Microsoft’s data-center shortages to persist longer than expected - Bloomberg

Introduction & Market Context

Amazon.com Inc (NASDAQ:AMZN) released its second quarter 2025 financial results on July 31, showcasing strong performance across all business segments. The e-commerce and cloud computing giant reported better-than-expected results, with revenue reaching $167.7 billion, exceeding analyst expectations of $162.05 billion. The company’s earnings per share of $1.68 significantly outperformed the forecasted $1.32, representing a 27.27% beat.

Following the earnings announcement, Amazon’s stock initially rose 1.7% in after-hours trading to $235.67, reflecting positive investor sentiment. However, premarket trading on August 1 showed a 7.54% decline, suggesting some concerns about the company’s outlook or specific aspects of the results not highlighted in the presentation.

Quarterly Performance Highlights

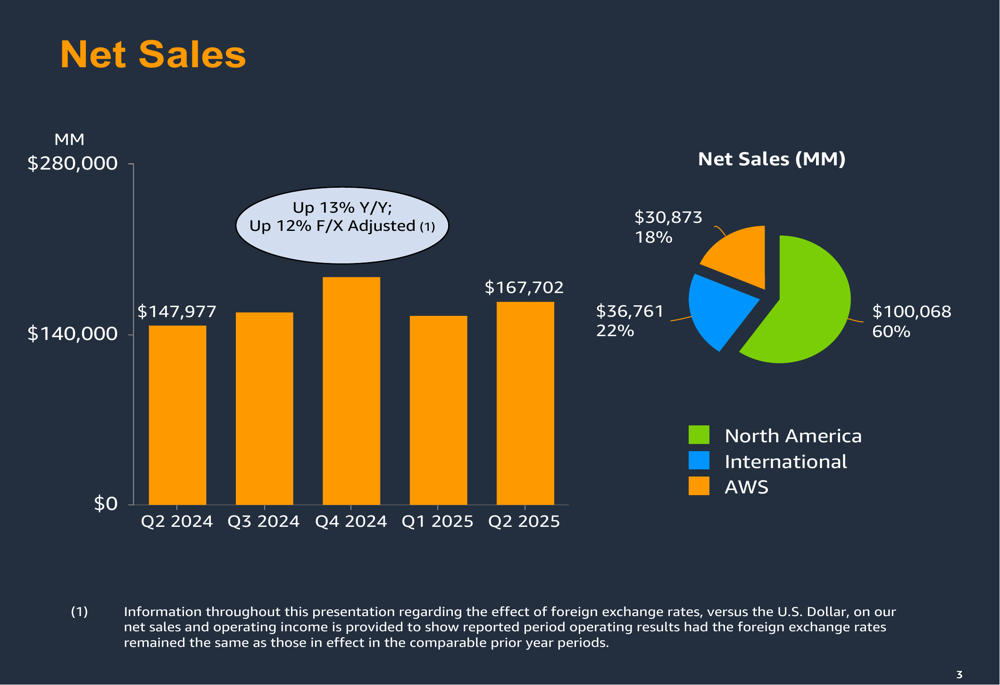

Amazon reported Q2 2025 net sales of $167.7 billion, representing a 13% year-over-year increase (12% on a foreign exchange-adjusted basis). This growth demonstrates the company’s continued ability to expand its business despite its already massive scale.

As shown in the following chart of quarterly net sales growth:

