BofA warns Fed risks policy mistake with early rate cuts

Introduction & Market Context

Alpine Income Property Trust (NYSE:PINE) released its second quarter 2025 investor presentation on July 25, highlighting its growing portfolio of retail net lease properties and emphasizing its discounted valuation relative to peers. The presentation comes after a challenging first quarter where the company missed earnings expectations, with the stock currently trading at $14.46, down 1.52% in the most recent session but showing signs of recovery with a 5.05% gain in premarket trading.

The company’s presentation positions Alpine Income as an undervalued investment opportunity in the net lease REIT sector, with a focus on its high-quality tenant base, growing dividend, and attractive valuation metrics compared to industry peers.

Portfolio Highlights

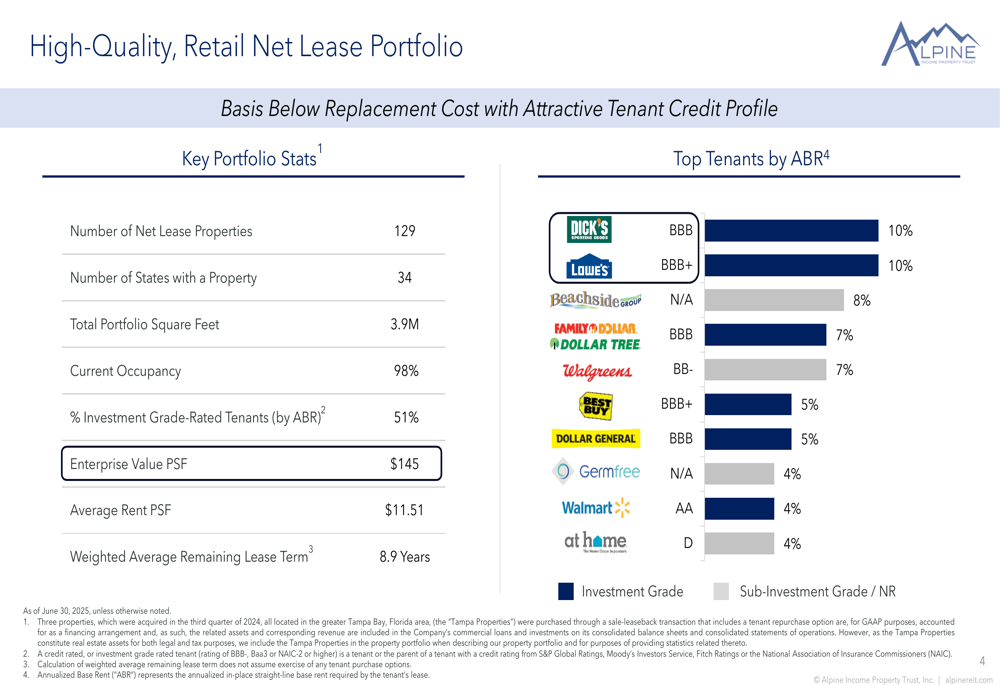

Alpine Income’s portfolio has grown substantially since its 2019 IPO, now comprising 129 properties across 34 states with 3.9 million total square feet and a 98% occupancy rate. The company emphasizes its high-quality tenant base, with 51% of annualized base rent (ABR) coming from investment grade-rated tenants.

As shown in the following portfolio overview chart, the company’s top tenants include Dick’s Sporting Goods (NYSE:DKS) (BBB, 10%), Lowe’s (NYSE:LOW) (BBB+, 10%), and Beachside Restaurant Group (LON:RTN) (8%), with a weighted average lease term of 8.9 years:

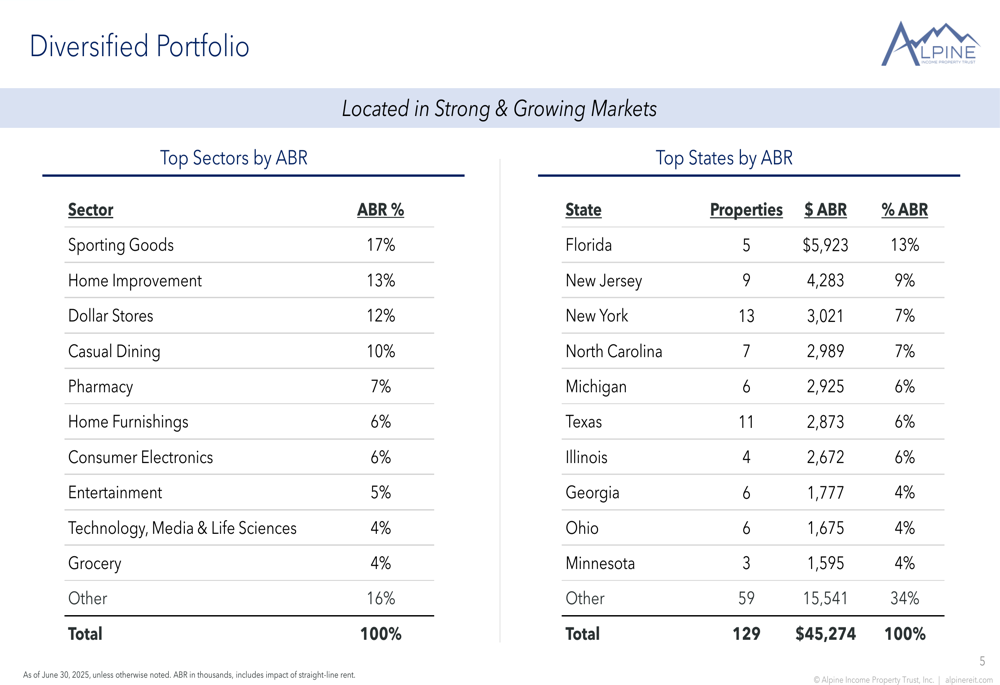

The portfolio is diversified across various retail sectors and geographic locations, with sporting goods (17%), home improvement (13%), and dollar stores (12%) representing the largest sector concentrations. Florida leads state exposure at 13% of ABR, followed by New Jersey (9%) and New York (7%).

The following chart illustrates the company’s sector and state diversification:

Alpine Income highlights its significant growth and diversification since its IPO, noting improvements in key metrics such as the reduction in concentration risk (top tenant reduced from 21% to 10% of ABR) and increased percentage of investment grade tenants (from 36% to 51%):

Financial Performance & Valuation

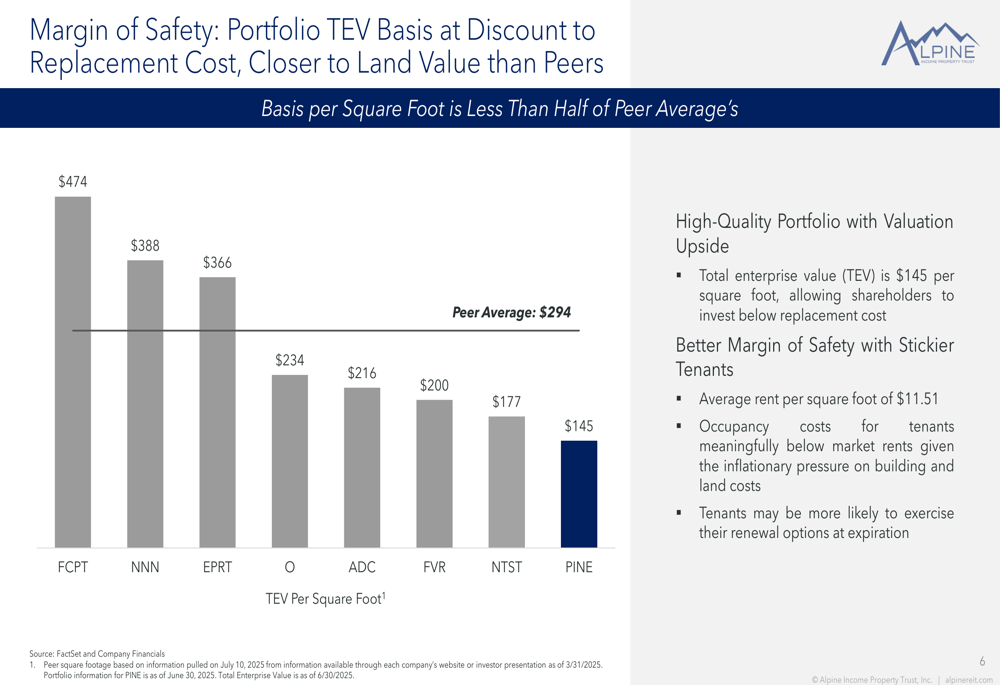

A central theme of Alpine’s presentation is its attractive valuation relative to peers. The company emphasizes its total enterprise value of $145 per square foot, which is less than half the peer average of $294, positioning the portfolio at a significant discount to replacement cost:

