Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Allianz (ETR:ALVG) (ETR:ALV) released its Q2 2025 financial results on August 7, 2025, showcasing record operating profit and strong growth across all business segments. The company’s stock responded positively, rising 4.95% to €371 following the presentation, a significant turnaround from the 2.56% drop after Q1 results when the company missed EPS forecasts.

The insurance and asset management giant has successfully navigated economic challenges from earlier in the year, with Q2 results demonstrating the resilience of its diversified business model. This performance comes as Allianz continues its strategic transformation from a "world-class product provider into a customer-driven organization," according to CEO Oliver Bäte.

Quarterly Performance Highlights

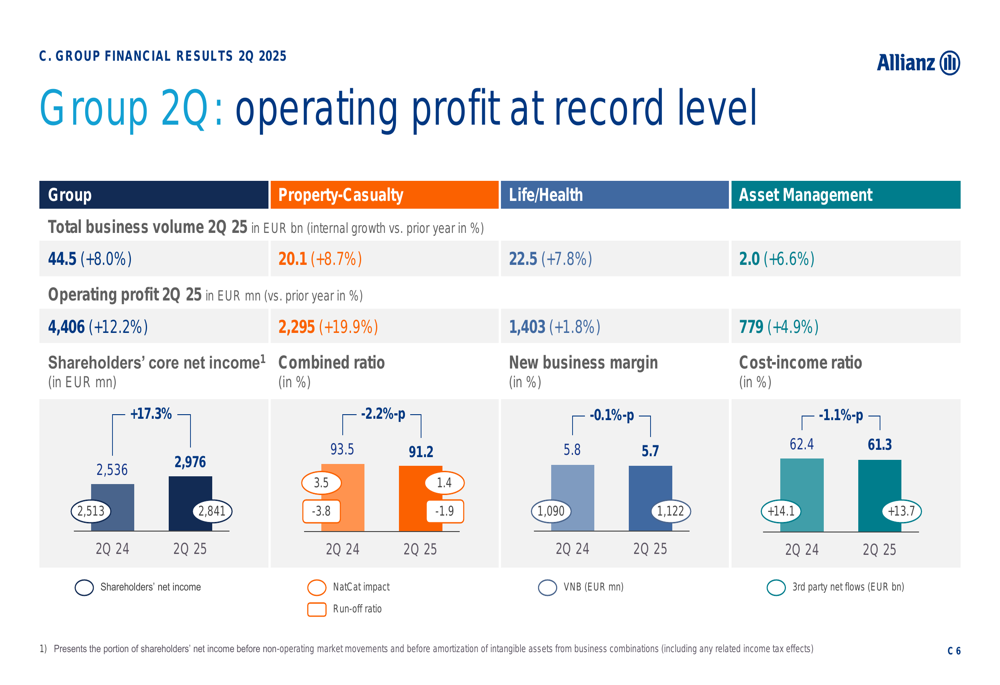

Allianz reported an operating profit of €4.4 billion for Q2 2025, representing a 12.2% increase compared to the same period last year. Total (EPA:TTEF) business volume grew by 8% to €44.5 billion, while shareholders’ core net income jumped 17.3% to €3.0 billion.

As shown in the following chart of quarterly performance metrics:

Core earnings per share increased by 20.2% to €7.39, a significant improvement from Q1 2025 when the company reported €6.61, missing analyst expectations of €6.74. The company maintained a robust Solvency II ratio of 209%, reflecting strong capital adequacy.

