S&P 500 eases slightly from fresh record high after stronger economic growth

AllianceBernstein Holding LP (NYSE:AB) reported record assets under management (AUM) of $829 billion in its second quarter 2025 presentation delivered on July 24, despite experiencing net outflows for the first time in eight quarters. The company’s stock closed at $41.77 on July 23, near its 52-week high of $42.60, reflecting continued investor confidence despite the mixed results.

Quarterly Performance Highlights

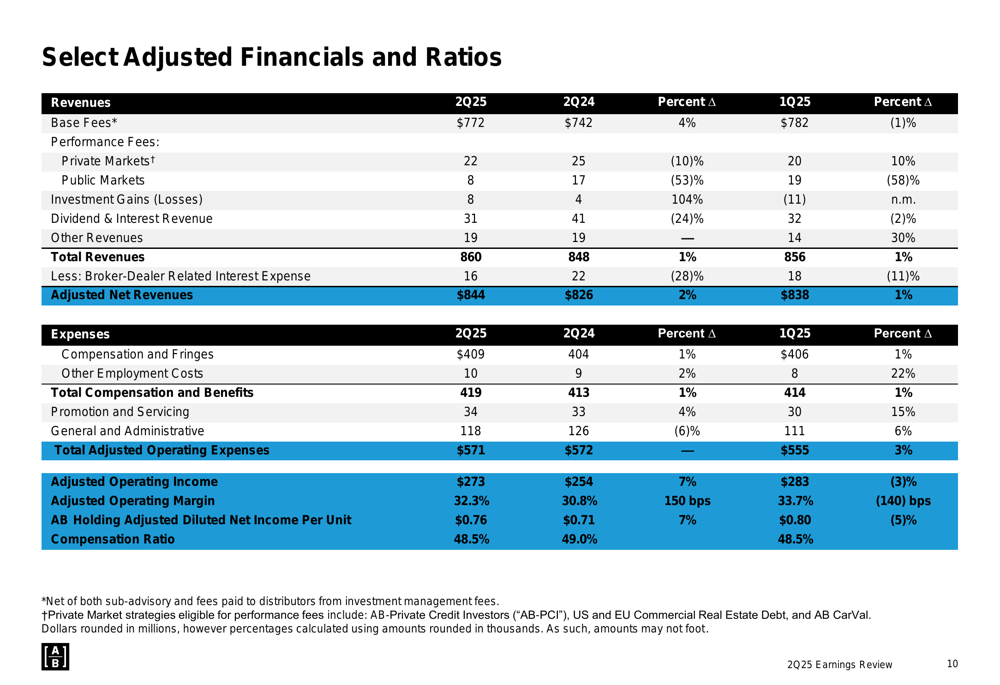

AllianceBernstein reported adjusted earnings per unit of $0.76 for Q2 2025, up from $0.71 in the same quarter last year but down from $0.80 in Q1 2025. Adjusted net revenues rose to $844 million from $826 million a year earlier, while adjusted operating income increased to $273 million from $254 million in Q2 2024.

