BTC Development Corp. completes $253 million IPO on NASDAQ

Introduction & Market Context

Amentum Holdings LLC (NYSE:AMTM) presented its Q3 FY25 earnings results on August 6, 2025, showcasing continued operational strength despite premarket trading indicating investor caution. The company’s shares were down 3.83% in premarket trading at $24.34, following a 3.39% gain in the previous session.

The defense and engineering services provider reported solid financial performance while highlighting its strategic focus on high-growth areas including nuclear energy, missile defense, and space technologies. This quarter’s results build upon the momentum seen in Q2, with further improvements in key metrics and continued progress on the company’s deleveraging initiatives.

Quarterly Performance Highlights

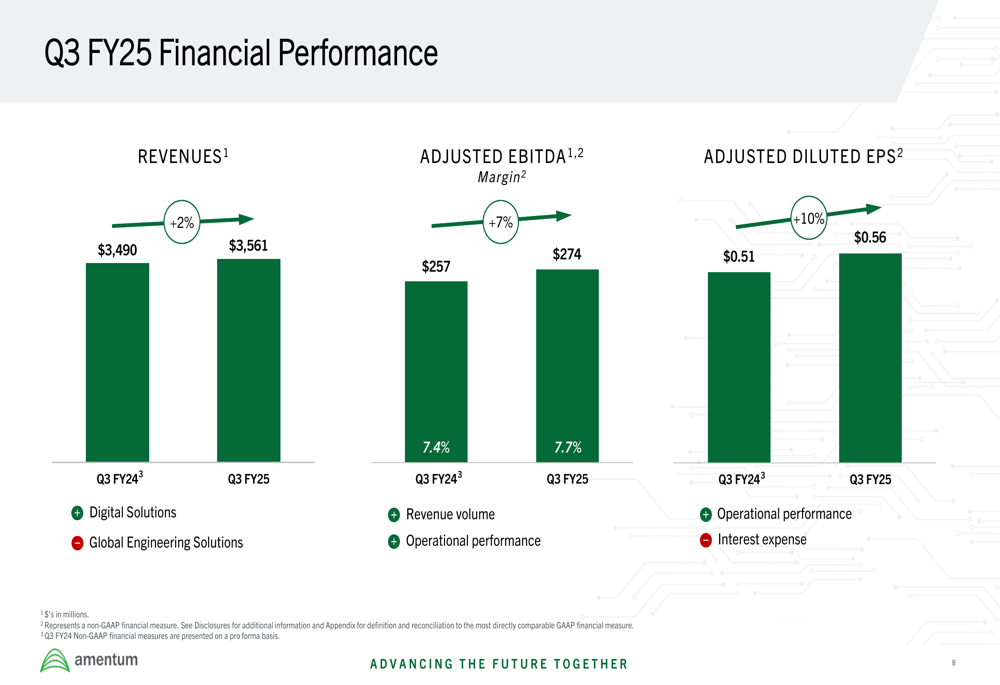

Amentum reported Q3 FY25 revenue of $3.6 billion, representing a 2% year-over-year increase from Q3 FY24. Adjusted EBITDA grew 7% to $274 million, while adjusted diluted EPS increased 10% to $0.56. The company also generated $100 million in free cash flow during the quarter.

As shown in the following financial performance overview:

The results demonstrate continued improvement from Q2 FY25, when the company reported revenue of $3.5 billion and EPS of $0.53. This sequential growth reflects Amentum’s successful execution of its strategic initiatives and strong market positioning.

