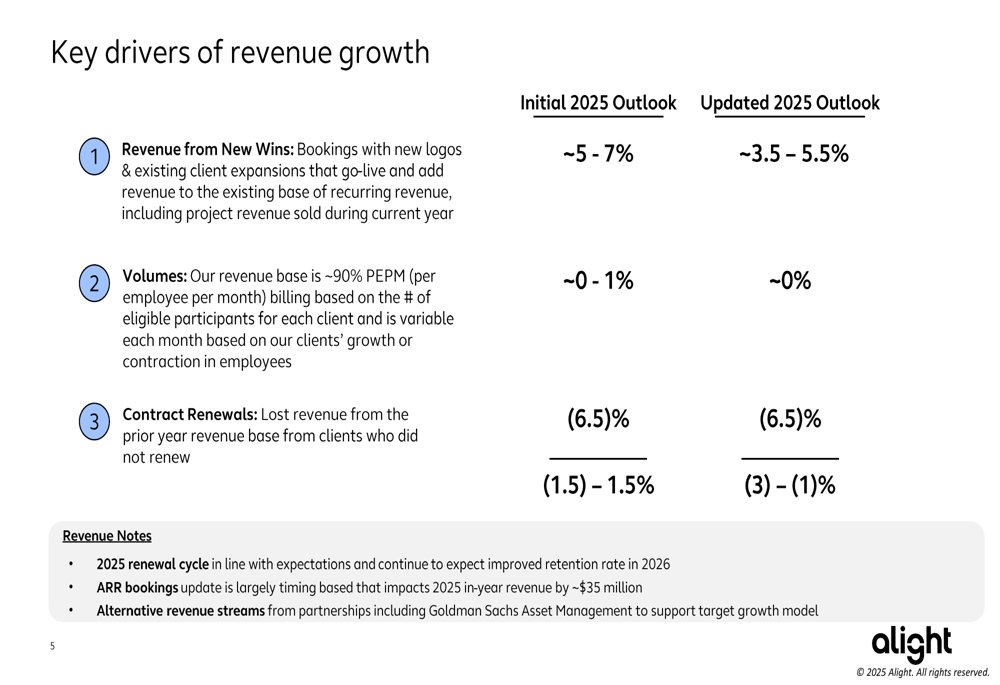

The presentation outlined several key drivers impacting revenue growth, with the company revising its outlook for new wins from an initial 5-7% to approximately 3.5-5.5%. Volume growth was adjusted from 0-1% to flat, while contract renewals remained consistent at -6.5%. These adjustments resulted in an updated overall revenue growth outlook of -3% to -1%, compared to the initial projection of -1.5% to 1.5%.

The company’s capital structure remained relatively stable, with total debt of $2,015 million as of June 30, 2025, slightly down from $2,025 million at the end of 2024. Cash decreased from $343 million to $227 million during the same period, resulting in net debt of $1,788 million and a net leverage ratio of 3.1x.

Strategic Initiatives

Alight continues to advance its AI capabilities, launching Alight Worklife® Insights during the quarter and increasing personalized content generation. The company also internally debuted an AI platform for purchase requisition, demonstrating its commitment to leveraging technology for operational improvements.

The company maintained its shareholder return initiatives, declaring a quarterly dividend of $0.04 per share and repurchasing $20 million of shares during the quarter, with $241 million remaining in the authorization.

However, the earnings call transcript revealed that the significant goodwill impairment charge of $983 million was a major concern for investors. This charge, while mentioned in the reconciliation tables of the presentation, was not prominently featured in the main slides, potentially contributing to the negative market reaction.

Forward-Looking Statements

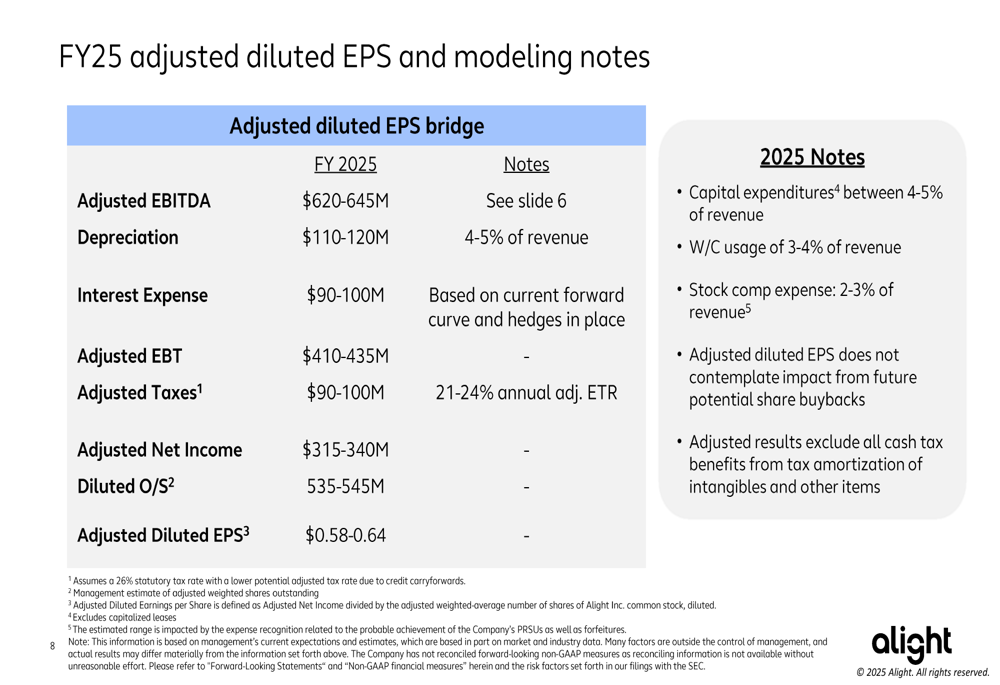

Alight provided a business outlook for the full year 2025, projecting revenue of $2,282-$2,329 million, representing a decline of 1-3%. The company expects Adjusted EBITDA to grow by 4-9% to $620-$645 million, with Adjusted EPS of $0.58-$0.64 (up 2-12%) and Free Cash Flow of $250-285 million (up 13-29%).

The company also shared its adjusted diluted EPS bridge for FY25, breaking down the components from Adjusted EBITDA to the final EPS figure. Capital expenditures are expected to be between 4-5% of revenue, with working capital usage of 3-4% of revenue.

CEO Dave Gilmette emphasized the company’s strategic progress in the earnings call, stating, "We are making strategic progress to accelerate our client management and delivery capabilities through AI, automation, and partnerships." CFO Jeremy Heaton highlighted the focus on execution, noting, "We are intensely focused on execution and improving our top line performance while continuing to drive greater margin expansion and cash flow."

Despite the positive operational narrative presented in the slides, the market’s negative reaction suggests investors remain concerned about the goodwill impairment and its implications for Alight’s valuation. With the stock trading near its 52-week low, analyst price targets ranging from $8 to $11 indicate potential upside if the company can execute on its strategic initiatives and improve top-line performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.