Aspire Biopharma faces potential Nasdaq delisting after compliance shortfall

Introduction & Market Context

American Airlines Group (NASDAQ:AAL) presented its second-quarter 2025 financial results on July 24, revealing record quarterly revenue despite facing pressure on profitability. The carrier’s shares rose 3.79% to $11.74 following the announcement, though they dipped 1.11% in premarket trading the following day, suggesting mixed investor sentiment about the results.

The airline achieved $14.4 billion in revenue, representing a modest 0.4% year-over-year increase, while reporting adjusted earnings per share of $0.95. This performance comes amid ongoing challenges in the domestic market, though the company highlighted its progress in debt reduction and strong cash flow generation.

Quarterly Performance Highlights

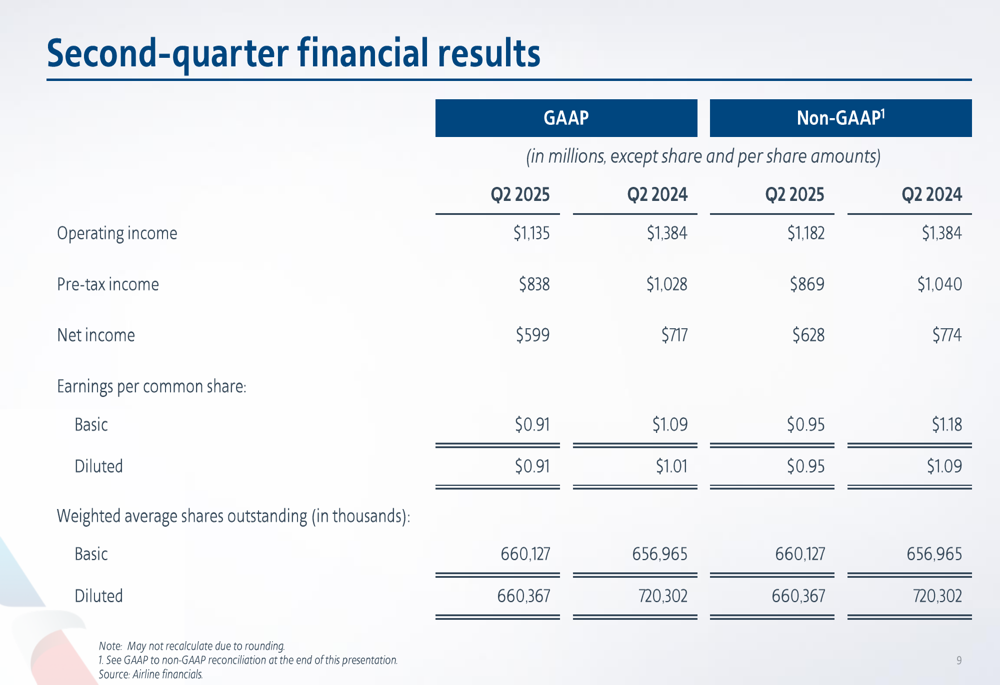

American Airlines reported record quarterly revenue of $14.4 billion for Q2 2025, though its profitability metrics showed year-over-year declines. GAAP operating income fell to $1,135 million from $1,384 million in Q2 2024, while GAAP net income decreased to $599 million from $717 million in the same period last year.

The company posted GAAP earnings per diluted share of $0.91 and non-GAAP earnings per diluted share of $0.95. American generated $3.4 billion in operating cash flow and $2.5 billion in free cash flow during the quarter, ending with $12 billion of total available liquidity.

