Missed the webinar? Here are Investing.com’s top 10 stock picks for 2026

Introduction & Market Context

Alithya Group (OTC:ALYAF) Inc. (NASDAQ:ALYA) presented its fourth quarter fiscal 2025 results on June 12, 2025, highlighting record profitability metrics and strategic growth initiatives. The company’s stock has responded positively to these results, with shares trading at $2.19, up 5.29% following the earnings announcement, and approaching its 52-week high of $2.31.

The IT consulting firm delivered a strong quarter marked by record gross margins and net earnings, demonstrating the success of its focus on higher-value services and operational efficiencies. This performance comes amid a broader industry trend of digital transformation and growing demand for AI-enabled solutions.

Quarterly Performance Highlights

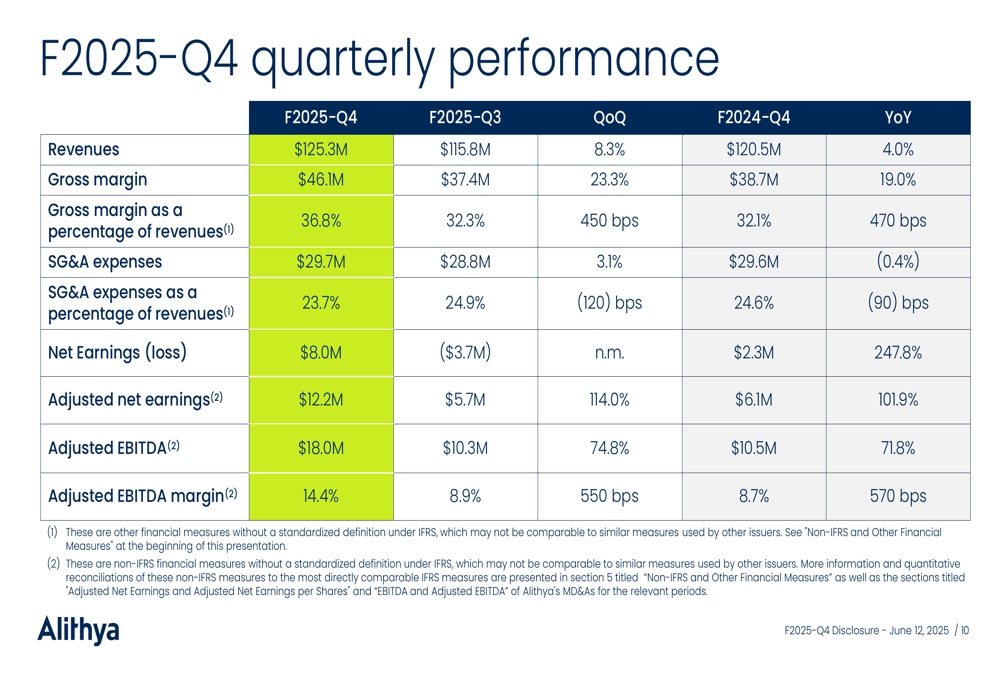

Alithya reported revenues of $125.3 million for Q4 F2025, representing an 8.3% increase quarter-over-quarter and a 4.0% increase year-over-year. More impressively, the company achieved record gross margin of 36.8%, a significant improvement of 450 basis points sequentially and 470 basis points year-over-year.

As shown in the comprehensive quarterly performance comparison below, Alithya demonstrated improvements across virtually all key financial metrics:

Net earnings reached $8.0 million, compared to a loss of $3.7 million in the previous quarter and representing a 247.8% increase from the $2.3 million reported in Q4 F2024. Adjusted EBITDA climbed to $18.0 million, up 74.8% quarter-over-quarter and 71.8% year-over-year, with the adjusted EBITDA margin expanding to 14.4% from 8.9% in Q3 F2025 and 8.7% in Q4 F2024.