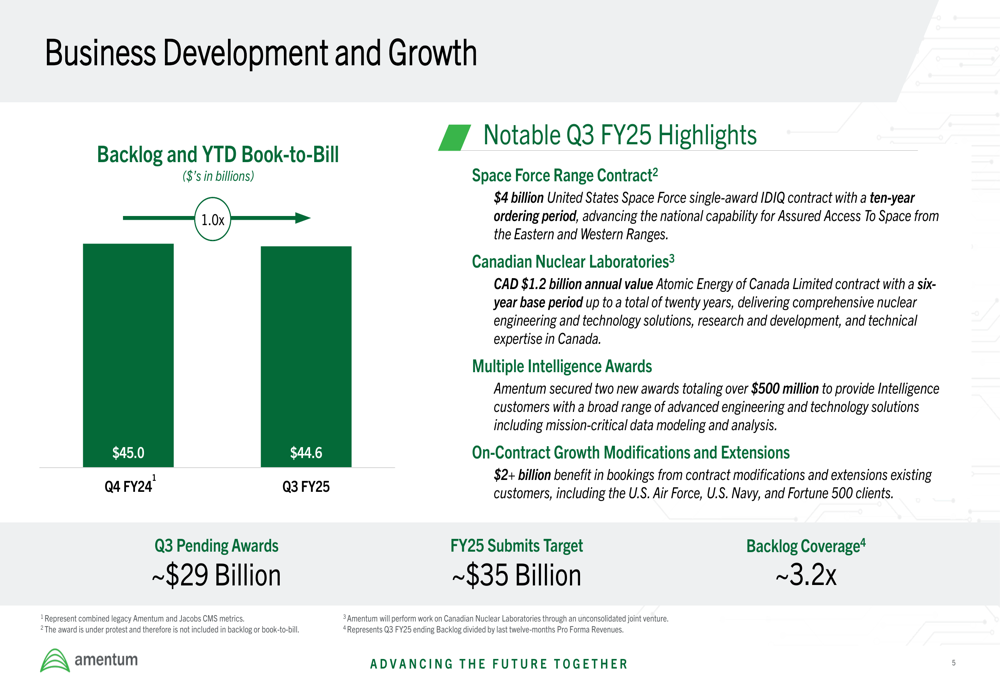

The company maintained a solid backlog of $44.6 billion with a year-to-date book-to-bill ratio of 1.0x, providing good visibility for future revenues. Notable Q3 contract wins included a $4 billion United States Space Force single-award IDIQ contract and a CAD $1.2 billion Atomic Energy of Canada Limited contract for Canadian Nuclear Laboratories.

The business development pipeline remains robust with approximately $29 billion in pending awards and a FY25 submission target of approximately $35 billion, as illustrated in the following slide:

Segment Performance Analysis

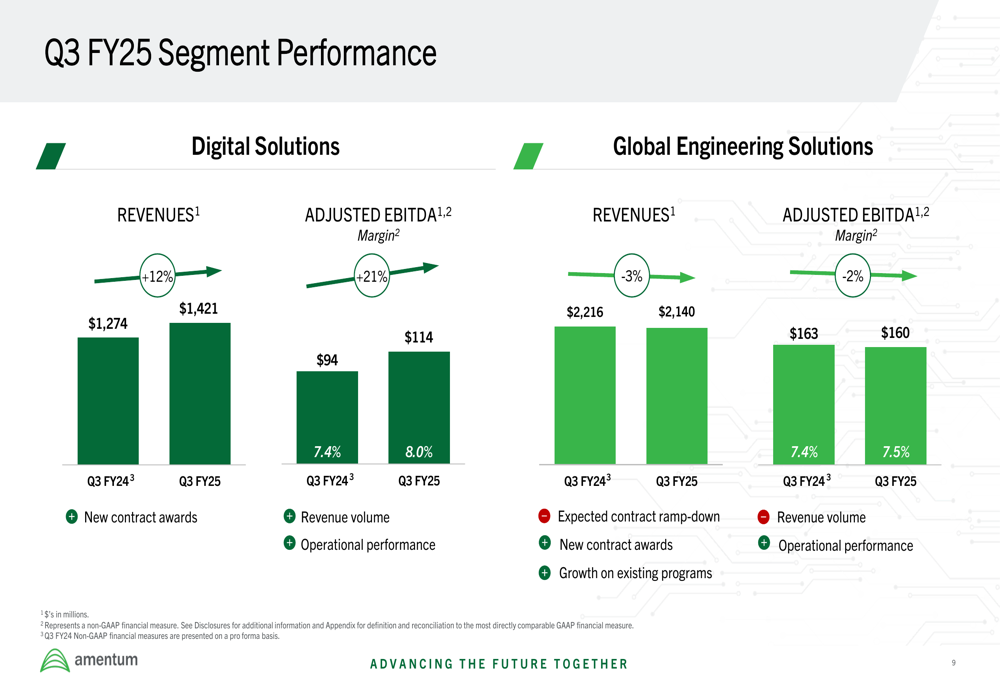

Amentum’s performance varied across its two business segments. The Digital Solutions segment showed strong growth with revenues of $1,421 million, up 12% year-over-year, and adjusted EBITDA of $114 million, representing a 21% increase. This segment achieved an 8.0% EBITDA margin.

In contrast, the Global Engineering Solutions segment experienced a slight decline with revenues of $2,140 million, down 3% year-over-year, and adjusted EBITDA of $160 million, a 2% decrease. This segment maintained a 7.5% EBITDA margin.

The following segment breakdown illustrates these contrasting performances:

The divergent segment performance reflects Amentum’s strategic shift toward higher-margin digital solutions while managing a more mature engineering solutions portfolio. The company’s successful completion of divestitures during the quarter is part of its strategy to focus on core high-growth areas.

