One & One Green Technologies stock soars 100% after IPO debut

Introduction & Market Context

Alsea SAB De CV (BMV:ALSEA), a leading restaurant operator valued at $1.8 billion, presented its first quarter 2025 results on April 30, highlighting strong sales growth despite pressure on profitability. The company, which manages brands including Starbucks (NASDAQ:SBUX), Domino’s Pizza (NYSE:DPZ), and Burger King across multiple regions, saw its stock rise 4.85% following the announcement, reflecting investor confidence in its growth strategy despite margin challenges.

The presentation, led by CEO Armando Torrado and CFO Federico Rodriguez, detailed the company’s performance across its extensive portfolio of nearly 4,800 units spanning Mexico, Europe, and South America, while also touching on its upcoming strategic partnership with Chipotle (NYSE:CMG) in Mexico.

Quarterly Performance Highlights

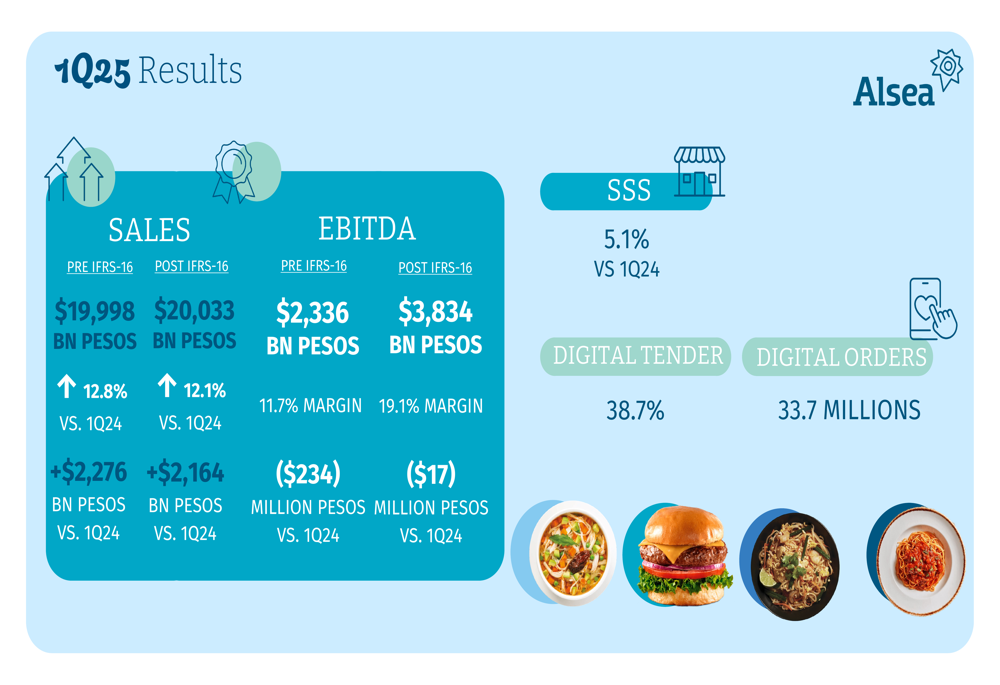

Alsea reported total sales of 19,998 billion pesos (pre IFRS-16), representing a 12.8% increase compared to Q1 2024. This growth translated to an additional 2,276 billion pesos in revenue year-over-year. However, EBITDA declined to 2,336 billion pesos (pre IFRS-16), with margins contracting to 11.7%, representing a decrease of 234 million pesos compared to the same period last year.

As shown in the following financial results summary:

Same-store sales (SSS) grew by 5.1% compared to Q1 2024, while digital channels continued to play a crucial role in the company’s operations, accounting for 38.7% of tender and generating 33.7 million digital orders during the quarter.

