Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

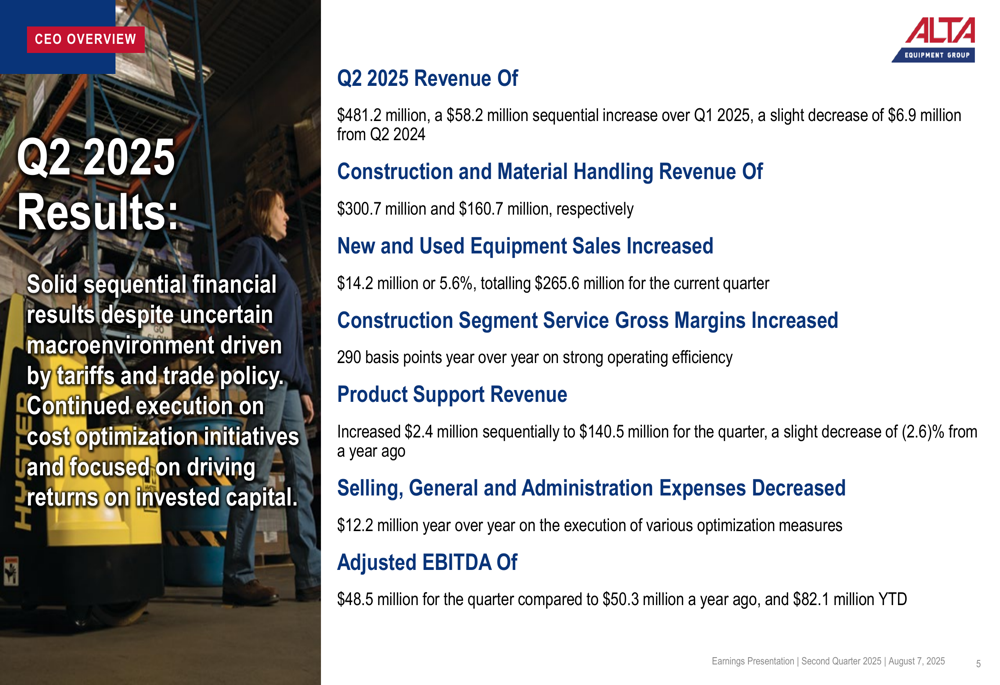

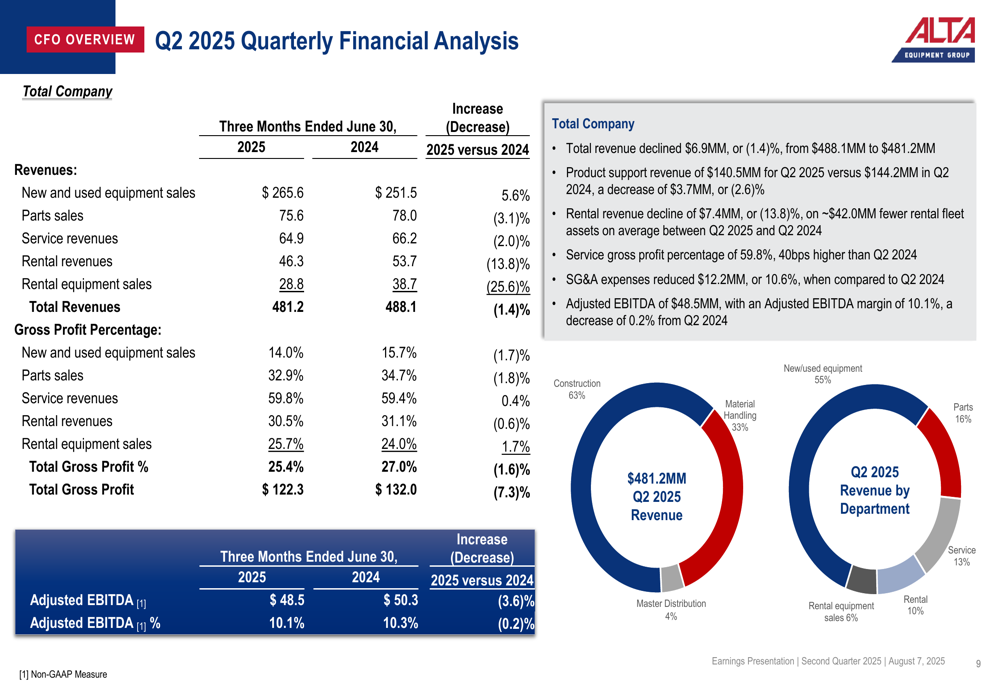

Alta Equipment Group Inc (NYSE:ALTG) released its second quarter 2025 earnings presentation on August 7, 2025, revealing sequential revenue improvement amid ongoing strategic repositioning efforts. The company reported Q2 revenue of $481.2 million, representing a $58.2 million increase from Q1 2025, though slightly below the $488.1 million reported in Q2 2024.

The equipment dealer continues to operate in a supportive infrastructure spending environment, with federal infrastructure funding reaching its middle stage and bulk spending forecast for 2025-2026. This positions Alta well in its key markets across the Northeast, Midwest, and Florida regions.

The stock closed at $7.17 on the day of the earnings release, down 2.32% for the session, but showing substantial recovery from its Q1 2025 levels when it traded below $5.

Quarterly Performance Highlights

Alta’s Q2 2025 performance showed mixed results across key financial metrics. While revenue declined slightly year-over-year, the company demonstrated sequential improvement and made progress on operational efficiency initiatives.

As shown in the following summary of Q2 2025 results:

New and used equipment sales increased by $14.2 million or 5.6% year-over-year to $265.6 million, offsetting declines in other revenue categories. The construction segment’s service gross margins improved significantly, increasing 290 basis points compared to the previous year, reflecting enhanced operational efficiency.

Selling, general and administrative expenses decreased by $12.2 million year-over-year, demonstrating the company’s commitment to cost optimization. Despite these improvements, adjusted EBITDA came in at $48.5 million for the quarter, slightly below the $50.3 million reported in Q2 2024.

The company’s total financial performance across segments shows the distribution of revenue sources and profitability metrics:

Segment Analysis

Alta’s performance varied significantly across its business segments, with construction equipment showing resilience while material handling faced more substantial headwinds.

