Gold prices fall as geopolitical tensions ease; U.S. CPI looms

Alliant Energy Corp (NYSE:NASDAQ:LNT) reported strong second-quarter results while highlighting significant growth opportunities from data centers and strategic positioning with tax credits during its earnings presentation on August 8, 2025. The utility reaffirmed its full-year guidance as it continues to execute on its clean energy transition.

Quarterly Performance Highlights

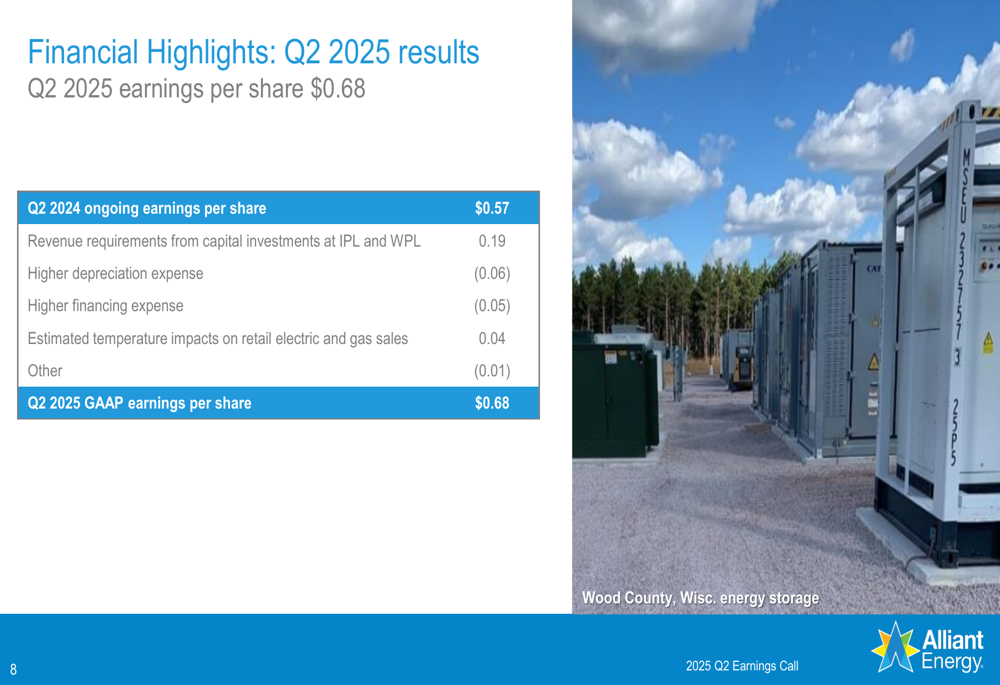

Alliant Energy reported second-quarter earnings per share of $0.68, representing a 19.3% increase from the $0.57 ongoing EPS reported in the same period last year. The company attributed this growth primarily to revenue requirements from capital investments at its Iowa Power and Light (IPL) and Wisconsin Power and Light (WPL) subsidiaries, which contributed $0.19 per share.

These gains were partially offset by higher depreciation expense (-$0.06) and increased financing costs (-$0.05). Favorable weather conditions contributed $0.04 per share to the quarterly results.

As shown in the following financial highlights:

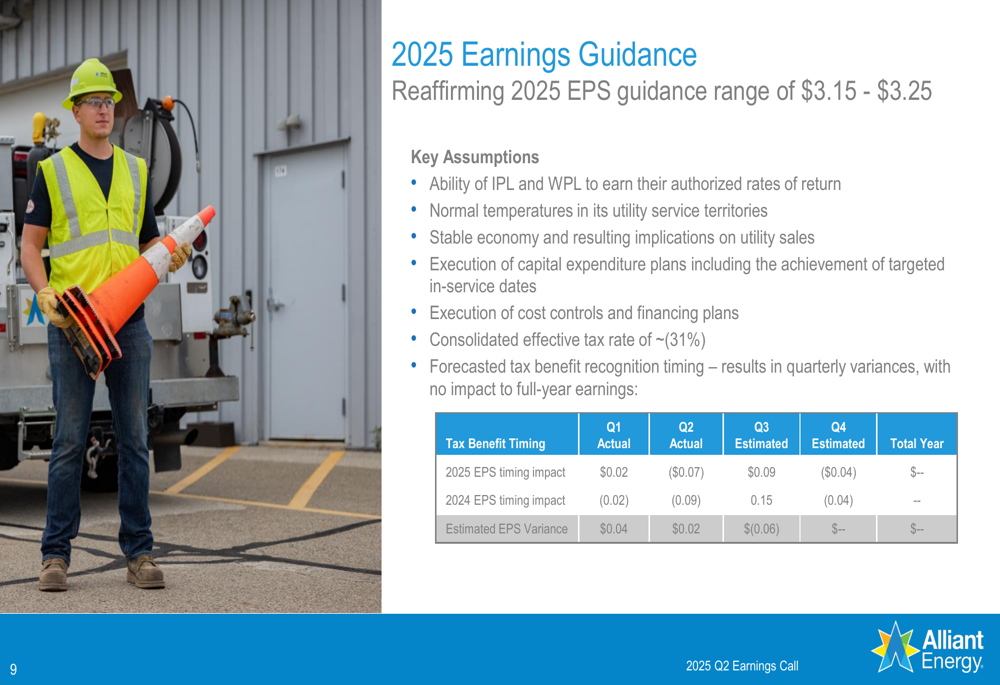

The company reaffirmed its 2025 earnings guidance range of $3.15 to $3.25 per share, maintaining the same outlook provided during its first-quarter results. Key assumptions supporting this guidance include the ability of its utilities to earn their authorized rates of return, normal temperatures, stable economic conditions, and successful execution of capital expenditure and financing plans.

Data Center Growth Strategy

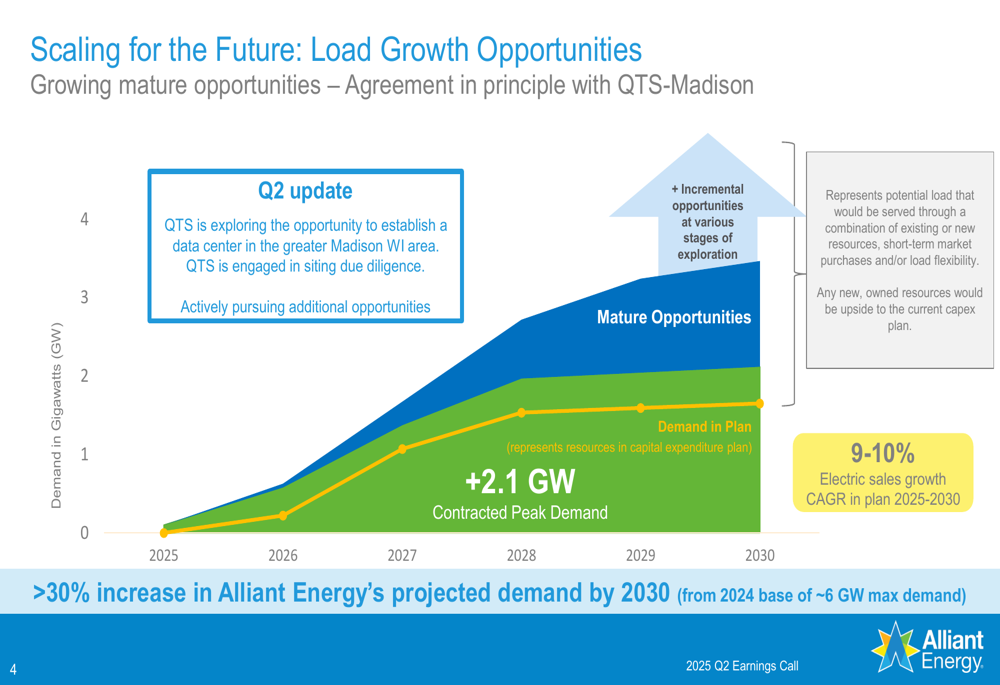

A central theme of Alliant’s presentation was the significant growth opportunity presented by data centers in its service territories. The company highlighted an agreement in principle with QTS for a potential data center in the greater Madison, Wisconsin area, with QTS currently engaged in siting due diligence and actively pursuing additional opportunities.

The presentation revealed contracted peak demand of +2.1 GW from data centers, contributing to a projected electric sales growth CAGR of 9-10% from 2025-2030. This represents more than a 30% increase in Alliant’s projected demand by 2030 from its 2024 base of approximately 6 GW maximum demand.

The following chart illustrates this projected demand growth:

The company detailed specific data center projects already under construction, including QTS and Google (NASDAQ:GOOGL) facilities in Cedar Rapids, Iowa, and Beaver Dam, Wisconsin. These projects have secured Energy Supply Agreements (ESAs) and, in some cases, Individual Customer Rate (ICR) approvals.