Regional and Brand Performance

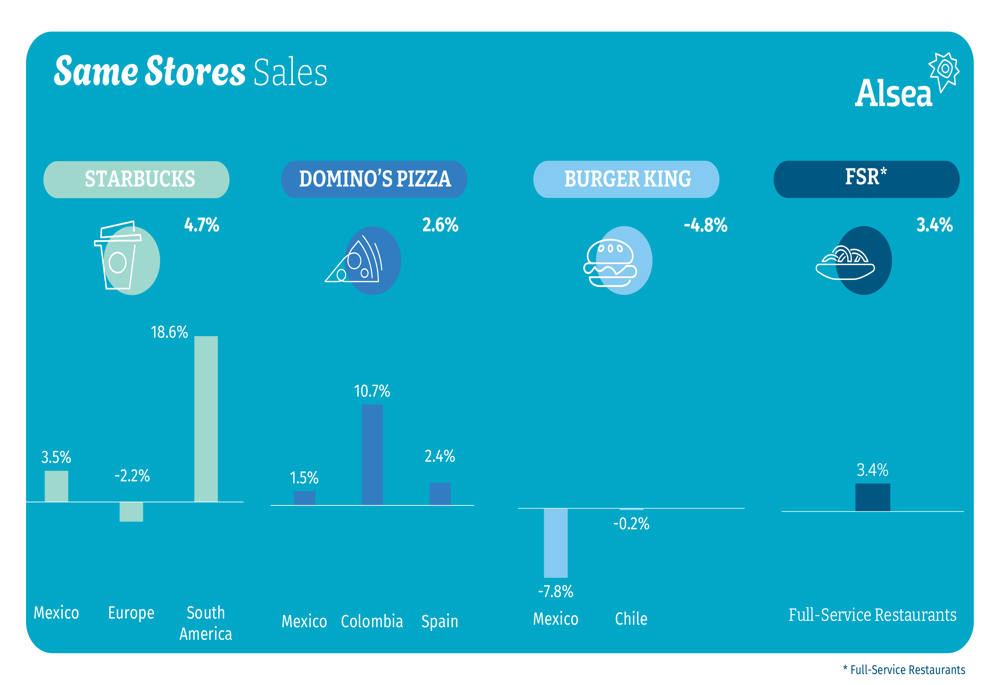

The presentation revealed varying performance across Alsea’s brands and regions. Starbucks showed overall growth of 4.7%, with particularly strong performance in South America (18.6%), while Europe saw a decline of 2.2%. Domino’s Pizza grew by 2.6% overall, with Colombia leading at 10.7%. Burger King faced challenges with a 4.8% overall decline, primarily due to a 7.8% drop in Mexico.

The following chart illustrates the same-store sales performance by brand and region:

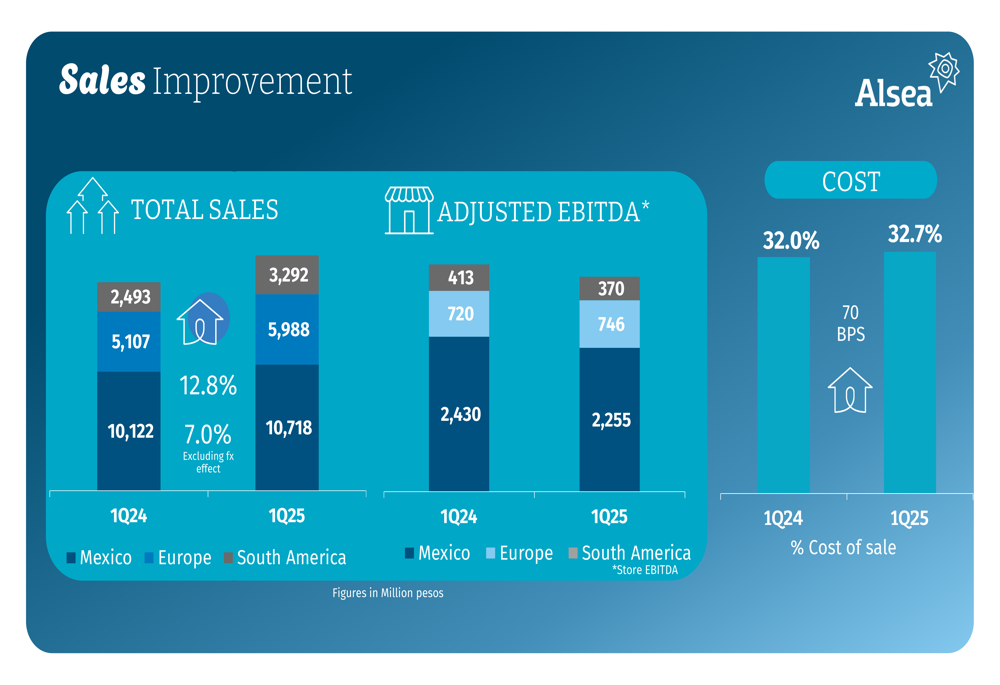

Regionally, South America demonstrated the strongest sales growth at 32%, reaching 3,292 billion pesos in Q1 2025 compared to 2,493 billion pesos in Q1 2024. Europe followed with 17.3% growth to 5,988 billion pesos, while Mexico showed more modest growth of 5.9% to 10,718 billion pesos.

The company’s global footprint now encompasses 4,795 units across multiple brands, with 77% being corporate-owned and 23% franchised. Starbucks remains the largest brand with 1,923 units, followed by Domino’s Pizza with 1,526 units.

Digital and Loyalty Program Performance

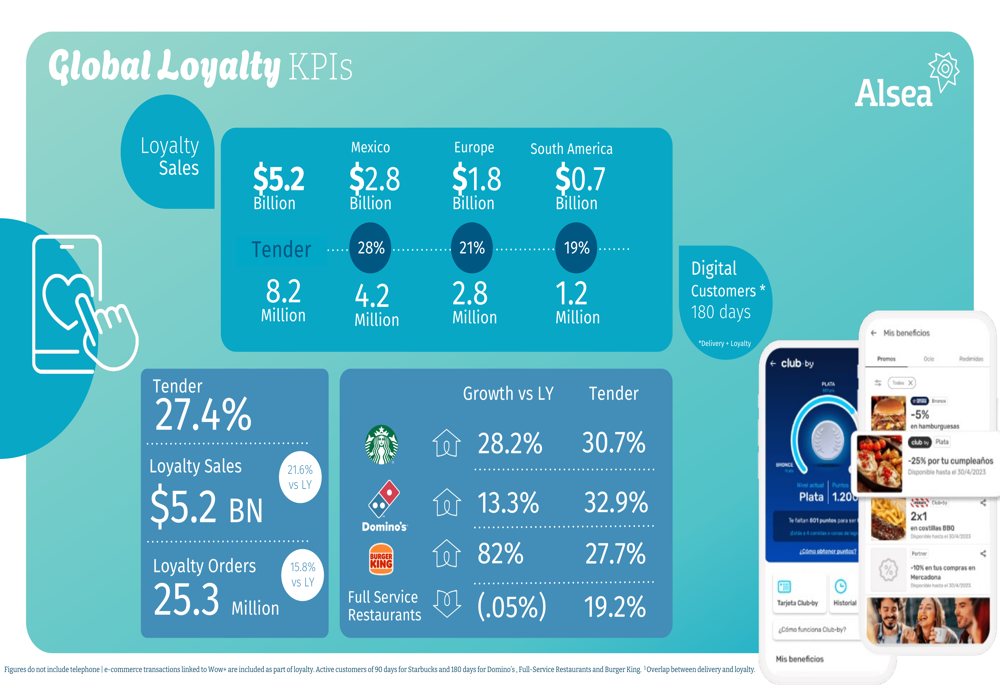

Alsea’s digital transformation continues to yield results, with loyalty programs generating 5.2 billion pesos in sales across its regions. Mexico led with 2.8 billion pesos, followed by Europe with 1.8 billion pesos and South America with 0.7 billion pesos. The company reported 25.3 million loyalty orders, with an overall tender penetration of 27.4%.

The loyalty program now encompasses 8.2 million customers with a 28% tender rate, demonstrating strong customer engagement across the portfolio. Starbucks showed particularly strong loyalty performance with 28.2% growth year-over-year and a tender rate of 30.7%.

Financial Position and Debt Profile

Despite the strong sales growth, Alsea’s regional EBITDA performance showed pressure, particularly in Mexico where adjusted EBITDA declined from 2,430 million pesos in Q1 2024 to 2,255 million pesos in Q1 2025. Europe saw modest growth from 720 million to 746 million pesos, while South America declined from 413 million to 370 million pesos.