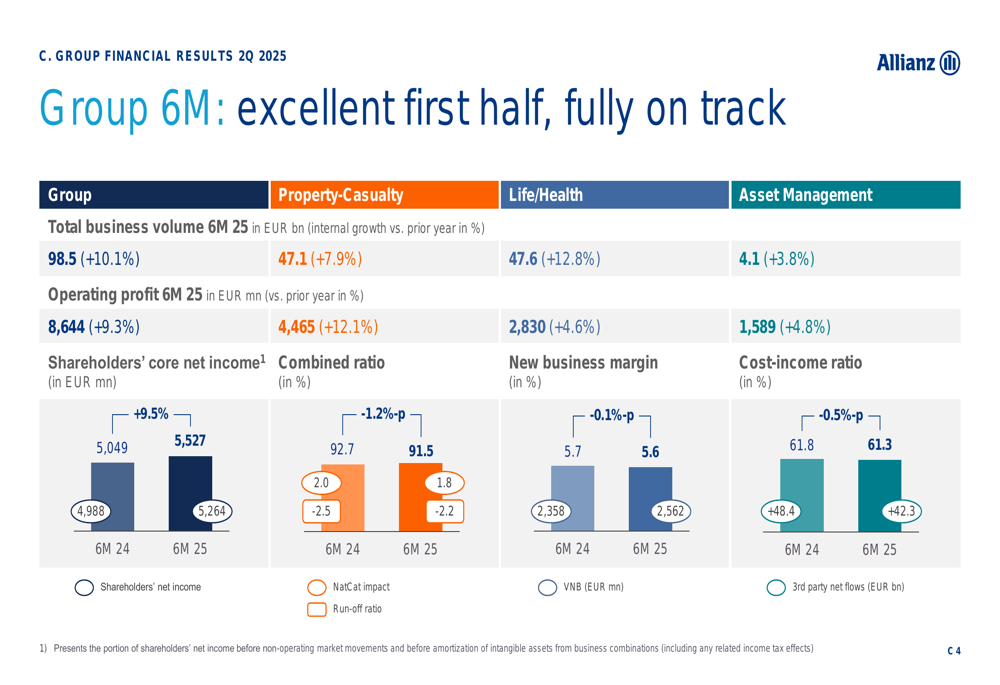

For the first half of 2025, Allianz achieved a total business volume of €98.5 billion, up 10.1% year-over-year, with operating profit reaching €8.6 billion (+9.3%). The company has already achieved 54% of its full-year operating profit outlook midpoint, positioning it well to meet or exceed annual targets.

The following chart illustrates the excellent first-half performance across key metrics:

Segment Performance

Property & Casualty (P&C)

