Futures surge; Trump on China trade tensions - what’s moving markets

Introduction & Market Context

Amalgamated Financial Corp. (NASDAQ:AMAL) released its first quarter 2025 earnings presentation on April 24, showing modest quarter-over-quarter declines in key metrics while maintaining its full-year guidance. The socially responsible financial institution reported mixed results as it continues to focus on mission-aligned banking segments.

The stock jumped 9.57% in premarket trading to $30.80, suggesting investors are looking beyond the quarterly dip to focus on deposit growth and maintained guidance. This follows a previous close of $28.11, with the stock having traded between $23.08 and $38.19 over the past 52 weeks.

Quarterly Performance Highlights

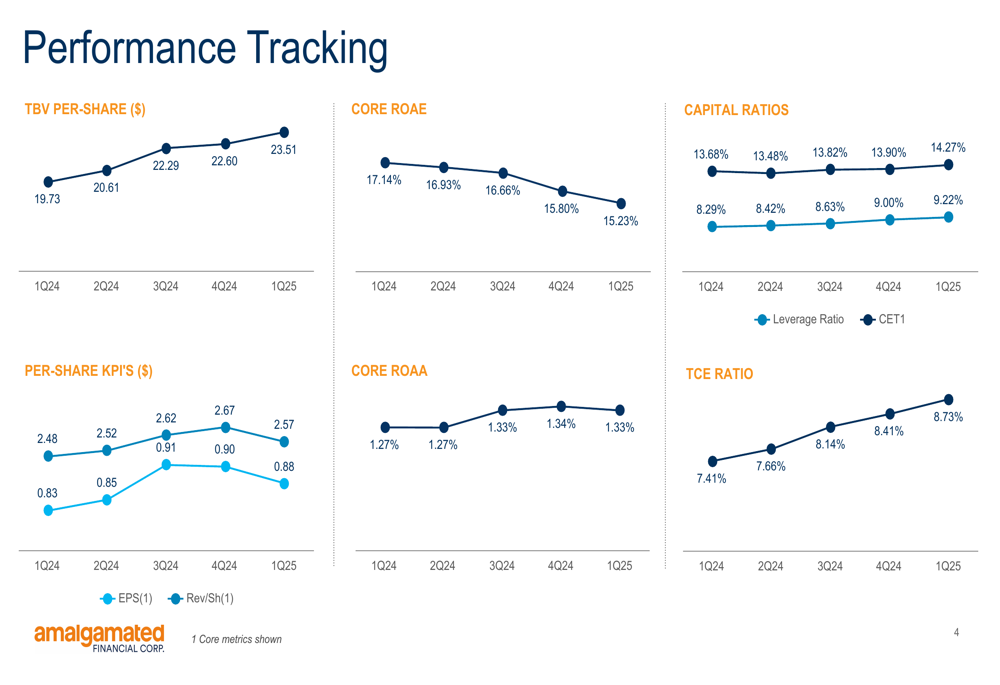

Amalgamated reported core net income of $27.1 million for Q1 2025, representing a 3.0% decrease from the previous quarter. Core earnings per share came in at $0.88, down 2.2% quarter-over-quarter, following the $0.90 EPS reported in Q4 2024 that had exceeded analyst expectations.

As shown in the following quarterly highlights chart:

Net interest income declined 3.4% to $70.6 million, though the bank’s net interest margin improved by 4 basis points to 3.55%. The company’s leverage ratio strengthened to 9.22%, a 2.4% increase from the previous quarter.

The bank’s performance metrics over the past five quarters show relatively stable returns:

Core return on average equity (ROAE) stood at 15.23% and core return on average assets (ROAA) at 1.33%, both maintaining the strong performance seen in previous quarters. Tangible book value per share increased to $23.51.