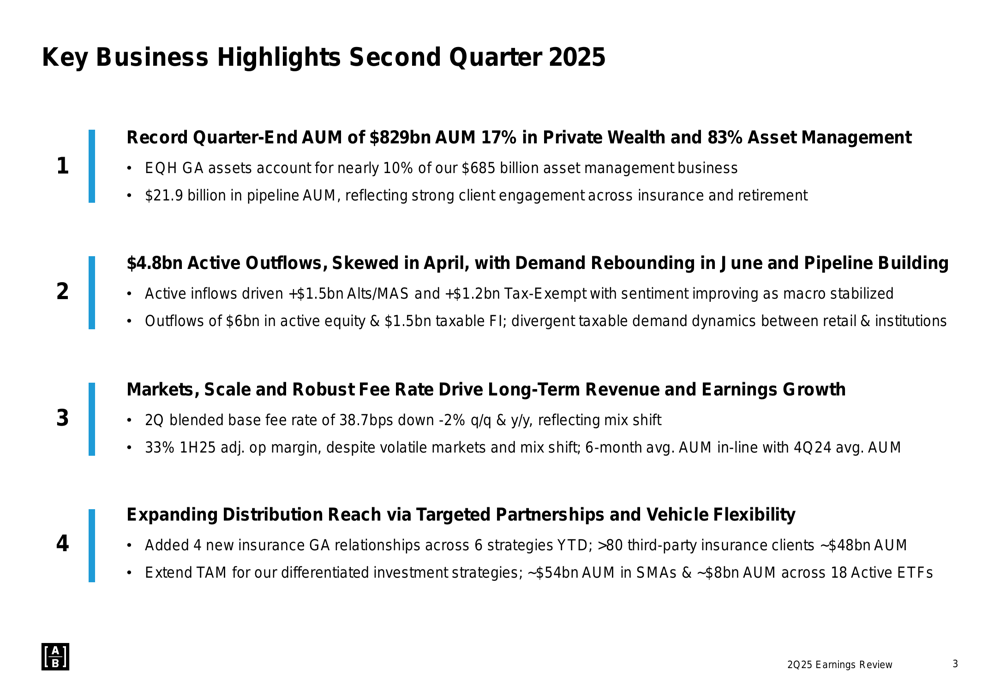

The firm achieved record quarter-end AUM of $829 billion, with 17% in Private Wealth and 83% in Asset Management. However, after seven consecutive quarters of inflows, the company experienced $4.8 billion in active outflows, primarily concentrated in April, with demand rebounding in June.

As shown in the following comprehensive overview of key business metrics:

The company’s blended base fee rate was 38.7 basis points in Q2 2025, down 2% both quarter-over-quarter and year-over-year. Despite this slight decline, AllianceBernstein maintained its first-half 2025 adjusted operating margin at 33%, keeping the company on track to meet its full-year target.

The detailed financial highlights demonstrate year-over-year growth in most key metrics:

Investment Performance

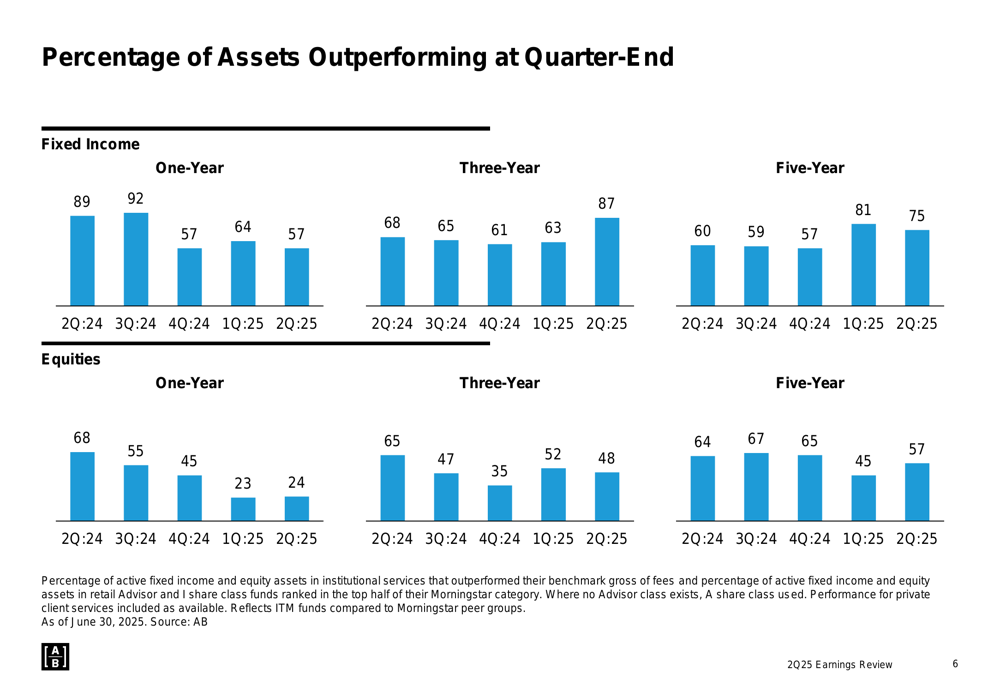

AllianceBernstein’s investment performance showed a stark contrast between asset classes. Fixed income products demonstrated strong results, with 87% of assets outperforming benchmarks over the three-year period, up significantly from 68% in Q2 2024. Meanwhile, equity performance faced challenges, with only 24% of assets outperforming over the one-year period, down from 68% a year earlier.

