Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

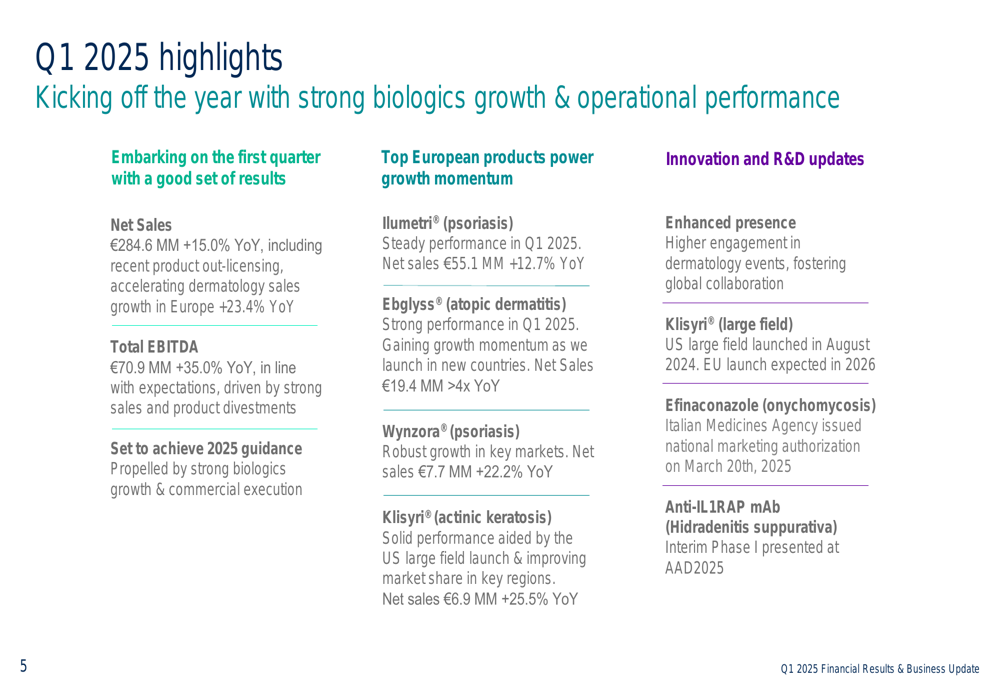

Almirall (BME:ALM) reported strong first-quarter 2025 results on May 12, with net sales increasing 15% year-over-year to €284.6 million, though slightly missing analyst expectations of €287.3 million. Despite this minor shortfall, investors responded positively, with shares rising 8.22% to €10.66, approaching the company’s 52-week high of €10.70.

The Spanish pharmaceutical company’s performance was primarily driven by its expanding dermatology portfolio, particularly its biologics segment, and strategic product launches across European markets. The company maintained its full-year 2025 guidance, expressing confidence in its growth trajectory.

