Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Spanish pharmaceutical company Almirall presented its H1 2025 financial results on July 25, 2025, showcasing strong growth driven primarily by its biologics portfolio and European dermatology business. The company’s stock has shown positive momentum recently, with shares trading at €10.76 as of July 24, 2025, up 2.28% and approaching its 52-week high of €11.40.

The H1 results continue the positive trajectory seen in Q1, when the company reported 15% year-on-year sales growth. Almirall’s focus on dermatology, particularly its biologics segment, has positioned it well in a competitive market, with the company reiterating its full-year guidance.

H1 2025 Financial Highlights

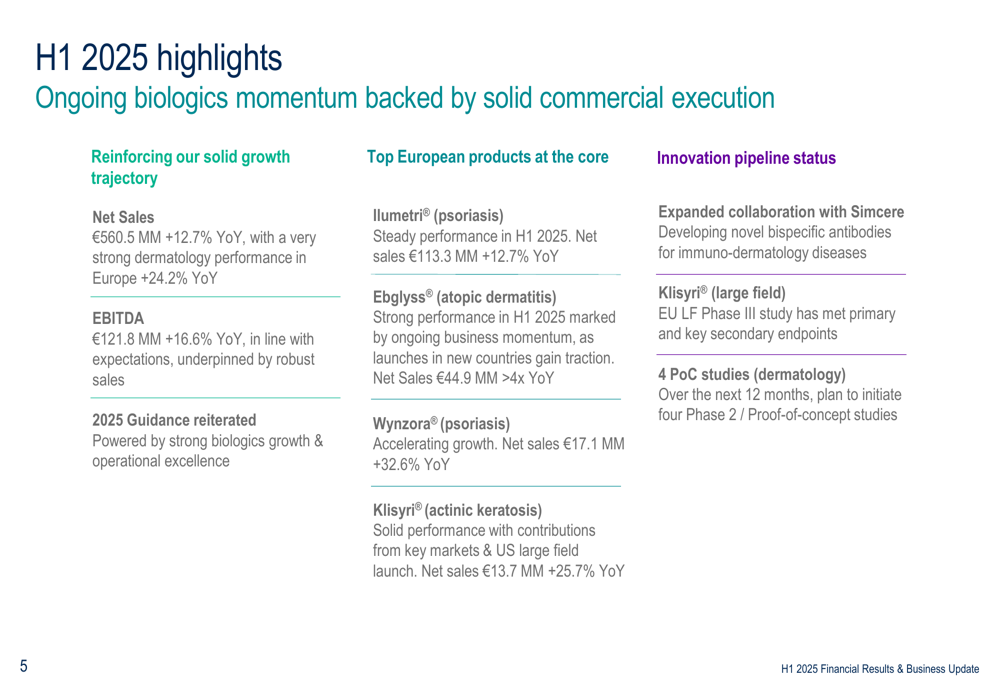

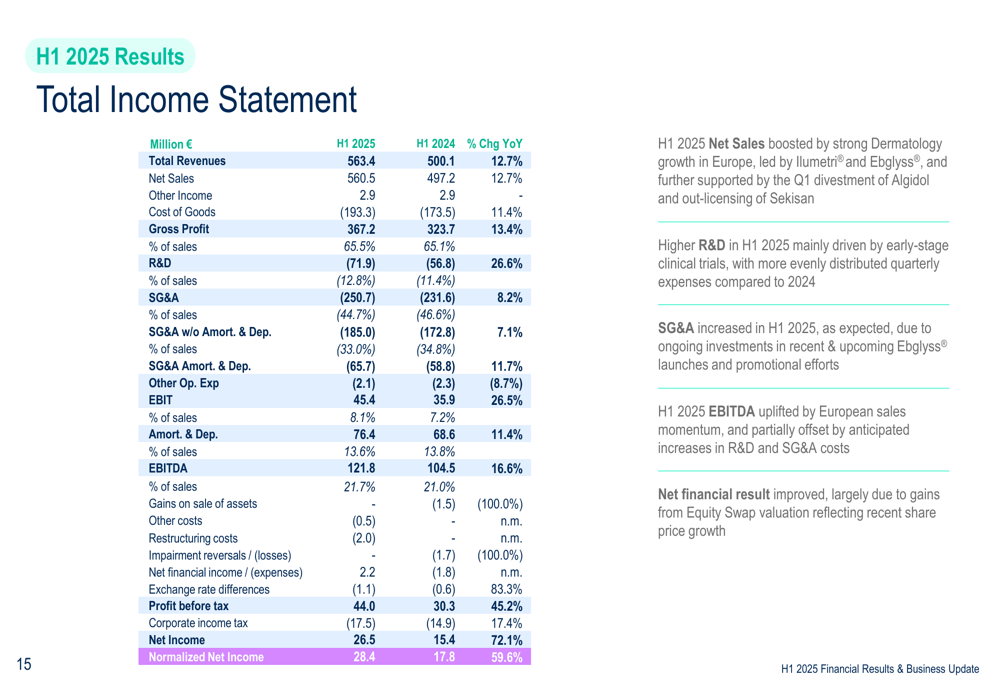

Almirall reported robust financial performance for the first half of 2025, with net sales reaching €560.5 million, representing a 12.7% increase compared to the same period last year. This growth was primarily driven by the company’s European dermatology business, which grew by 24.2% year-on-year.