Tax Credit and Investment Positioning

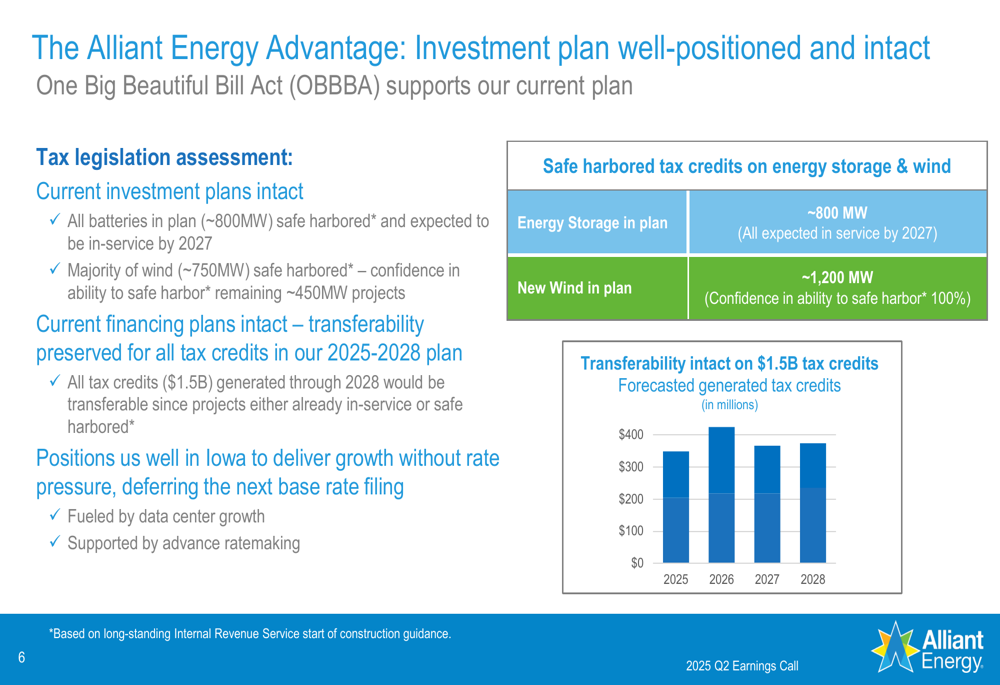

Alliant emphasized how its investment plan remains well-positioned despite recent tax legislation changes, supported by the One Big Beautiful Bill Act (OBBBA). The company has safe harbored all batteries in its plan (approximately 800MW) that are expected to be in-service by 2027, along with the majority of its planned wind projects (approximately 750MW).

The presentation highlighted that all tax credits ($1.5 billion) generated through 2028 would be transferable, as projects are either already in-service or safe harbored. This positions the company well in Iowa to deliver growth without rate pressure, potentially deferring the next base rate filing.

The following chart shows the forecasted generated tax credits through 2028:

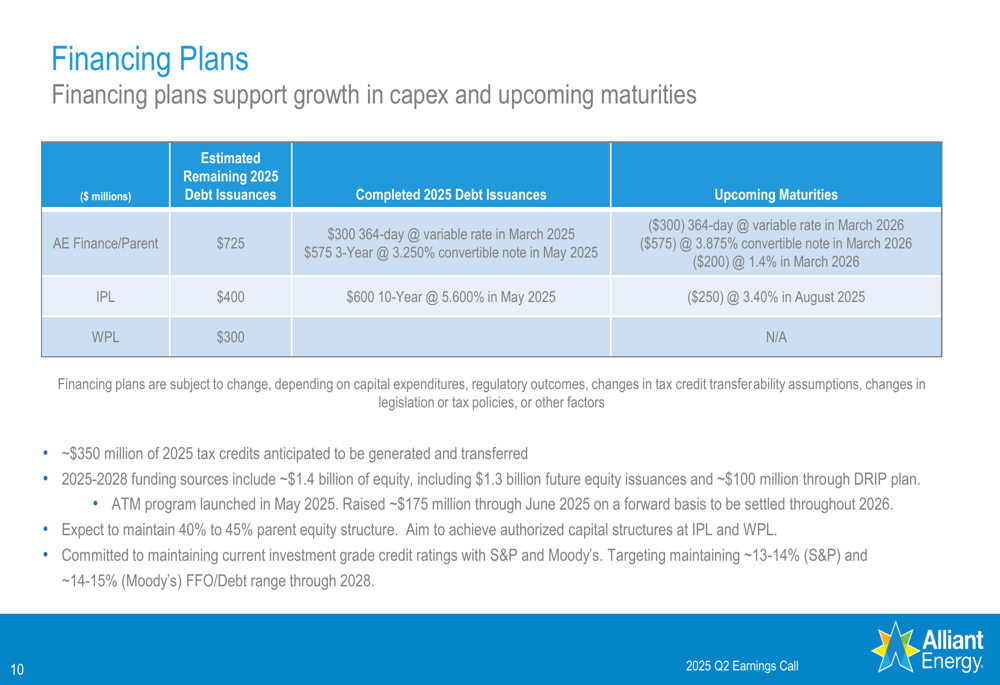

Regarding financing, Alliant outlined plans to support growth in capital expenditures and upcoming maturities. The company expects to maintain a 40% to 45% parent equity structure while targeting investment grade credit ratings. Financing plans include approximately $1.4 billion of equity through 2028, with about $175 million already raised through an ATM program launched in May 2025.

Regulatory Framework and Rate Cases

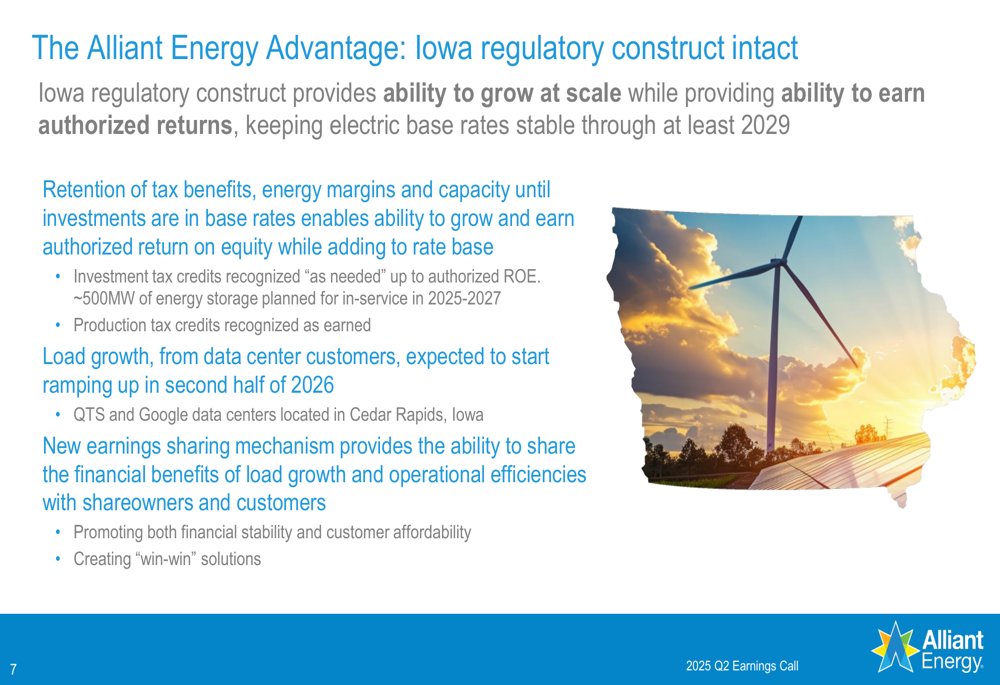

Alliant detailed how Iowa’s regulatory construct provides the ability to grow at scale while maintaining stable electric base rates through at least 2029. The company can retain tax benefits, energy margins, and capacity until investments are included in base rates, enabling growth and authorized returns while adding to rate base.