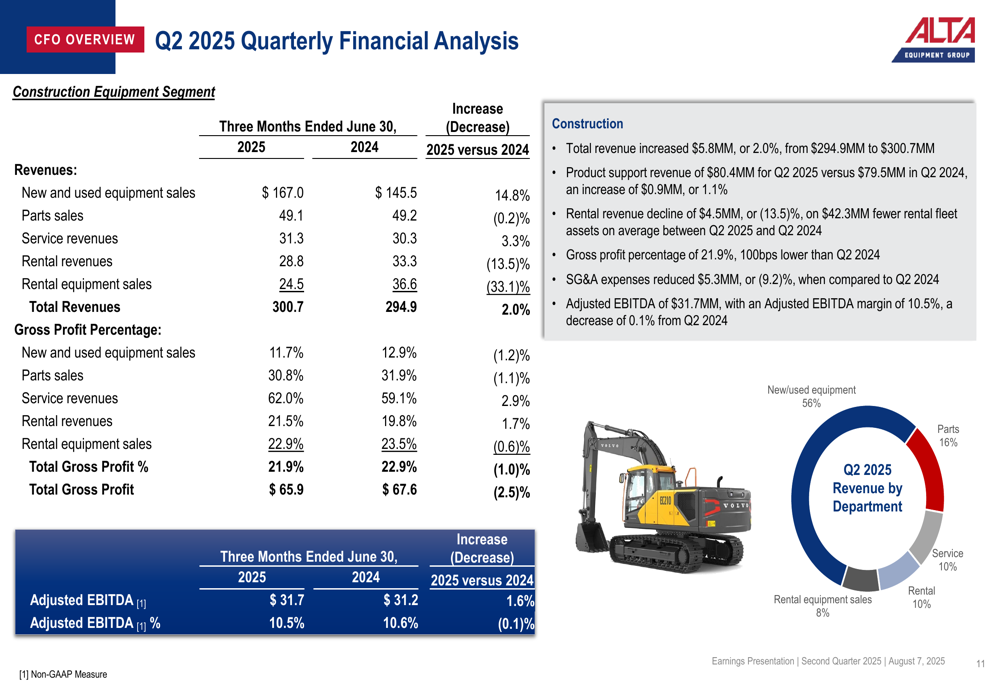

The construction equipment segment reported revenue of $300.7 million, a 2.0% increase from Q2 2024, driven by a 14.8% jump in new and used equipment sales. This growth was partially offset by a 13.5% decline in rental revenues and a 33.1% drop in rental equipment sales, reflecting the company’s strategic shift in its rental fleet approach.

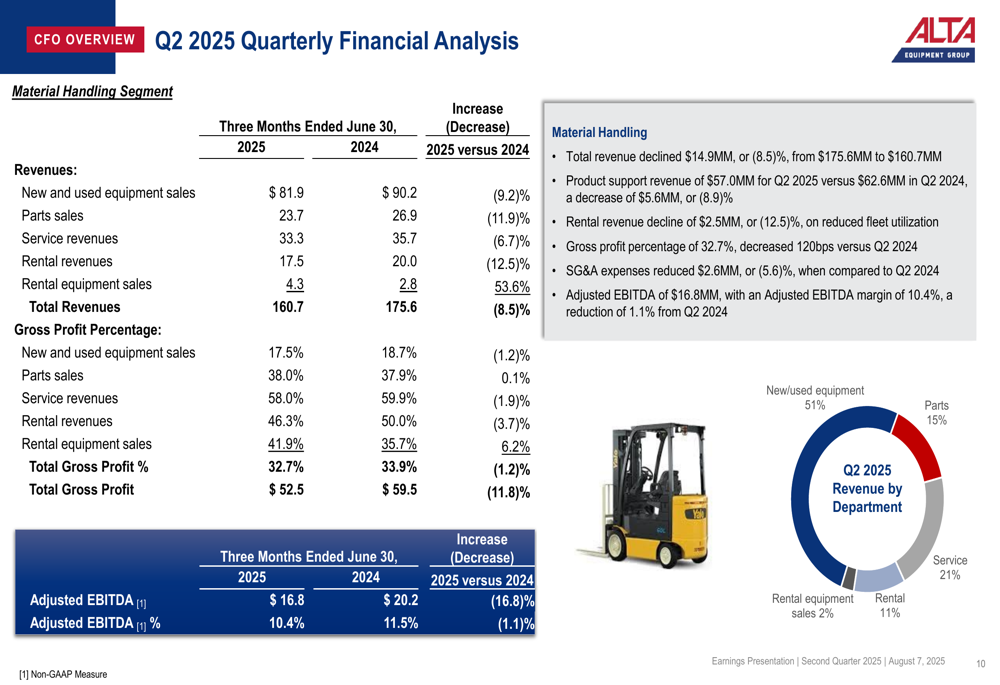

In contrast, the material handling segment experienced an 8.5% revenue decline to $160.7 million, with decreases across most revenue categories. New and used equipment sales fell 9.2%, while parts sales and service revenues declined 11.9% and 6.7% respectively. This segment’s adjusted EBITDA decreased 16.8% to $16.8 million.

