How are energy investors positioned?

Introduction & Market Context

Allied Gold Corp (TSX:AAUC, NYSE:AAUC) presented its second quarter 2025 results on August 7, 2025, revealing a mixed performance that sent shares tumbling 11.75% to close at $16.60. Despite reporting a 28.8% year-over-year revenue increase to $252.0 million, investors reacted negatively to the company’s elevated production costs, which overshadowed otherwise positive operational developments. The gold producer, which operates mines across Africa, continues to balance current operational challenges with ambitious growth initiatives.

Quarterly Performance Highlights

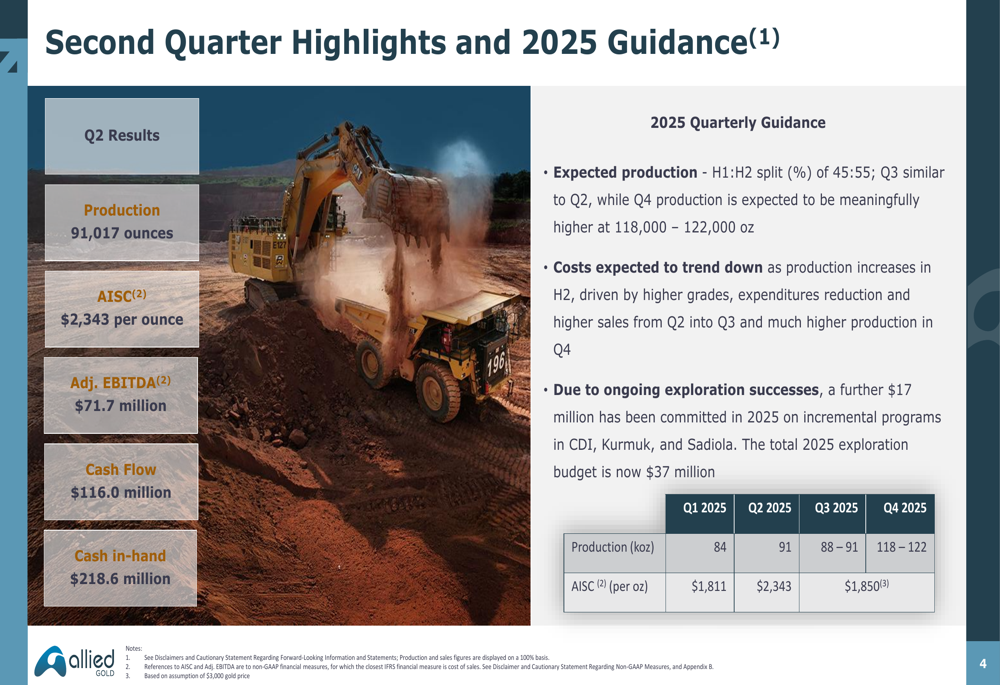

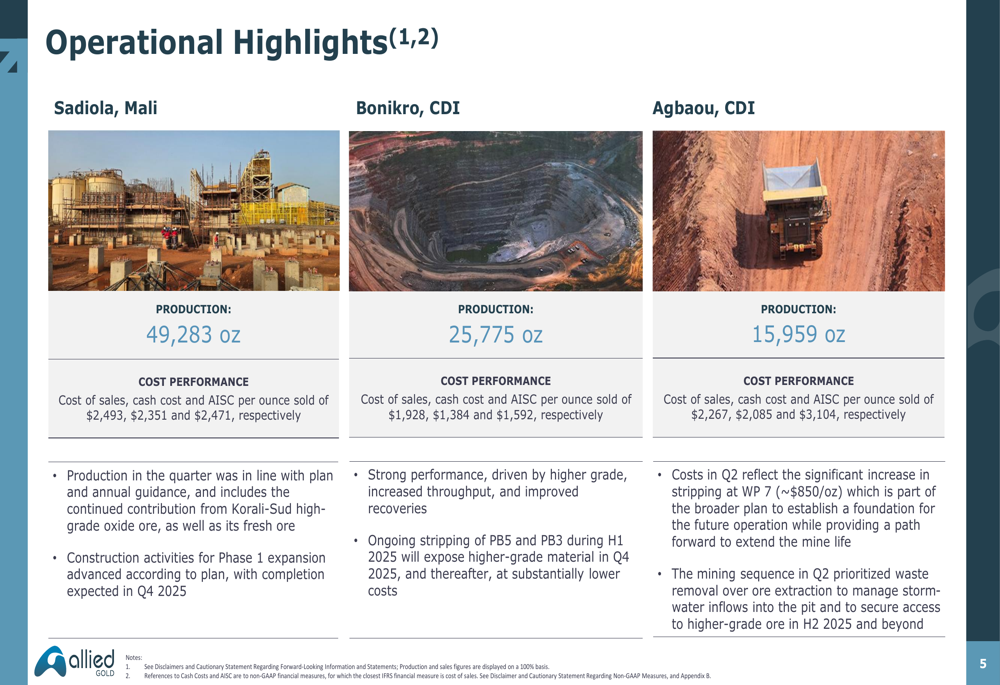

Allied Gold produced 91,017 ounces of gold in Q2 2025, with production distributed across its three operating mines: Sadiola (49,283 oz), Bonikro (25,775 oz), and Agbaou (15,959 oz). The company maintained strong cash flow of $116.0 million before taxes and working capital adjustments, ending the quarter with a robust cash position of $218.6 million.

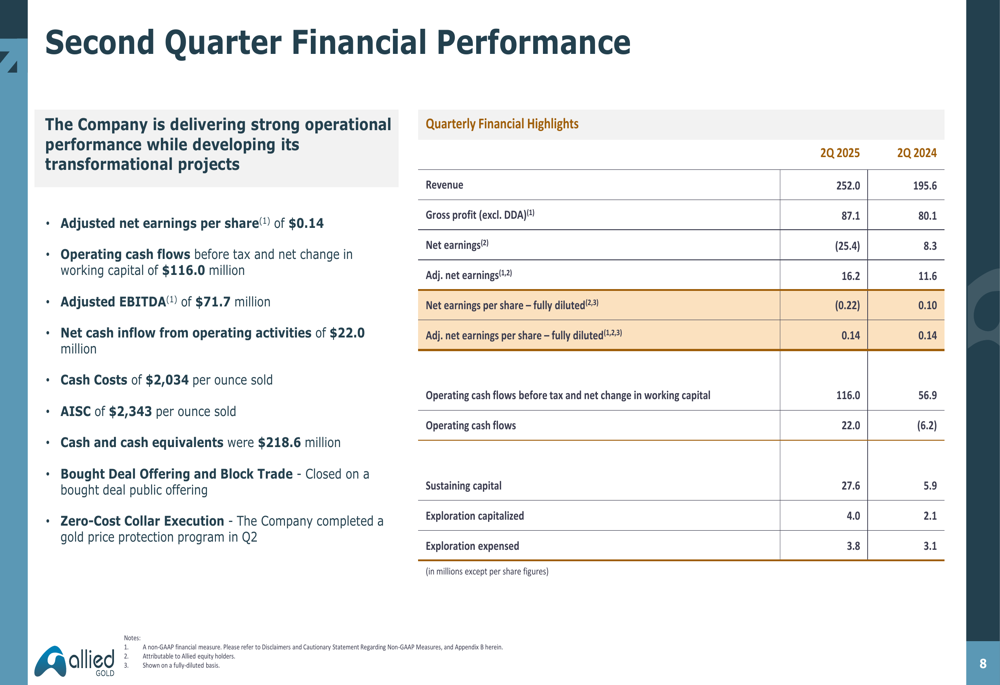

As shown in the following quarterly performance summary:

However, the company’s all-in sustaining cost (AISC) of $2,343 per ounce remains significantly above industry averages and appears to be the primary concern for investors. Management has indicated that costs are expected to trend downward in the second half of the year, with production volumes forecasted to increase substantially.

Detailed Financial Analysis

Allied Gold reported revenue of $252.0 million for Q2 2025, representing a 28.8% increase from $195.6 million in the same period last year. Despite this growth, the company posted a net loss of $25.4 million for the quarter. Adjusted net earnings, which exclude certain non-recurring items, came in at $16.2 million or $0.14 per share.

The company’s financial performance is detailed in the following slide:

Gross profit (excluding depreciation, depletion, and amortization) reached $87.1 million, while adjusted EBITDA totaled $71.7 million. Capital expenditures included $27.6 million in sustaining capital, with an additional $7.8 million allocated to exploration activities ($4.0 million capitalized and $3.8 million expensed).