Deposit and Loan Portfolio Analysis

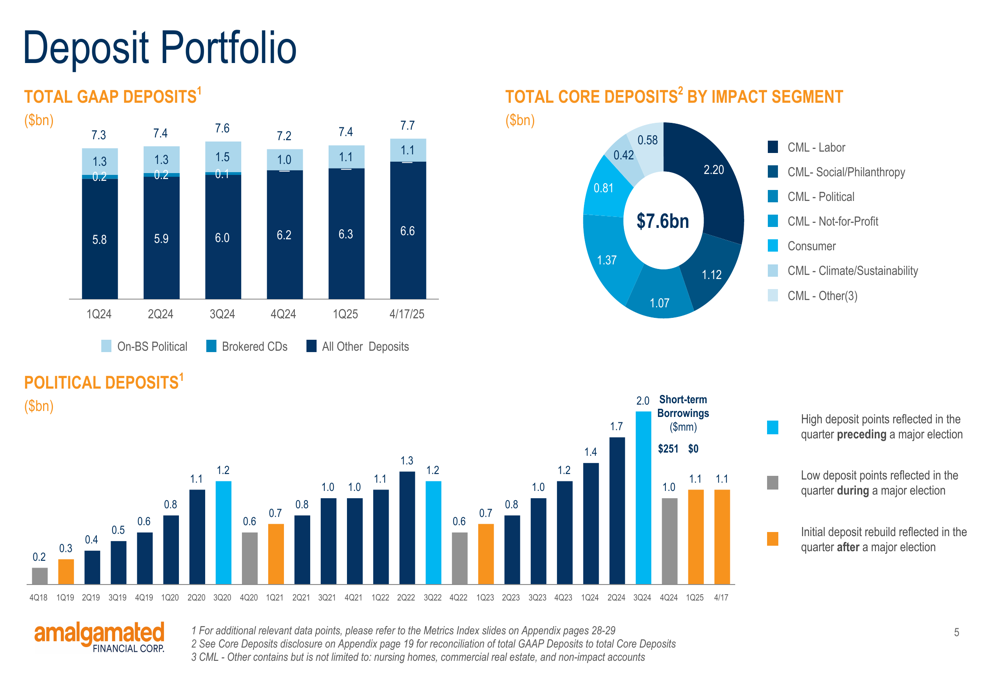

A bright spot in the quarterly results was deposit growth, which increased by $231.5 million or 3.2% quarter-over-quarter, reaching $7.7 billion. This growth came despite the bank moving an additional $214.5 million of deposits off-balance sheet during the quarter.

The deposit portfolio breakdown illustrates Amalgamated’s focus on mission-aligned segments:

Political deposits represent the largest segment at $2.2 billion, followed by consumer deposits at $1.37 billion and climate/sustainability at $1.12 billion. This composition reflects the bank’s strategic positioning in socially responsible banking.