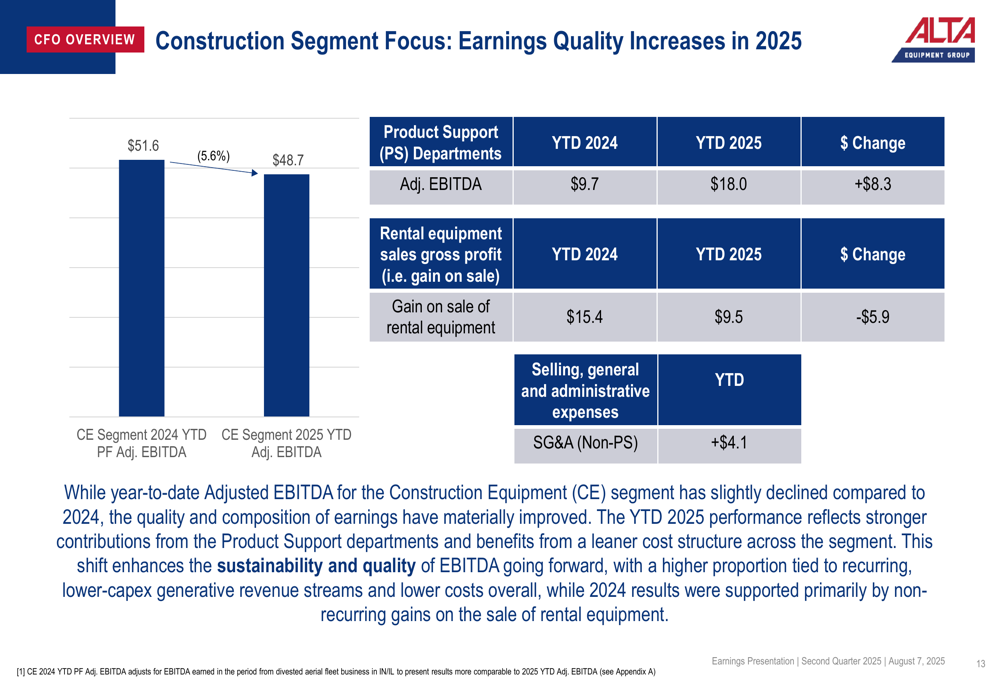

A notable bright spot in Alta’s performance is the improving quality of earnings within the construction segment, as highlighted in the following slide:

Product support departments’ adjusted EBITDA increased by $8.3 million year-to-date compared to 2024, while gain on sale of rental equipment decreased by $5.9 million. This shift toward more sustainable earnings sources reflects Alta’s strategic focus on building recurring revenue streams through parts and service.

