Fubotv earnings beat by $0.10, revenue topped estimates

Introduction & Market Context

Altice USA (NYSE:ATUS) presented its second quarter 2025 results on August 7, showing signs of stabilization in its subscriber base while still facing revenue and profitability challenges. The company’s stock closed at $2.39 on August 6, down 1.24% for the day, and has been trading in a 52-week range of $1.52 to $3.20.

The cable and telecommunications provider continues to navigate a highly competitive landscape, with pressure from fiber overbuilders and fixed wireless providers affecting its traditional business. Despite these headwinds, Altice is making progress on its strategic initiatives focused on fiber expansion, operational efficiency, and debt management.

Quarterly Performance Highlights

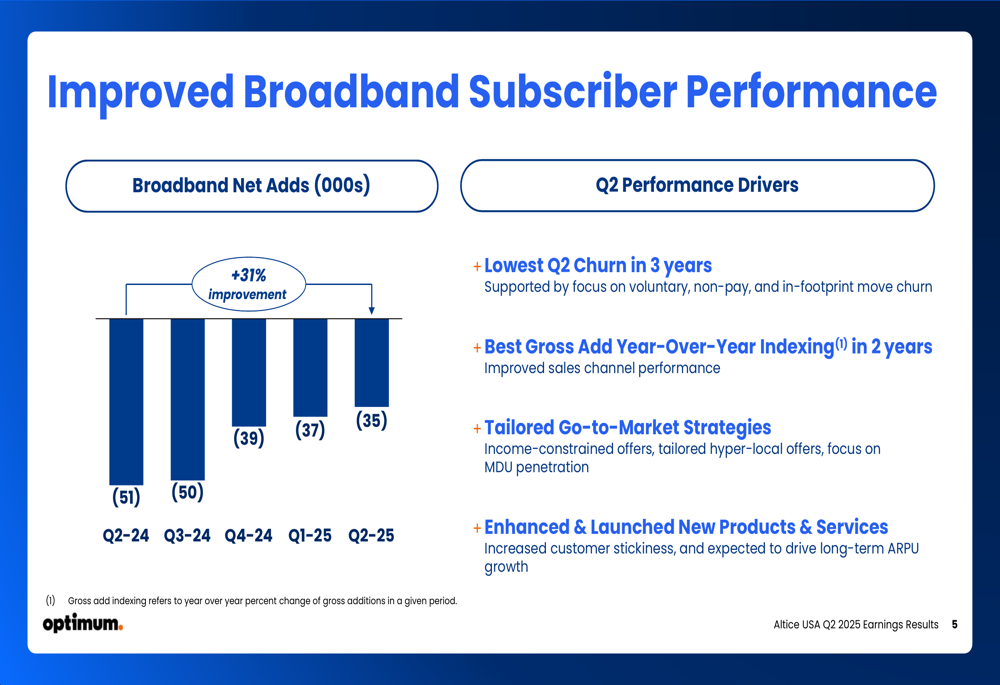

Altice reported Q2 2025 revenue of $2.15 billion, representing a 4.2% year-over-year decline. While still negative, the company showed improvement in broadband subscriber losses, with net losses of 35,000 in Q2 2025 compared to 51,000 in the same quarter last year – a 31% improvement.

As shown in the following chart of broadband subscriber trends, Altice has been steadily reducing its quarterly subscriber losses over the past year:

The company attributed this improvement to its lowest Q2 churn in three years, better gross add performance, and tailored marketing strategies for different customer segments. However, these subscriber metrics still indicate ongoing competitive pressures in Altice’s markets.