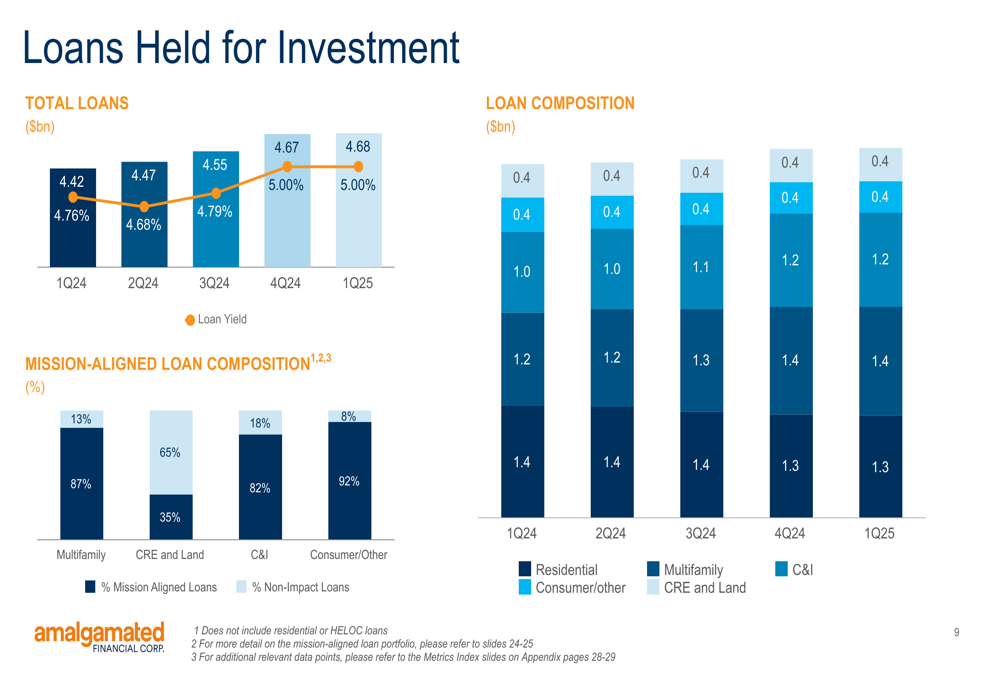

On the lending side, total loans held for investment amounted to $4.68 billion with a yield of 5.00%:

The loan portfolio is balanced between commercial real estate and land ($1.4 billion), commercial and industrial loans ($1.4 billion), and multifamily loans ($1.2 billion). Consumer and other loans make up the remaining $0.4 billion.

Credit Quality and Risk Management

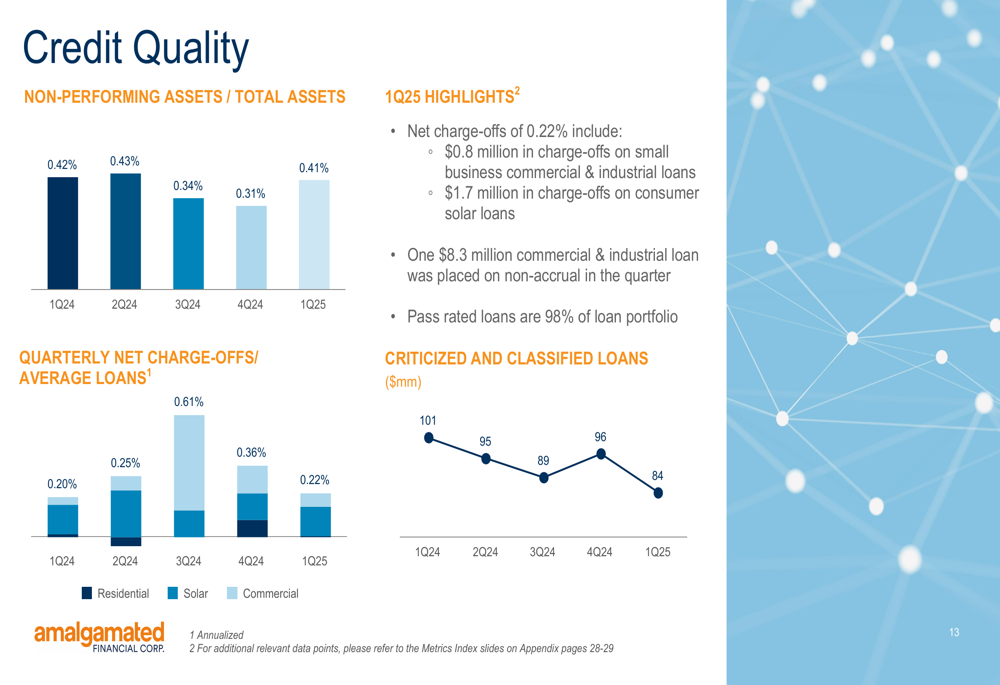

Credit quality metrics remained relatively stable, with non-performing assets to total assets at 0.41%, up slightly from the previous quarter’s 0.31%. Quarterly net charge-offs decreased to 0.22% from 0.36% in Q4 2024.

