Street Calls of the Week

Introduction & Market Context

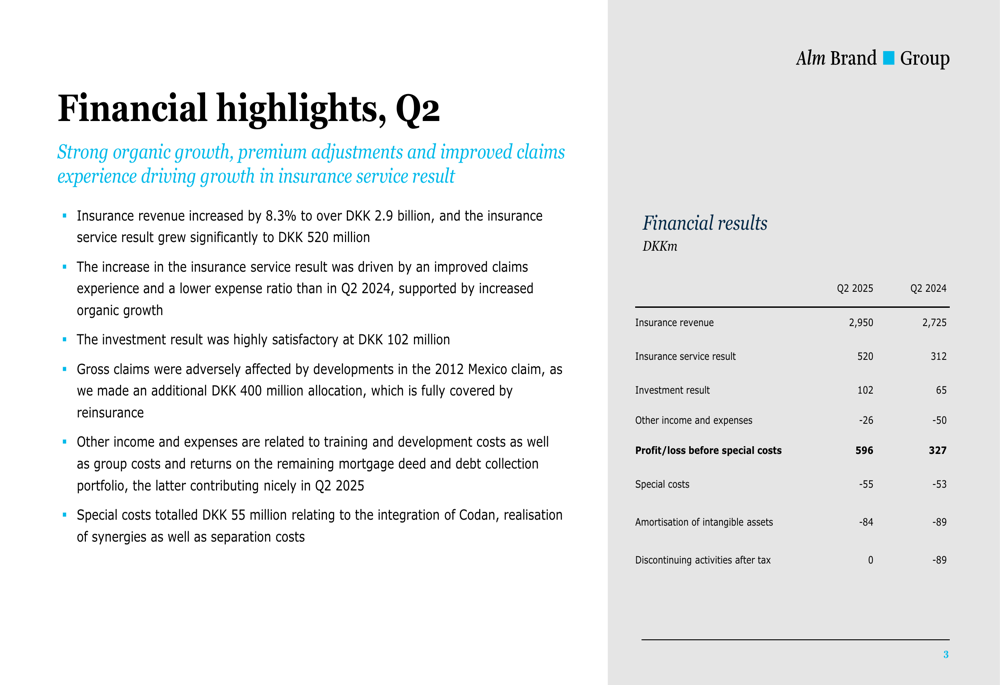

Alm. Brand (CPSE:ALMB) reported strong Q2 2025 results on July 16, showing significant improvement over its Q1 performance. The Danish insurer, which holds approximately 15% market share in the non-life insurance sector, saw its insurance revenue increase by 8.3% to DKK 2.95 billion, while the insurance service result grew substantially to DKK 520 million compared to DKK 312 million in the same period last year.

This performance represents a notable turnaround from Q1 2025, when the company missed earnings expectations. Following the Q2 results announcement, Alm. Brand’s stock closed at DKK 17.42 on July 15, though it has since seen a slight decline of 0.97% in recent trading.

Quarterly Performance Highlights

Alm. Brand’s Q2 2025 results were characterized by strong organic growth, effective cost control, and a favorable investment environment. The company highlighted several key achievements in its presentation, including a significant improvement in the underlying claims experience and major claims below the normal level.

As shown in the following financial highlights table, the insurance service result saw a substantial year-over-year increase of 66.7%, while the investment result grew by 56.9% compared to Q2 2024:

The company’s profit before special costs reached DKK 596 million, an 82.3% increase from DKK 327 million in Q2 2024. This improvement was driven by both the strong insurance service result and a highly satisfactory investment result of DKK 102 million.