The following chart illustrates this performance divergence across different time periods:

The retail segment posted its first outflowing quarter after seven consecutive quarters of organic gains. Gross sales declined to $19.4 billion in Q2 2025 from $25.7 billion in Q1 2025, while redemptions remained elevated at $24.2 billion, resulting in net outflows of $4.8 billion.

In the institutional channel, demand remained robust for liquid and private credit products, with positive active net flows in taxable fixed income and alternatives. The institutional pipeline grew substantially to $21.9 billion at quarter-end, more than doubling from $9.8 billion a year earlier, though at a lower fee rate of 21 basis points compared to 49 basis points in Q2 2024.

Private Wealth and Strategic Growth

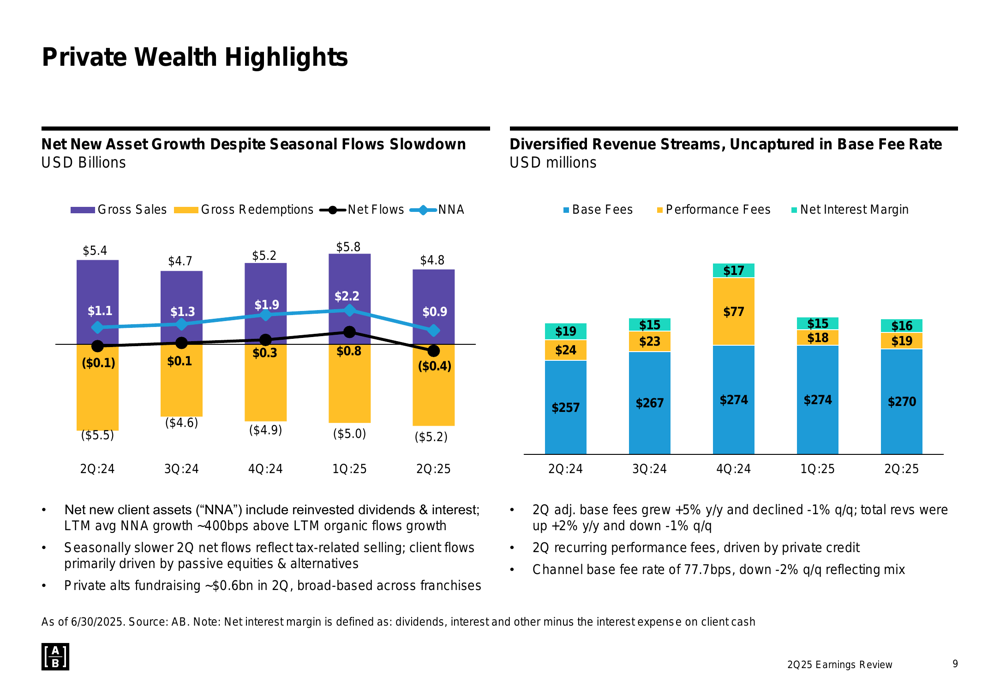

The private wealth segment showed resilience with continued net new asset growth despite seasonal slowdowns. While the segment experienced modest net outflows of $0.4 billion in Q2 2025, net new client assets (including reinvested dividends and interest) remained positive at $0.9 billion.

The following chart details private wealth performance metrics:

AllianceBernstein continues to strengthen its partnership with Equitable Holdings (NYSE:EQH) through what it calls the "Permanent Capital Flywheel" model. This strategic relationship supports the company’s growth in private markets, where AUM reached $77.1 billion in Q2 2025, up from $64.1 billion a year earlier. The firm remains on track to achieve its target of $90-100 billion in private markets AUM by 2027.