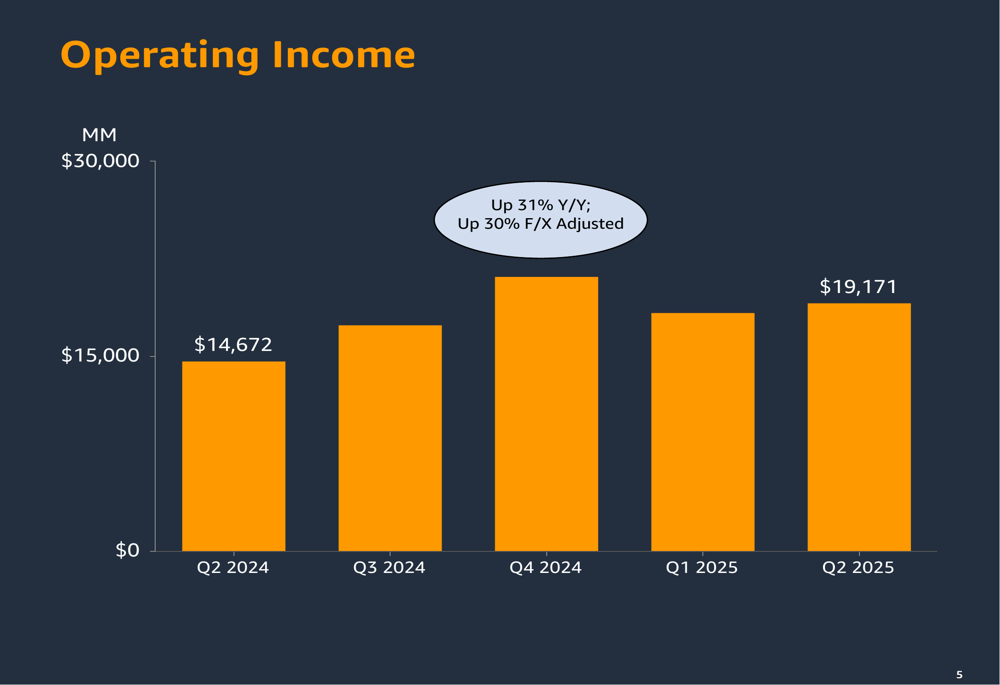

Operating income showed even stronger growth, reaching $19.2 billion in Q2 2025, a 31% increase compared to the same period last year. This substantial improvement in profitability reflects Amazon’s increasing operational efficiency and the growing contribution from higher-margin businesses like AWS and advertising.

The operating income trend is illustrated in this quarterly comparison:

Net income for the quarter totaled $18.2 billion, up 35% year-over-year, further highlighting Amazon’s ability to translate revenue growth into bottom-line results. On a trailing twelve-month basis, net income reached $70.6 billion, representing an impressive 59% increase compared to the previous year.

Segment Analysis

Amazon’s business is divided into three main segments: North America, International, and AWS (Amazon Web Services). Each segment showed strong performance in Q2 2025, though with varying growth rates and profitability profiles.