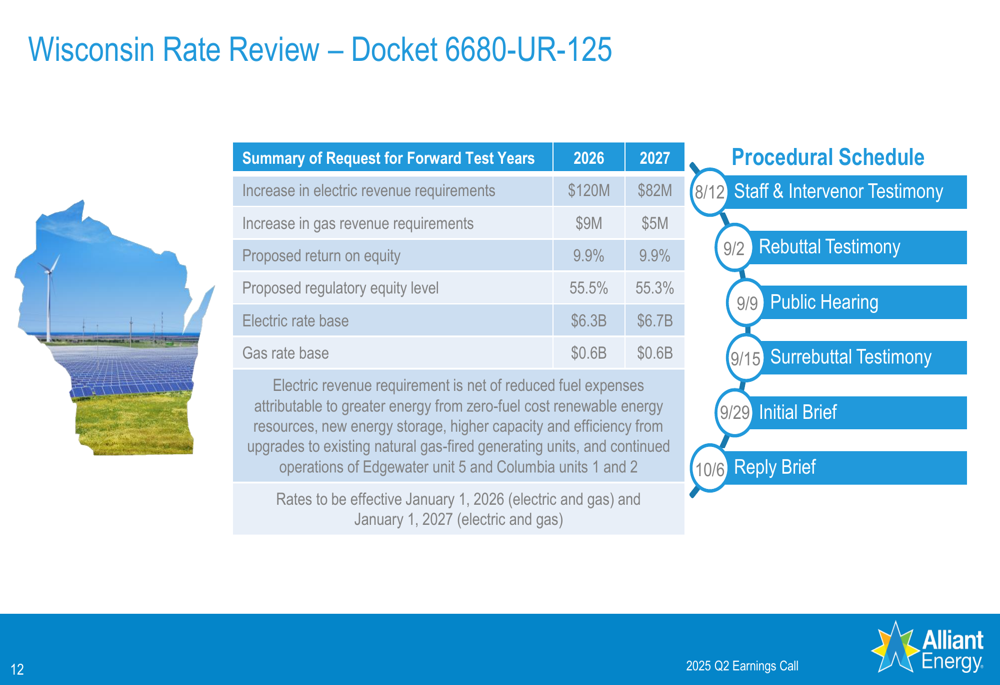

In Wisconsin, the company has filed for a rate review for 2026 and 2027, requesting increases in electric revenue requirements of $120 million and $82 million for the respective years, along with increases in gas revenue requirements of $9 million and $5 million. The proposed return on equity is 9.9% for both years.

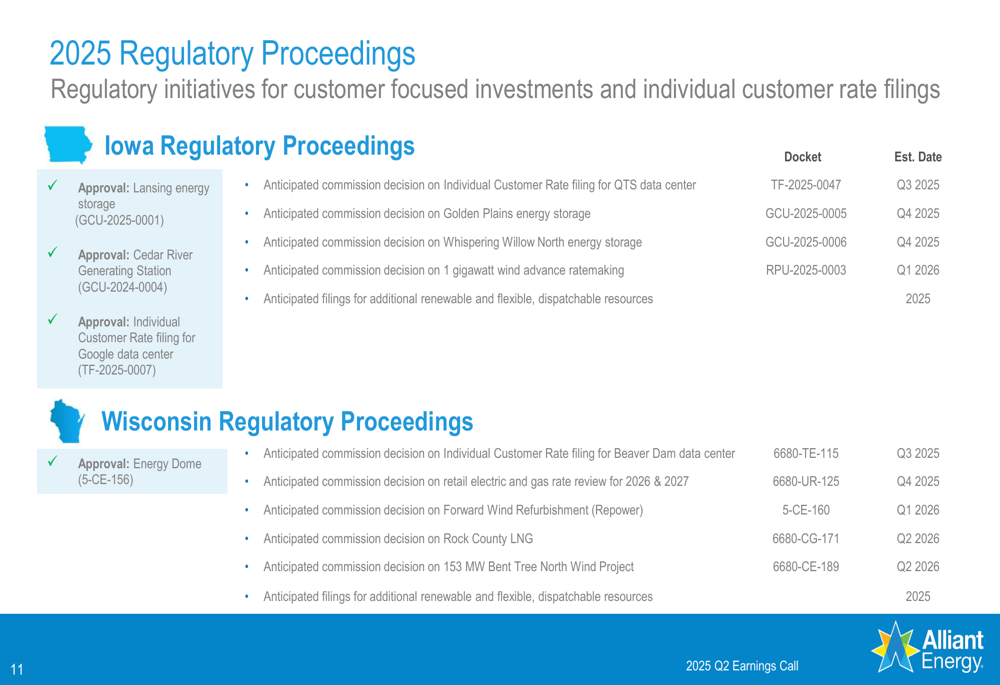

The company also provided a comprehensive overview of pending regulatory proceedings in both Iowa and Wisconsin, including decisions expected on energy storage projects, wind developments, and individual customer rate filings for data centers.

Forward Outlook

Alliant Energy’s presentation emphasized its "Alliant Energy Advantage," defined as "Powering a future you want to own." This strategy focuses on industry-leading growth opportunities driven by data centers and constructive regulation, growing at the pace of customers through adaptive resource planning, and consistently delivering on customer and investor expectations.

The company’s stock closed at $66.12 on August 7, 2025, up 0.53% ahead of the earnings presentation, and has risen approximately 6.6% since its Q1 earnings report in May. With its current strategic positioning in renewable energy, data center growth, and tax credit optimization, Alliant appears well-positioned to execute on its long-term growth plans while maintaining financial stability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.