Microsoft sued by Australia competition regulator over Copilot, 365 pricing

Allegion plc (NYSE:ALLE) reported solid second-quarter results and raised its full-year outlook during its earnings presentation on July 24, 2025. The security products manufacturer posted revenue growth of 5.8% and announced several strategic acquisitions while increasing its adjusted EPS guidance for the year.

Quarterly Performance Highlights

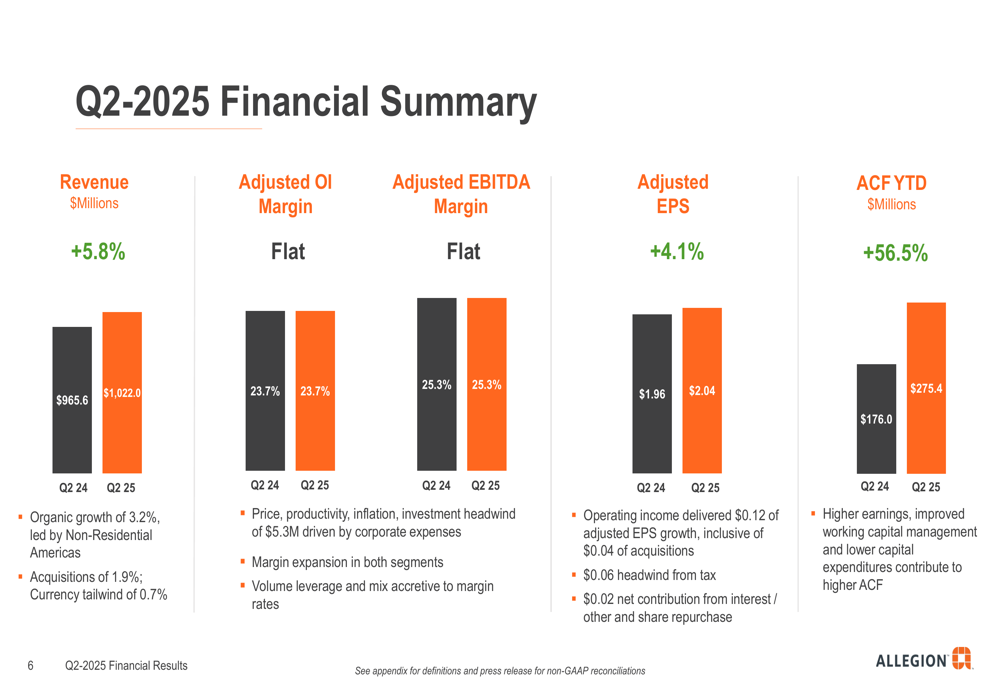

Allegion reported Q2 2025 revenue of $1,022.0 million, a 5.8% increase from $965.6 million in the same period last year. Organic growth contributed 3.2%, acquisitions added 1.9%, and currency provided a 0.7% tailwind. Adjusted earnings per share rose 4.1% to $2.04, compared to $1.96 in Q2 2024.

The company maintained stable profitability with adjusted operating income margin and adjusted EBITDA margin both flat year-over-year at 23.7% and 25.3%, respectively. Volume leverage and favorable mix helped offset investment headwinds.

As shown in the following financial summary:

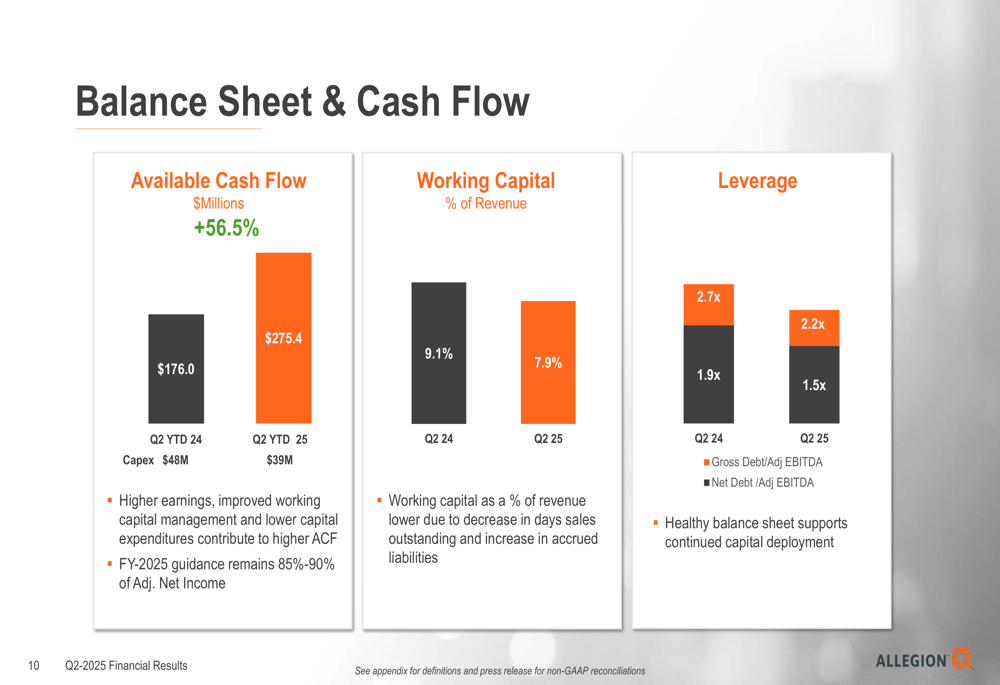

Available cash flow saw a significant improvement, increasing 56.5% year-to-date to $275.4 million, driven by higher earnings, improved working capital management, and lower capital expenditures. Working capital as a percentage of revenue improved from 9.1% to 7.9%.

Segment Analysis

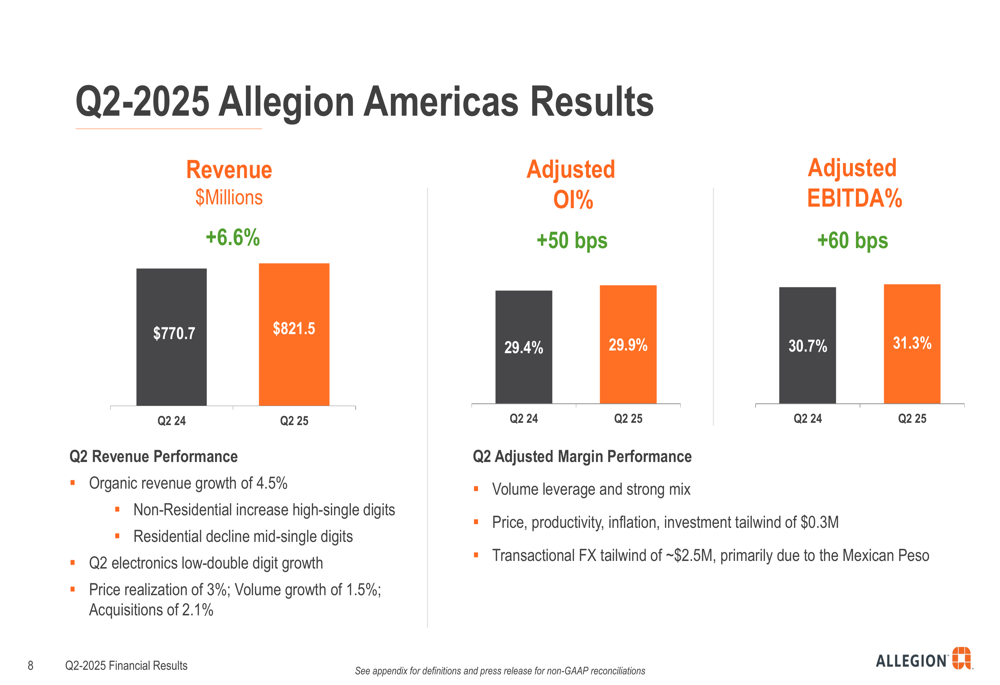

Allegion’s Americas segment, which accounts for approximately 80% of total revenue, delivered 6.6% growth to $821.5 million. Organic growth in this segment reached 4.5%, with non-residential markets showing high single-digit growth, partially offset by mid-single-digit declines in residential markets. Electronics continued its strong performance with low-double-digit growth.

