Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

Ambac Financial Group Inc (NYSE:AMBC) released its first quarter 2025 investor presentation on May 13, 2025, revealing a complex financial picture that triggered a significant market reaction. Despite reporting substantial revenue growth, the specialty insurance provider’s stock plummeted 20.18% to $6.66, reflecting investor concerns over widening losses and mixed segment performance.

The presentation comes as Ambac continues its strategic transformation from a financial guarantee business to a specialty property and casualty (P&C) insurance platform. While the company highlighted several growth metrics, the market’s negative reaction suggests investors remain skeptical about Ambac’s path to profitability.

Quarterly Performance Highlights

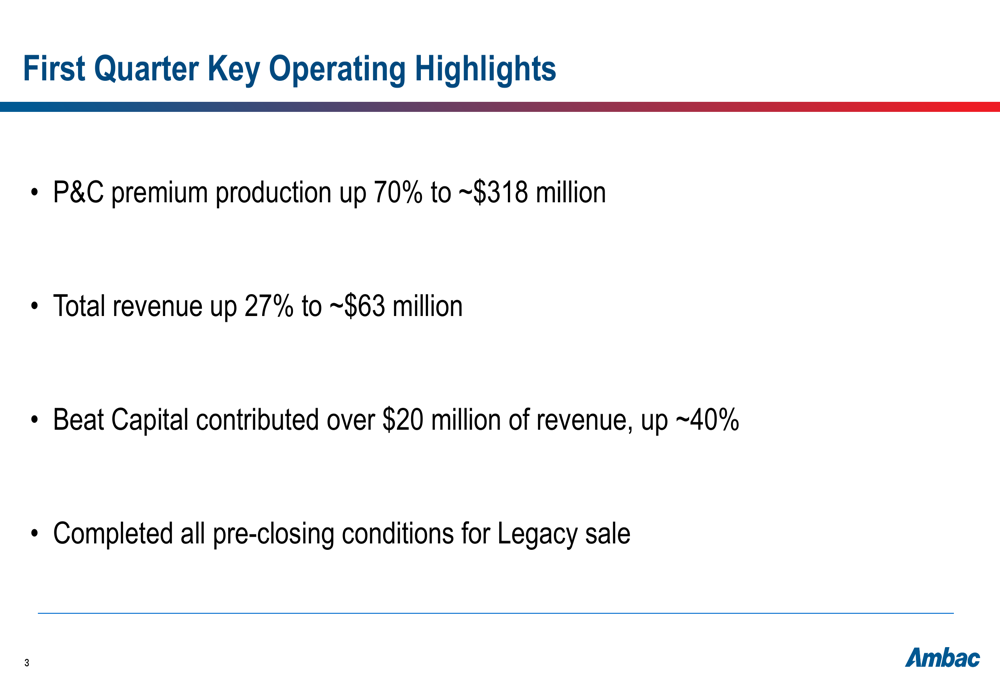

Ambac’s presentation emphasized several positive developments in the first quarter, including a 27% year-over-year increase in total revenue to approximately $63 million. The company also reported a 70% increase in P&C premium production to approximately $318 million, demonstrating strong top-line momentum.

As shown in the following quarterly highlights slide, the company completed all pre-closing conditions for its Legacy business sale, a key strategic milestone in its transformation:

However, these positive metrics were overshadowed by a significant deterioration in the bottom line. Ambac reported a net loss of $16.1 million for Q1 2025, compared to a $4.1 million loss in the same period last year. The company’s adjusted EBITDA also declined to a loss of $1.3 million, down from a positive $0.4 million in Q1 2024.