Financial Outlook and Performance Expectations

The company’s adjusted operating margin of 32.3% in Q2 2025 showed improvement from 30.8% in Q2 2024, though it declined from 33.7% in Q1 2025. Management confirmed they remain on track for a 33% full-year adjusted operating margin in 2025, assuming flat markets.

The following table provides a clear comparison of key financial metrics:

AllianceBernstein has revised its performance fee expectations upward, now projecting total FY25 performance fees of $110-130 million, compared to the $90-105 million forecast mentioned in its Q1 earnings. The company noted that its private markets platform has accounted for approximately two-thirds of annual performance fees.

The firm’s base fee rate has remained relatively stable through recent market cycles, ending Q2 2025 at 38.7 basis points, identical to its level four years earlier in Q2 2021. This stability provides a solid foundation for revenue growth as AUM expands.

Strategic Positioning

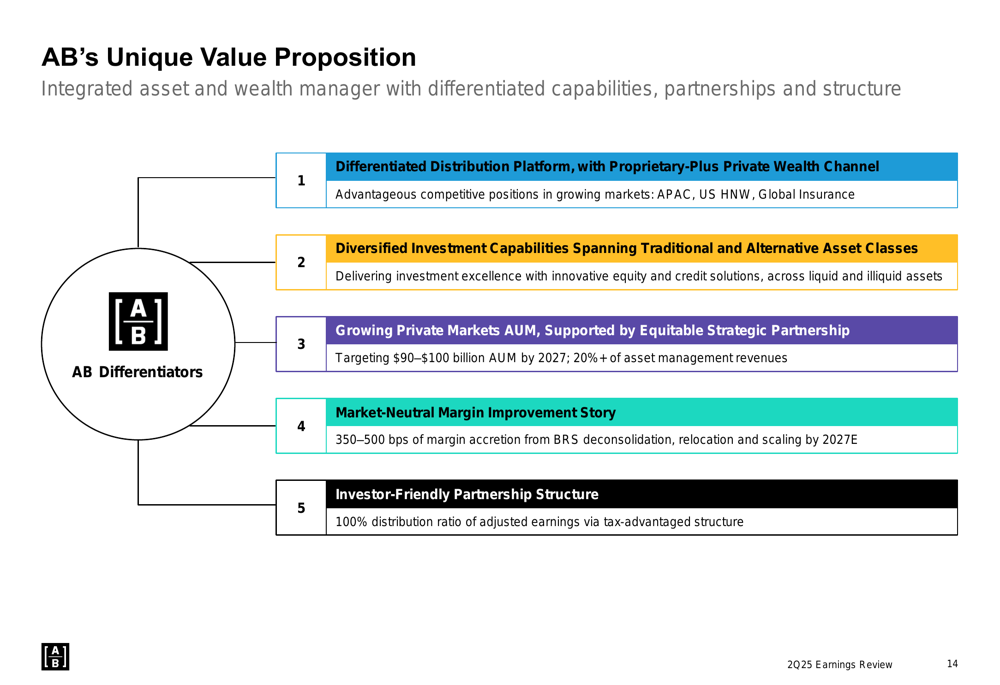

AllianceBernstein highlighted its unique value proposition, emphasizing its differentiated distribution platform, diversified investment capabilities, growing private markets AUM, margin improvement potential, and investor-friendly partnership structure with a 100% distribution ratio of adjusted earnings.

The following summary outlines the company’s strategic advantages:

The company continues to expand its distribution reach, having added four new insurance general account relationships across six strategies year-to-date. AllianceBernstein now serves over 80 third-party insurance clients with approximately $48 billion in AUM, while also growing its separately managed accounts to approximately $54 billion and active ETFs to approximately $8 billion across 18 products.

Despite the mixed results in Q2 2025, AllianceBernstein’s strategic focus on private markets growth, expanded distribution channels, and margin improvement positions the company to navigate market challenges while pursuing long-term growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.