Strategic Positioning in Nuclear Market

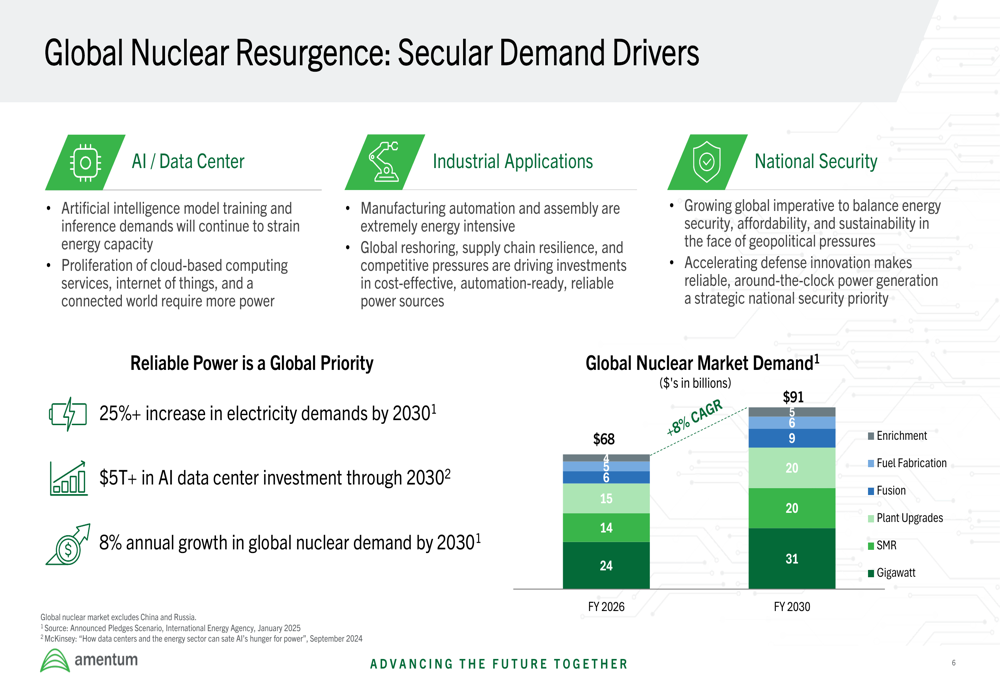

A significant portion of Amentum’s presentation focused on the company’s positioning within the growing global nuclear market. Management highlighted several secular demand drivers, including increasing energy requirements for AI data centers, industrial applications, and national security priorities.

The global nuclear market is projected to grow at an 8% CAGR, expanding from $68 billion in FY2026 to $91 billion in FY2030. This growth is driven by factors including a projected 25%+ increase in electricity demands by 2030 and over $5 trillion in AI data center investment through 2030.

The following slide illustrates these market dynamics:

Amentum positions itself as a global leader in nuclear engineering with capabilities spanning the entire lifecycle from design and construction to operations and decommissioning. The company estimates its total addressable market at approximately $20 billion, with expectations for this to more than double by 2035.

The nuclear market opportunity includes approximately 250 new gigawatt power plants and 500 new small modular reactors by 2050, along with 60+ gigawatt reactor life extensions through 2050.