Quarterly Performance Highlights

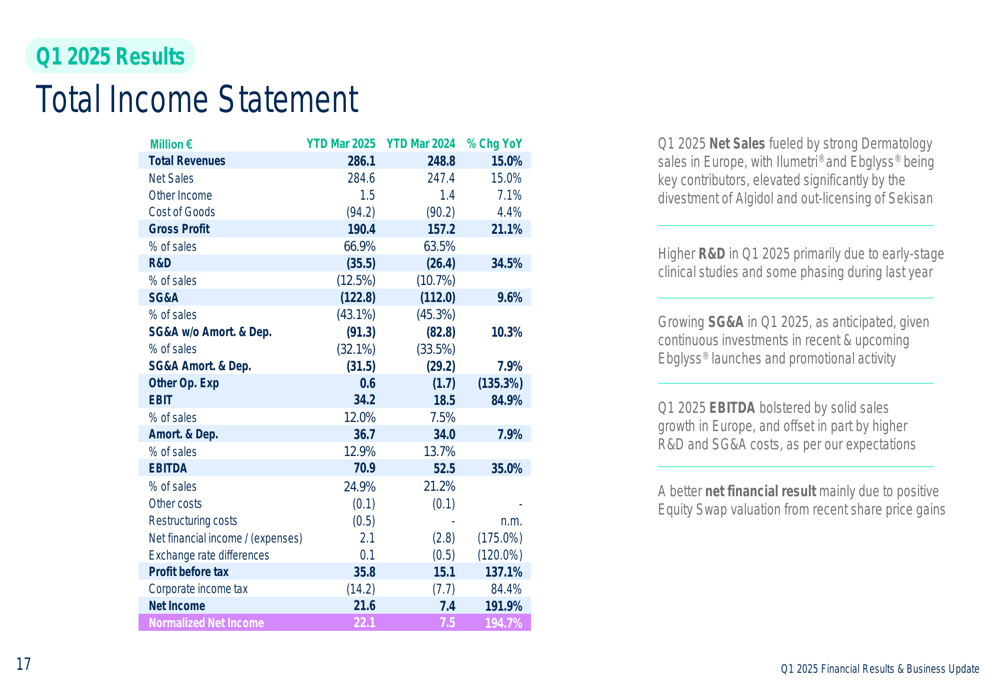

Almirall’s Q1 2025 results demonstrated strong momentum across key financial metrics, with total EBITDA increasing 35% year-over-year to €70.9 million. European dermatology sales were particularly impressive, growing 23.4% compared to Q1 2024.

As shown in the following comprehensive overview of Q1 2025 performance:

The company’s gross margin reached 66.9%, positively impacted by recent product divestments. R&D investment increased 34.5% year-over-year to €35.5 million, representing 12.5% of net sales, while SG&A expenses rose 9.6% to €122.8 million, reflecting continued investment in the ongoing rollout of Ebglyss®.

Biologics Growth Drivers

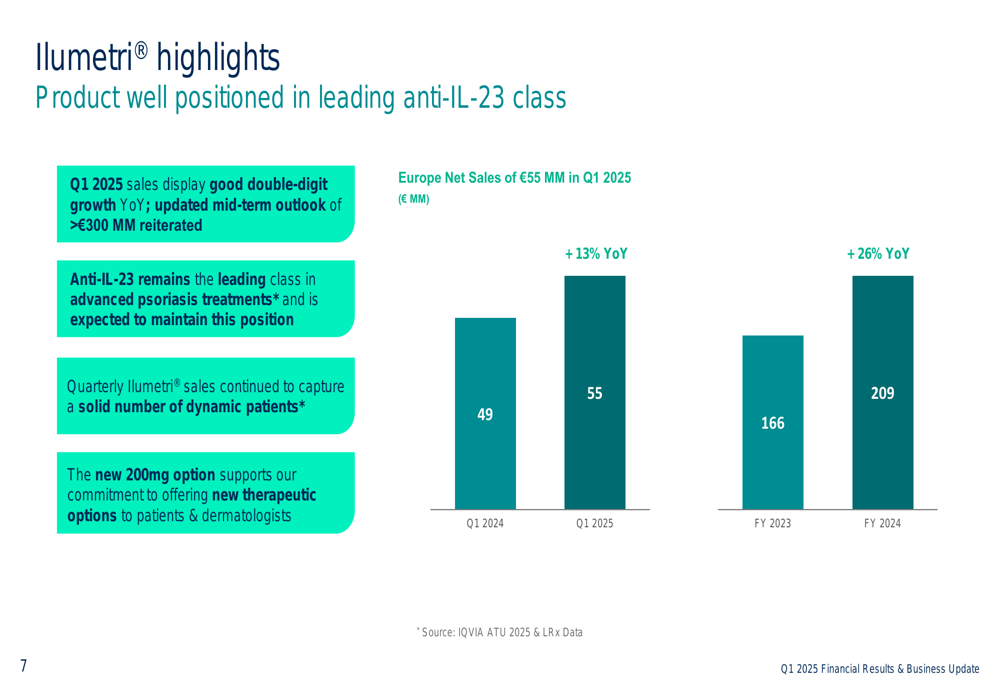

Almirall’s biologics portfolio continues to be a significant growth driver, with Ilumetri® (tildrakizumab) for psoriasis generating €55.1 million in Q1 2025, up 12.7% year-over-year. The company reiterated its mid-term outlook of achieving more than €300 million in Ilumetri® sales.