The operational breakdown by mine site reveals varying cost structures across the company’s portfolio:

Notably, Agbaou recorded the highest AISC at $3,104 per ounce, significantly above the company average, while Bonikro demonstrated better cost control with an AISC of $1,592 per ounce. Sadiola, the company’s largest producing asset, reported an AISC of $2,471 per ounce.

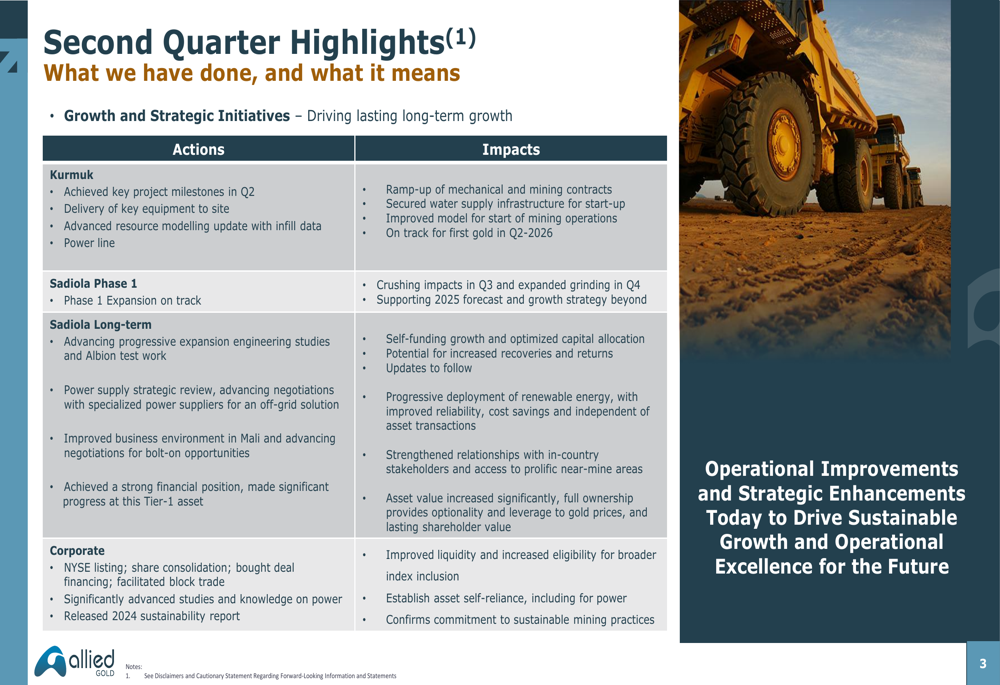

Strategic Initiatives

Allied Gold continues to advance two major growth projects that are central to its future production profile. The Kurmuk project is progressing toward first gold production in mid-2026, with engineering approximately 90% complete and bulk earthworks ahead of schedule.

