Missed the webinar? Here are Investing.com’s top 10 stock picks for 2026

Introduction & Market Context

Alpha Metallurgical Resources Inc (NYSE:AMR) released its investor presentation on November 6, 2025, coinciding with its third-quarter earnings announcement that revealed significant challenges. The stock dropped 6.6% in premarket trading following an earnings miss, with shares falling from $173.99 to $162.51, moving closer to its 52-week low of $97.41 than its high of $255.04.

The company reported Q3 earnings per share of -$0.3157, missing analyst expectations of -$0.2525, while revenue came in at $526.78 million, below the forecasted $550.75 million. This performance stands in contrast to the confident positioning in the company's presentation, highlighting the volatile nature of the metallurgical coal market.

Executive Summary

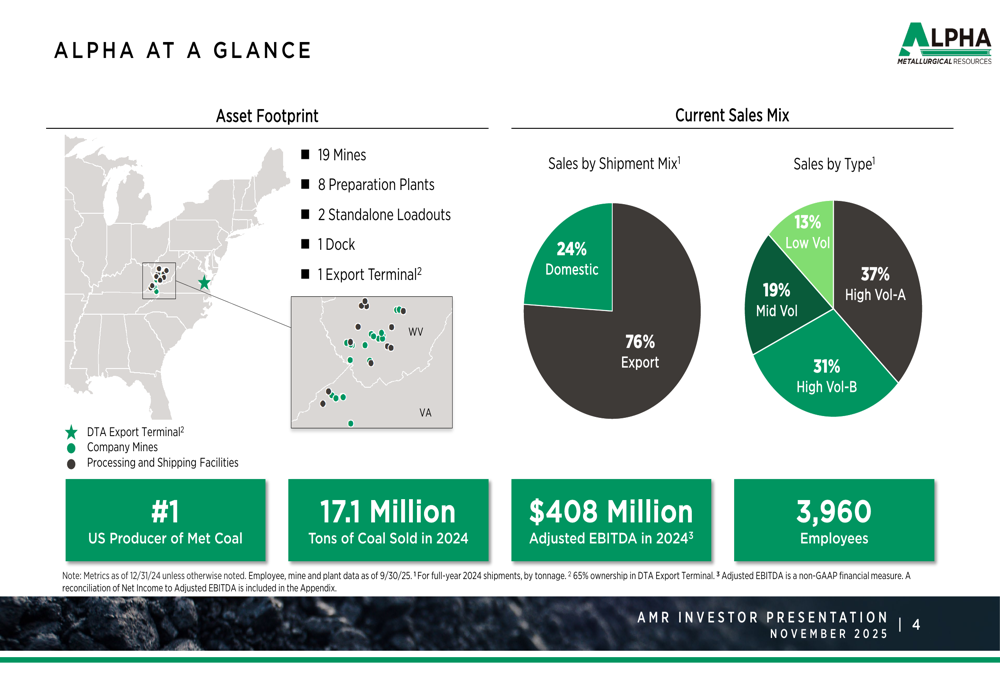

Alpha Metallurgical Resources positions itself as the largest and most diverse metallurgical coal supplier in the United States, with a production footprint spanning 19 mines and 8 preparation plants across the Eastern US. The company sold 17.1 million tons of coal in 2024, generating $2.9 billion in revenue and $408 million in Adjusted EBITDA.

As shown in the following overview of Alpha's key metrics and operational footprint:

Despite these impressive credentials, Alpha's recent financial performance reflects industry-wide challenges. CEO Andy Eidson acknowledged during the earnings call that the company is "anticipating what we believe could be another challenging year for the coal industry" in 2026, suggesting ongoing headwinds despite the optimistic long-term market outlook presented in the investor materials.

