Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Ambac Financial Group (NYSE:AMBC) released its second quarter 2025 investor presentation, highlighting substantial premium growth amid its ongoing transformation into a specialty property and casualty insurer. The company’s stock has faced pressure in recent months, trading at $8.29 as of August 7, 2025, down 2.93% and significantly below its 52-week high of $13.64.

The presentation comes after a challenging first quarter where Ambac reported a net loss from continuing operations of $16 million, or $0.58 per share. The Q2 results suggest some operational improvements but continued profitability challenges as the company pursues its strategic transformation.

Quarterly Performance Highlights

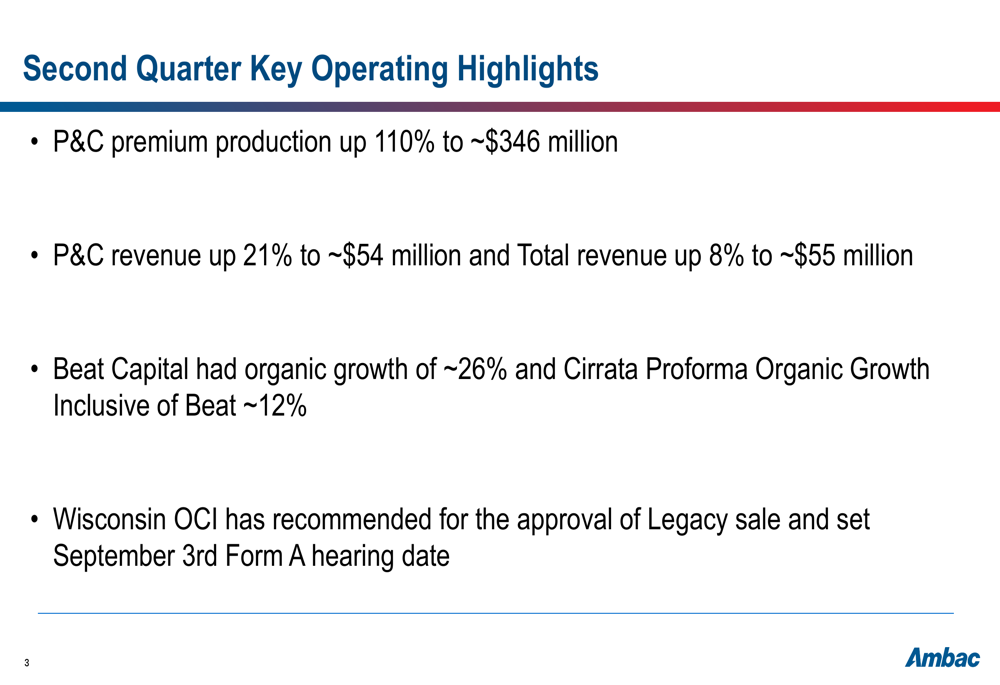

Ambac reported impressive top-line growth in the second quarter, with property and casualty premium production surging 110% to approximately $346 million. P&C revenue increased 21% to approximately $54 million, while total revenue rose 8% to approximately $55 million.

As shown in the following key operating highlights:

The company also announced that the Wisconsin Office of the Commissioner of Insurance has recommended approval of Ambac’s legacy business sale, with a Form A hearing date set for September 3rd. This represents a significant milestone in the company’s transformation strategy to become a pure-play specialty P&C insurer.