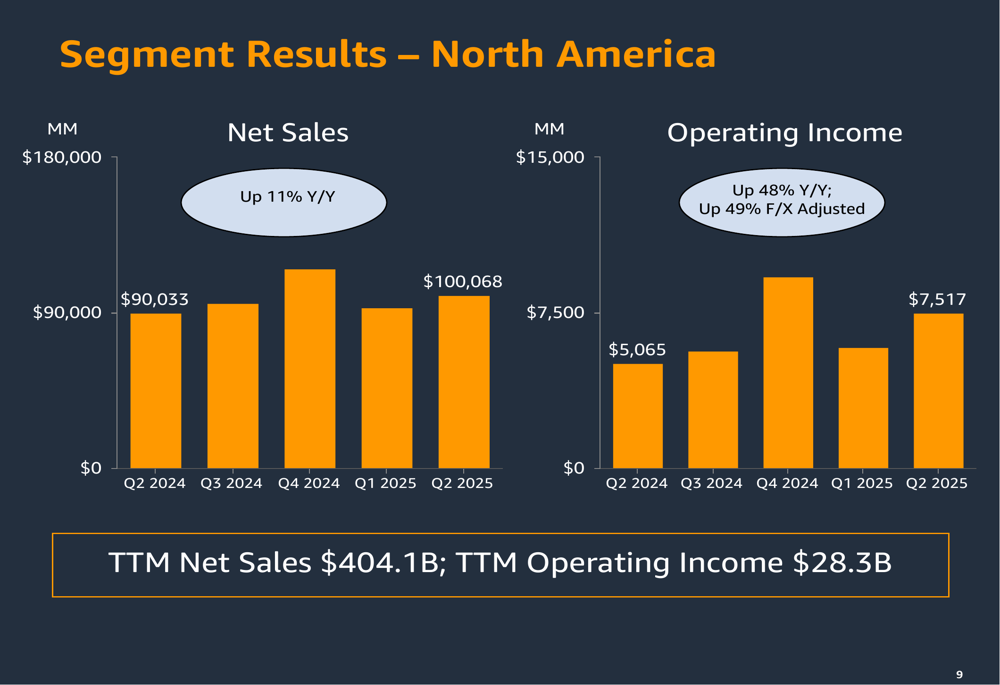

The North America segment, which includes the company’s e-commerce operations in the U.S. and Canada, generated $100.1 billion in net sales, up 11% year-over-year. More impressively, operating income for this segment surged 48% to $7.5 billion, indicating significant margin expansion in Amazon’s core market.

The North America segment’s performance is shown in the following chart:

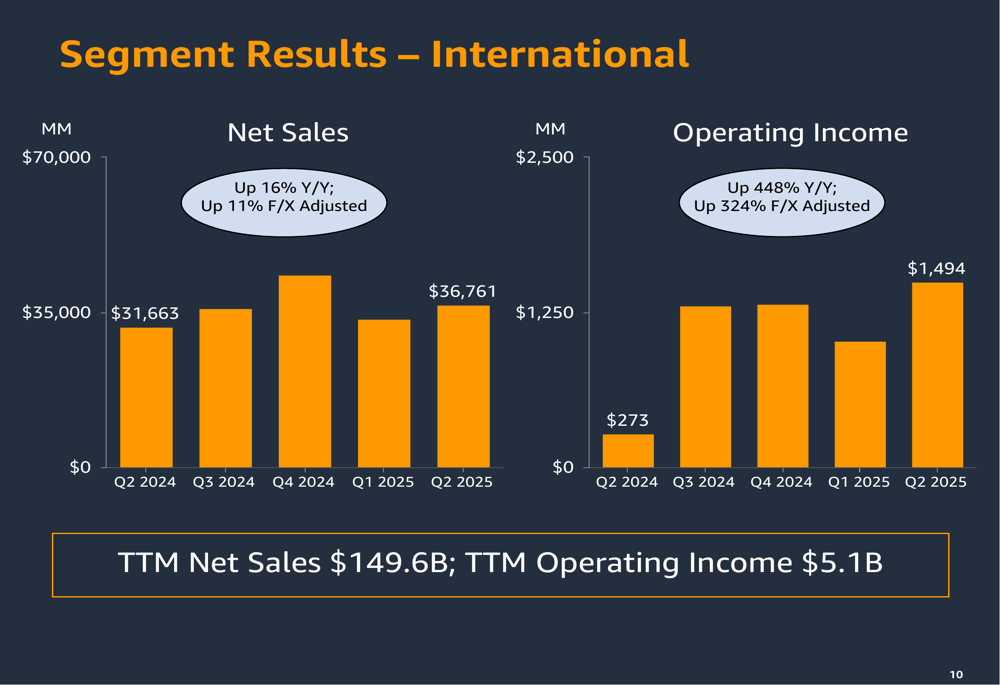

The International segment delivered the most dramatic improvement in profitability, with operating income skyrocketing 448% year-over-year to $1.5 billion, while net sales increased 16% to $36.8 billion. This remarkable profit growth suggests that Amazon’s investments in international markets are finally yielding substantial returns, as operations outside North America achieve greater scale and efficiency.

The International segment’s exceptional performance is illustrated here:

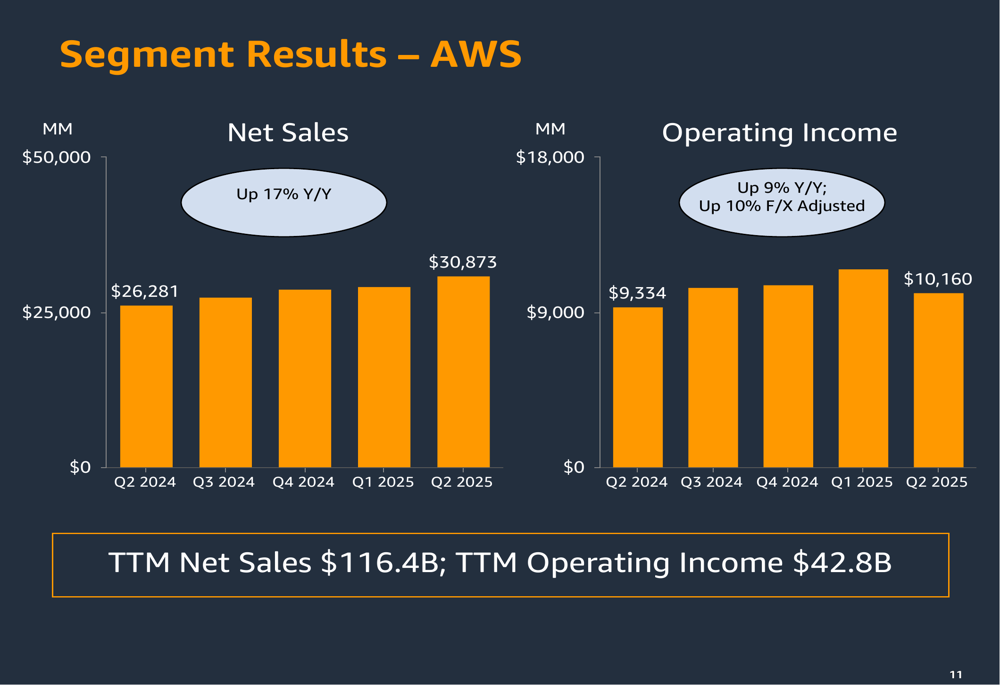

AWS, Amazon’s cloud computing division, maintained its position as a key growth driver with net sales of $30.9 billion, up 17% year-over-year. However, operating income growth was more modest at 9%, reaching $10.2 billion. This suggests some pressure on AWS margins, possibly due to increased competition in the cloud space or significant investments in AI capabilities, which CEO Andy Jassy described as "the biggest technology transformation of our lifetime" during the earnings call.

The AWS segment results are presented in this chart:

Cash Flow and Investment Trends

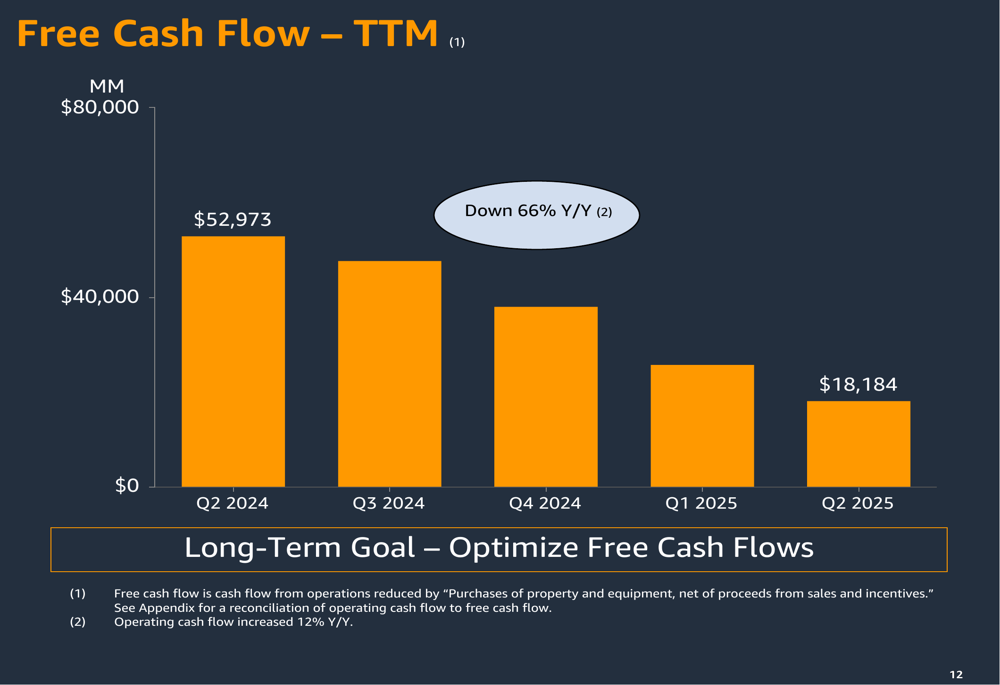

Despite strong earnings growth, Amazon’s free cash flow on a trailing twelve-month basis decreased significantly, falling 66% year-over-year to $18.2 billion. This decline was primarily driven by massive capital expenditures, with purchases of property and equipment nearly doubling to $103 billion on a TTM basis, up from $55 billion in the comparable period last year.