Competitive Industry Position

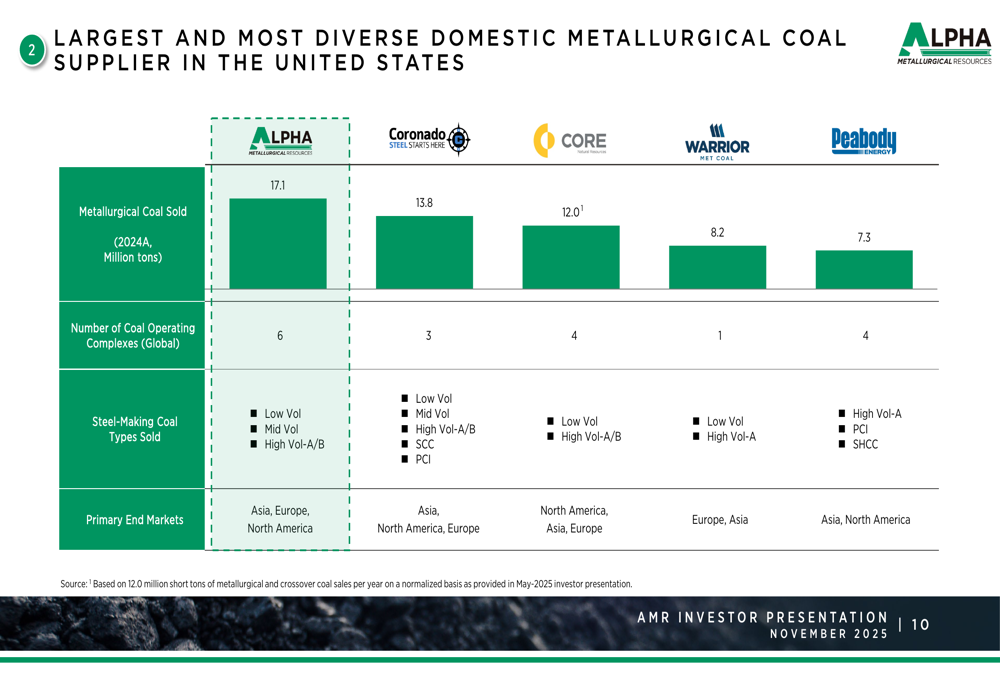

Alpha's presentation emphasizes its market leadership position compared to competitors like Coronado, CORE, Warrior, and Peabody. The company outpaces its peers in metallurgical coal sales volume and offers a more diverse product portfolio spanning low volatility, mid volatility, high volatility-A/B, and PCI coal types.

This competitive positioning is clearly illustrated in the following comparison:

The company's strategic asset locations, particularly its ownership stake in the Dominion Terminal Associates (DTA) coal export terminal in Newport News, VA, provide Alpha with significant advantages in serving both domestic and international markets. In 2024, the company sold 13 million tons internationally across 26 countries, with exports representing 76% of total shipments.

The strategic importance of these assets is highlighted in this overview:

Detailed Financial Analysis

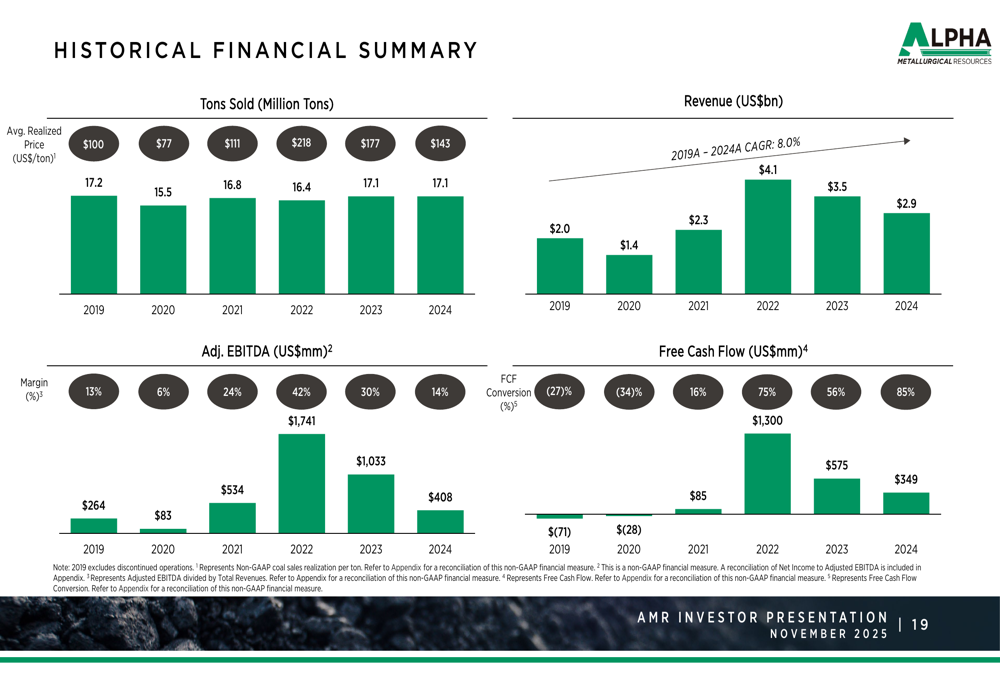

Alpha's presentation showcases a positive long-term financial trajectory, with revenue growing from $2.0 billion in 2019 to $2.9 billion in 2024, representing an 8.0% compound annual growth rate. However, this contrasts with the company's recent quarterly performance, where Adjusted EBITDA fell to $41.7 million in Q3 2025, down from $46.1 million in the previous quarter.

The historical financial performance is summarized in the following chart:

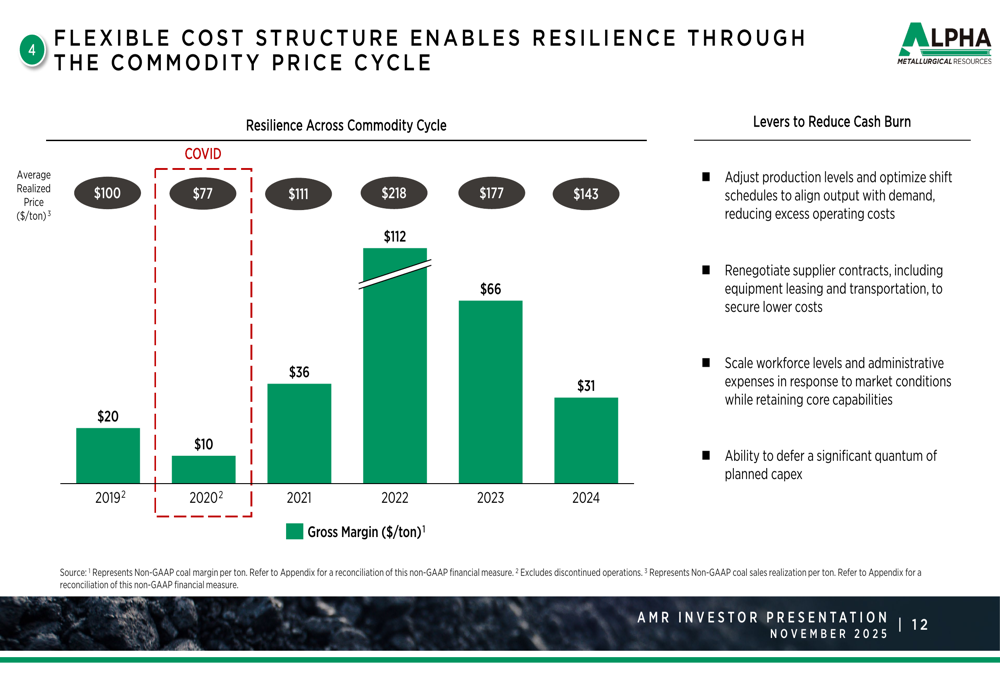

One bright spot in Alpha's recent performance has been its success in cost management. The company reported that cost of coal sales reached a record low since 2021 at $97.27 per ton in Q3 2025. This aligns with the presentation's emphasis on a flexible cost structure that enables resilience through commodity price cycles.