The following chart illustrates Ilumetri’s consistent growth trajectory:

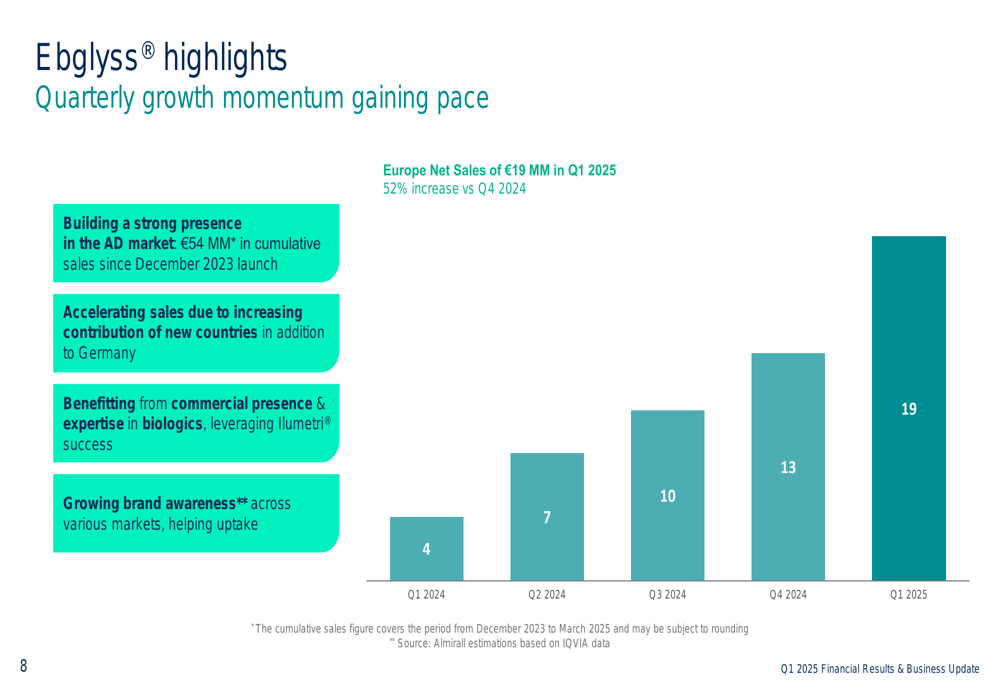

Even more impressive was the performance of Ebglyss® (lebrikizumab) for atopic dermatitis, which generated €19.4 million in Q1 2025, more than quadrupling compared to the same period last year. The product has achieved €54 million in cumulative sales since its December 2023 launch.

As shown in this chart of Ebglyss® quarterly performance:

Other key dermatology products also showed strong growth, with Wynzora® (psoriasis) increasing 22.2% to €7.7 million and Klisyri® (actinic keratosis) growing 25.5% to €6.9 million.