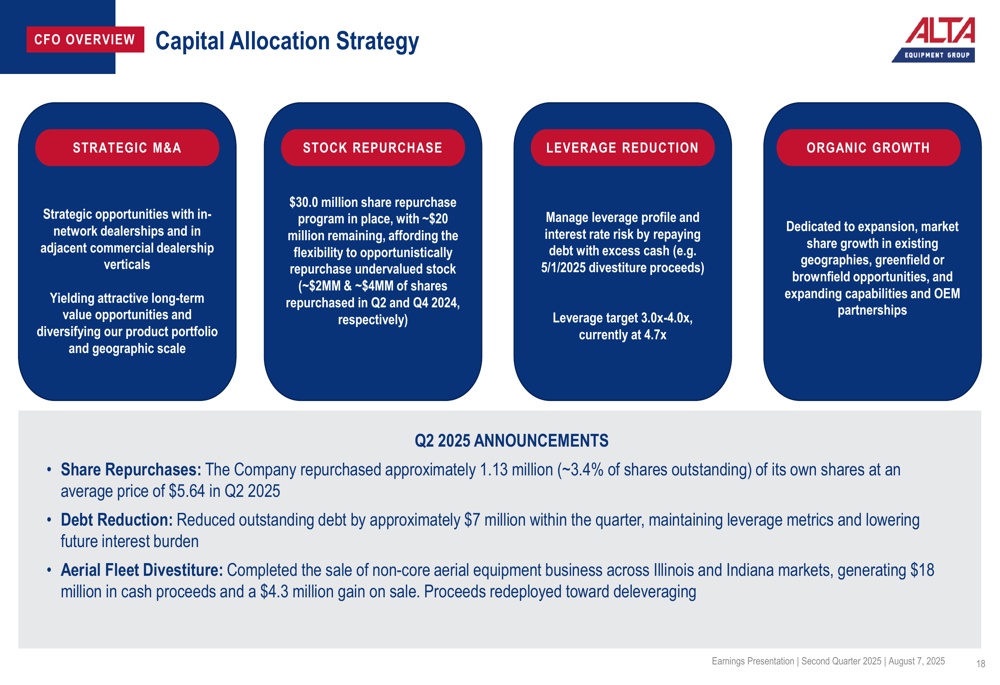

Strategic Initiatives & Capital Allocation

Alta continues to execute on its strategic initiatives, focusing on portfolio optimization, debt reduction, and shareholder returns. The company’s capital allocation strategy prioritizes strategic M&A, stock repurchases, leverage reduction, and organic growth.

In Q2 2025, Alta repurchased approximately 1.13 million shares and reduced outstanding debt by approximately $7 million. The company also completed the sale of its non-core aerial equipment business across Illinois and Indiana markets, generating $18 million in cash proceeds and a $4.3 million gain on sale.

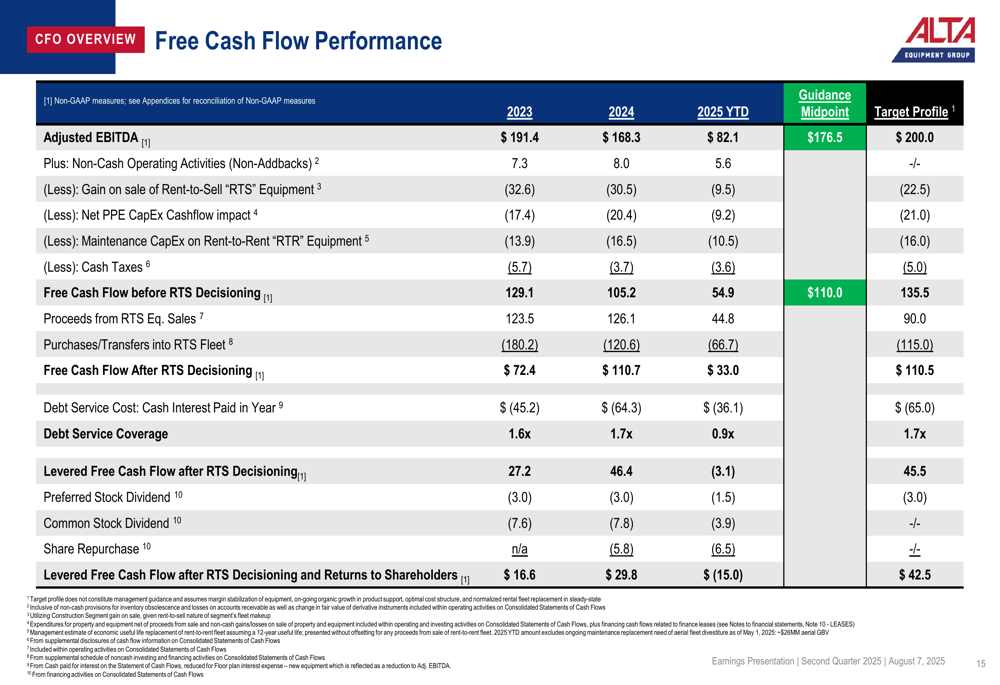

The company’s free cash flow performance shows a target profile that aims to improve from current levels:

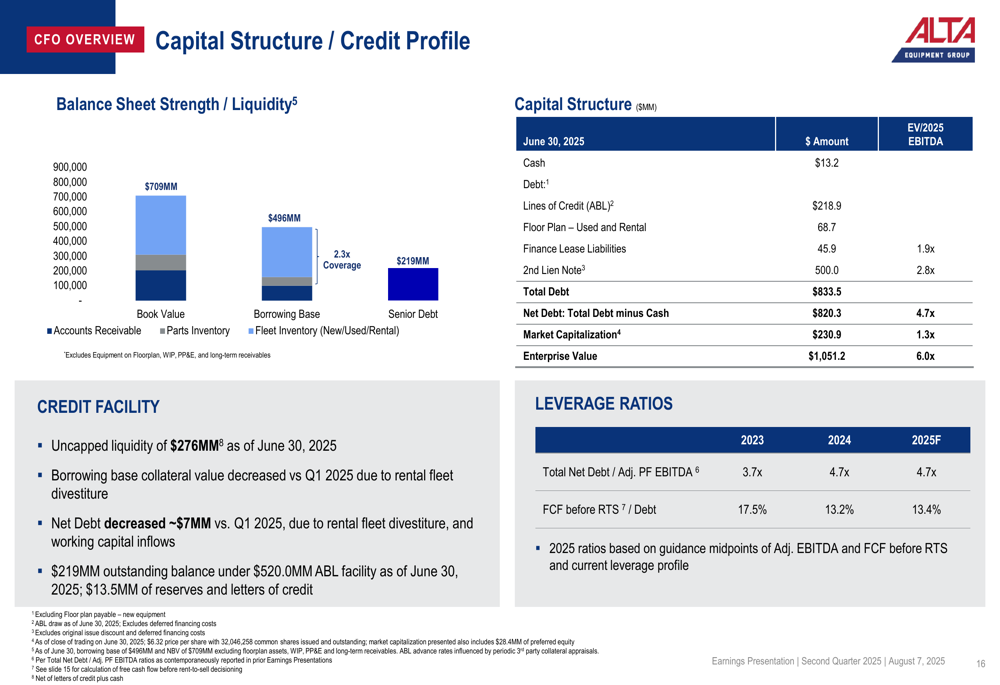

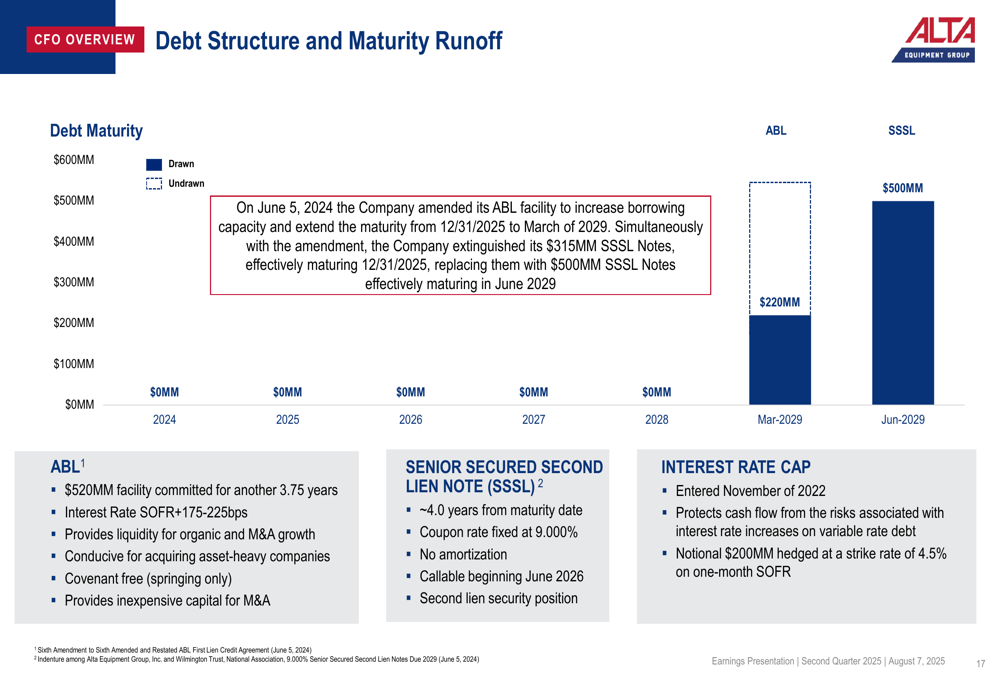

Alta’s capital structure and credit profile reveal a significant debt position, with total debt of $833.5 million as of June 30, 2025. The company’s net debt to adjusted EBITDA ratio stands at 4.7x, unchanged from 2024 but up from 3.7x in 2023.