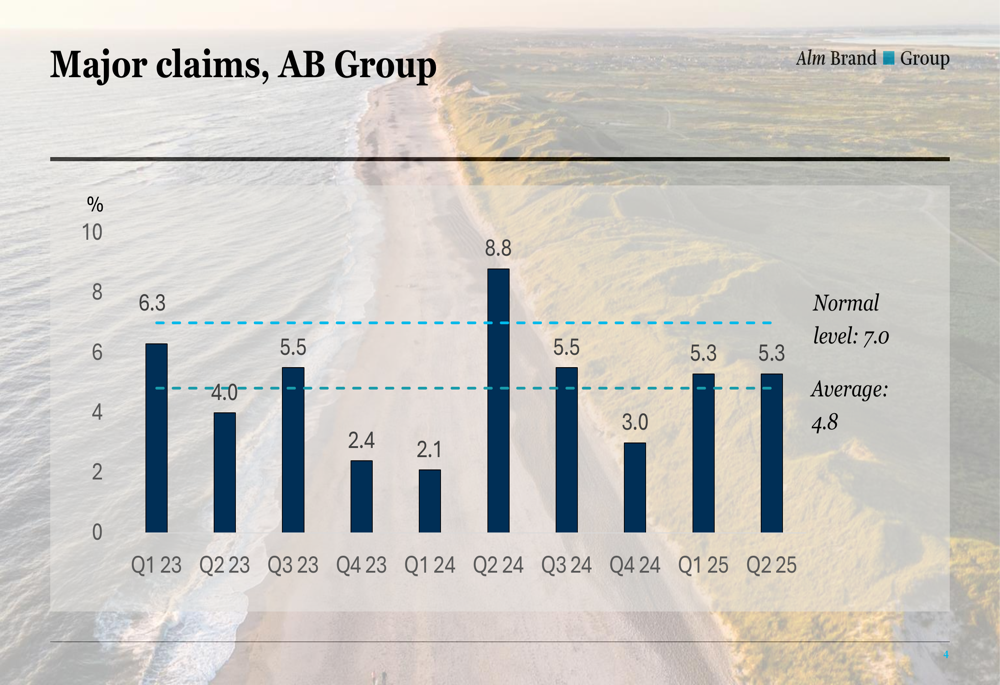

Major claims remained below the normal level at 5.3% for Q2 2025, significantly lower than the 8.8% recorded in Q2 2024, as illustrated in the following chart:

Segment Performance

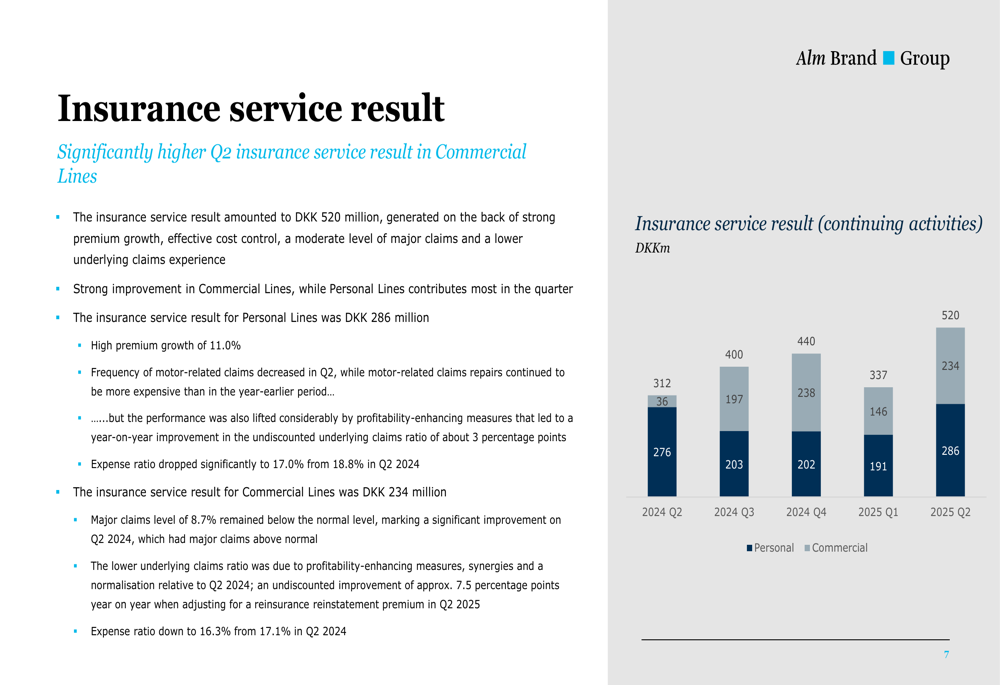

Both Personal and Commercial Lines contributed to the strong Q2 results, with Personal Lines delivering DKK 286 million to the insurance service result and Commercial Lines contributing DKK 234 million. The following chart illustrates the consistent improvement in both segments over the past five quarters:

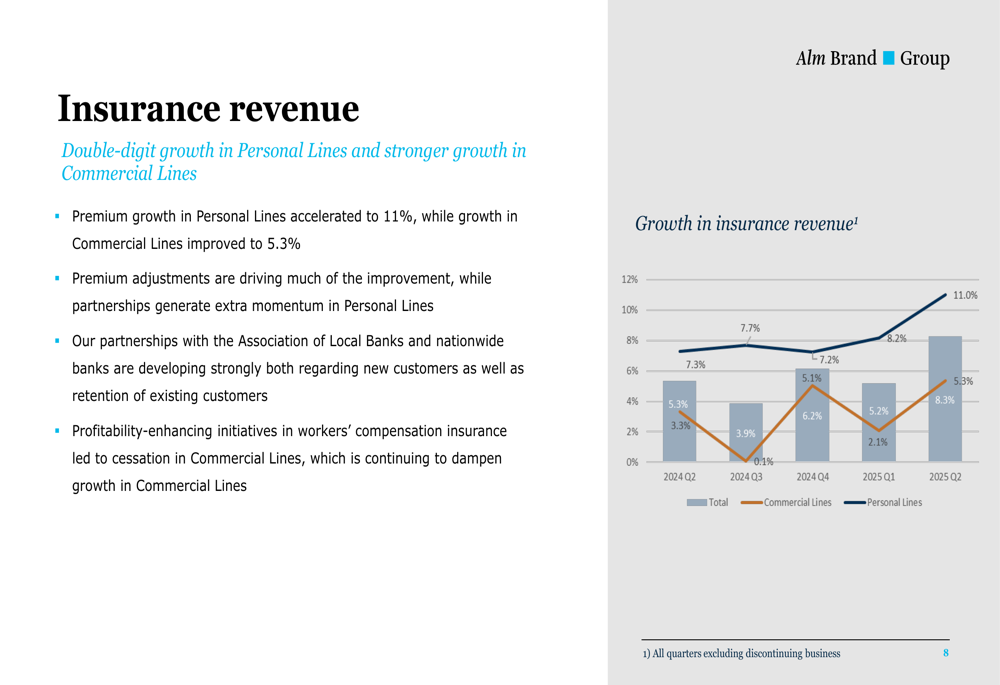

Personal Lines showed particularly impressive growth, with premium increases accelerating to 11.0% in Q2 2025. Meanwhile, Commercial Lines growth improved to 5.3%, recovering from slower growth in previous quarters. This growth trajectory is clearly visible in the following chart:

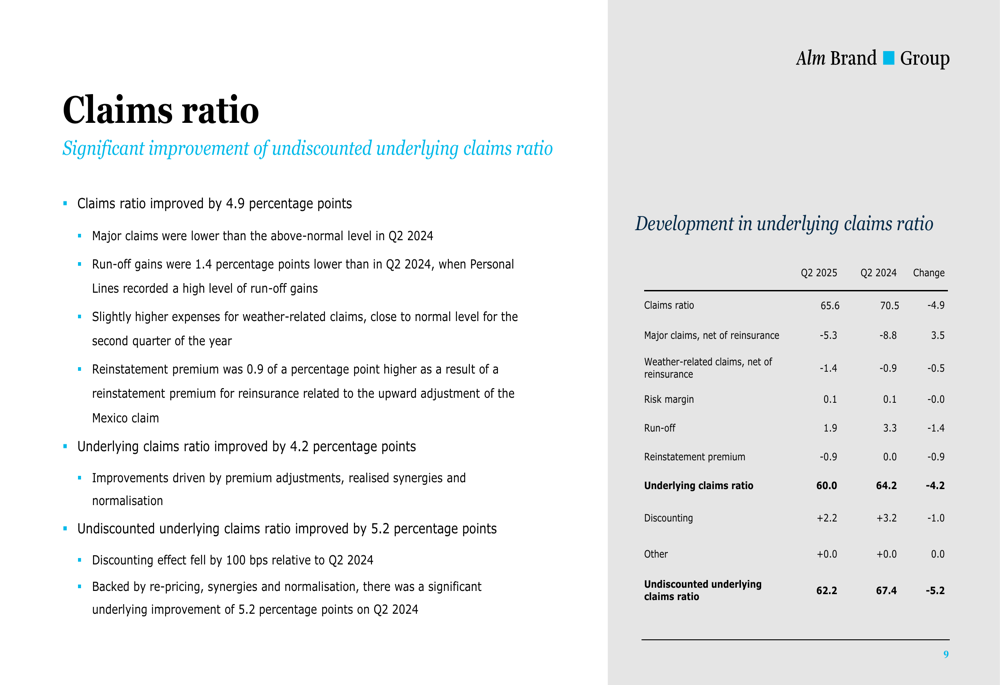

The claims ratio improved significantly, decreasing by 4.9 percentage points compared to Q2 2024. This improvement was driven by lower major claims, premium adjustments, realized synergies, and normalization of claims patterns, as detailed in this breakdown:

The expense ratio also saw notable improvement, dropping to 17.0% in Personal Lines (from 18.8% in Q2 2024) and to 16.3% in Commercial Lines (from 17.1% in Q2 2024). These reductions were attributed to headcount reductions implemented in October 2024 and ongoing synergy realization.

Synergy Realization

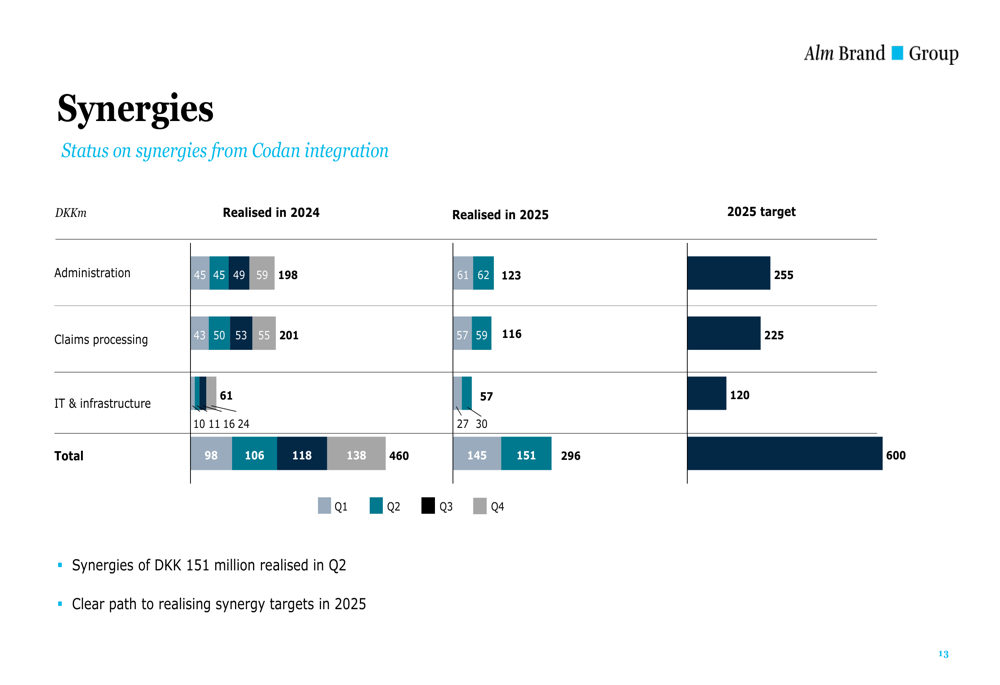

Alm. Brand continues to make substantial progress in realizing synergies from the Codan integration. In Q2 2025, the company achieved synergies of DKK 151 million, bringing the total realized synergies for 2025 to DKK 296 million. The company remains on track to meet its full-year target of DKK 600 million in synergies.