EBITDA rose to €121.8 million, a 16.6% increase from H1 2024, while net income surged by 72.1% to €26.5 million. The company maintained a solid gross margin of 65.5% and increased its R&D investment to €71.9 million, representing 12.8% of net sales.

As shown in the following comprehensive overview of H1 2025 financial highlights:

The company’s financial position remains strong, with net debt of €76.6 million and a net debt to EBITDA ratio of 0.4x, indicating substantial financial flexibility for future investments and potential acquisitions.

Biologics Growth Drivers

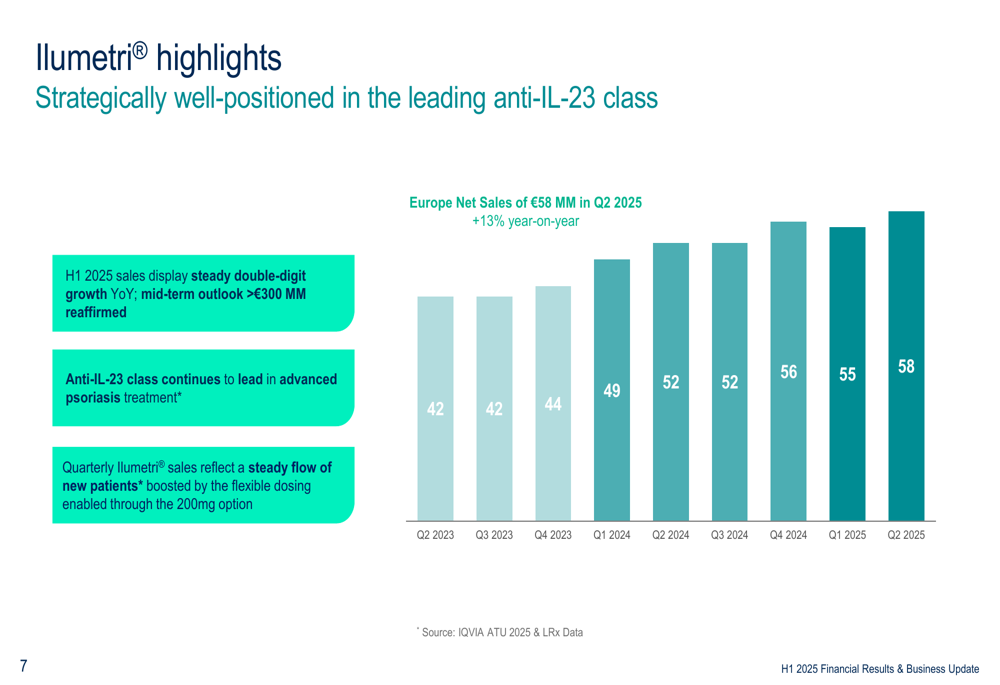

Almirall’s biologics portfolio continues to be the primary growth driver, with Ilumetri® (tildrakizumab) for psoriasis generating sales of €113.3 million, up 12.7% year-on-year. The company reaffirmed its mid-term outlook of achieving more than €300 million in Ilumetri® sales.

The quarterly sales trend for Ilumetri® demonstrates consistent growth, as illustrated in the following chart:

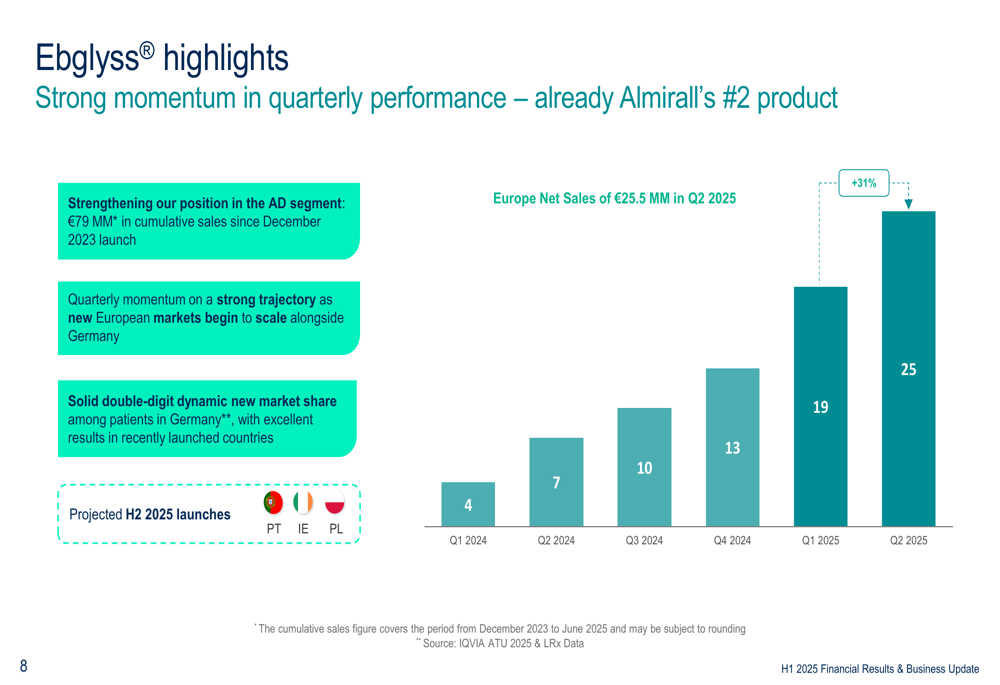

Even more impressive has been the performance of Ebglyss® (lebrikizumab) for atopic dermatitis, which generated €44.9 million in sales during H1 2025, more than quadrupling compared to the same period last year. Ebglyss® has quickly become Almirall’s second-largest product, with cumulative sales of €79 million since its December 2023 launch.

The rapid growth trajectory of Ebglyss® is clearly demonstrated in the following quarterly sales chart:

Other key dermatology products also performed well, with Wynzora® (psoriasis) sales increasing by 32.6% to €17.1 million and Klisyri® (actinic keratosis) growing by 25.7% to €13.7 million.