The following chart illustrates this substantial decline in free cash flow:

This aggressive investment strategy likely reflects Amazon’s commitment to expanding its logistics network, data center capacity for AWS, and other infrastructure to support future growth. During the earnings call, CEO Andy Jassy noted that demand currently exceeds capacity, particularly in AWS, stating, "We have more demand than we have capacity right now."

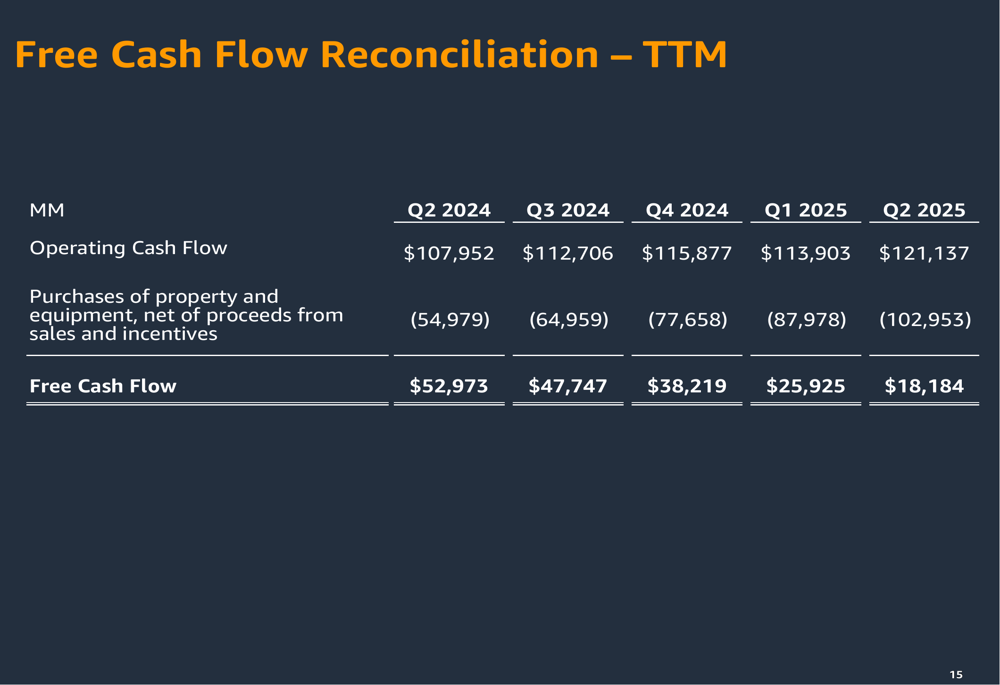

The reconciliation of free cash flow shows that operating cash flow actually increased by 12% year-over-year to $121.1 billion, but this growth was more than offset by the massive increase in capital expenditures:

Market Reaction and Forward Outlook

Amazon provided optimistic guidance for Q3 2025, projecting net sales between $174 billion and $179.5 billion. The company remains focused on enhancing customer value through improved selection, pricing, and convenience, while also anticipating continued growth in AWS driven by increased demand for AI and cloud migration services.

However, the significant premarket stock decline following the earnings announcement suggests investors may have concerns about the sustainability of Amazon’s massive capital expenditures or potential margin pressures in the AWS segment. The company’s P/E ratio of 37.31 indicates that investors still expect substantial growth, but the market reaction points to some uncertainty about the near-term outlook.

Potential risks highlighted in the earnings call include supply chain disruptions, increased competition in cloud computing and e-commerce, macroeconomic uncertainties, regulatory scrutiny, and capacity constraints in AWS. These factors will be important to monitor in the coming quarters as Amazon continues to execute its ambitious growth strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.