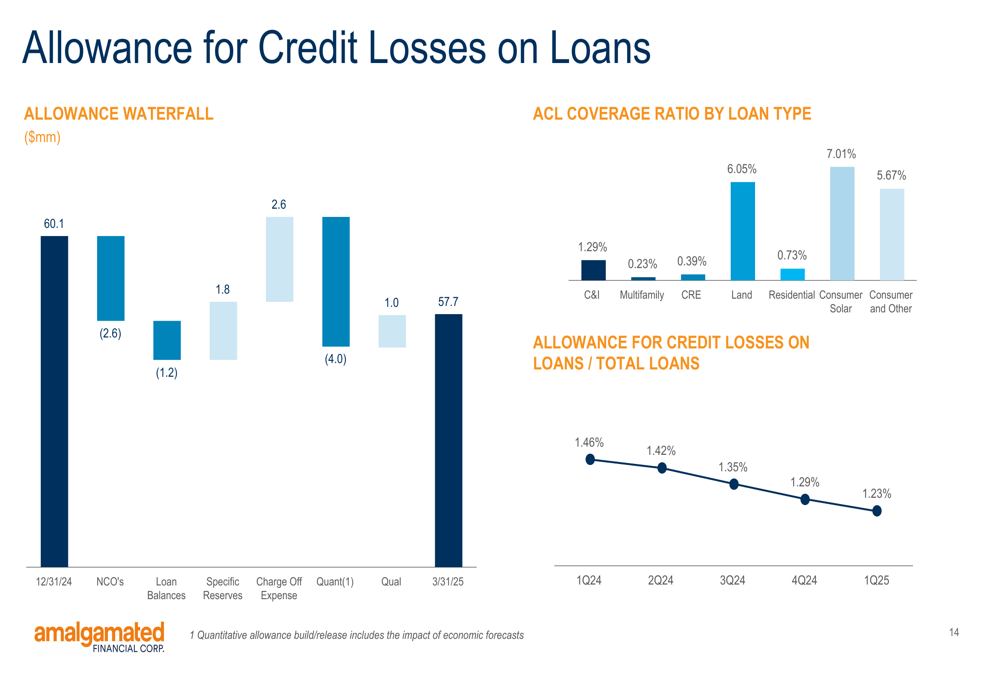

The credit quality trends are illustrated in the following chart:

The allowance for credit losses on loans continued its gradual decline, reaching 1.23% of total loans, compared to 1.29% in the previous quarter:

The bank noted that 98% of its loans are rated as "pass," indicating strong overall credit quality, though one $8.3 million commercial loan was placed on non-accrual status during the quarter.

Forward Guidance and Strategic Focus

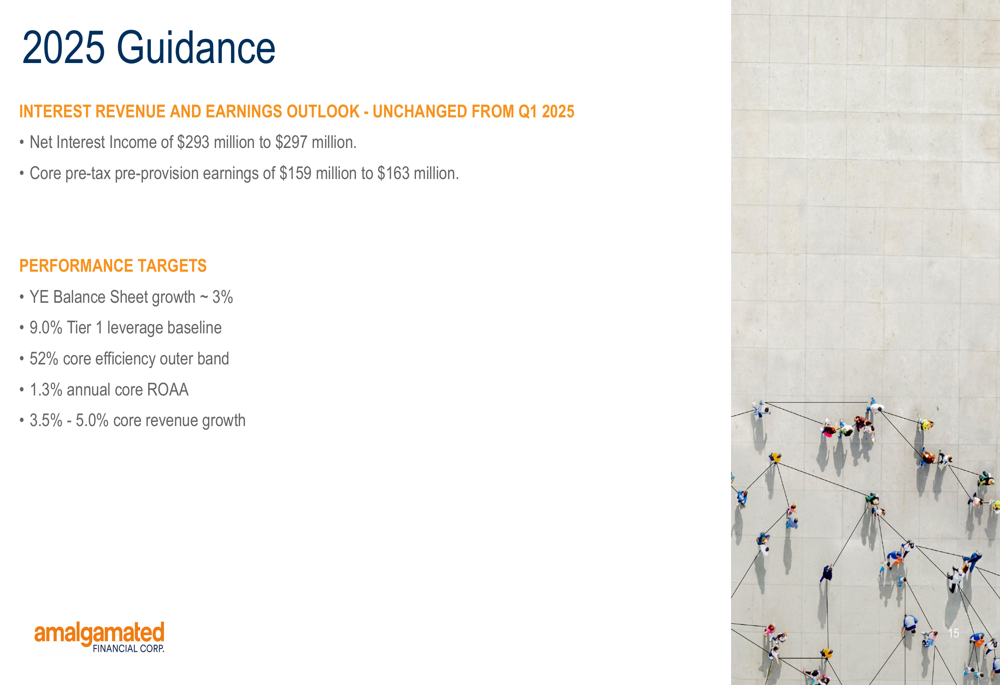

Amalgamated maintained its 2025 guidance unchanged from the previous quarter, projecting:

The bank continues to target approximately 3% year-end balance sheet growth, a Tier 1 leverage ratio of 9.0%, core efficiency ratio of 52%, core return on average assets of 1.3% annually, and core revenue growth between 3.5% and 5.0%.

This guidance aligns with the bank’s previous statements from Q4 2024, when CEO Priscilla Sims Brown noted that the bank was "nearing the inflection point of becoming a larger bank" and CFO Jason Darby characterized 2025 as "a transformative year where we make necessary investments for the purpose of significantly growing revenue in 2026."

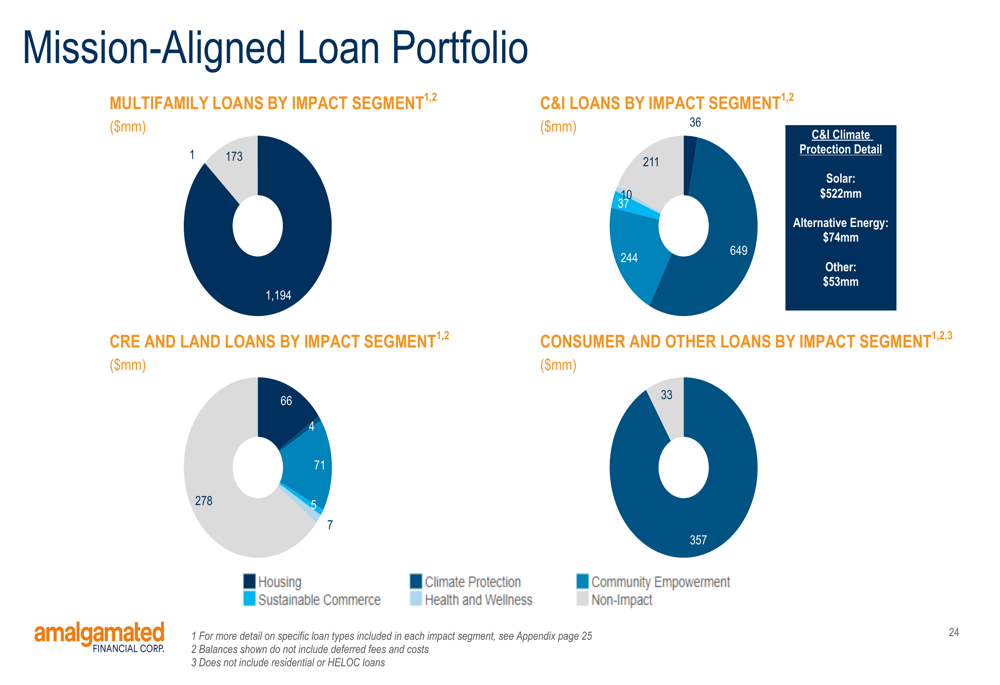

The bank’s focus on not-for-profit and mission-aligned segments remains central to its strategy, with detailed breakdowns of its impact investments:

Analyst Perspectives

While the quarterly results showed modest declines in some key metrics, the maintained guidance and continued deposit growth suggest management confidence in meeting full-year targets. Previous analyst price targets ranged from $42 to $45, indicating potential upside from current trading levels.

The strong premarket reaction suggests investors may be focusing on the bank’s unique positioning in mission-aligned banking segments and its ability to continue growing deposits despite moving some off-balance sheet. The slight compression in earnings appears to be viewed as temporary rather than indicative of a longer-term trend.

As Amalgamated continues its transformation efforts in 2025, investors will be watching for signs that these investments are translating into the promised revenue growth for 2026 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.