Futures turn lower; Musk’s $1 trn pay package approved - what’s moving markets

Introduction & Market Context

Ambev SA (BOVESPA:ABEV3) presented its third quarter 2025 earnings results on October 30, showing resilience in revenue growth despite volume challenges across several key markets. The company’s stock has been performing well, with a 3.68% increase following the presentation, reflecting positive investor sentiment despite industry headwinds.

The Brazilian beverage giant demonstrated its ability to navigate a challenging consumer environment through effective pricing strategies and continued focus on premiumization, digital transformation, and operational efficiency.

Quarterly Performance Highlights

Ambev reported 7% EPS growth for Q3 2025, supported by net revenue growth with resilient net revenue per hectoliter (NR/hl) up 7% and EBITDA growth with margin expansion across most business units.

As shown in the following quarterly delivery highlights:

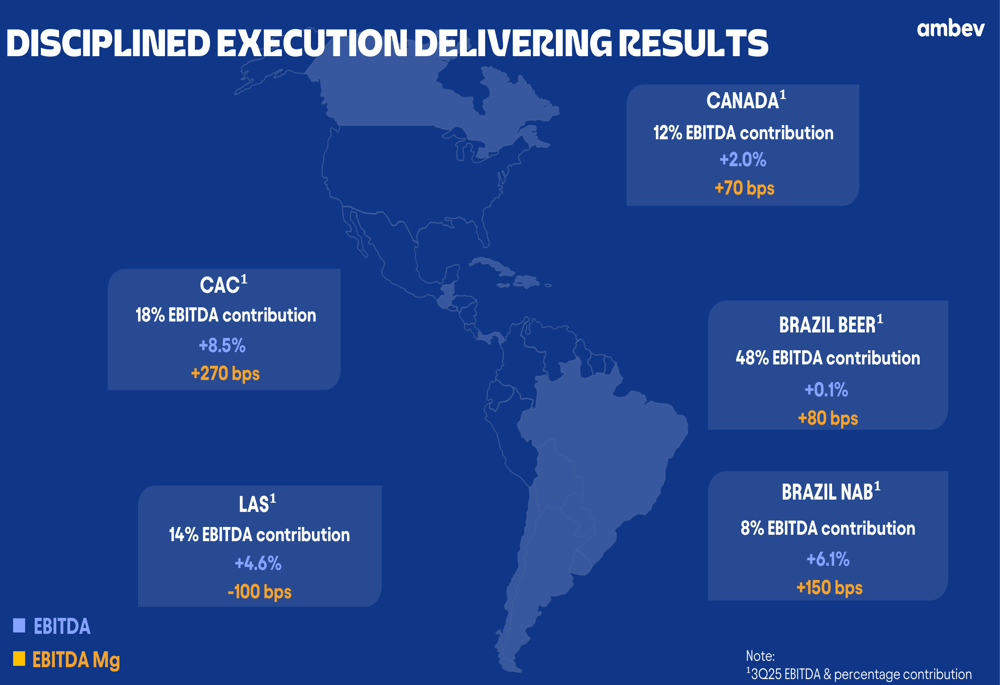

The company’s performance varied significantly across regions, with volume declines in most markets offset by improved revenue per hectoliter. Brazil Beer, which represents 48% of Ambev’s EBITDA, saw volumes decline by 7.7% but achieved NR/hl growth of 5.7%. Management attributed the volume decline entirely to industry softness rather than market share losses.

The regional EBITDA contribution breakdown reveals the disciplined execution across markets:

Brazil’s non-alcoholic beverage (NAB) business experienced an 8.6% volume decline but achieved impressive NR/hl growth of 10.0%. The Latin America South (LAS) region, primarily Argentina, saw volumes decline by 0.8% with NR/hl growing 10.0%, while the Central America and Caribbean (CAC) region delivered volume growth of 1.3% with NR/hl up 1.4%. Canada experienced a 2.0% volume decline but grew NR/hl by 2.0%.

Strategic Initiatives

Ambev’s growth strategy continues to focus on three key pillars: leading and growing the category, digitizing and monetizing their ecosystem, and optimizing the business.

The premium and super premium segments remain bright spots, with volumes up more than 9%, reaching their highest share levels since 2015 according to company estimates. This performance stands in contrast to the core segment, which declined by low-teens percentages in Brazil.

The company identified several structural factors affecting the Brazilian beer market:

Ambev’s digital ecosystem continues to gain momentum, with the BEES B2B platform reaching BRL 8.0 billion in annualized gross merchandise value (GMV). Meanwhile, Zé Delivery, the company’s direct-to-consumer platform, saw GMV increase by 7% with average order value (AOV) up 9%.

The digital transformation is providing valuable data insights:

Detailed Financial Analysis

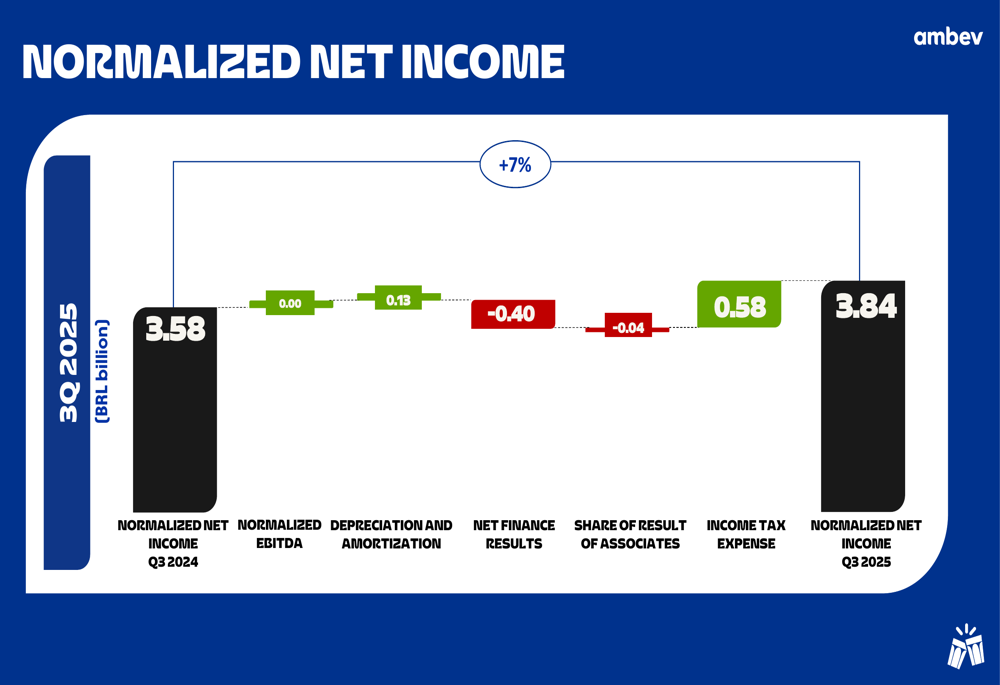

Ambev’s normalized net income for Q3 2025 reached 3.84 billion BRL, representing a 7% increase from 3.58 billion BRL in Q3 2024. This growth was supported by improvements in depreciation and amortization (+0.13) and income tax expense (+0.58), partially offset by negative impacts from net finance results (-0.40) and share of results from associates (-0.04).

The company’s effective tax rate (ETR) dropped significantly to 6.7% compared to 23.6% in Q3 2024, contributing substantially to the bottom-line improvement. This reduction was attributed to tax amnesty partial reduction, fiscal incentives, and the Barbados divestment.

The financial performance breakdown is illustrated in this waterfall chart:

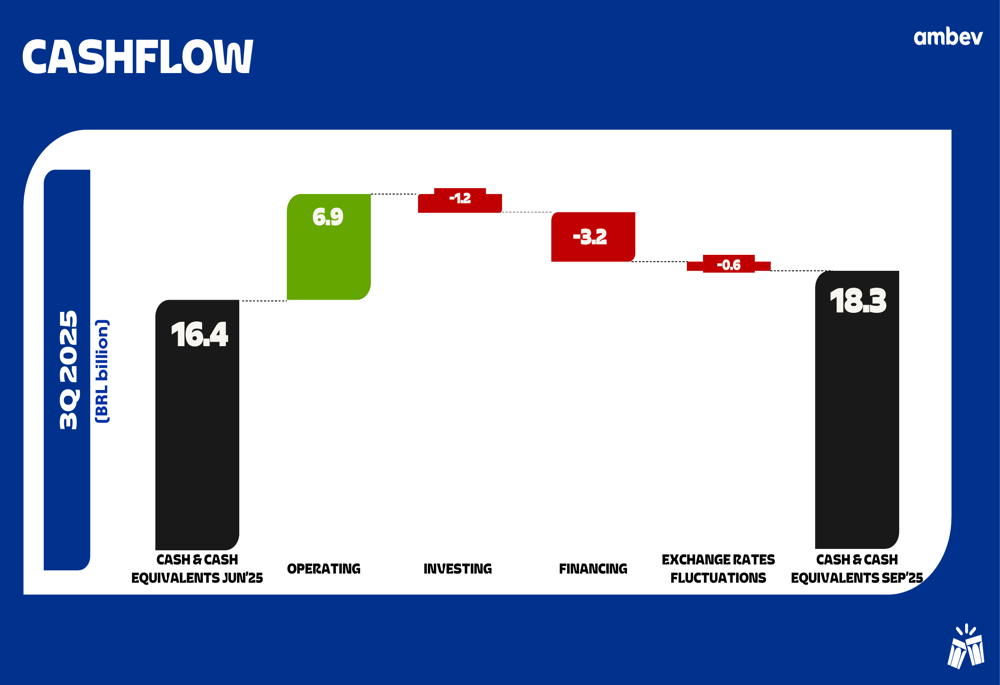

Cash flow performance remained strong, with cash and cash equivalents increasing from 16.4 billion BRL in June 2025 to 18.3 billion BRL by the end of September 2025. Operating activities contributed 6.9 billion BRL, while investing activities used 1.2 billion BRL and financing activities used 3.2 billion BRL.

Ambev continues to prioritize shareholder returns, announcing 6 billion BRL in dividends year-to-date and approving a share buyback program of 2.5 billion BRL.

Forward-Looking Statements

Looking ahead, Ambev management expressed confidence in closing the year strongly despite ongoing challenges in the Brazilian beer market. The company highlighted the upcoming 2026 FIFA World Cup as a significant opportunity to connect with consumers and drive growth.

Management remains focused on cost discipline to offset expected cost pressures, freeing up resources to invest in the business while maintaining margin expansion. The company plans to continue investing in premium brands and digital platforms while optimizing its core portfolio.

Ambev’s ability to grow revenue per hectoliter above inflation while managing costs effectively positions the company well for continued profitability improvement, even as it navigates volume challenges in key markets. The company’s diversified geographic footprint and product portfolio provide resilience against regional economic headwinds.

Building on the 15% net income growth reported in Q2 2025, Ambev’s Q3 results demonstrate continued momentum, albeit at a somewhat moderated pace with 7% EPS growth. The company’s strategic focus on premiumization, digital transformation, and operational efficiency appears to be yielding results despite challenging market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.