The segment’s adjusted operating income margin improved by 50 basis points to 29.9%, while adjusted EBITDA margin increased 60 basis points to 31.3%.

The Americas segment performance is illustrated here:

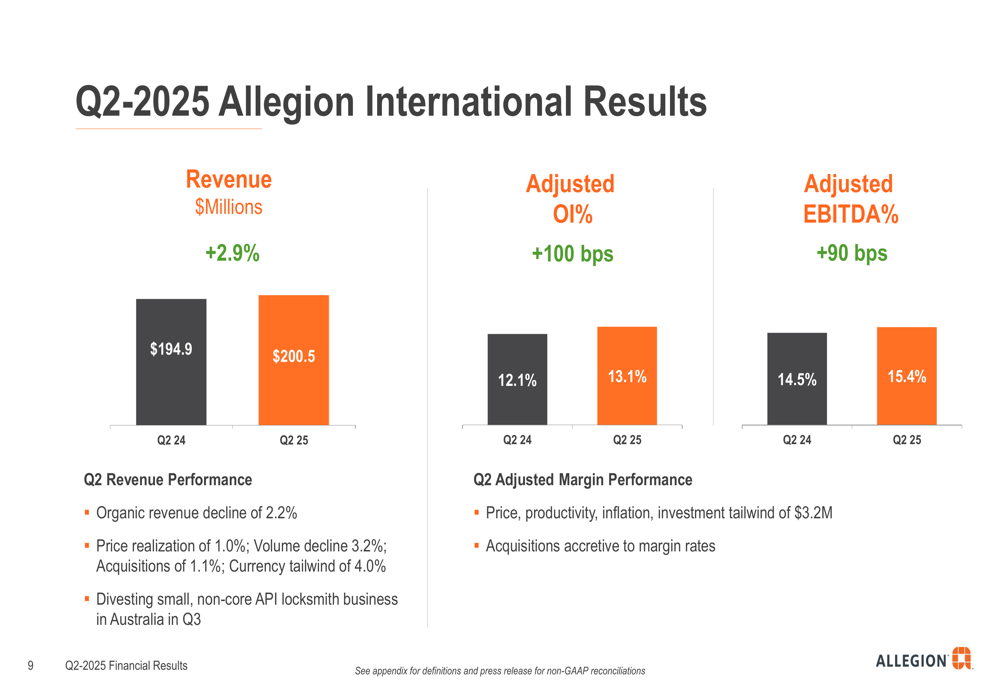

The International segment reported revenue of $200.5 million, up 2.9% from the prior year, though organic revenue declined 2.2%. Despite volume challenges, the segment improved its adjusted operating income margin by 100 basis points to 13.1%, benefiting from price realization, productivity improvements, and accretive acquisitions.

The following chart details the International segment results:

Strategic Acquisitions & Capital Allocation

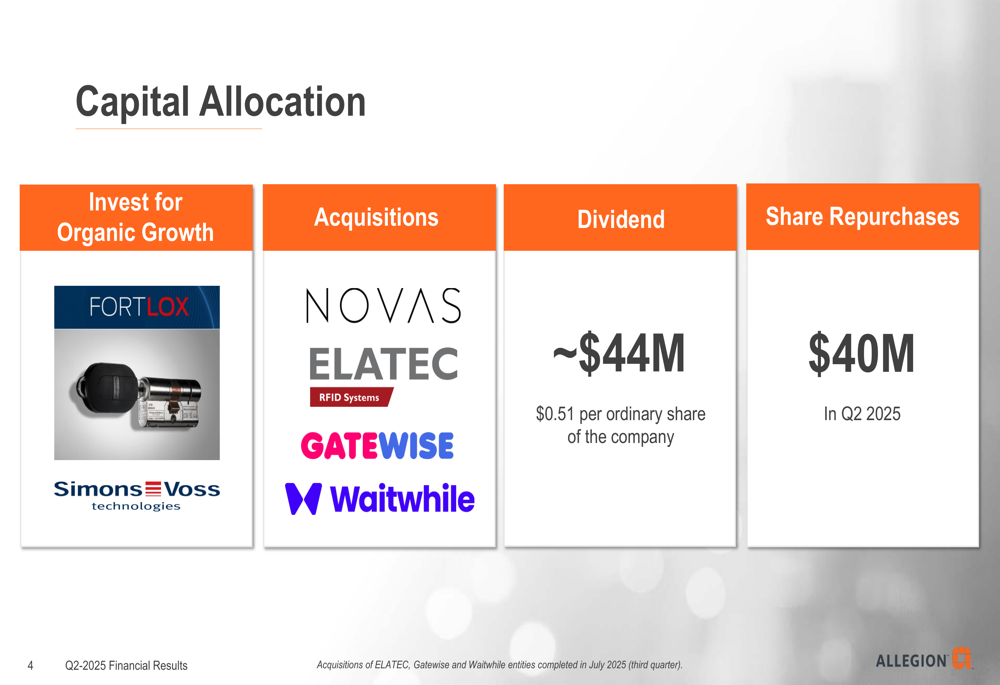

Allegion demonstrated a balanced approach to capital allocation across four key areas: organic growth investments, acquisitions, dividends ($44 million), and share repurchases ($40 million in Q2).

The company’s capital allocation strategy is shown here:

Allegion announced several strategic acquisitions totaling approximately $525 million, targeting three areas: mechanical portfolio expansion (Novas and Trimco, ~$55 million combined), technology and electronics (Elatec, €330 million or ~$390 million), and complementary software services (Gatewise and Waitwhile, ~$80 million combined).

These acquisitions are expected to be accretive to 2026 adjusted EPS and deliver portfolio growth rates with approximately 20% EBITDA margins, as detailed below:

Balance Sheet & Cash Flow Improvements

Allegion’s balance sheet remained strong, supporting its accelerated capital deployment strategy. The company reported significant improvements in cash flow and working capital efficiency, with available cash flow up 56.5% year-to-date to $275.4 million.

Working capital as a percentage of revenue improved from 9.1% in Q2 2024 to 7.9% in Q2 2025, driven by a decrease in days sales outstanding and an increase in accrued liabilities. The company maintained its full-year available cash flow guidance at 85-90% of adjusted net income.

The following chart illustrates these improvements:

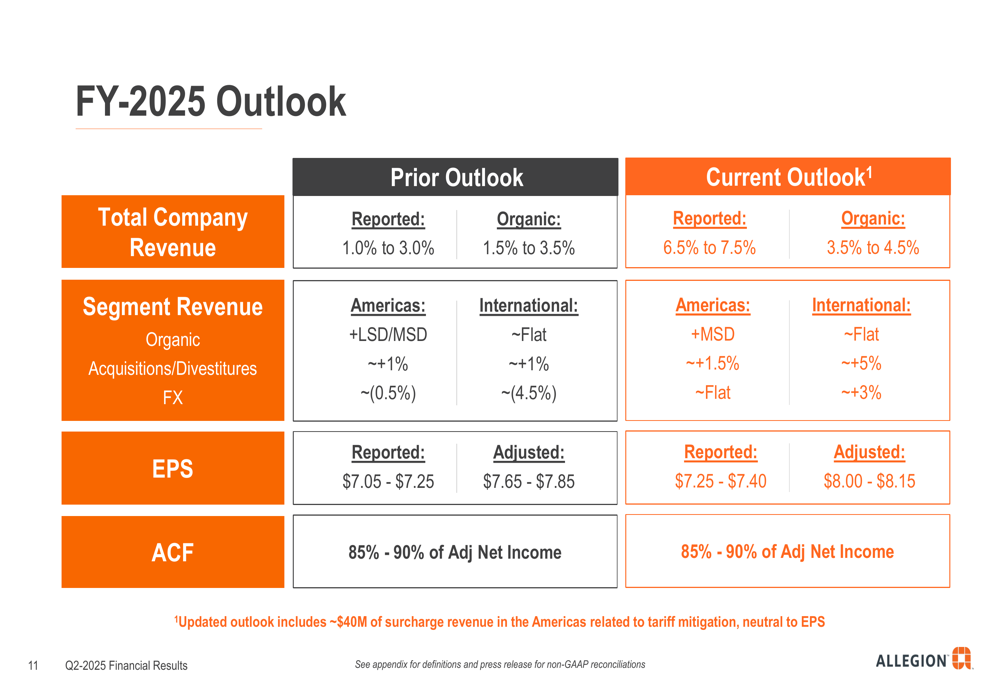

Updated Outlook & Guidance

Based on strong first-half performance and recent acquisitions, Allegion raised its full-year 2025 outlook. The company now expects total revenue growth of 6.5% to 7.5%, up from the previous guidance of 1.0% to 3.0%. Organic growth is projected at 3.5% to 4.5%, compared to the earlier forecast of 1.5% to 3.5%.

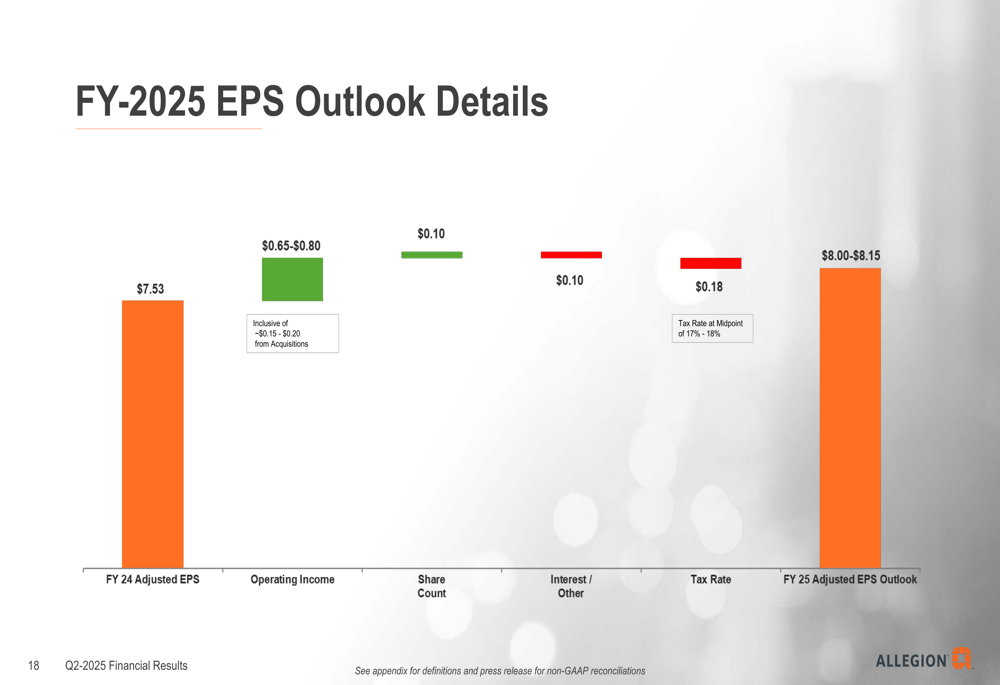

Most notably, Allegion increased its adjusted EPS guidance to $8.00-$8.15, up from the previous range of $7.65-$7.85 provided after Q1 results. This represents a significant improvement from the $7.53 adjusted EPS reported for fiscal year 2024.

The revised outlook is detailed in the following chart:

The company’s outlook includes the impact of enacted tariffs, estimated at approximately $40 million for FY 2025. Allegion noted that its sourcing strategy includes approximately 20-25% of enterprise cost of goods sold from Mexico (with the vast majority USMCA compliant), less than 5% from China, and 5-10% from other countries.

In the Americas, Allegion expects mid-single-digit growth, supported by continued strength in non-residential markets, while the International segment is projected to grow approximately 5%, primarily driven by favorable currency impacts.

The EPS outlook bridge shows that operating income is expected to contribute $0.65-$0.80 to the year-over-year EPS growth, with additional positive contributions from share count reductions, interest/other factors, and tax rate benefits:

Allegion’s Q2 results and updated guidance reflect the company’s ability to execute effectively in a challenging environment, with strong performance in its core non-residential business offsetting weakness in residential markets. The strategic acquisitions announced during the quarter position the company for continued growth in both mechanical and electronic security solutions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.