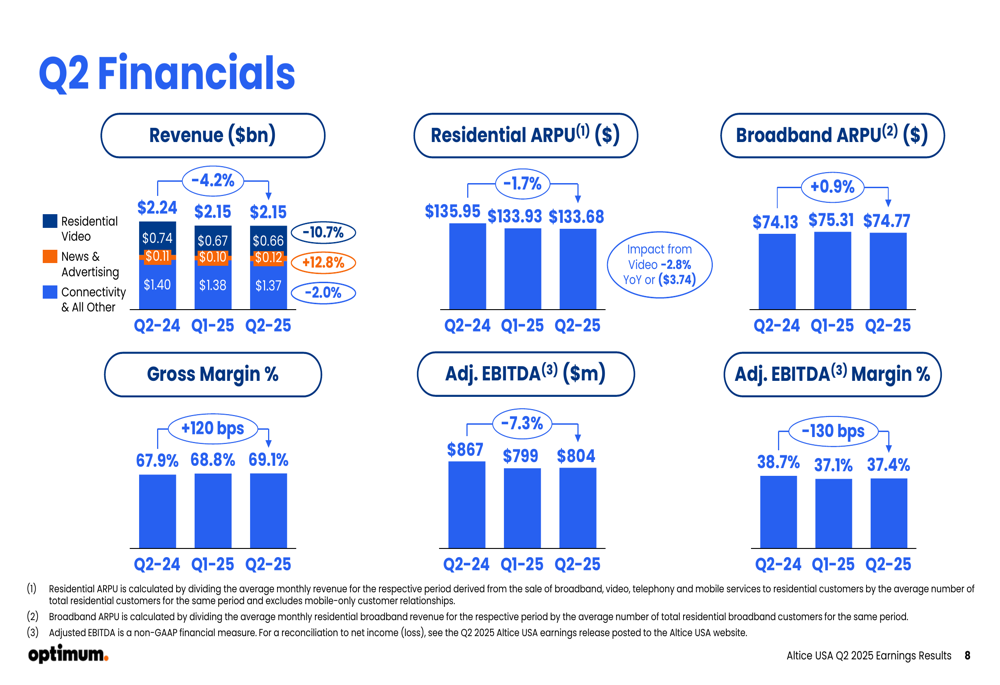

Adjusted EBITDA for the quarter came in at $804 million, down 7.3% year-over-year, with an adjusted EBITDA margin of 37.4%, representing a 130 basis point decline from Q2 2024. Despite these challenges, gross margin improved to 69.1%, up 120 basis points year-over-year.

The following financial summary highlights key metrics for the quarter:

Strategic Initiatives

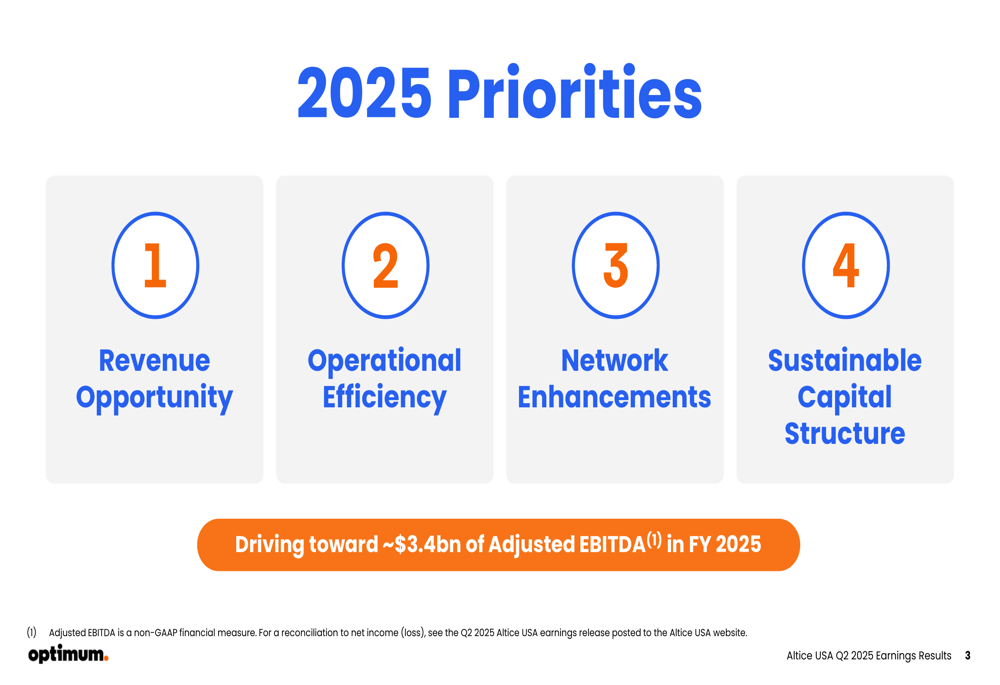

Altice outlined four key strategic priorities for 2025: Revenue Opportunity (SO:FTCE11B), Operational Efficiency, Network Enhancements, and Sustainable Capital Structure. These initiatives aim to drive the company toward approximately $3.4 billion in Adjusted EBITDA for the full year 2025.