The following chart shows the breakdown of realized synergies across administration, claims processing, and IT & infrastructure:

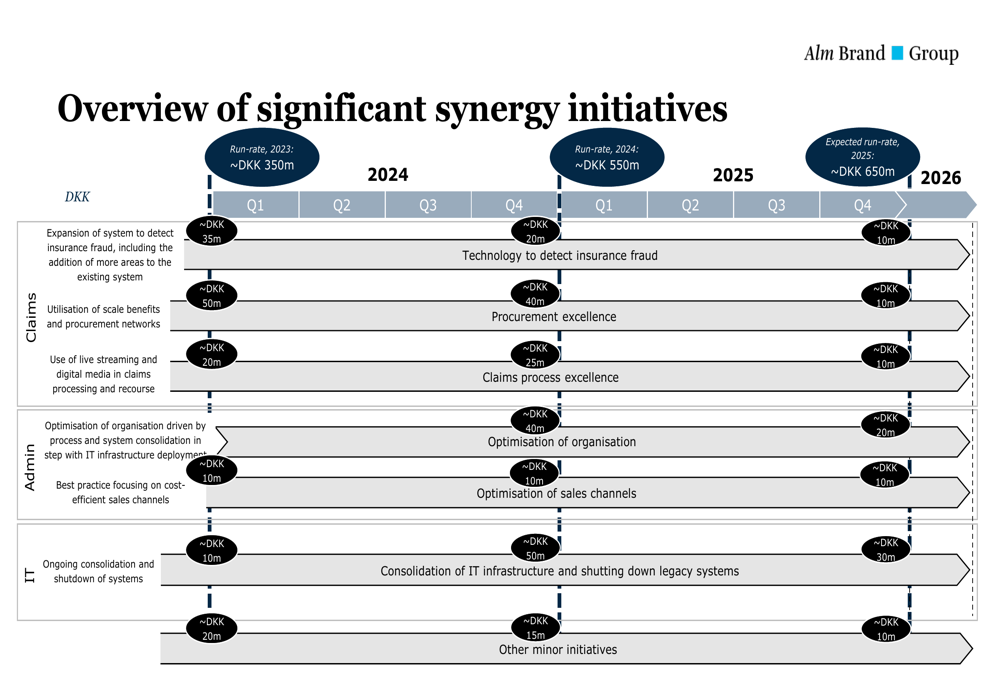

These synergies are being achieved through various initiatives, including expansion of fraud detection systems, procurement excellence, claims process optimization, and IT system consolidation. The company provided a detailed timeline of these initiatives in its presentation:

Guidance and Outlook

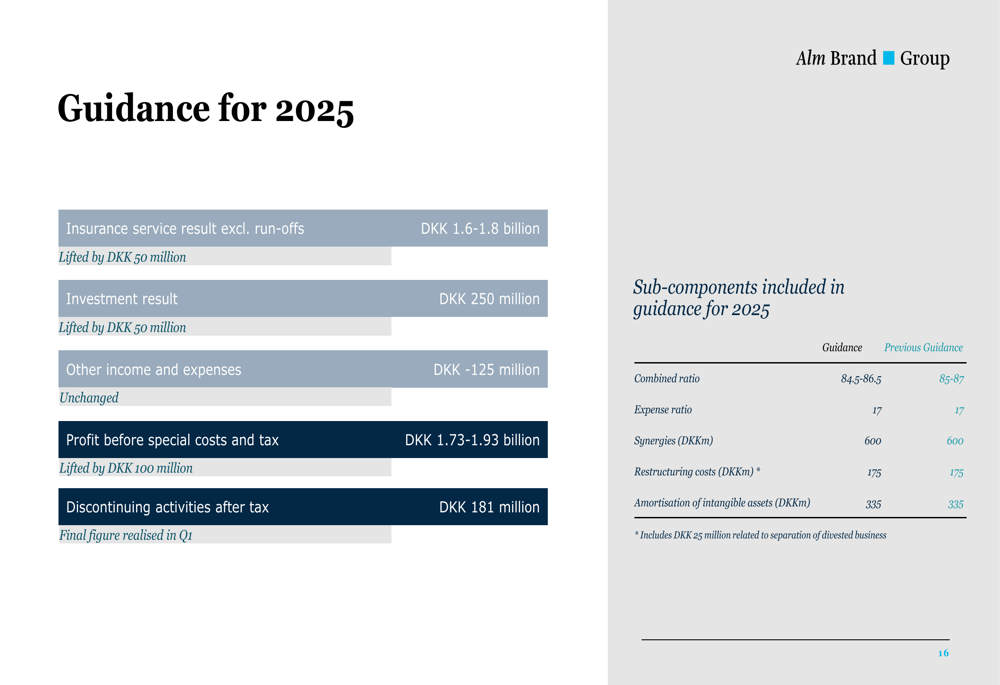

Based on the strong Q2 performance, Alm. Brand has raised its full-year 2025 guidance. The insurance service result excluding run-offs is now expected to reach DKK 1.6-1.8 billion, an increase of DKK 50 million from previous guidance. Similarly, the investment result forecast has been lifted by DKK 50 million to DKK 250 million.