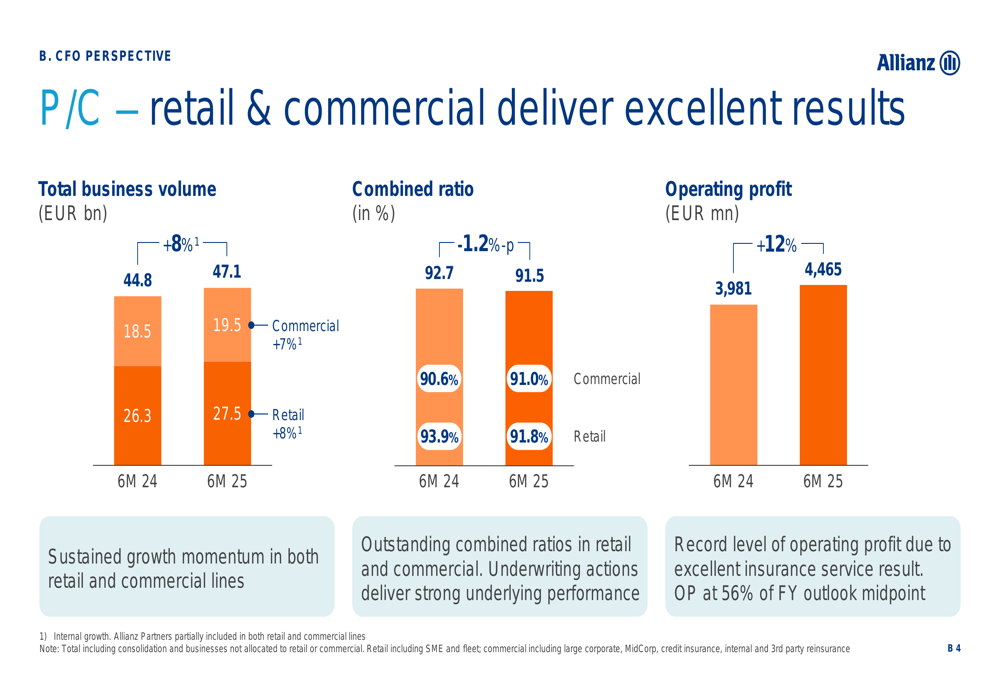

The P&C segment delivered exceptional results, with operating profit increasing by 20% to €2.3 billion in Q2 2025. For the first half of the year, operating profit reached €4.5 billion, up 12% year-over-year. The combined ratio improved by 1.2 percentage points to 91.5%, reflecting enhanced underwriting discipline and productivity gains.

As illustrated in the following segment breakdown:

Internal growth remained strong at 8%, with retail lines growing at 8%, Allianz Partners at 9%, and commercial lines at 6%. The expense ratio continued its positive trajectory, improving to 24.0% for the first half of 2025 compared to 24.4% in the same period of 2024.

Life & Health (L&H)

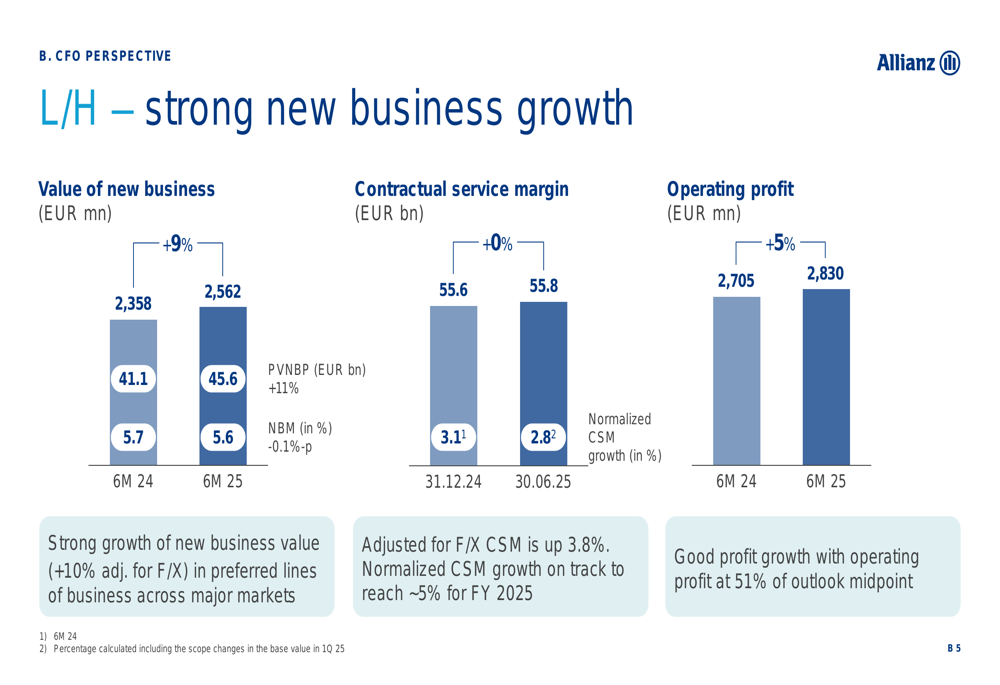

The L&H segment showed robust performance with operating profit slightly increasing to €1.4 billion in Q2 2025. For the first half of the year, operating profit grew by 5% to €2.8 billion. The value of new business increased by 9% to €2.6 billion, while the contractual service margin remained stable at €55.8 billion.

The following chart demonstrates the strong new business growth in this segment:

Normalized contractual service margin (CSM) growth for the first half of 2025 was 2.8%, with the company on track to reach its target of 5% normalized CSM growth. The segment benefited from successful RILA (Registered Index-Linked Annuity) sales campaigns in the USA and continued strong sales momentum in Italy.