As shown in the detailed financial breakdown below, the airline’s adjusted EBITDAR margin reached 14.2%, though this represents a 1.5-point reduction from the previous year:

Strategic Initiatives

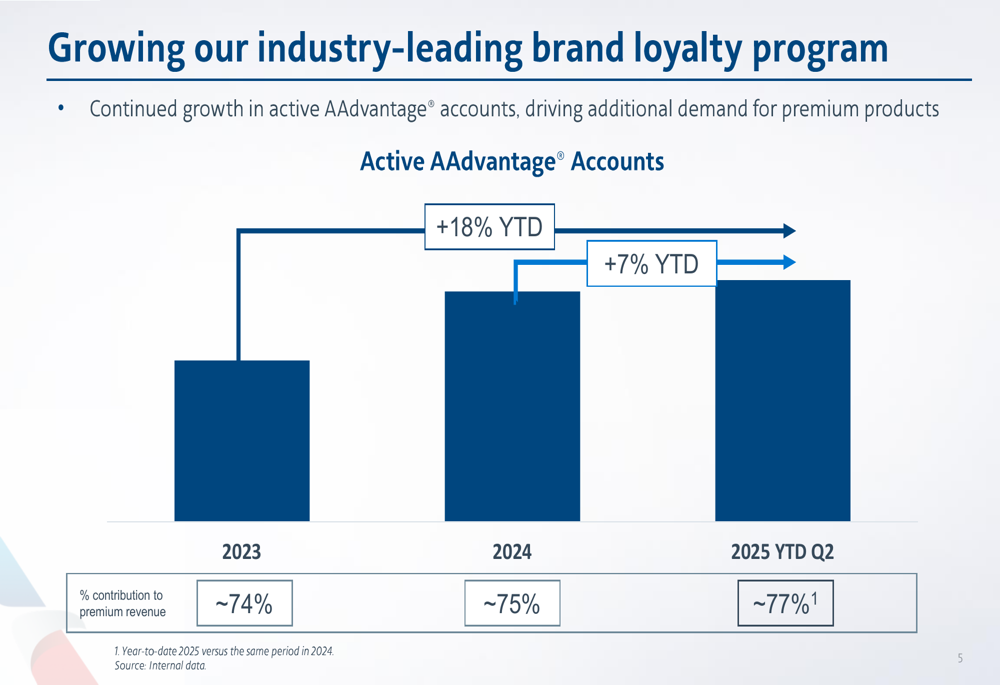

American Airlines is focusing on enhancing its premium offerings and loyalty program to drive revenue growth. The company’s AAdvantage program continues to show strong performance, with active members contributing 77% to premium revenue in Q2 2025, up from 75% in 2024 and 74% in 2023. This represents an 18% year-to-date growth in the program’s contribution to premium revenue.

The following chart illustrates the growing importance of the loyalty program to American’s premium revenue strategy:

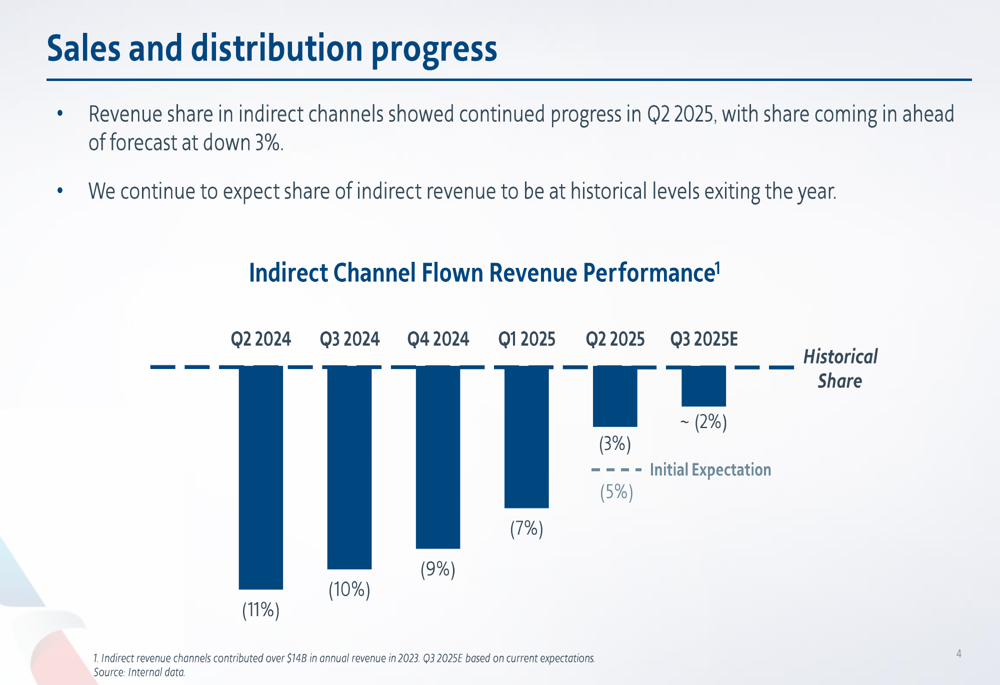

The airline is also seeing improvement in its indirect channel revenue performance, with Q2 2025 showing a revenue share decline of only 3% compared to an initially expected 5% decline. Management anticipates continued improvement, with indirect channel revenue expected to return to normal historical levels by the end of the year.

This recovery trajectory in indirect channel revenue is clearly demonstrated in the following chart:

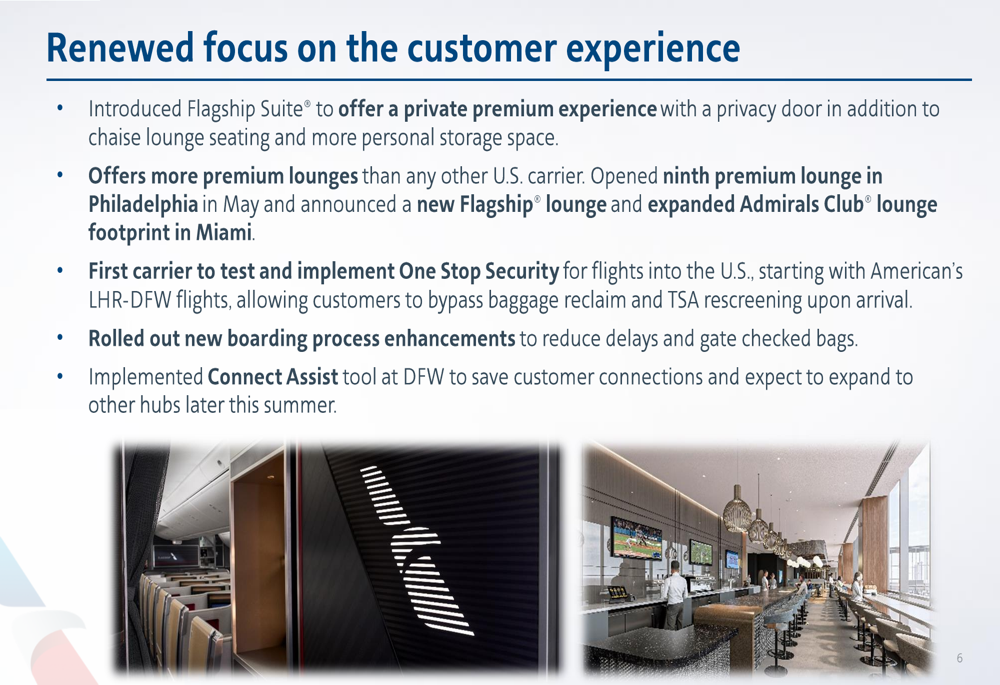

American is making significant investments in customer experience enhancements, introducing the Flagship Suite to offer a private premium experience and maintaining more premium lounges than any other U.S. carrier. Additional initiatives include the implementation of One Stop Security for international flights, boarding process enhancements to reduce delays, and the Connect Assist tool at DFW to improve customer connections.

The following image showcases some of these premium customer experience initiatives:

Detailed Financial Analysis

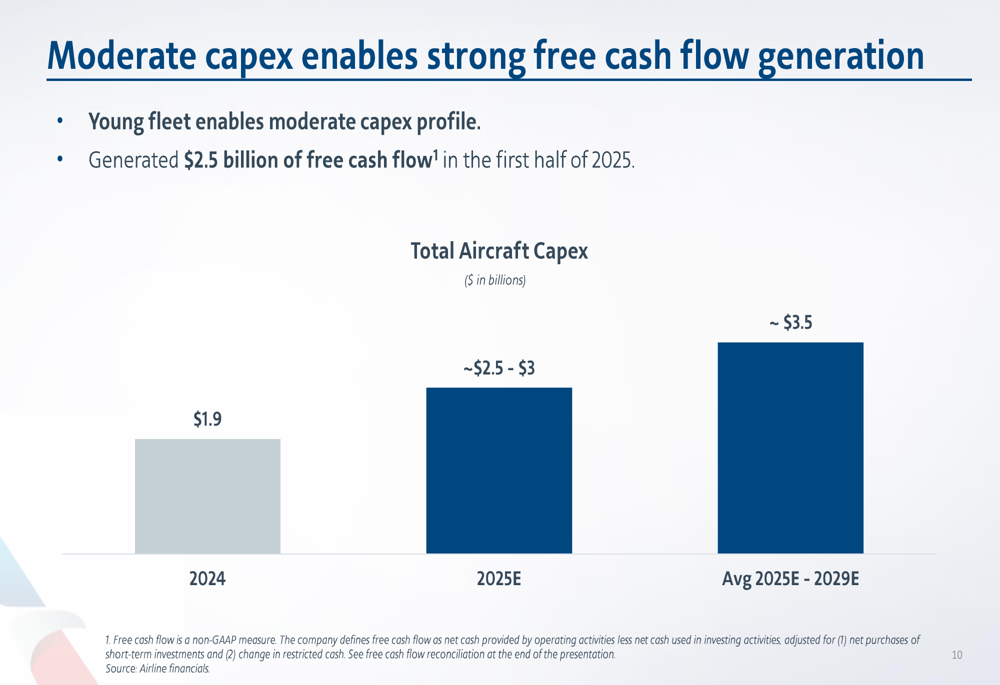

American Airlines continues to benefit from its relatively young fleet, which enables a moderate capital expenditure profile and strong free cash flow generation. The company generated $2.5 billion in free cash flow during the first half of 2025, with aircraft capital expenditures projected to be between $2.5 billion and $3 billion for the full year 2025.

The following chart illustrates American’s capital expenditure outlook through 2029:

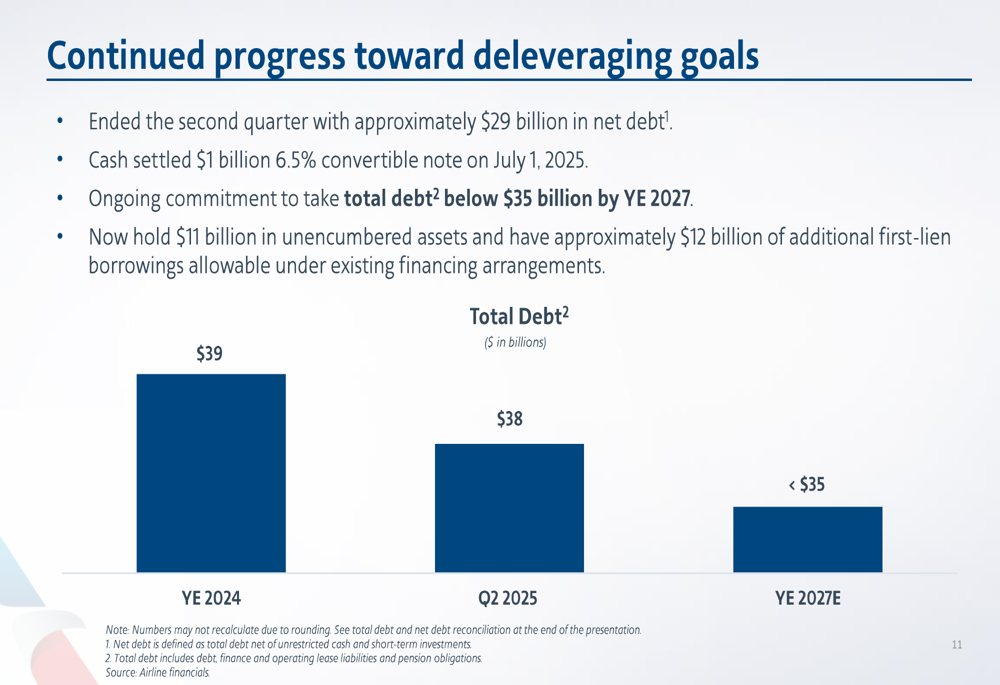

Debt reduction remains a key priority for the airline. American ended Q2 2025 with approximately $29 billion in net debt, its lowest level since Q3 2015. The company recently cash settled a $1 billion 6.5% convertible note on July 1, 2025, and maintains its commitment to reduce total debt below $35 billion by the end of 2027. Additionally, American holds $11 billion in unencumbered assets, providing financial flexibility.