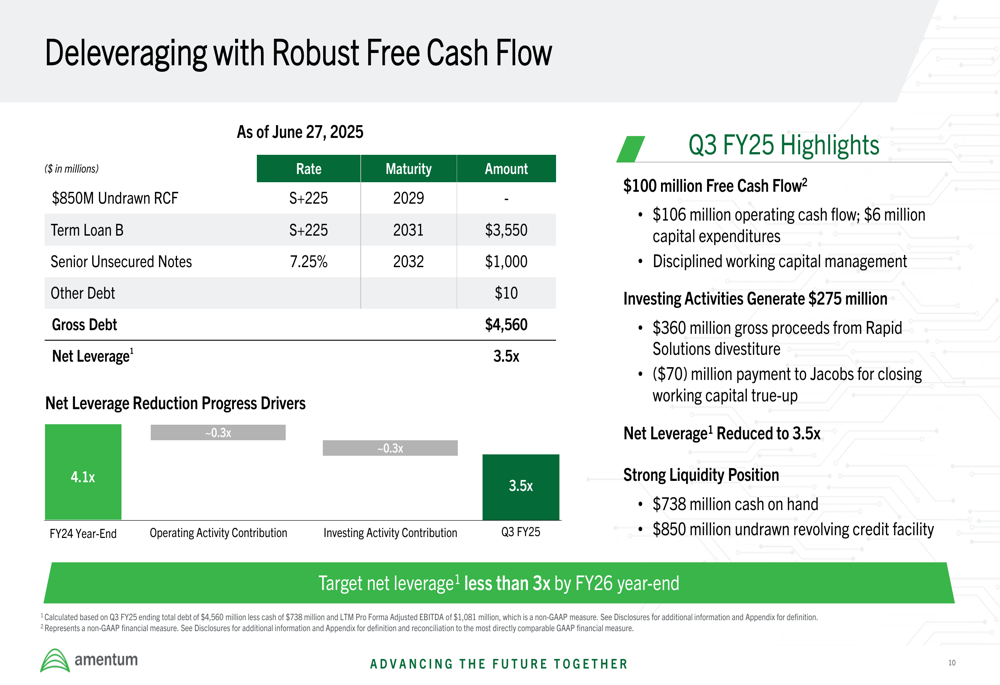

Deleveraging Progress

Amentum continues to make significant progress on its deleveraging initiatives. The company reduced its net leverage ratio from 4.1x at FY24 year-end to 3.5x in Q3 FY25, which represents further improvement from the 4.0x reported in Q2 FY25.

The company ended the quarter with $738 million in cash on hand and an $850 million undrawn revolving credit facility, providing substantial financial flexibility. Amentum’s debt structure consists primarily of a $3,550 million Term Loan B and $1,000 million in Senior Unsecured Notes.

The following slide details the company’s deleveraging progress and debt structure:

Management reaffirmed its target to reduce net leverage to less than 3x by FY26 year-end, demonstrating a continued commitment to strengthening the balance sheet.

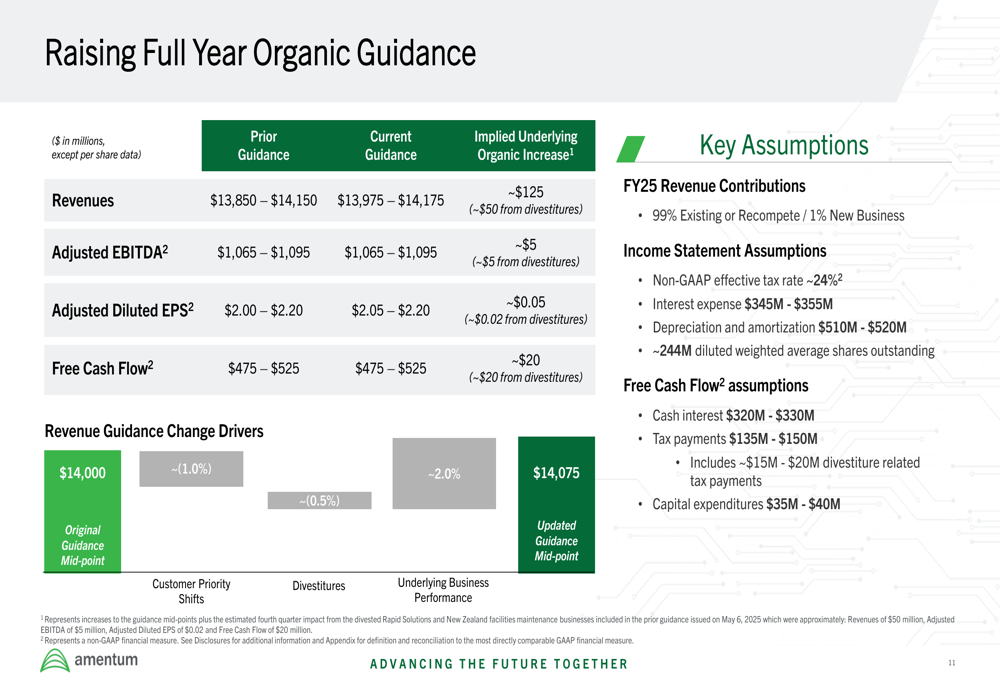

Raised Guidance and Outlook

Based on strong year-to-date performance, Amentum raised its full-year FY25 organic guidance. The company now expects:

- Revenues of $13,975-$14,175 million (increased by approximately $125 million)

- Adjusted EBITDA of $1,065-$1,095 million (increased by approximately $5 million)

- Adjusted Diluted EPS of $2.05-$2.20 (increased by approximately $0.05)

- Free Cash Flow of $475-$525 million (increased by approximately $20 million)

The guidance update accounts for recent divestitures while reflecting confidence in underlying business performance. The company noted that 99% of FY25 revenue is expected to come from existing contracts or recompetes, with only 1% dependent on new business.

The following slide details the updated guidance and key assumptions:

Looking ahead, Amentum emphasized its alignment with enduring global trends and well-funded priority areas, including missile defense, unmanned systems, INDOPACOM, space, digital transformation, and energy infrastructure. The company’s strategy focuses on these high-growth areas while continuing to streamline its portfolio and reduce debt.

Despite the positive quarterly results and raised guidance, the premarket trading decline suggests investors may be focusing on other factors or taking a cautious approach to the company’s outlook. Nevertheless, Amentum’s Q3 FY25 presentation portrays a company executing well on its strategic initiatives while positioning itself for long-term growth in key markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.