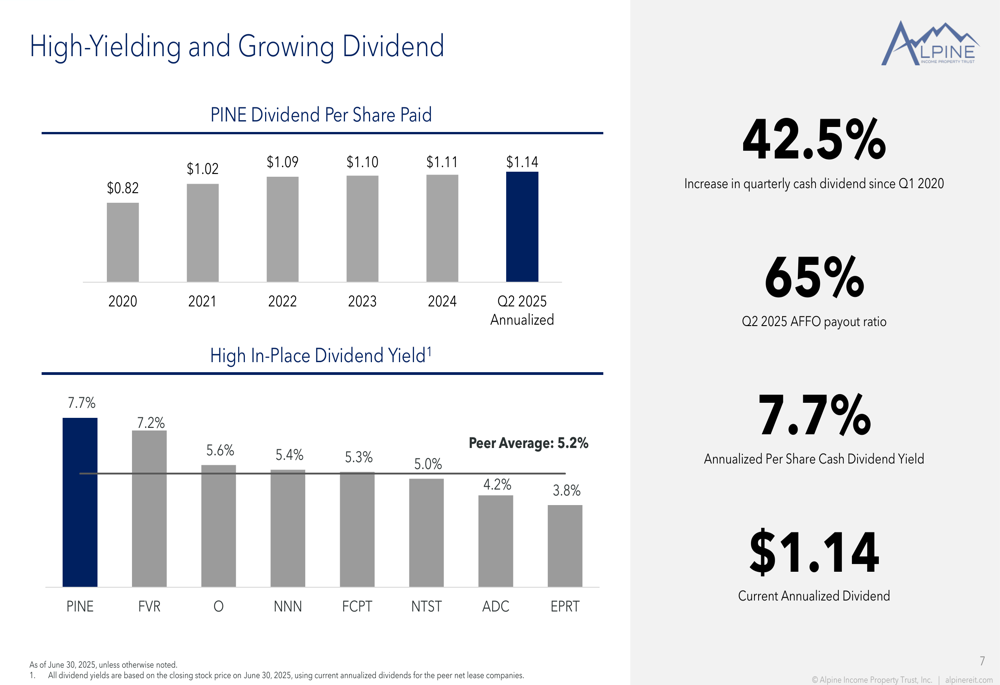

The company also highlights its dividend yield of 7.7%, which is substantially higher than the peer average of 5.2%, while maintaining a lower AFFO payout ratio of 64% compared to the peer average of 70%:

Alpine Income trades at an AFFO multiple of 8.3x, well below the peer average of 14.0x, suggesting potential valuation upside if the gap were to narrow:

These valuation metrics align with information from the recent earnings report, which noted the company’s 7% dividend yield and consecutive dividend increases over six years. However, the presentation doesn’t directly address the Q1 2025 earnings miss (-$0.08 vs expected $0.02) that contributed to recent stock price pressure.