Geographic Expansion

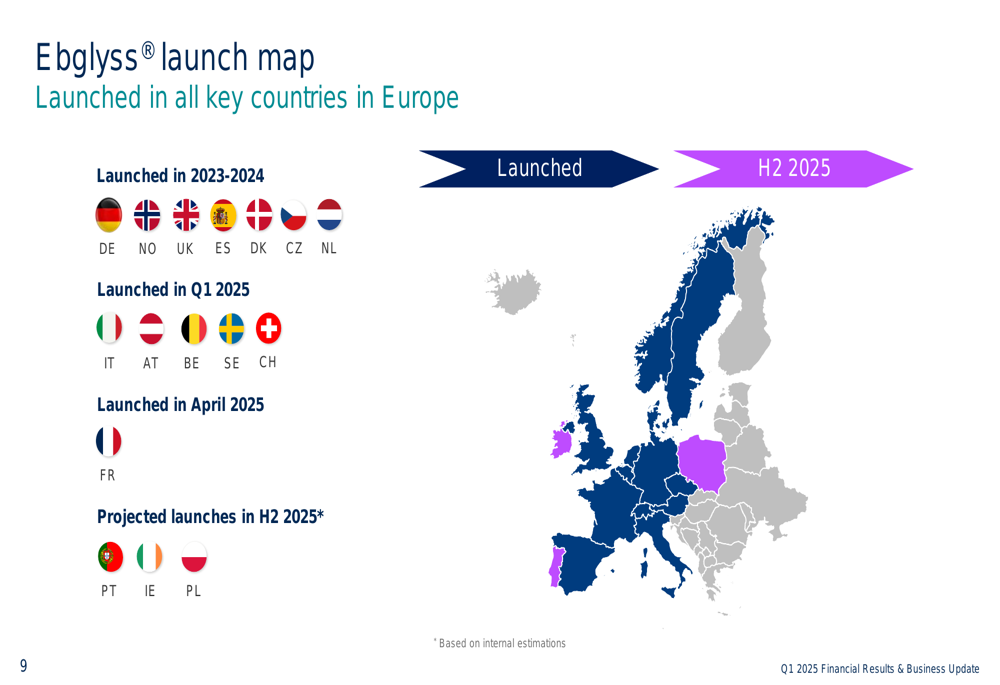

A key element of Almirall’s growth strategy is the continued geographic expansion of Ebglyss® across European markets. The product has now been launched in 13 European countries, with additional launches planned for the second half of 2025.

The following map illustrates Almirall’s phased launch strategy for Ebglyss®:

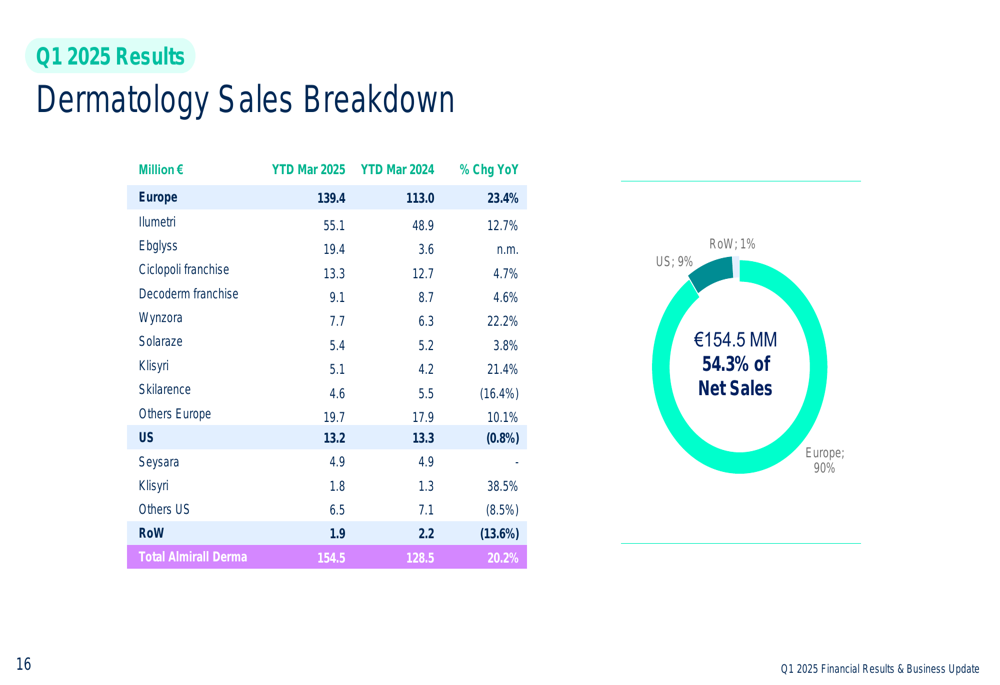

Europe remains Almirall’s primary market, accounting for 91.4% of total net sales, with the US and rest of world contributing 4.7% and 3.9%, respectively. Within Europe, dermatology products represented 54% of total sales, underscoring the company’s strategic focus on this therapeutic area.