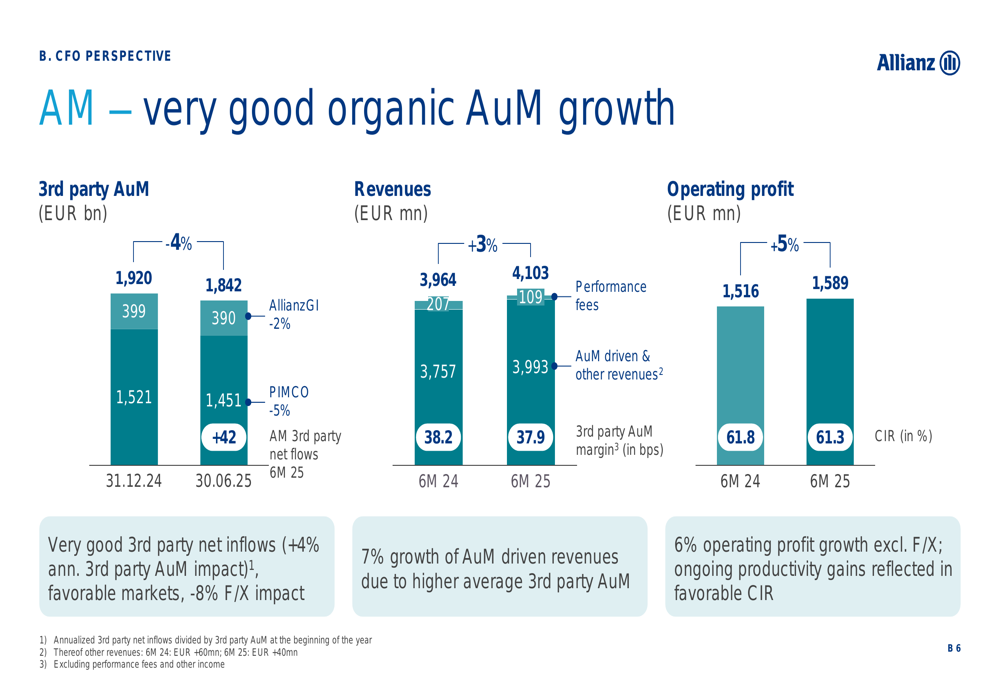

Asset Management

Despite adverse foreign exchange impacts, the Asset Management segment delivered solid results. Operating profit increased by 9% excluding FX effects in Q2 2025. For the first half of the year, operating profit grew by 5% to €1.6 billion.

The segment recorded €42 billion in third-party net inflows, with PIMCO contributing €15 billion in Q2 alone. Total third-party assets under management reached €1.8 trillion, though this represented a 4% decrease primarily due to currency effects.

As shown in the following asset management performance chart:

Strategic Initiatives

Allianz continues to optimize its portfolio and pursue strategic growth opportunities globally. The company has increased its stake in the Sanlam Allianz joint venture to 49% and established a new joint venture with Jio in India after selling its 26% stake in a legacy joint venture.