The company's approach to managing costs through market volatility is illustrated here:

Strategic Initiatives

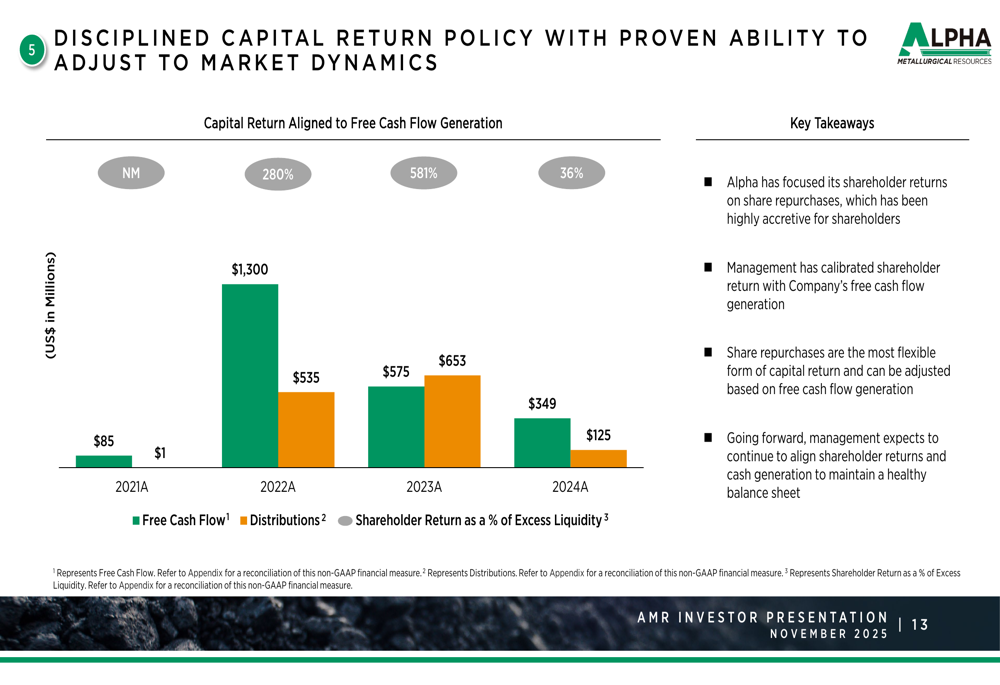

Alpha's presentation outlines a disciplined capital allocation strategy focused on maintaining balance sheet strength while returning value to shareholders primarily through share repurchases. The company emphasizes that this approach provides flexibility to adjust to market conditions, which has proven valuable given recent challenges.

The capital return strategy is detailed in the following chart showing the relationship between free cash flow generation and shareholder returns:

A key strategic initiative highlighted in the presentation is the development of the Kingston Wildcat mine, which is expected to produce low-volatile metallurgical coal with first production anticipated in late 2025. This project represents Alpha's ongoing investment in high-quality reserves despite market headwinds.