Segment Analysis: Cirrata Shows Strong Growth

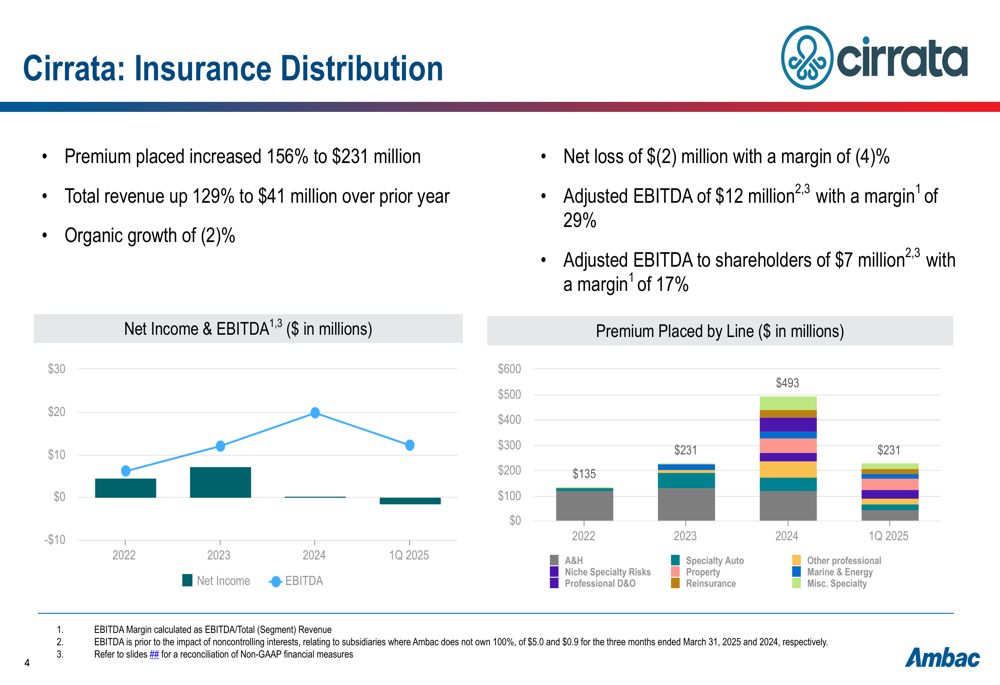

Ambac’s insurance distribution segment, Cirrata, emerged as a bright spot in the quarterly results. The segment demonstrated remarkable growth with premium placed increasing 156% to $231 million and total revenue rising 129% to $41 million compared to the prior year.

The following slide illustrates Cirrata’s impressive trajectory in both premium growth and EBITDA performance:

Despite the strong revenue performance, Cirrata reported a net loss of $2 million with a margin of -4%. However, the segment’s adjusted EBITDA reached $12 million with a healthy margin of 29%, suggesting underlying operational strength despite bottom-line challenges.

Segment Analysis: Everspan Faces Headwinds

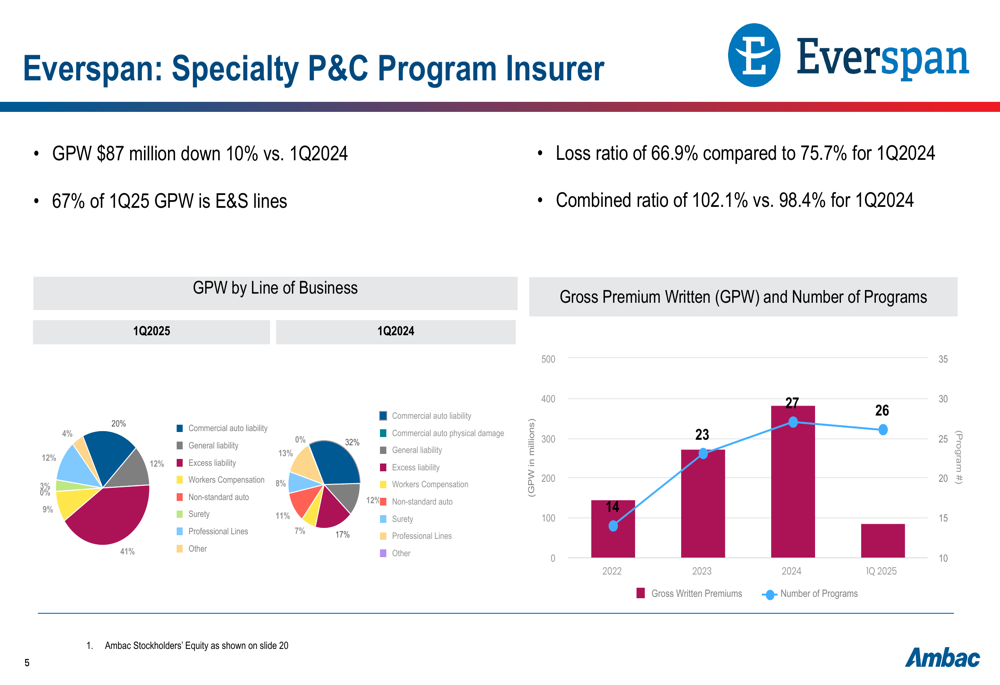

In contrast to Cirrata’s strong showing, Ambac’s specialty P&C program insurer, Everspan, faced more significant challenges. Gross written premiums (GPW) declined 10% year-over-year to $87 million, while the combined ratio deteriorated to 102.1% from 98.4% in Q1 2024, indicating underwriting losses.