The company’s debt structure and maturity schedule provide a clear view of its financial obligations, with major maturities not due until 2029:

Outlook & Guidance

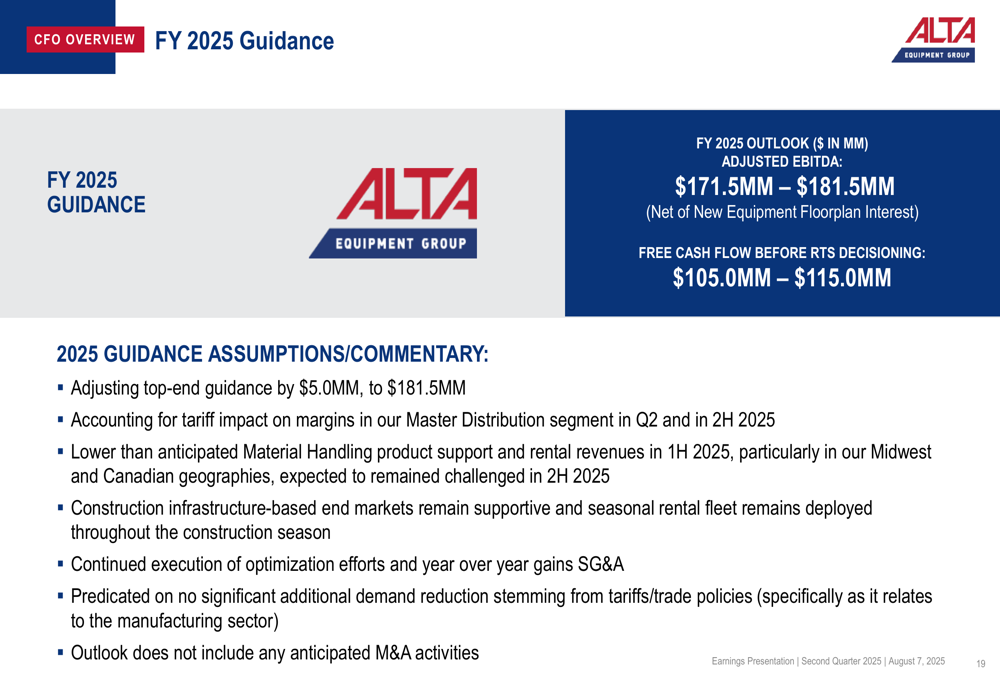

Alta Equipment Group has adjusted its full-year 2025 guidance, lowering the top end of its adjusted EBITDA range by $5 million to $181.5 million. The company now expects adjusted EBITDA between $171.5 million and $181.5 million, and free cash flow before RTS decisioning of $105.0 million to $115.0 million.

This guidance adjustment reflects several factors, including tariff impacts on margins in the master distribution segment, lower than anticipated material handling product support and rental revenues, and continued execution of optimization efforts. The outlook does not include any anticipated M&A activities and assumes no significant additional demand reduction stemming from tariffs or trade policies.

The company remains optimistic about construction infrastructure-based end markets, which continue to show strength. Alta’s business model, with its multiple sales channels and product support capabilities, positions it well to navigate varying market conditions.

Alta Equipment Group’s Q2 2025 results demonstrate the company’s ongoing transformation toward a more resilient business model with higher-quality earnings. While facing some headwinds in certain segments, the sequential improvement from Q1 and strategic portfolio optimization suggest the company is making progress on its long-term objectives despite a challenging operating environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.