Forward-Looking Statements

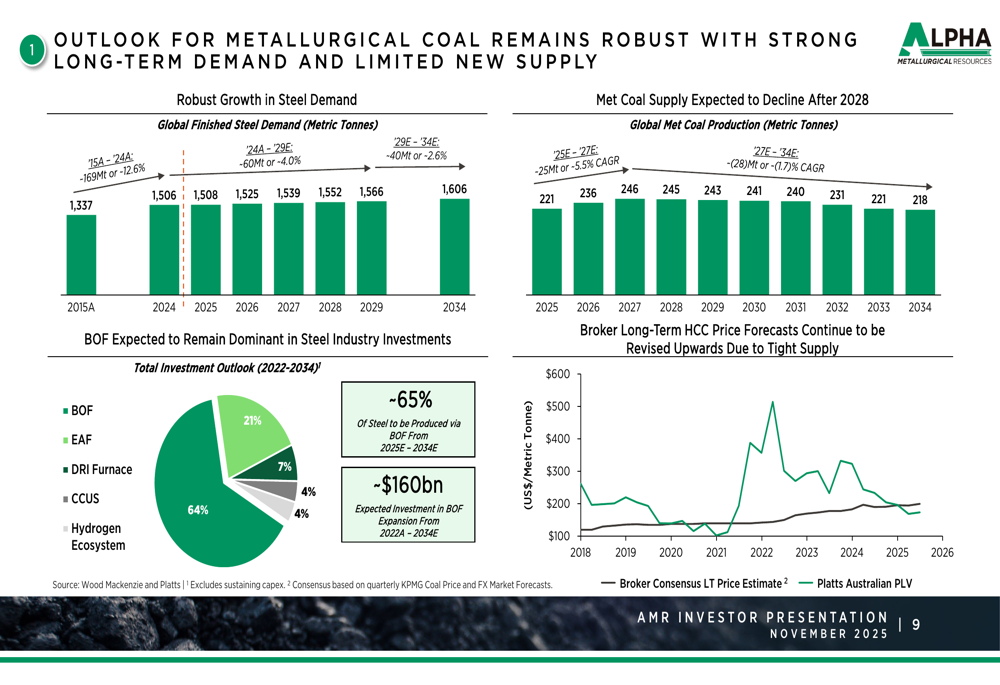

While Alpha's presentation paints an optimistic picture of the metallurgical coal market outlook with robust steel demand growth projected through 2034, the company's recent earnings call struck a more cautious tone. Management indicated they are preparing for potentially challenging conditions in 2026, with domestic contract negotiations pending.

The market outlook presented in the investor materials shows expected growth in steel demand contrasted with declining metallurgical coal supply after 2028:

Alpha maintains a strong liquidity position with $408.5 million in unrestricted cash, which provides a buffer against continued market volatility. The company's focus on operational efficiency and cost discipline will be crucial as it navigates what management describes as potential ongoing challenges in the coal industry.

President and COO Jason Whitehead emphasized during the earnings call that the company remains committed to its core metallurgical coal business, stating, "We are pretty happy mining metallurgical coal. If something else pops up, that will be great. That is really not our strategic intent at this moment."

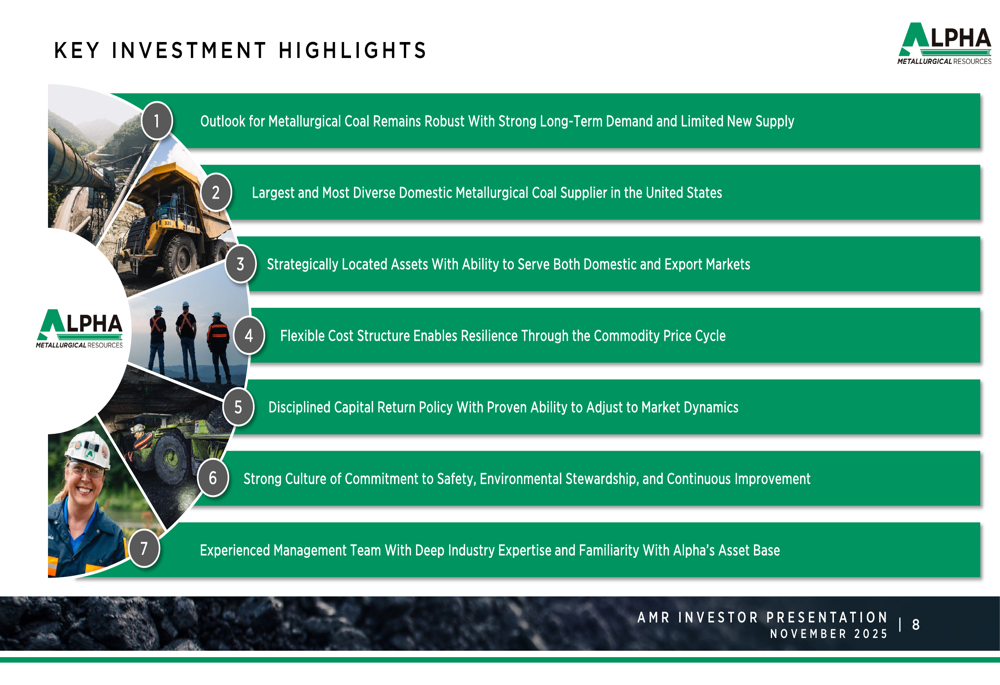

Alpha's investment highlights summarize the company's value proposition despite near-term challenges:

As Alpha Metallurgical Resources balances its long-term strategic positioning against current market realities, investors will be watching closely to see if the company's industry leadership and operational flexibility can overcome the headwinds facing the metallurgical coal sector in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.