The following slide details Everspan’s performance metrics and business mix:

On a positive note, Everspan’s loss ratio improved to 66.9% from 75.7% in the prior year period, suggesting some progress in claims management. The segment also maintained a diverse business mix, with 67% of Q1 2025 GPW coming from excess and surplus (E&S) lines.

Financial Analysis and Challenges

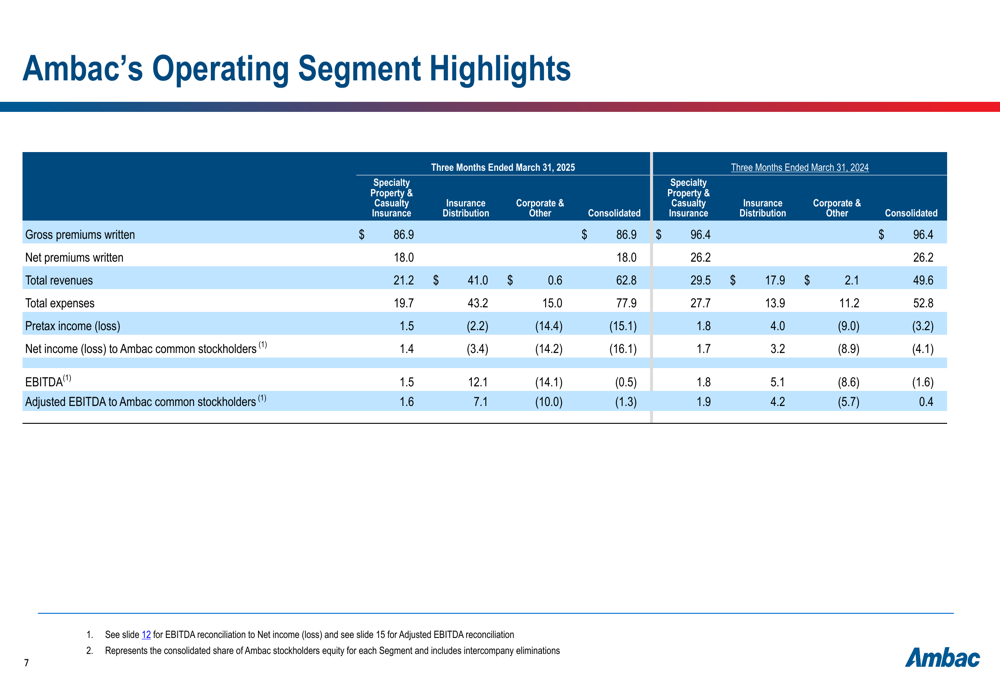

A detailed breakdown of Ambac’s operating segments reveals the contrasting performance across the company’s business units. While the Insurance Distribution segment showed strong revenue growth, both the Specialty P&C Insurance and Corporate segments faced challenges.

The following segment comparison highlights these disparities:

The consolidated financial results underscore Ambac’s current profitability challenges, with expenses outpacing revenue growth. Total (EPA:TTEF) expenses increased significantly year-over-year, contributing to the wider net loss despite the strong top-line performance.