Pipeline & R&D

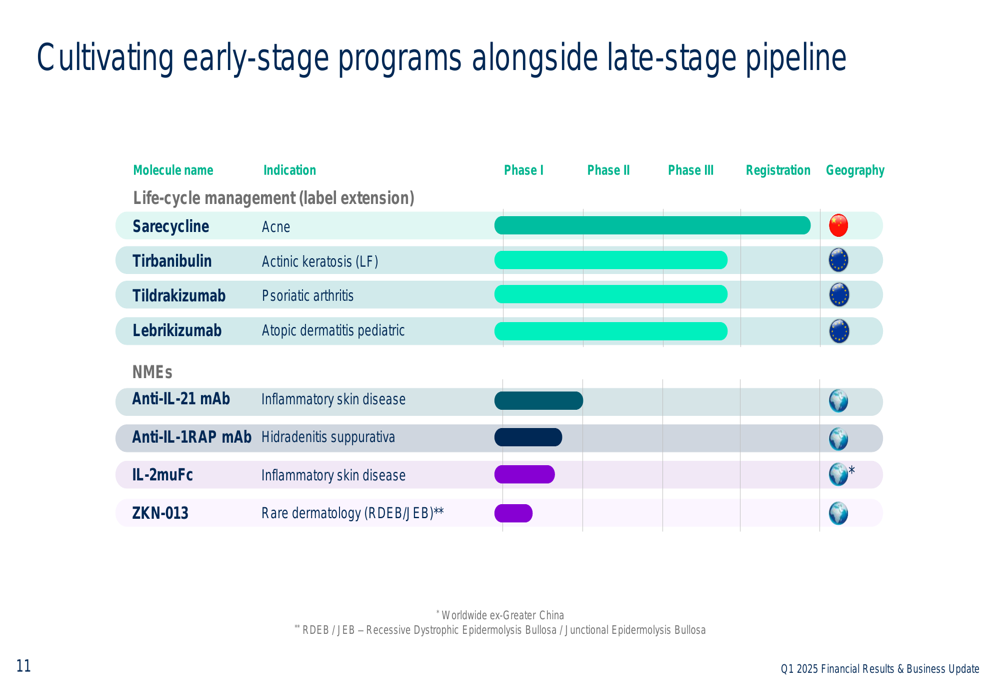

Almirall continues to invest in its pipeline, with multiple molecules in various stages of development. The company’s R&D efforts focus on both life-cycle management of existing products and new molecular entities for dermatological conditions.

The following overview illustrates Almirall’s current pipeline:

Notable pipeline developments include the Phase III studies for tirbanibulin in actinic keratosis (large field), tildrakizumab in psoriatic arthritis, and lebrikizumab in pediatric atopic dermatitis. The company is also advancing several early-stage candidates, including an anti-IL-1RAP monoclonal antibody for hidradenitis suppurativa, which was presented at the American Academy of Dermatology 2025 meeting.

Detailed Financial Analysis

A closer examination of Almirall’s financial performance reveals strong growth across most product categories and geographic regions. The company’s net sales breakdown highlights the importance of European operations and the increasing contribution from dermatology products.

The following table provides a detailed breakdown of net sales by product category and geography:

Within the dermatology segment, which now represents 54.3% of total net sales, European markets dominate with 90% of dermatology sales, as illustrated in this breakdown:

Almirall’s income statement shows solid performance across key metrics, with total revenues of €286.1 million (+15.0% YoY) and net income of €21.6 million:

Financial Position

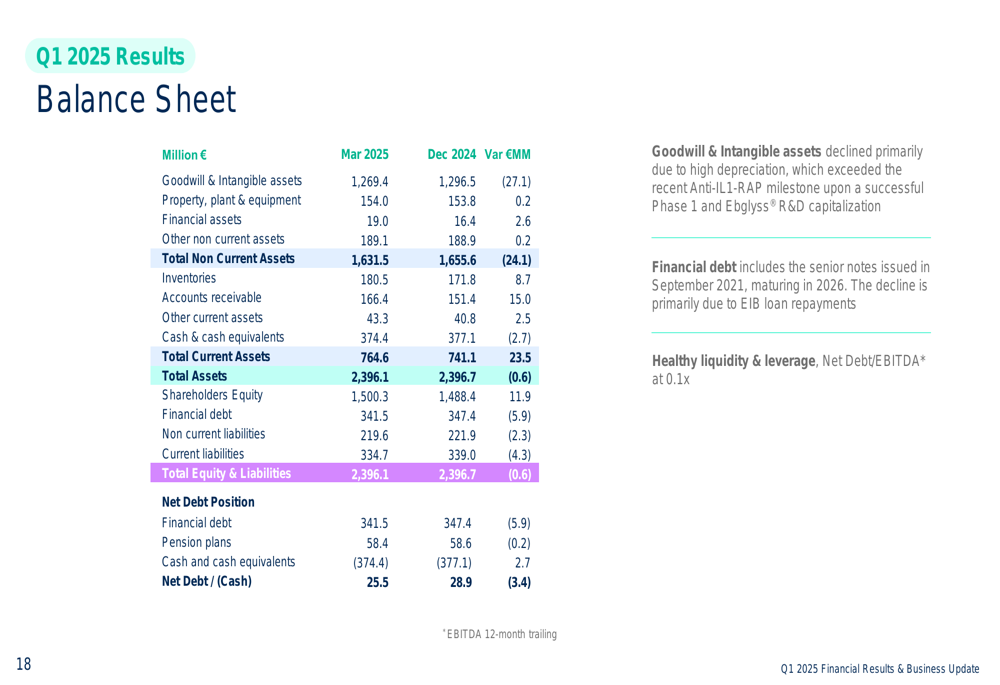

Almirall maintains a strong financial position with €374.4 million in cash and cash equivalents and a net debt of just €25.5 million as of March 2025. The company’s net debt to EBITDA ratio stands at a very conservative 0.1x, providing significant flexibility for potential inorganic growth opportunities.

The following balance sheet summary illustrates Almirall’s financial strength:

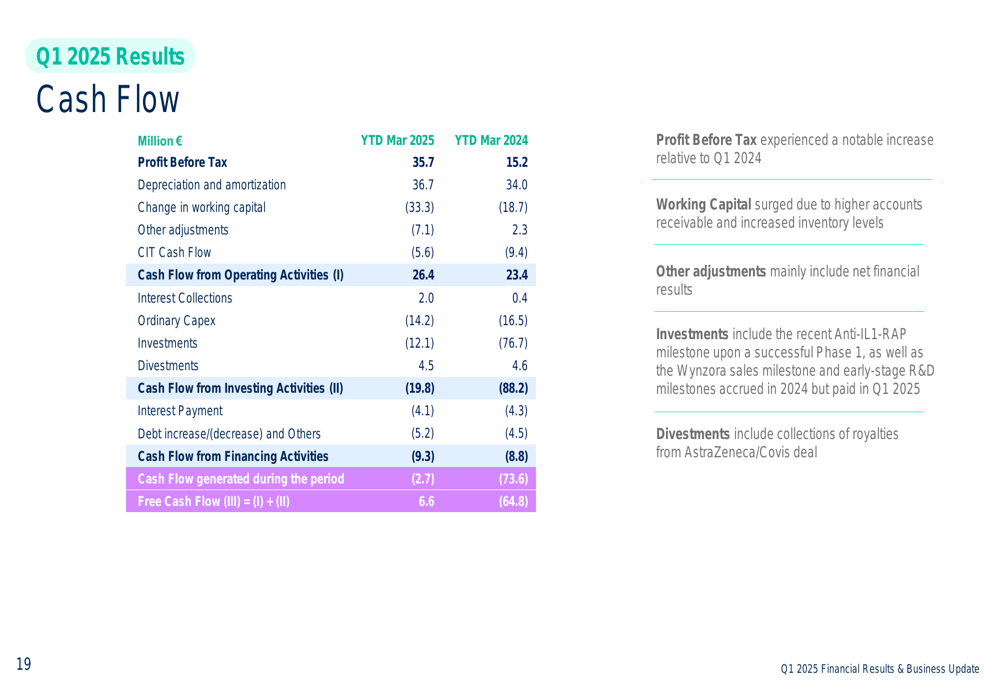

Cash flow from operating activities reached €26.4 million in Q1 2025, while free cash flow was €6.6 million after accounting for investing activities:

Forward-Looking Statements

Almirall confirmed it remains on track to achieve its 2025 guidance, propelled by biologics growth and commercial execution. The company is positioning itself to "excel in dermatology in the next decade and beyond" by seizing market opportunities in dermatology, enhancing its platform, and accelerating growth.

According to CEO Carlos Gallardo, "We are excited to lead Almirall into the next phase of our journey towards becoming leaders in medical dermatology." The company is targeting double-digit net sales CAGR by 2023 and aims for a 25% EBITDA margin by 2028.

Despite the positive outlook, investors should consider potential risks highlighted in the earnings call, including competitive pressures in the dermatology market, regulatory challenges in new markets, and the company’s dependence on key products like Ilumetri® and Ebglyss® for growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.