Segment Analysis

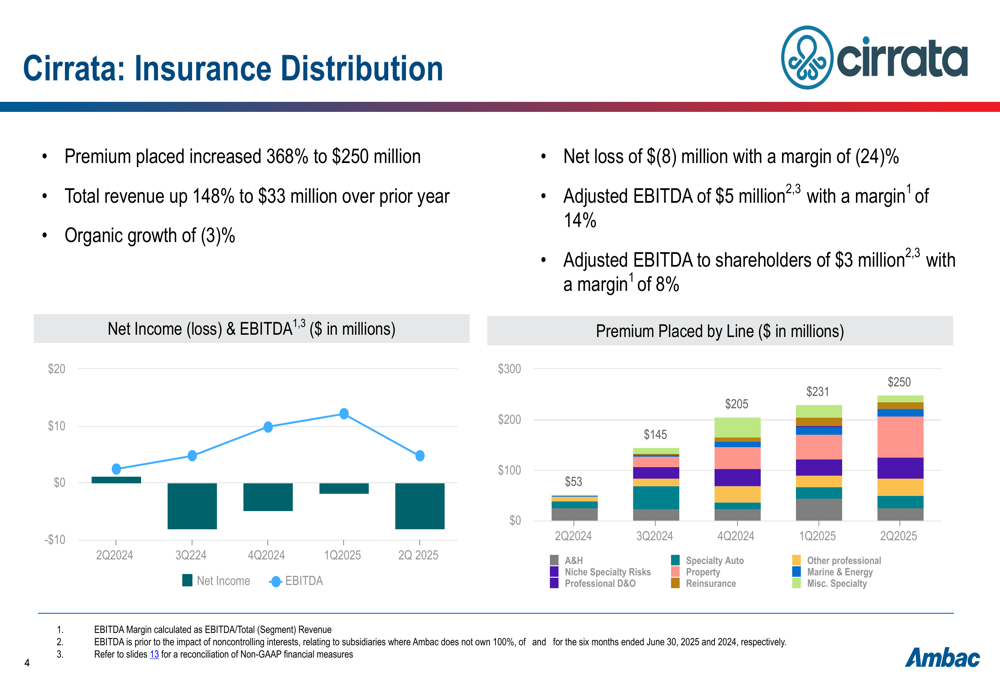

Ambac’s Insurance Distribution segment, Cirrata, showed dramatic growth in premium placement and revenue, though organic growth remains challenging. Premium placed increased 368% to $250 million, while total revenue grew 148% to $33 million compared to the prior year. However, organic growth decreased by 3%, indicating that acquisitions are driving much of the expansion.

The segment posted a net loss of $8 million with a margin of (24%), while adjusted EBITDA reached $5 million with a 14% margin. The following chart illustrates Cirrata’s performance metrics and premium distribution by line:

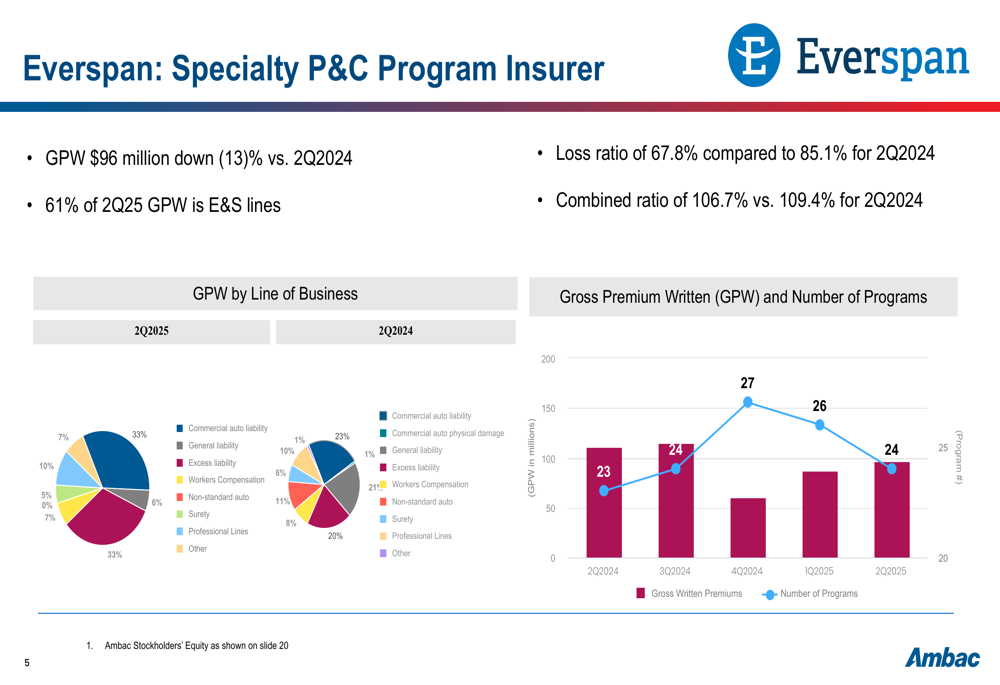

In the Specialty P&C Program Insurer segment, Everspan reported gross premium written (GPW) of $96 million, down 13% compared to Q2 2024. However, underwriting metrics showed improvement, with the loss ratio decreasing to 67.8% from 85.1% in Q2 2024, and the combined ratio improving to 106.7% from 109.4%.