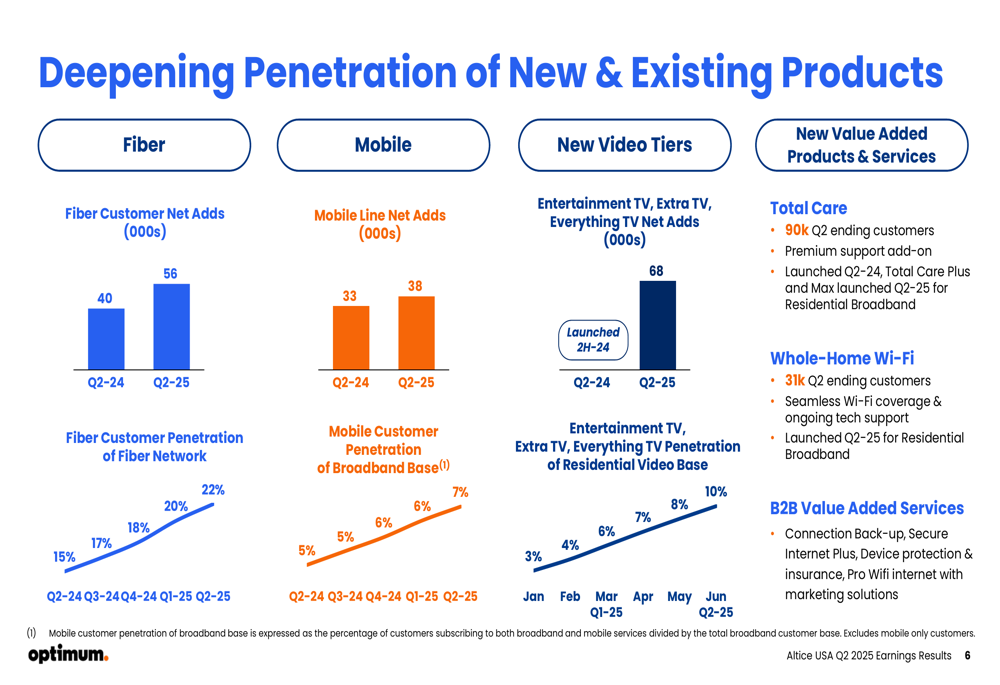

A significant bright spot in Altice’s strategy is the accelerating penetration of its fiber network. Fiber customer penetration reached 22% in Q2 2025, up from 15% in Q2 2024, with 56,000 fiber customer net adds in the quarter. Similarly, mobile line penetration increased to 7% of the broadband base, up from 5% a year earlier.

The following chart illustrates the growing adoption of Altice’s fiber and mobile offerings:

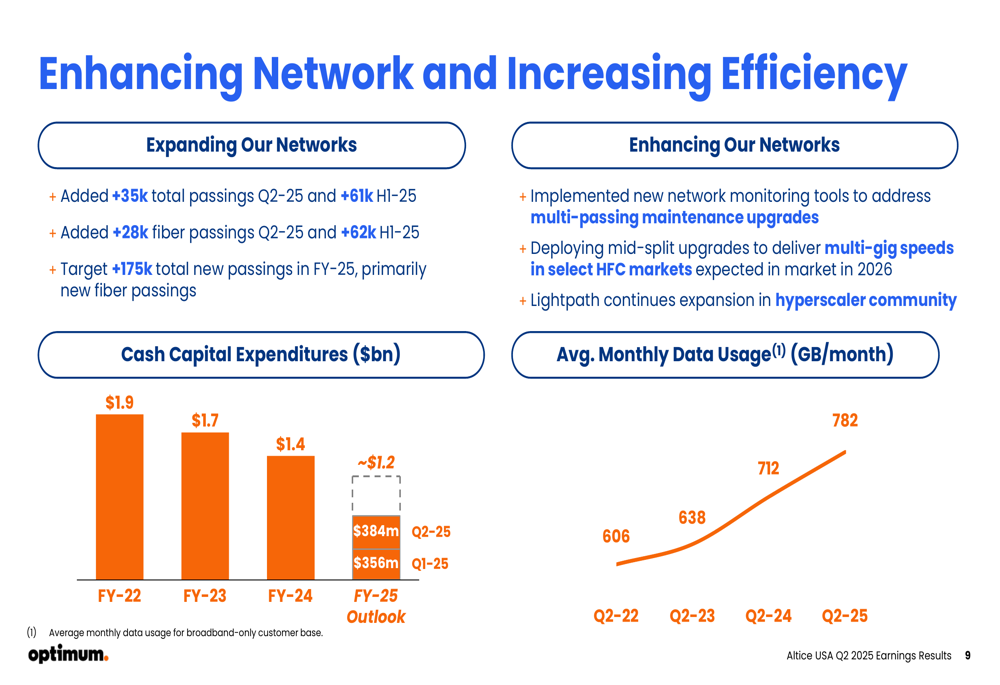

On the network front, Altice added 35,000 total passings in Q2 2025, including 28,000 fiber passings. The company is targeting 175,000 total new passings for the full year 2025, primarily focused on fiber. Altice’s Optimum Fiber was recognized by Ookla® as offering the fastest and most reliable internet speeds in New York and New Jersey, and by PCMag as the fastest ISP in NY, NJ, and PA.

Detailed Financial Analysis

While Altice’s revenue declined 4.2% year-over-year, there were some positive developments in specific segments. News & Advertising revenue grew 12.8% compared to Q2 2024, reaching $119 million. However, this was offset by a 6.0% decline in Residential revenue and a 2.0% drop in Business Services.

Residential ARPU decreased 1.7% year-over-year to $133.68, with video accounting for a 2.8% negative impact. On a positive note, Broadband ARPU increased by 0.9% to $74.77, suggesting some pricing power in the company’s core internet business.

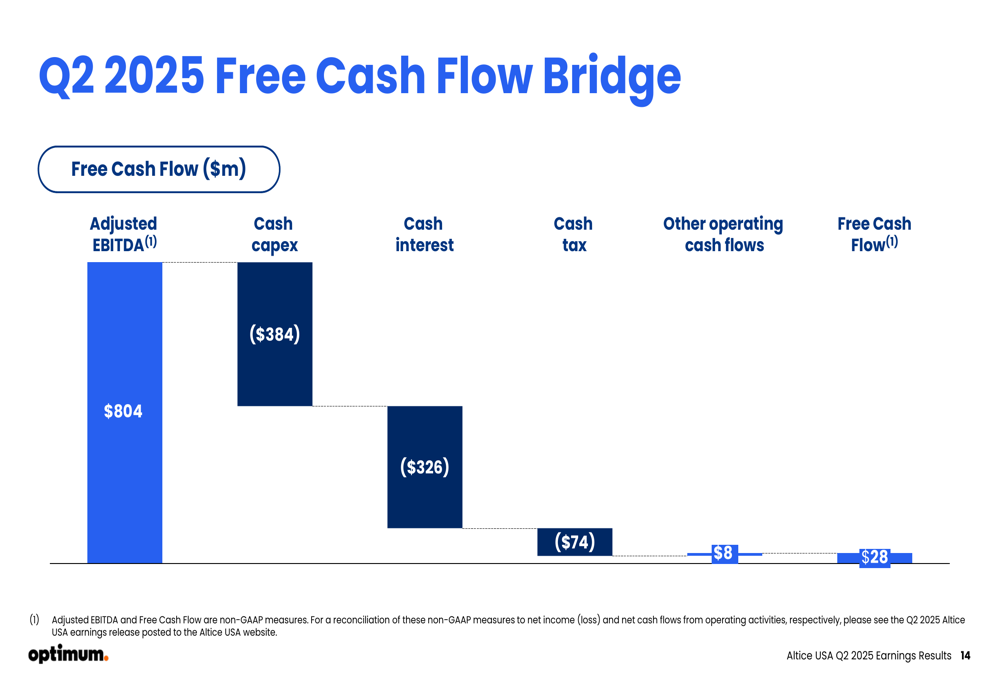

The company generated $28 million in Free Cash Flow during Q2 2025, as illustrated in the following bridge:

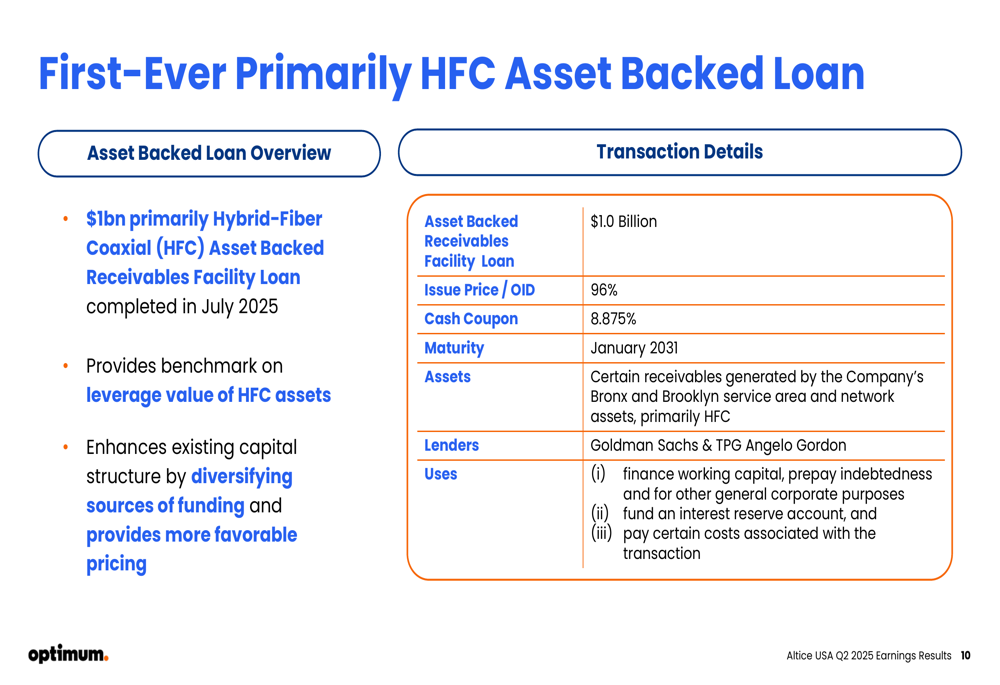

In July 2025, Altice completed a $1 billion primarily Hybrid-Fiber Coaxial (HFC) Asset-Backed Loan, which the company described as enhancing its capital structure by diversifying funding sources and providing more favorable pricing. The loan matures in January 2031 and carries an 8.875% cash coupon.