The combined ratio guidance has also been improved to 84.5-86.5%, down from the previous range of 85-87%. The company’s updated guidance is summarized in the following table:

Alm. Brand also announced that it will host a Capital Markets Day on November 18, 2025, where it will launch its strategy and financial targets for the 2026-2028 period.

Capital Position

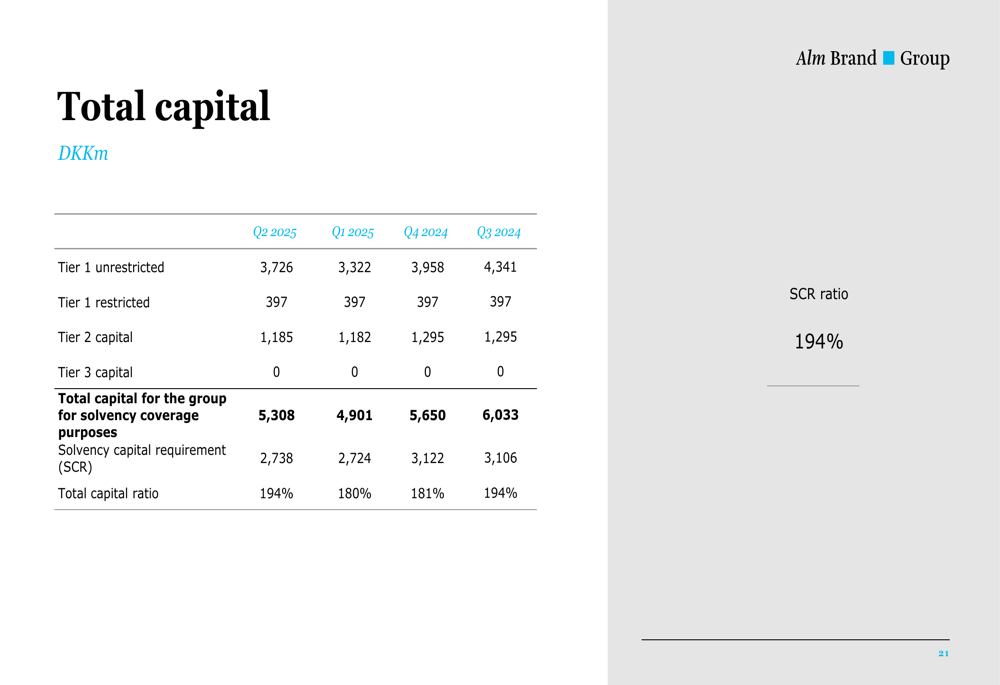

The company maintained a strong capital position, with a Solvency Capital Requirement (SCR) ratio of 194% at the end of Q2 2025, up from 180% in Q1 2025. This improvement provides the company with additional financial flexibility and capacity for potential growth initiatives.

The following table details the company’s capital structure and regulatory ratios:

The investment portfolio delivered a highly satisfactory return of DKK 102 million in Q2 2025, supported particularly by the performance of bond and share portfolios. The company maintains a cautious investment strategy with a well-diversified, low-risk portfolio calibrated according to earnings from insurance operations.

Forward-Looking Statements

Looking ahead, Alm. Brand is focused on maintaining its momentum in both Personal and Commercial Lines. The company expects continued benefits from premium adjustments and partnership growth, particularly with the Association of Local Banks and nationwide banks, which are developing strongly in terms of both new customer acquisition and retention.

The company’s distribution policy prescribes a pay-out ratio of at least 80%, with substantial distribution capacity of 90% or more. This suggests that shareholders can expect continued returns through dividends or share buybacks as the company generates excess capital.

With the synergy realization from the Codan integration progressing as planned and profitability-enhancing measures supporting the path to achieving 2025 financial targets, Alm. Brand appears well-positioned to meet its upgraded guidance for the full year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.