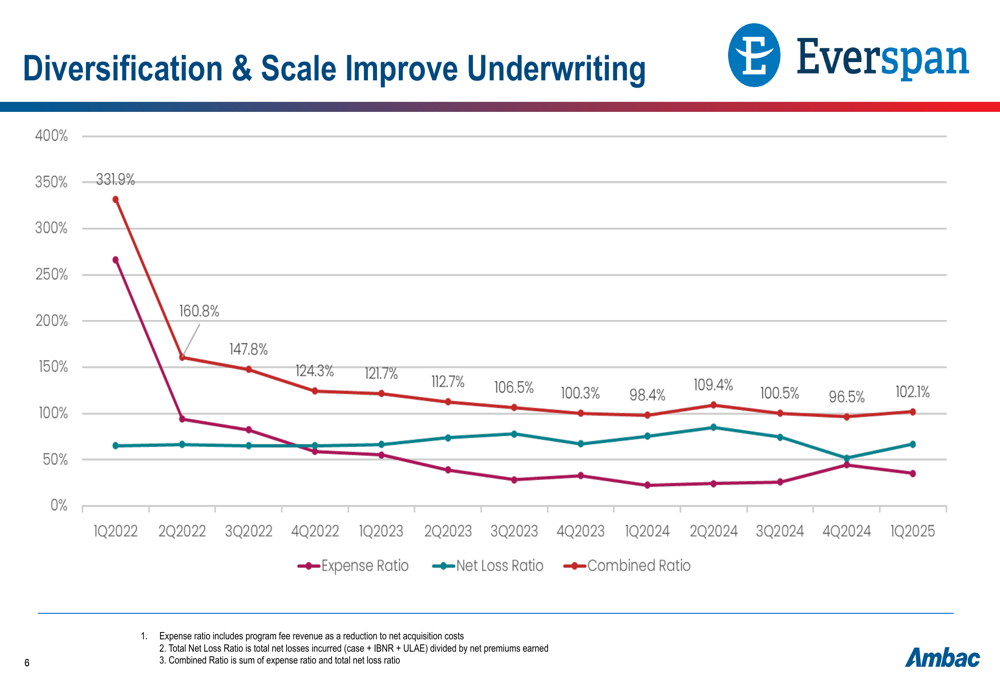

Ambac’s underwriting metrics have shown improvement over time, as illustrated in the following trend chart:

While the combined ratio has improved dramatically from over 300% in early 2022 to 102.1% in Q1 2025, it remains above the crucial 100% threshold, indicating that the company is still not achieving underwriting profitability.

Strategic Initiatives and Future Outlook

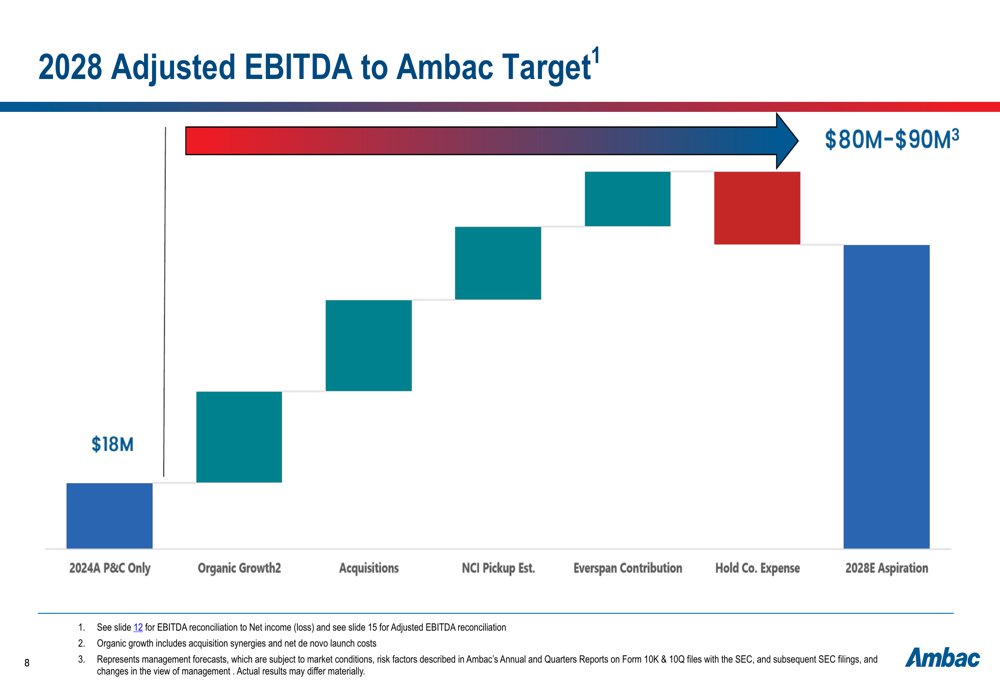

Despite current challenges, Ambac’s presentation outlined an ambitious growth strategy aimed at achieving adjusted EBITDA of $80-90 million by 2028. This represents a substantial increase from the 2024 P&C-only EBITDA of $18 million.

The following waterfall chart illustrates the company’s path to reaching this target:

The growth strategy relies on a combination of organic growth, acquisitions, and improved contribution from Everspan. However, the significant gap between current performance and future targets, coupled with the widening losses in Q1 2025, may explain investors’ skepticism as reflected in the sharp stock decline.

During the earnings call, CEO Claude LeBlanc emphasized the company’s long-term focus, stating, "We are building our business for the long term," and highlighting Ambac’s "unique value proposition" in the market. Management also noted that the pending sale of the legacy business would transform Ambac into a pure-play specialty P&C insurer.

While Ambac’s Q1 2025 presentation showcases impressive revenue growth and strategic progress, the widening losses and mixed segment performance present significant challenges. The stark market reaction suggests investors will need to see clearer signs of bottom-line improvement before regaining confidence in Ambac’s transformation strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.