The company noted that 61% of Everspan’s Q2 2025 GPW came from excess and surplus (E&S) lines, highlighting its focus on specialty risks. The following breakdown shows Everspan’s premium distribution and program count:

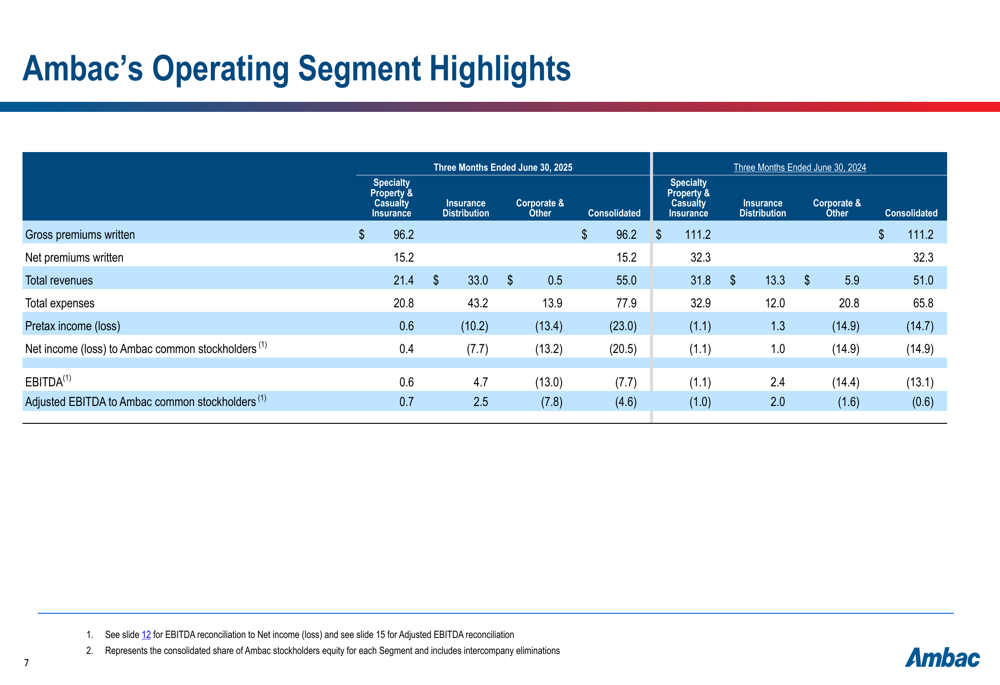

Ambac’s consolidated segment performance shows the company’s progress and ongoing challenges across its business units:

Strategic Initiatives & Transformation

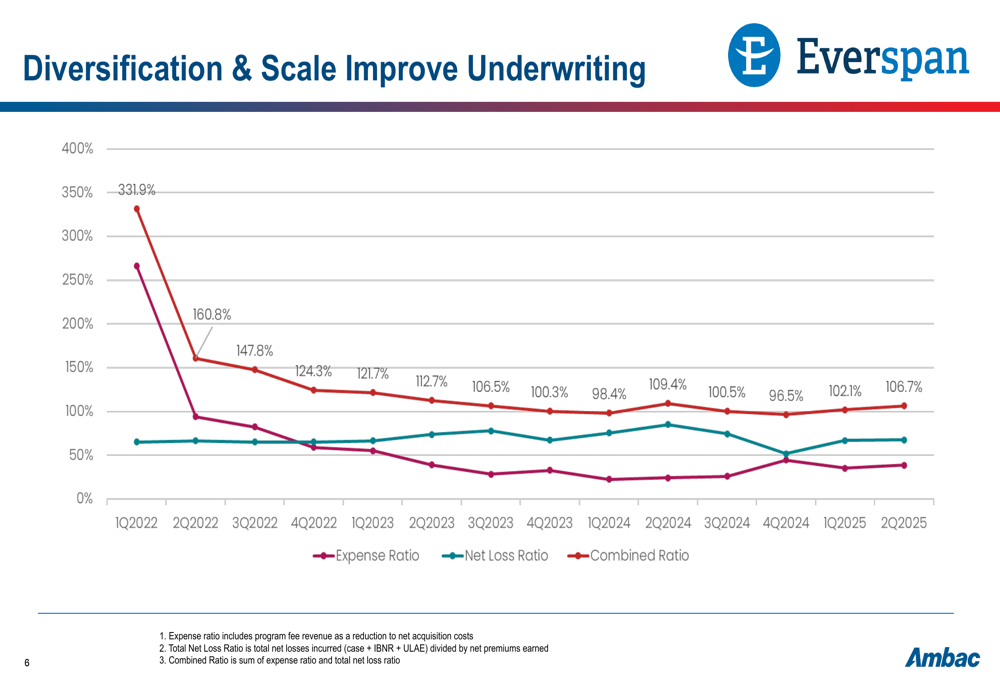

A key element of Ambac’s transformation strategy is improving underwriting results through diversification and scale. The company has made significant progress in reducing its combined ratio from over 330% in early 2022 to 106.7% in Q2 2025, as illustrated in this trend chart:

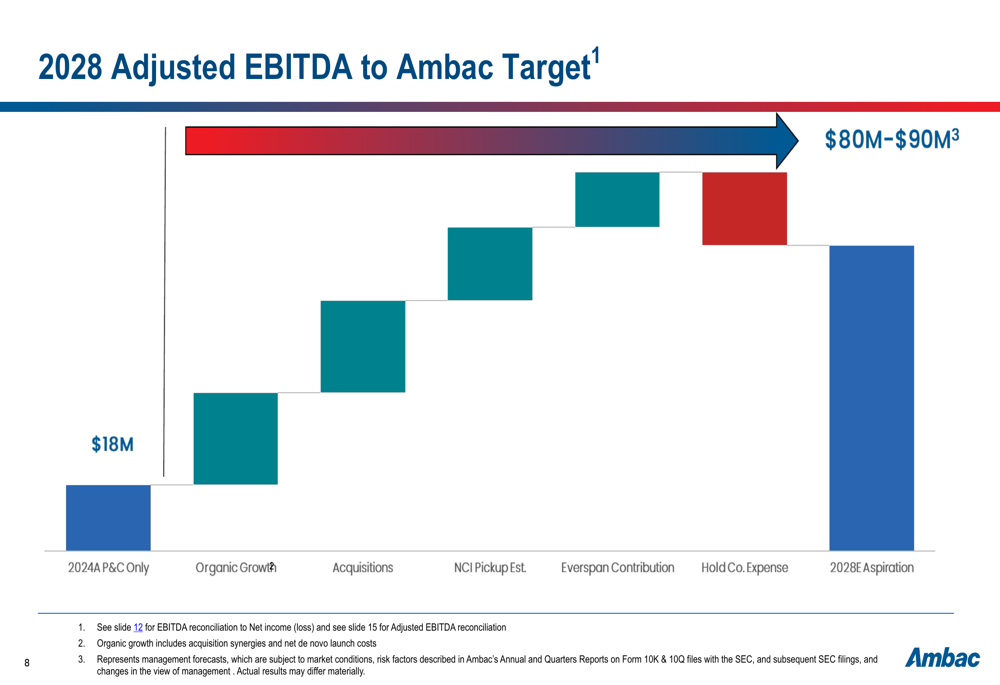

Looking forward, Ambac has outlined an ambitious path to achieve adjusted EBITDA of $80-90 million by 2028. Starting from a base of $18 million in 2024 for P&C operations only, the company plans to grow through a combination of organic expansion, strategic acquisitions, and improved performance at Everspan.

The following waterfall chart details Ambac’s roadmap to its 2028 EBITDA target:

Financial Analysis

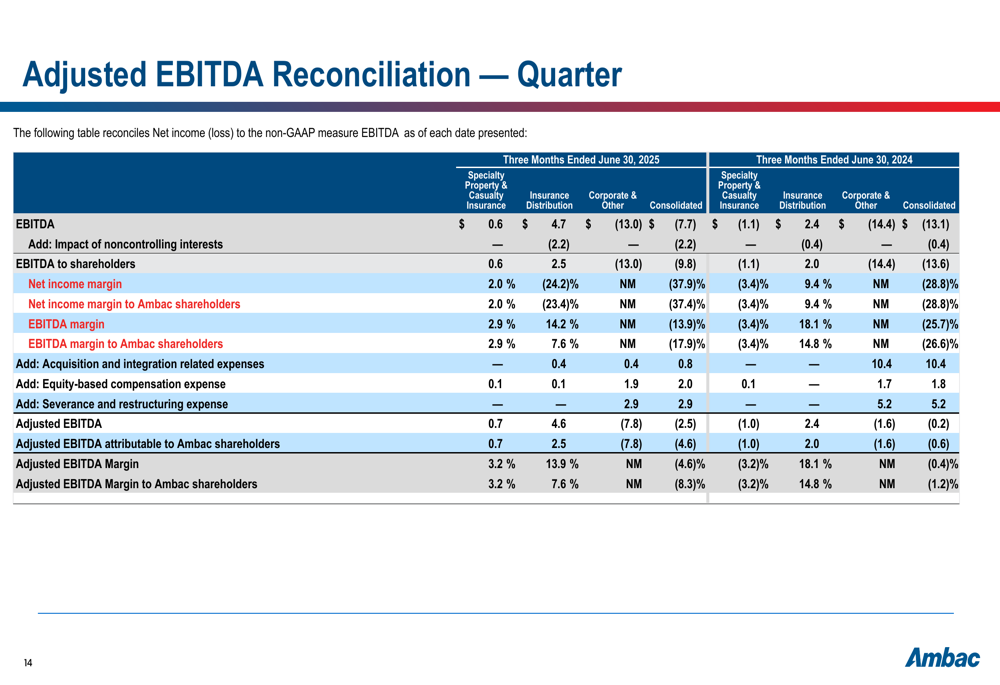

Ambac’s financial reconciliations provide deeper insight into its performance metrics. The company’s adjusted EBITDA reconciliation shows the impact of various adjustments to arrive at this non-GAAP measure:

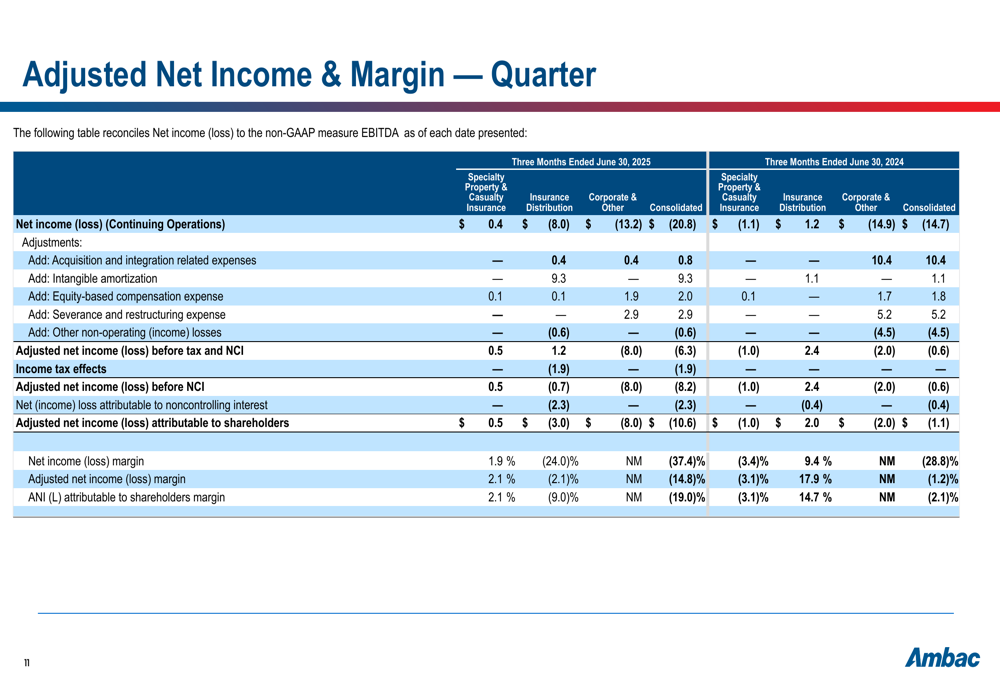

Similarly, the adjusted net income reconciliation reveals the company’s underlying performance after accounting for acquisition-related expenses, intangible amortization, and other non-recurring items:

Forward-Looking Statements

While Ambac’s presentation emphasizes growth and transformation, investors should note the gap between current performance and the company’s ambitious 2028 targets. The Q1 2025 earnings showed a wider-than-expected net loss, and the Q2 presentation indicates continued profitability challenges despite strong premium growth.

The pending sale of Ambac’s legacy business represents a pivotal moment in the company’s transformation strategy. If approved at the September 3rd hearing, this transaction would significantly alter Ambac’s risk profile and balance sheet structure, potentially creating a clearer path to achieving the company’s long-term financial targets.

Market reaction to Ambac’s recent performance has been cautious, with the stock trading well below its 52-week high. Investors appear to be taking a wait-and-see approach as the company works to improve profitability while pursuing aggressive growth through both organic expansion and acquisitions.

As Ambac continues its transformation journey, key metrics to watch include the combined ratio trend, organic growth rates across segments, and progress toward the 2028 adjusted EBITDA target of $80-90 million.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.