The company’s long-term performance trends illustrate the consistent improvement in gross margin percentage and the recent acceleration in profitability:

Strategic Initiatives

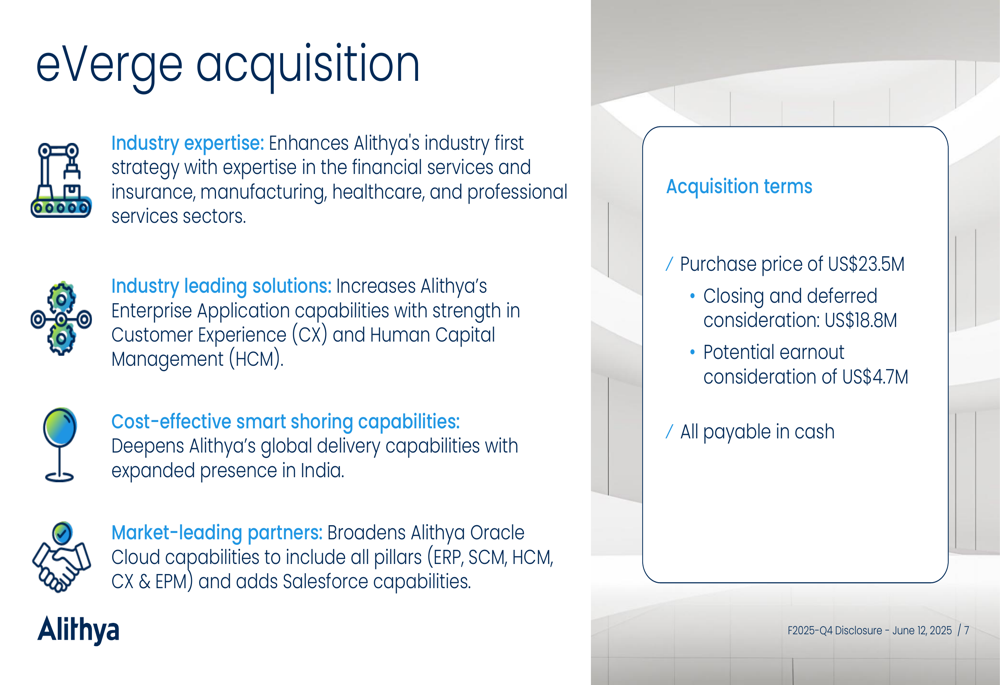

A key strategic development during the quarter was Alithya’s acquisition of eVerge, a U.S.-based boutique consultancy specializing in Oracle (NYSE:ORCL), Salesforce (NYSE:CRM), and AI solutions. This acquisition strengthens Alithya’s industry-first strategy and expands its capabilities across multiple platforms.

The acquisition details reveal a purchase price of US$23.5 million, comprising US$18.8 million in closing and deferred consideration plus a potential earnout of US$4.7 million, all payable in cash:

This strategic move enhances Alithya’s industry expertise in financial services, insurance, manufacturing, healthcare, and professional services sectors. It also broadens the company’s Oracle Cloud capabilities to include all pillars (ERP, SCM, HCM, CX & EPM) while adding Salesforce capabilities to its portfolio.

Additionally, the acquisition deepens Alithya’s global delivery capabilities with an expanded presence in India, supporting its cost-effective smart shoring strategy.

Operational Achievements

Alithya’s operational highlights for Q4 F2025 demonstrate its commitment to quality delivery and innovation. The company reported an impressive customer satisfaction score of 9.0 out of 10 based on 194 surveys conducted during fiscal 2025, underscoring its strong client relationships.

The company received industry recognition through the 2024-2025 Microsoft (NASDAQ:MSFT) Inner Circle award for Business Applications for the 19th time, reinforcing its position as a leading Microsoft partner. Alithya also secured multiple AI enablement engagements for M365 Copilot Tech Readiness, Deployment, and Adoption Services, reflecting its growing capabilities in artificial intelligence solutions.