Regional Performance Analysis

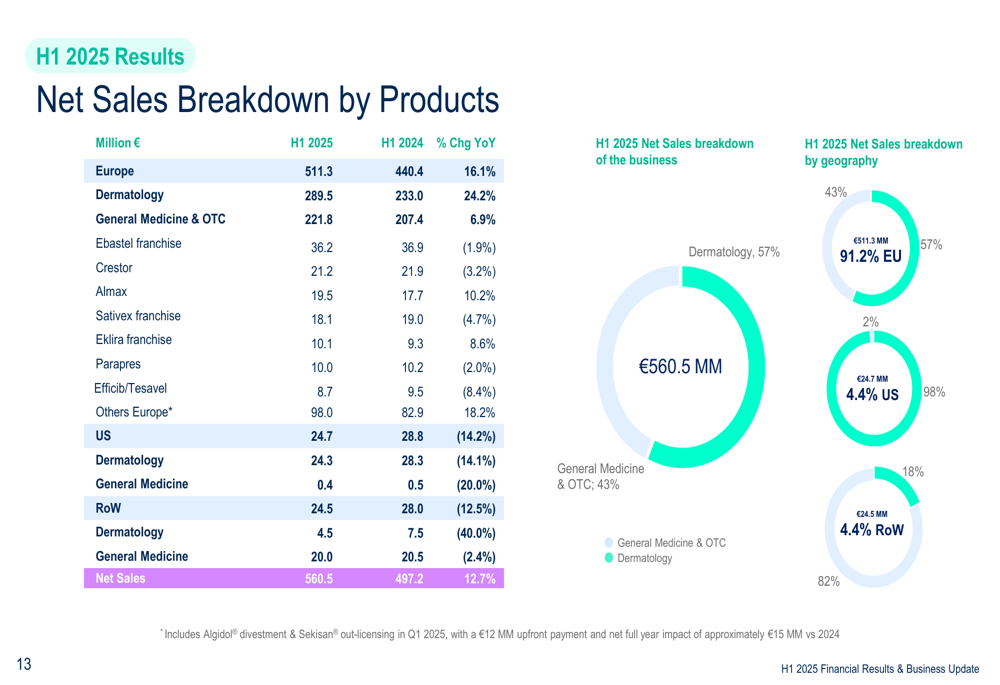

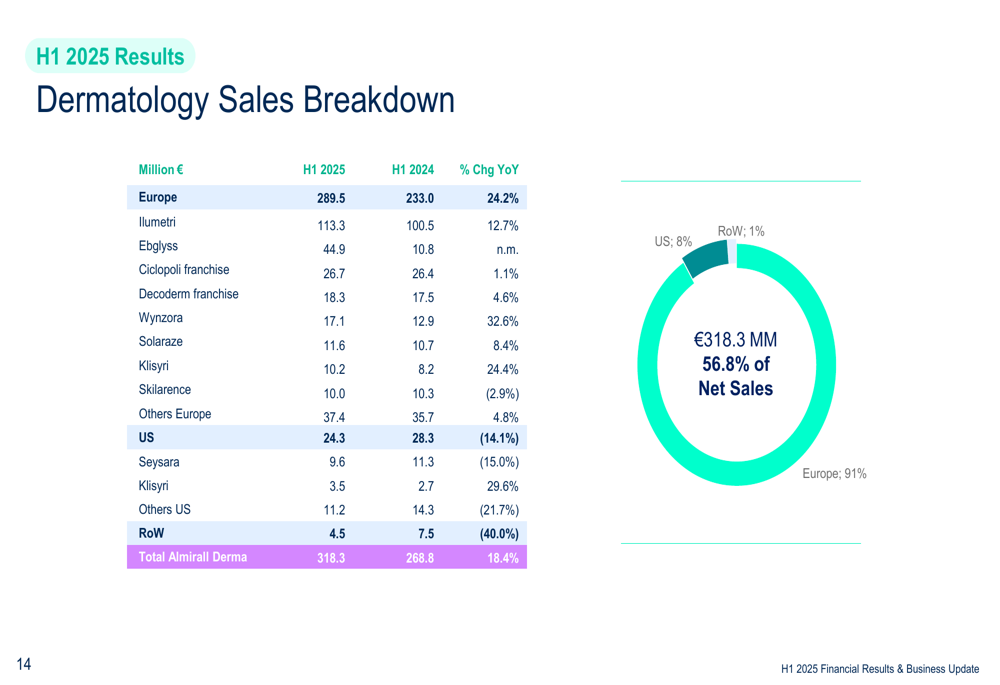

Almirall’s performance shows significant geographic variation, with Europe driving growth while the US and rest of world markets faced challenges. European sales increased by 16.1% to €511.3 million, with dermatology sales in the region surging by 24.2% to €289.5 million.

In contrast, US sales declined by 14.2% to €24.7 million, while rest of world sales decreased by 12.5% to €24.5 million. Europe now accounts for 91.2% of Almirall’s total net sales, highlighting both the company’s strength in its home market and its dependence on the region.

The following breakdown illustrates Almirall’s sales by business segment and geography:

Within the dermatology segment, which now represents 56.8% of total net sales, the company’s performance was primarily driven by its European operations, as shown in this detailed breakdown:

Pipeline and R&D Updates

Almirall continues to invest significantly in research and development, with R&D expenses increasing by 26.6% year-on-year to €71.9 million in H1 2025. The company plans to initiate four Phase 2 proof-of-concept studies in dermatology, reinforcing its commitment to innovation in this therapeutic area.

Key pipeline developments include the expansion of its collaboration with Simcere for bispecific antibodies and positive results from the EU Phase III study for Klisyri® in large field actinic keratosis, which met both primary and key secondary endpoints.

The company’s pipeline includes several promising candidates across various development stages, targeting conditions such as psoriatic arthritis, atopic dermatitis, hidradenitis suppurativa, and rare dermatological diseases.

Management Changes and Outlook

Almirall announced a key leadership change with the appointment of Jon U. Garay Alonso as the new CFO and Executive VP. Garay joins from Camurus AB, a publicly listed Swedish pharmaceutical and biotechnology company, and will report directly to Carlos Gallardo, Almirall’s Chairman and CEO.

Looking ahead, the company reiterated its 2025 guidance, expressing confidence in continued growth driven by its biologics portfolio and operational excellence. Almirall remains focused on its strategic priorities, which include capitalizing on market opportunities in dermatology, enhancing its platform to unlock long-term value, and driving accelerated growth through disciplined strategy execution.

The company’s total income statement provides a comprehensive view of its financial performance:

Conclusion

Almirall’s H1 2025 results demonstrate strong performance, particularly in its core European dermatology business. The company’s biologics portfolio, led by Ilumetri® and Ebglyss®, continues to drive growth, offsetting challenges in the US and other international markets.

With a solid financial position, ongoing R&D investments, and clear strategic focus on dermatology, Almirall appears well-positioned to maintain its growth trajectory. However, the company’s heavy reliance on the European market and the need to address declining sales in the US and other regions represent potential challenges that management will need to address to ensure sustainable long-term growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.