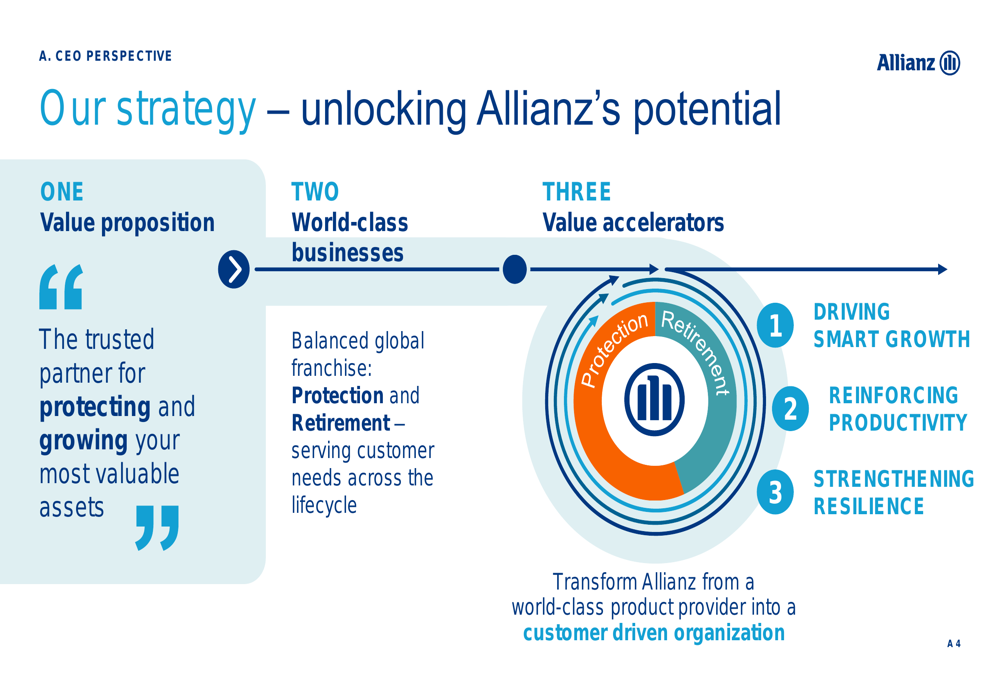

The company’s strategy framework focuses on three key pillars: becoming "the trusted partner for protecting and growing your most valuable assets," maintaining a "balanced global franchise" across protection and retirement services, and implementing value accelerators to drive smart growth, reinforce productivity, and strengthen resilience.

The following strategic framework illustrates Allianz’s approach to unlocking potential:

In Australia, Allianz has formed a strategic partnership with the Royal Automobile Association of South Australia, while in Europe, the company has consolidated various portfolios including Allianz Direct, Eurofil, iptiQ, FRIDAY, and Luko.

Forward-Looking Statements

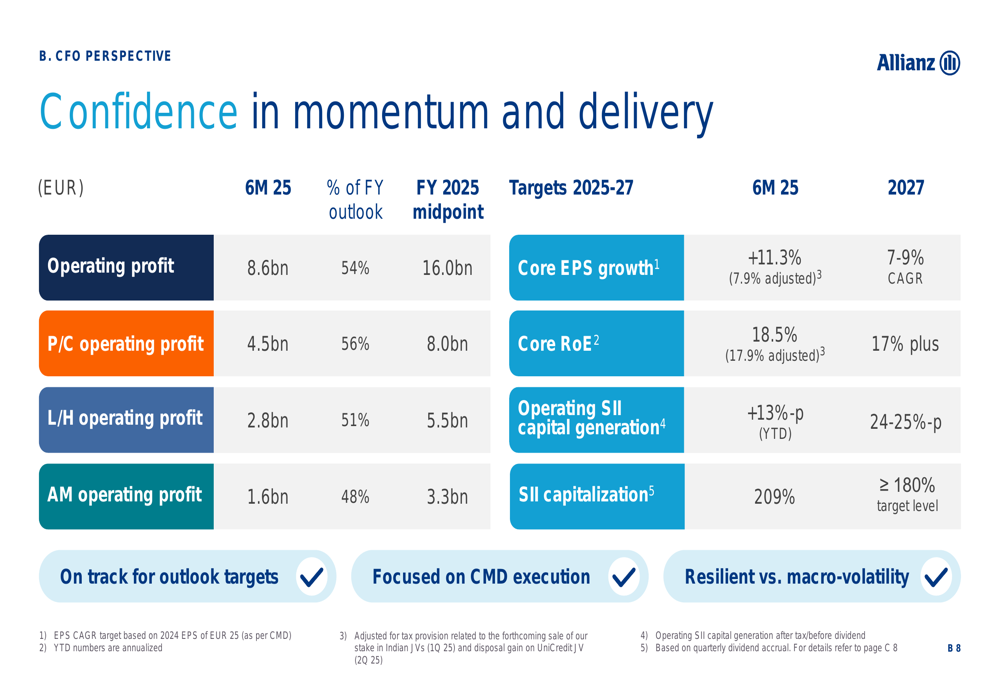

Allianz expressed confidence in its momentum and ability to deliver on its targets. The company is aiming for a core EPS growth of 7-9% CAGR by 2027, with a target of 24-25% growth from 2023 to 2027.