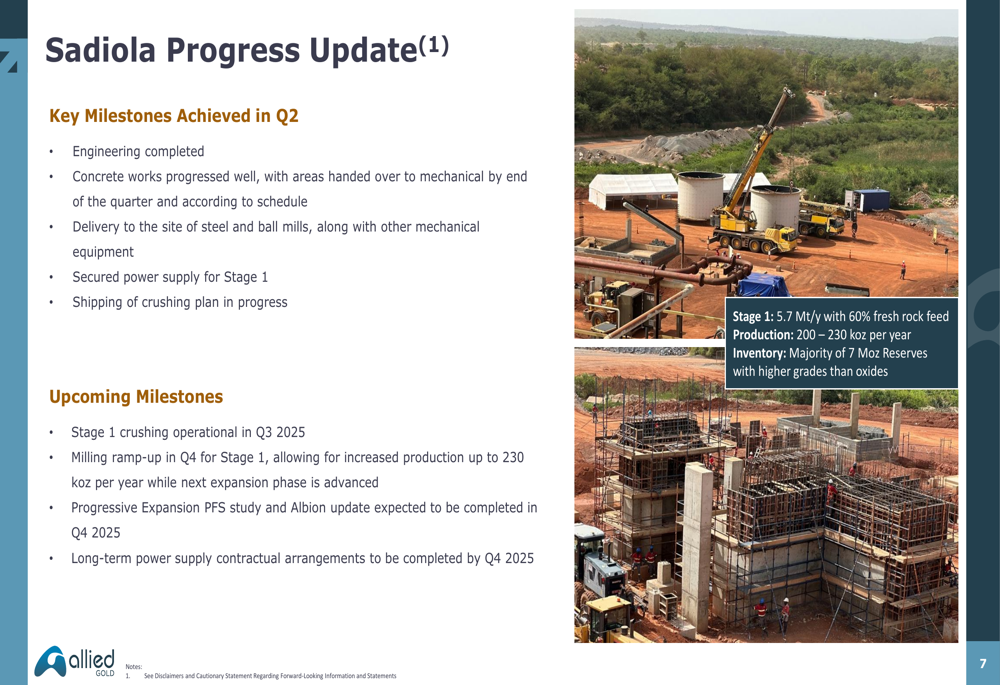

Similarly, the Sadiola expansion project is advancing with engineering completion and concrete works progressing well. The expansion is expected to increase production capacity to 5.7 million tonnes per year with potential annual gold production of 200,000-230,000 ounces from the 7 million ounce reserve.

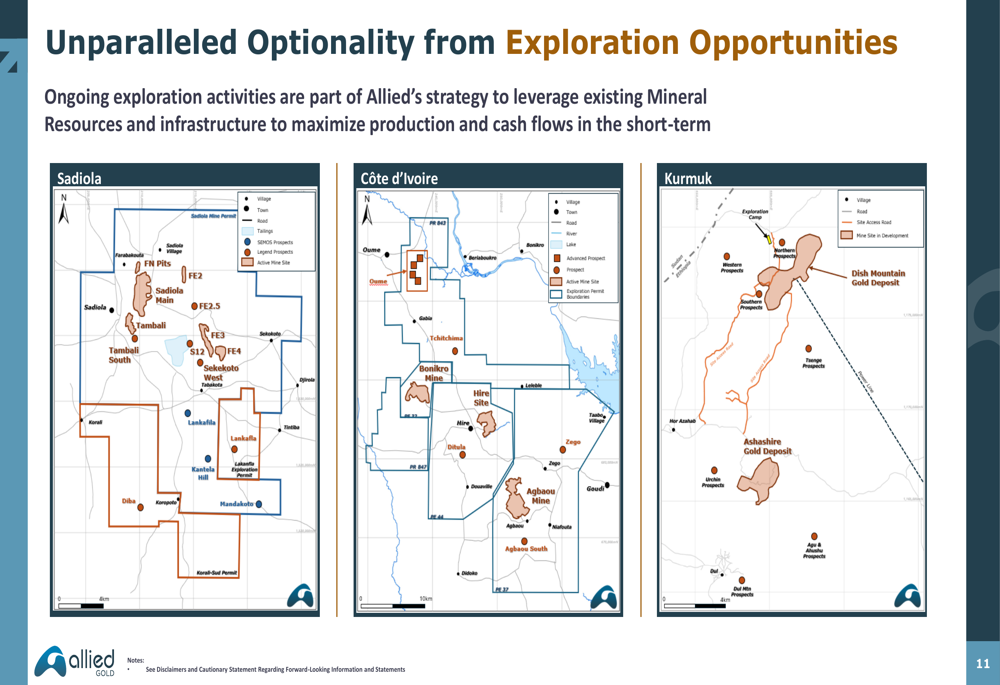

The company has also increased its commitment to exploration, allocating an additional $17 million for a total exploration budget of $37 million in 2025. This investment aims to extend mine life and increase mineral resources across its portfolio.

Allied Gold’s mineral reserves and resources position remains substantial, as detailed in the following comprehensive breakdown:

Forward-Looking Statements

Management has provided quarterly production guidance for the remainder of 2025, projecting 88,000-91,000 ounces in Q3 and a significant increase to 118,000-122,000 ounces in Q4. This implies a 45:55 production split between the first and second halves of the year, with costs expected to trend downward.

The company’s upcoming milestones include exploration updates for Sadiola in October, Kurmuk in November, and Côte d’Ivoire in January 2026. The completion of Sadiola expansion Phase 1 is targeted for late 2025, while Kurmuk operations are scheduled to commence in mid-2026.

Despite the positive long-term outlook, Allied Gold faces immediate challenges in managing production costs while executing its growth strategy. The significant stock decline following the earnings release suggests investors remain concerned about the company’s ability to control costs in the current operating environment, even as it positions itself as "Africa’s Next (LON:NXT) Leading Gold Producer."

With gold prices remaining elevated, the company’s ability to reduce its AISC in the coming quarters will likely be crucial to restoring investor confidence and realizing the full potential of its expanding production profile.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.