Cost of goods sold increased by 70 basis points year-over-year, rising from 32.0% in Q1 2024 to 32.7% in Q1 2025, contributing to the margin pressure.

The company’s capital expenditures for the year-to-date period totaled 1.1 billion pesos, with Mexico accounting for 62% of investments, followed by Europe (31%) and South America (7%). In terms of project allocation, 44% went toward new openings and remodeling, 36% to other projects, and 20% to maintenance.

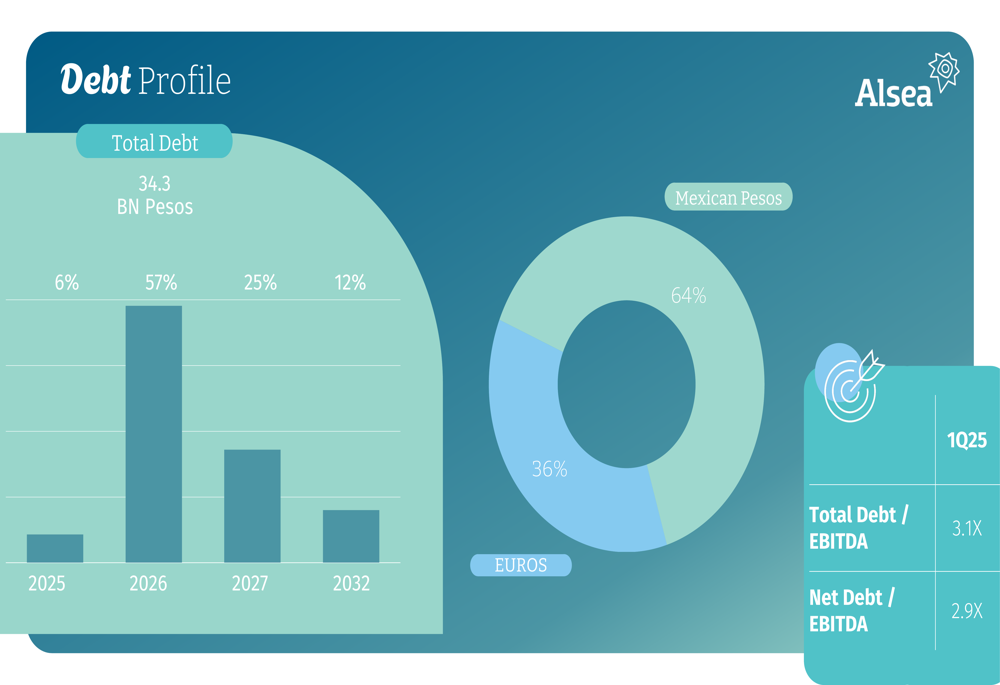

Alsea’s debt profile shows total debt of 34.3 billion pesos, with the majority (57%) maturing in 2026. The debt is primarily denominated in Mexican pesos (64%) and euros (36%). The company reported a total debt to EBITDA ratio of 3.1x and a net debt to EBITDA ratio of 2.9x.

Forward-Looking Statements and Strategic Initiatives

Despite the challenges in profitability, Alsea’s management reaffirmed its 2025 guidance, projecting low-teen top-line growth and mid-single-digit EBITDA growth. The company expects a gradual recovery in working capital during the second half of the year.

A key strategic development is Alsea’s partnership with Chipotle, which aims to bring the brand to the Mexican market by early 2026. CEO Armando Torrado highlighted Chipotle’s "solid value proposition with high standards" as a complementary addition to Alsea’s portfolio.

The company also emphasized its commitment to environmental, social, and governance (ESG) initiatives, including a double materiality assessment, 13 million pesos invested in social programs benefiting over 80,000 people in Mexico through Fundación Alsea, and the installation of more than 580 solar panels in Spain, reducing CO2 emissions by 345 tons.

While Alsea continues to focus on digital transformation and expansion, the decline in EBITDA and net income despite strong sales growth suggests ongoing challenges in managing costs and maintaining margins across its diverse portfolio and regions. Investors appear to be looking past these short-term pressures, focusing instead on the company’s growth trajectory and strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.