Financial Position

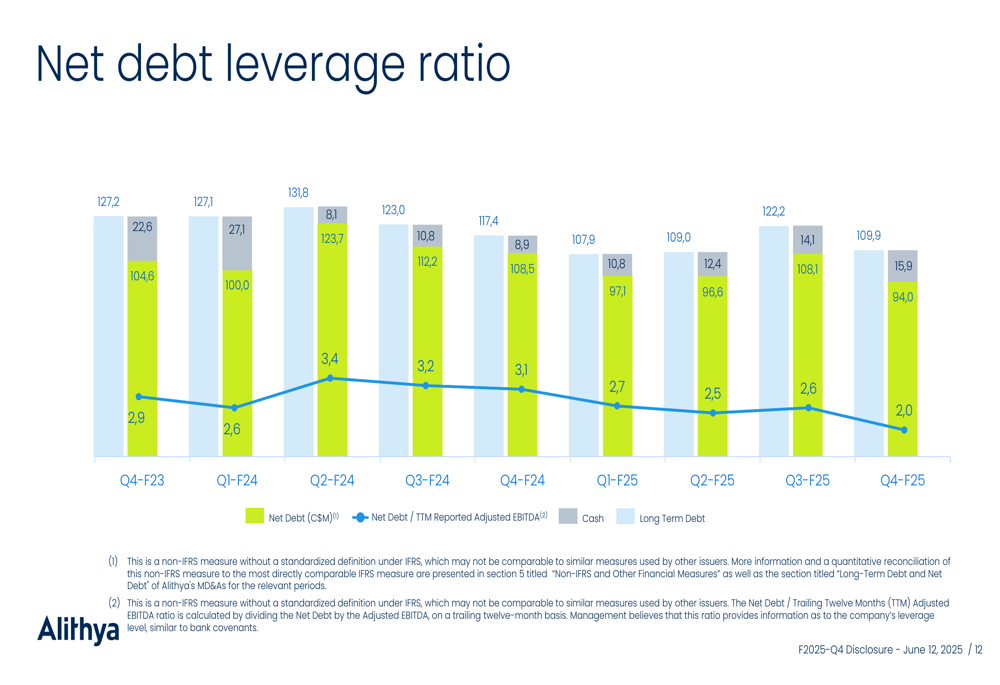

Alithya has made significant progress in strengthening its financial position, with a focus on deleveraging to support future M&A activities. The company’s net debt leverage ratio improved to 2.0x trailing twelve-month adjusted EBITDA in Q4 F2025, down from 2.6x in the previous quarter and 3.1x in Q4 F2024.

The chart below illustrates the company’s consistent reduction in net debt over the past year, alongside improvements in cash position:

This improved financial flexibility positions Alithya well for its continued acquisition strategy, focusing on higher-margin complementary businesses that can enhance its service offerings and geographic reach.