The progress toward the company’s deleveraging goals is shown in the following chart:

Forward-Looking Statements

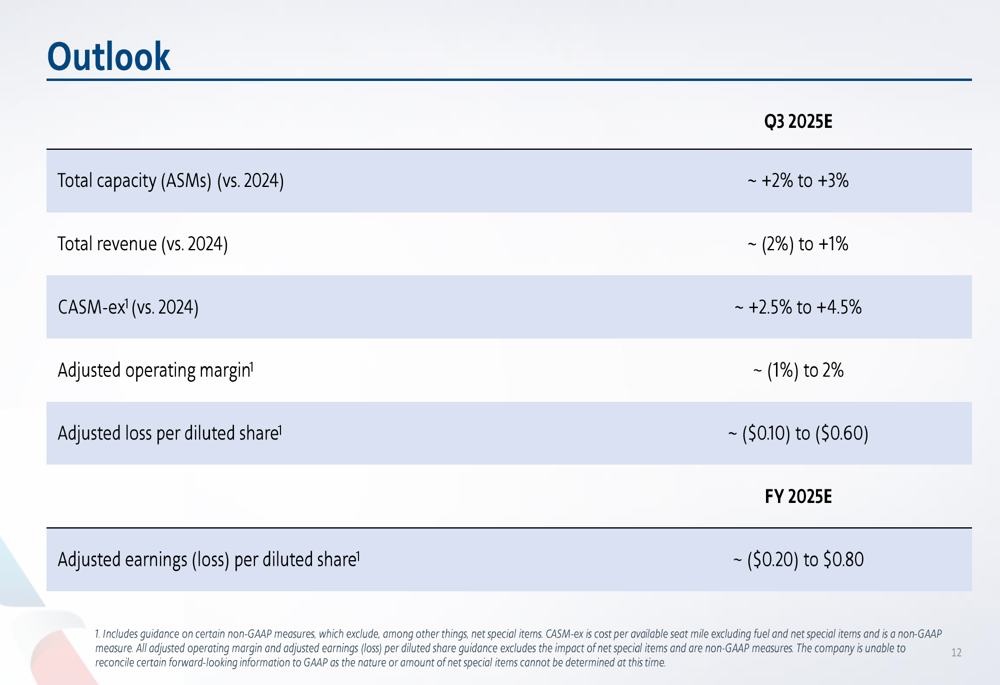

American Airlines provided a cautious outlook for the third quarter and full year 2025. For Q3 2025, the company expects total capacity to increase by 2% to 3% year-over-year, while total revenue is projected to range from a 2% decline to a 1% increase compared to Q3 2024. Cost per available seat mile, excluding fuel and special items (CASM-ex), is expected to increase by 2.5% to 4.5%, with adjusted operating margin between -1% and 2%.

For the full year 2025, American forecasts adjusted earnings per diluted share to be between a loss of $0.20 and a profit of $0.80, reflecting continued uncertainty in the domestic market.

The complete outlook for Q3 and full-year 2025 is presented below:

During the earnings call, CEO Robert Isom expressed confidence in the company’s long-term initiatives, while CFO Devon May noted that the top end of the guidance range could be achievable if domestic market demand continues to strengthen. Management believes there is positive unit revenue potential in the fourth quarter, driven by expected recovery in domestic demand and strategic investments in customer experience and technology.

Despite near-term challenges, American Airlines’ record revenue achievement, strong cash flow generation, and continued progress on debt reduction demonstrate the company’s resilience in a competitive industry environment. Investors will be closely watching whether the airline’s premium strategy and loyalty program growth can offset domestic market pressures in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.