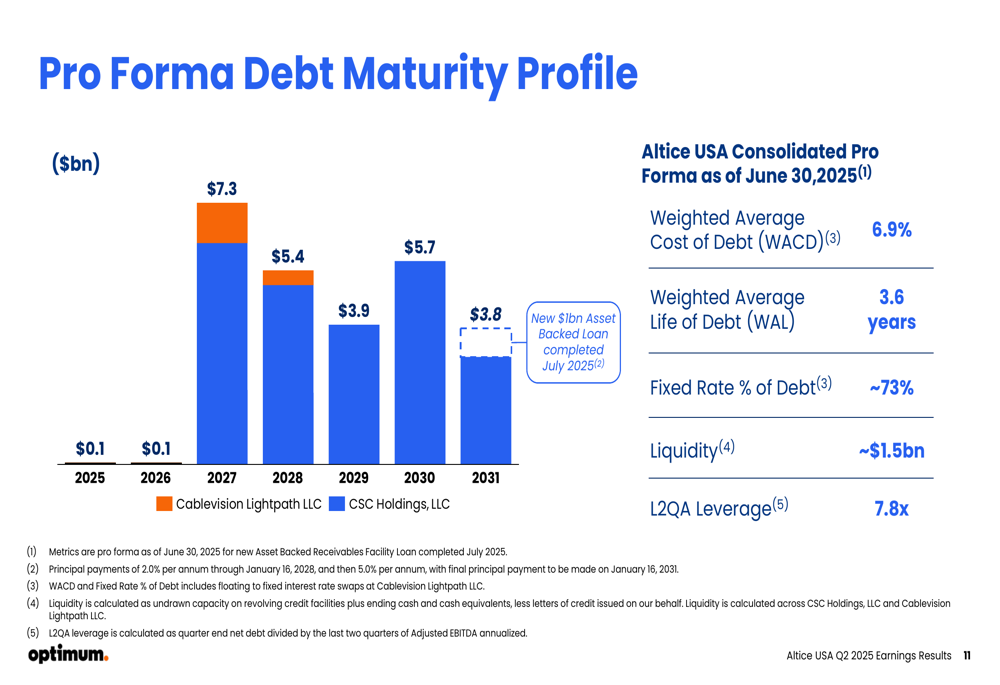

Altice’s debt maturity profile shows significant obligations coming due in 2027 ($7.3 billion) and 2028 ($5.4 billion). The company reported a weighted average cost of debt of 6.9% and a leverage ratio of 7.8x, highlighting the ongoing challenges in its capital structure.

Forward-Looking Statements

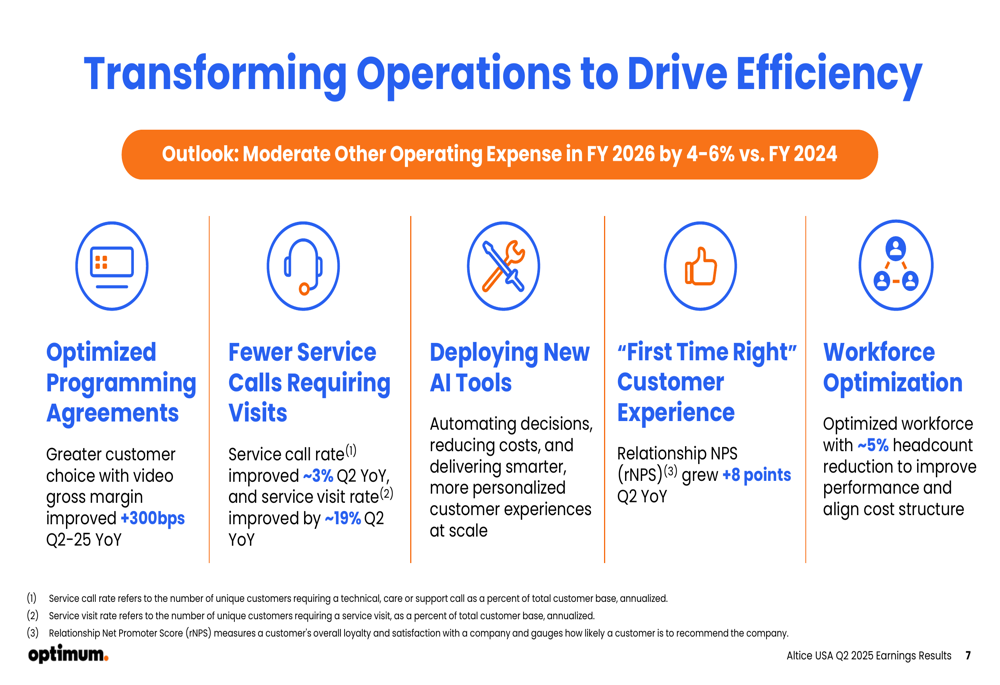

Altice is focusing on operational efficiency to improve its financial performance, targeting a 4-6% reduction in operating expenses in FY 2026 compared to FY 2024. The company has implemented workforce optimization with approximately 5% headcount reduction and is deploying new AI tools to automate decisions and reduce costs.

For the full year 2025, Altice is targeting capital expenditures of approximately $1.2 billion, down from $1.4 billion in FY 2024. This reduction in capex, combined with operational efficiencies, is part of the company’s strategy to improve free cash flow generation while still investing in network enhancements.

While Altice faces ongoing challenges in its traditional cable business, the company’s focus on fiber expansion, operational efficiency, and new product offerings provides a potential path toward stabilization and eventual growth. However, the high leverage ratio and competitive market conditions remain significant hurdles for the company to overcome in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.