Forward Outlook

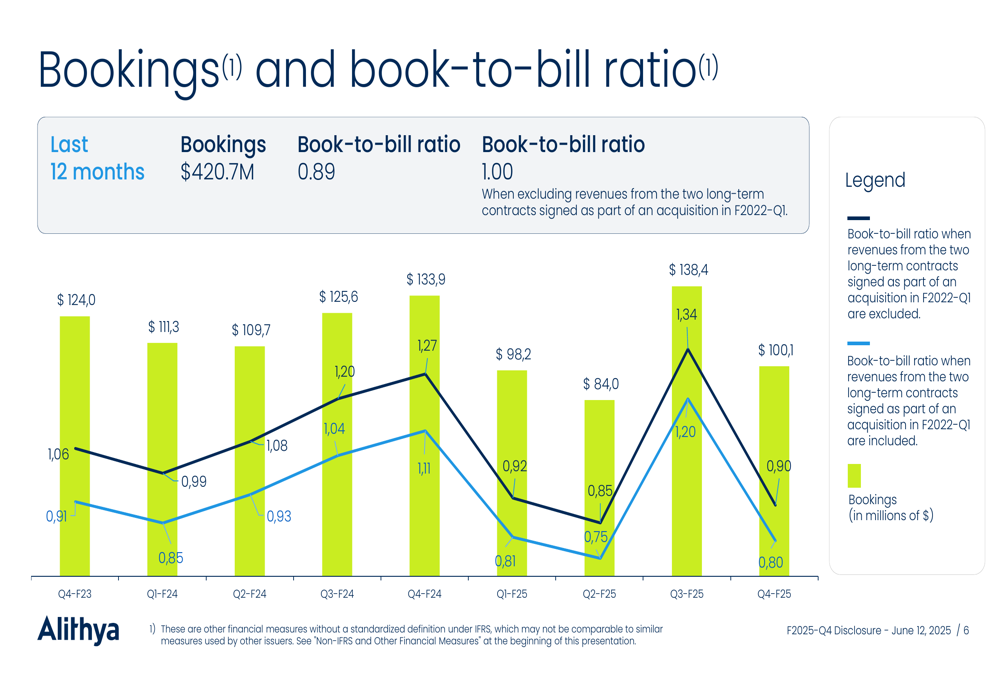

Looking ahead, Alithya’s bookings and book-to-bill ratio provide insights into its future revenue potential. For the last 12 months, the company reported bookings of $420.7 million with a book-to-bill ratio of 0.89, or 1.00 when excluding revenues from two long-term contracts signed as part of an acquisition in Q1 F2022.

The quarterly breakdown of bookings shows some fluctuation, with a particularly strong Q3 F2025 followed by a more moderate Q4:

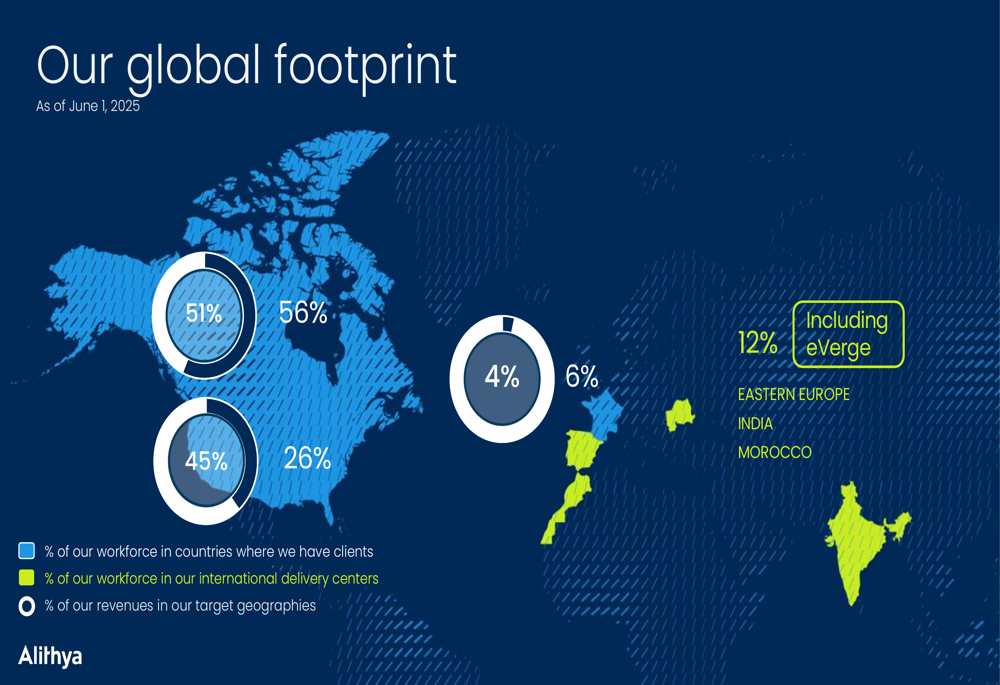

Alithya’s global footprint continues to evolve, with 56% of its workforce now in North America, 4% in Europe, and a growing presence in India that reaches 12% including the eVerge acquisition. This geographic diversification supports the company’s ability to deliver services efficiently while maintaining proximity to clients.

Executive Summary

Alithya’s Q4 F2025 results represent a significant milestone in the company’s journey toward sustainable profitability and growth. The record gross margins and earnings demonstrate the success of management’s focus on higher-value services and operational efficiency. The strategic acquisition of eVerge strengthens Alithya’s capabilities in key technology platforms and expands its global delivery model.

With a stronger balance sheet and improved profitability metrics, Alithya appears well-positioned to continue its disciplined growth strategy through both organic initiatives and strategic acquisitions. The company’s focus on AI enablement and multi-platform expertise aligns well with current market demands for digital transformation and intelligent automation solutions.

As CEO Paul Raymond (NSE:RYMD) noted in the earnings call, "AI is not going to replace people, people who use AI are going to replace people," highlighting the company’s pragmatic approach to integrating artificial intelligence into its service offerings and client solutions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.