Strategic Positioning

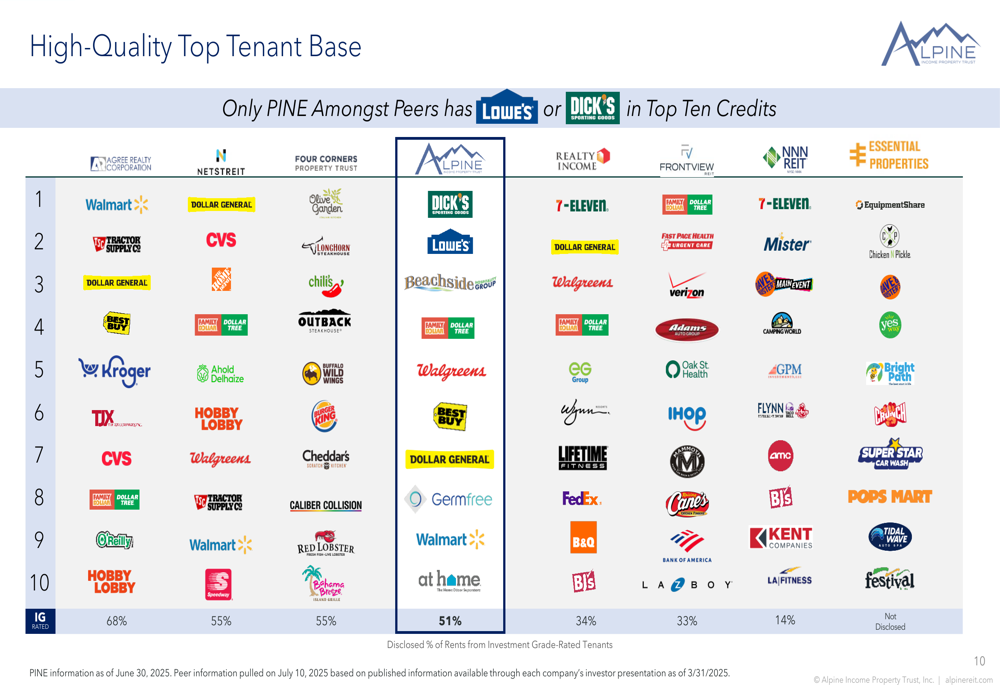

Alpine Income emphasizes several competitive advantages in its presentation, including its high-quality tenant base. The company notes it is the only REIT among its peers with both Dick’s Sporting Goods and Lowe’s in its top ten tenants:

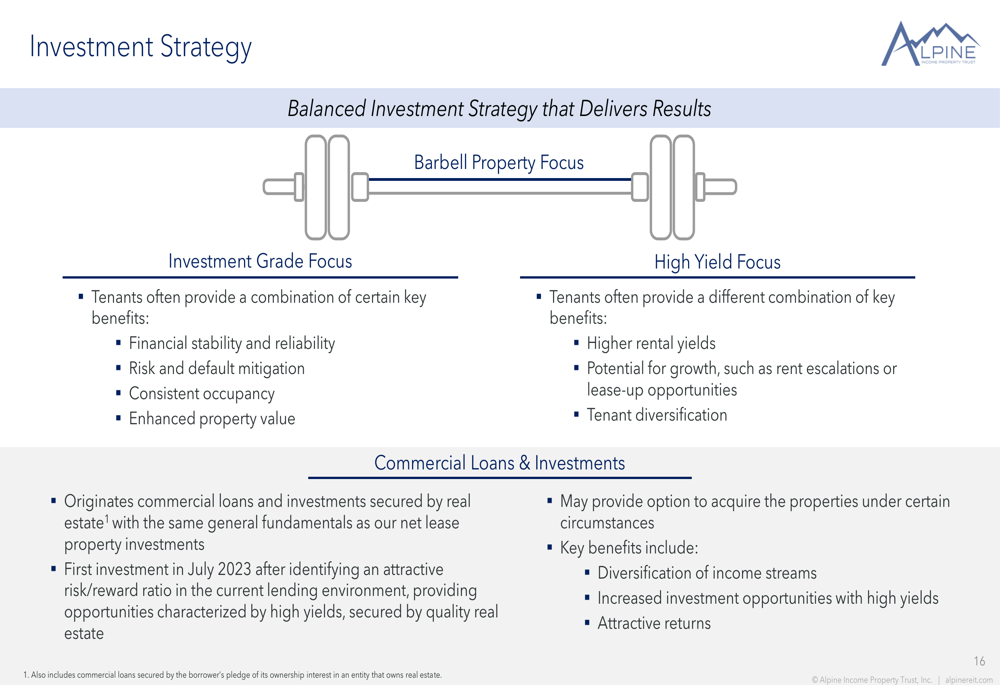

The company’s investment strategy balances investment-grade tenants for stability with higher-yield opportunities for growth, complemented by a commercial loan portfolio that provides diversification and attractive returns:

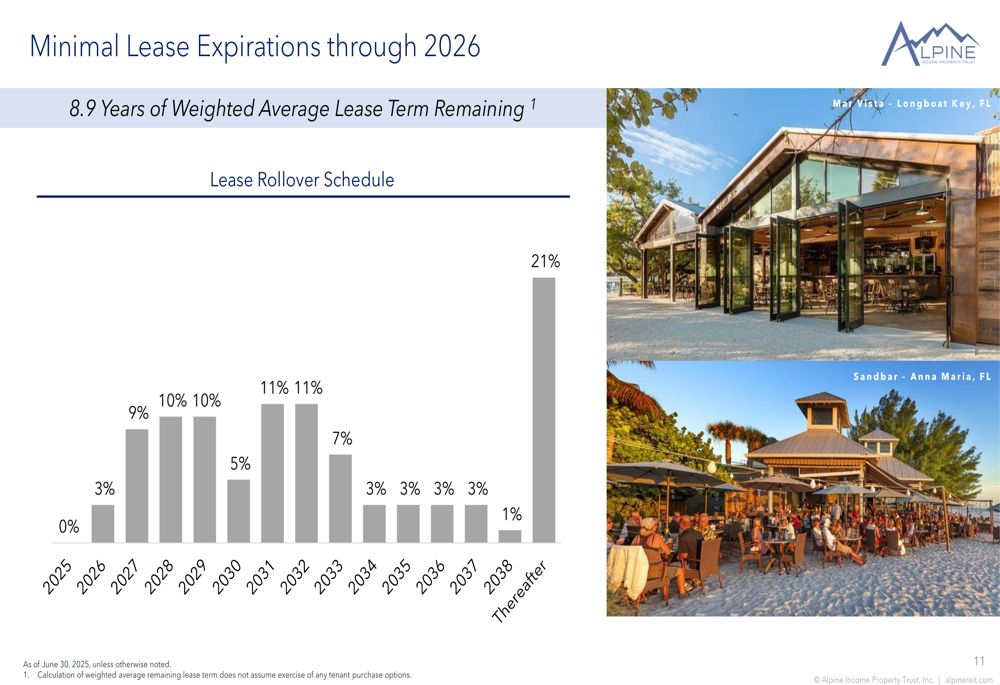

Alpine Income also highlights its minimal lease expirations through 2026, with only 3% of leases expiring in 2025 and none in 2026, providing near-term cash flow stability:

Capital Structure & Outlook

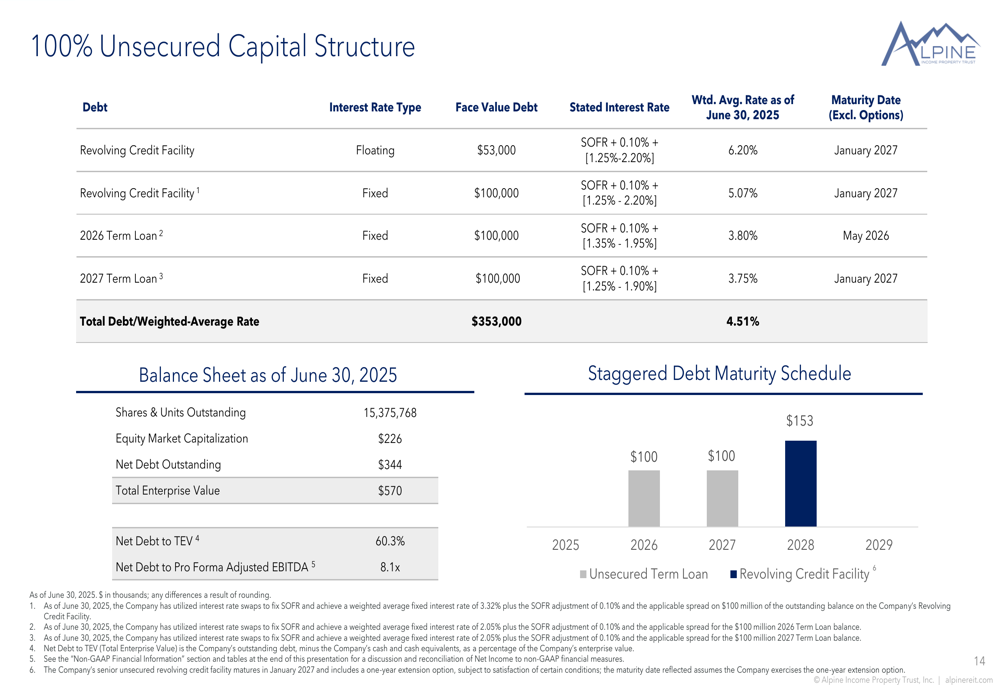

The presentation details Alpine Income’s 100% unsecured capital structure with $353 million in total debt at a weighted average interest rate of 4.51%. The company reports a net debt to total enterprise value ratio of 60.3% and net debt to pro forma adjusted EBITDA of 8.1x:

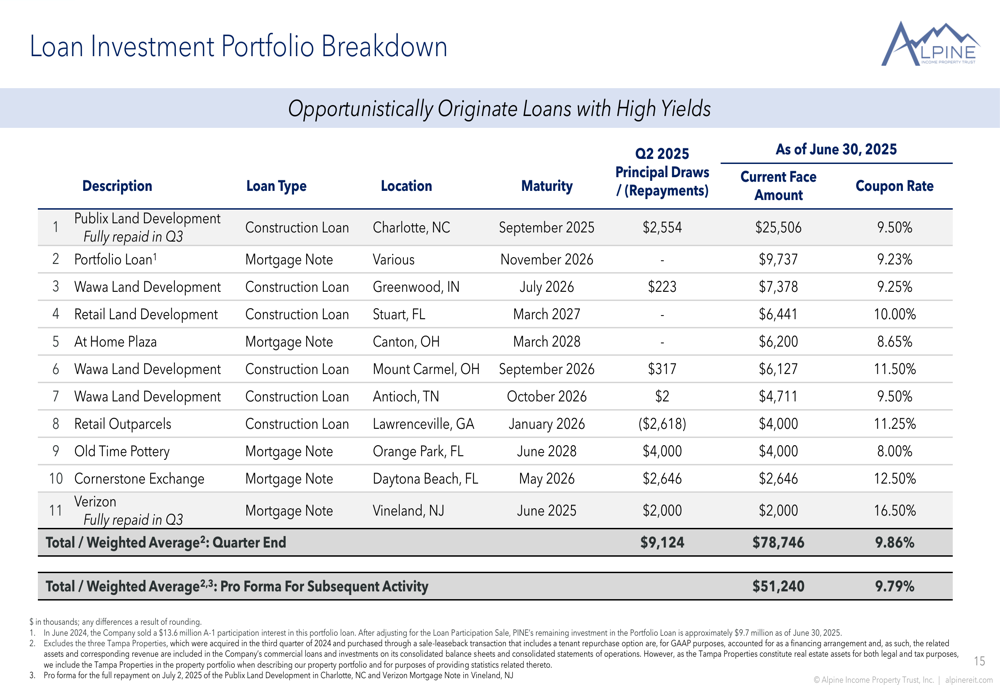

Alpine Income also maintains a loan investment portfolio with a weighted average coupon rate of 9.86%, providing an additional income stream beyond traditional property leases:

While the presentation doesn’t explicitly address forward guidance, the recent earnings report indicated that Alpine Income raised its full-year FFO/AFFO guidance to $1.74-$1.77 per share, suggesting confidence in its operational strategies despite the Q1 earnings miss.

The company continues to repurchase shares, with 546,390 common shares repurchased year-to-date for $8.8 million, indicating management’s belief in the stock’s undervaluation.

Analyst Perspectives

According to the recent earnings article, analyst price targets for Alpine Income range from $17 to $22, indicating potential upside from current levels. The company’s strong liquidity position, with a current ratio of 14.67, provides financial flexibility to pursue its investment strategy.

Management has expressed optimism about investment opportunities, with guidance for $70-$100 million in investments for the full year. As noted in the earnings call, an executive stated, "We’re taking advantage of some good opportunities out there and the pipeline looks good," and highlighted the attractive total return potential from the dividend yield combined with free cash flow.

While Alpine Income’s presentation paints a positive picture of its portfolio quality and valuation, investors will likely continue to monitor the company’s ability to translate these fundamentals into consistent earnings performance in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.