As illustrated in the following outlook chart:

The company’s resilience across all dimensions is supported by a diversified growth profile, strong financials, and a robust balance sheet. With operating profit already at 54% of the full-year outlook midpoint and core EPS growth at 11.3%, Allianz appears well-positioned to meet or exceed its financial targets for 2025.

CFO Claire-Marie Coste-Lepoutre emphasized the company’s focused execution and resilience during the presentation, echoing her earlier statements from the Q1 earnings call about the company’s "strong downside protection" amid market volatility.

Competitive Industry Position

Allianz continues to strengthen its competitive position through a combination of organic growth and strategic acquisitions. The company’s internal growth momentum remains high, particularly in the P&C segment where retail lines, Allianz Partners, and commercial lines all showed strong growth.

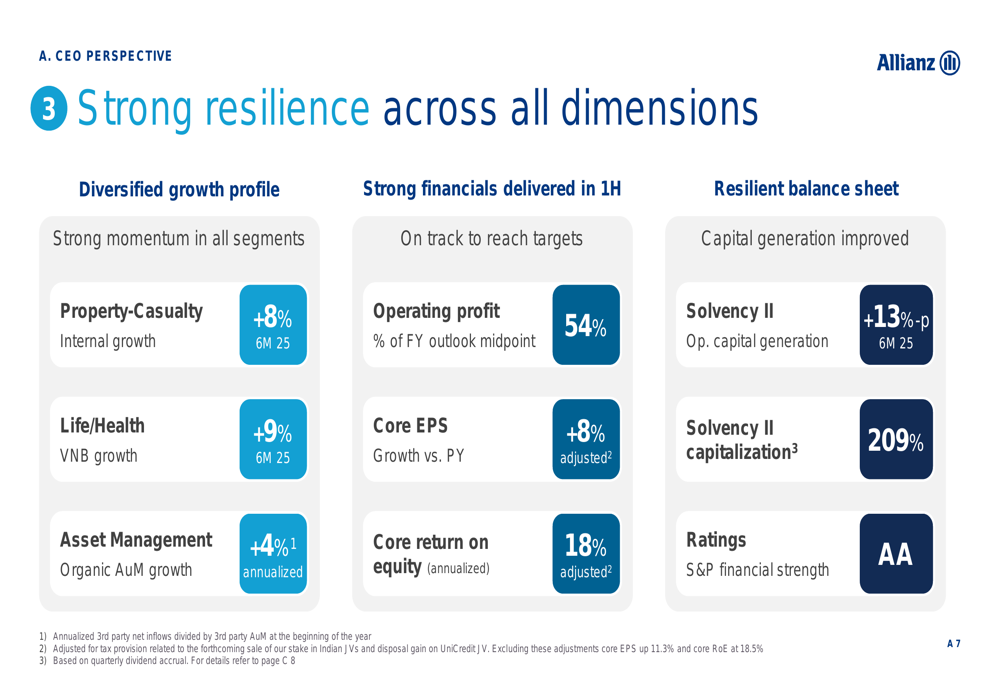

The following chart demonstrates Allianz’s resilience across multiple dimensions:

With a Solvency II ratio of 209% and an AA rating from S&P for financial strength, Allianz maintains a strong position relative to its peers in the insurance and asset management industry. The company’s diversified business model provides stability even as individual segments face different market conditions.

The ongoing €2 billion share buyback program further demonstrates management’s confidence in the company’s financial position and commitment to delivering shareholder value, a significant turnaround from the cautious outlook following Q1 results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.