Nvidia and TSMC to unveil first domestic wafer for Blackwell chips, Axios reports

Introduction & Market Context

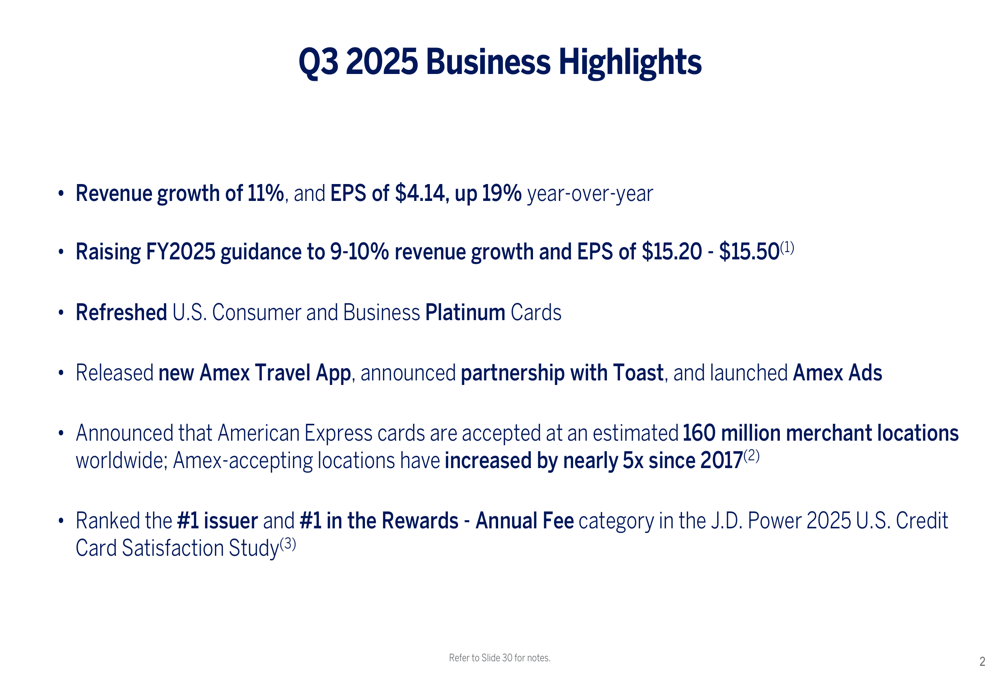

American Express (NYSE:AXP) delivered impressive third-quarter results for 2025, with earnings per share reaching $4.14, exceeding analyst expectations of $3.99 and representing a 19% year-over-year increase. Revenue grew 11% to $18.43 billion, also surpassing forecasts of $18.05 billion. Following the strong earnings report, American Express shares rose 4.17% in regular trading after initially jumping 3.06% in pre-market activity.

The company’s performance was driven by continued success in its premium card strategy, strong transaction growth, and balanced expansion across consumer, commercial, and international segments. American Express also raised its full-year 2025 guidance, signaling confidence in sustained momentum.

As shown in the following slide highlighting key business results, American Express demonstrated strength across multiple metrics:

Quarterly Performance Highlights

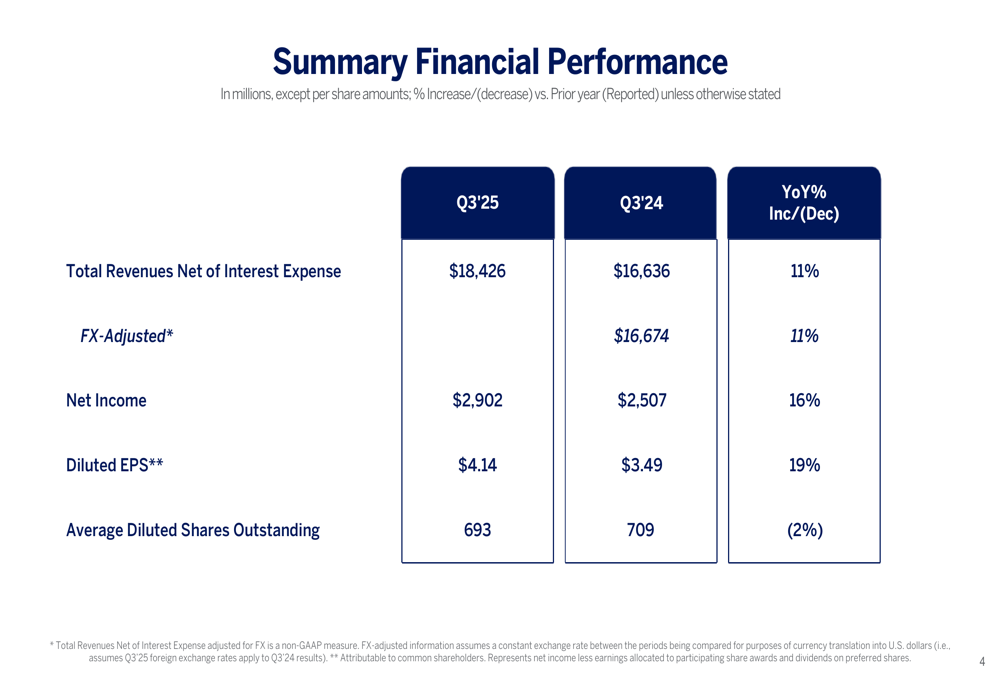

American Express reported robust financial performance for the third quarter of 2025, with total revenues net of interest expense reaching $18.43 billion, an 11% increase compared to the same period last year. Net income grew 16% year-over-year to $2.9 billion, while diluted earnings per share increased 19% to $4.14, benefiting from both operational growth and a 2% reduction in outstanding shares.

The detailed financial summary shows consistent improvement across key metrics:

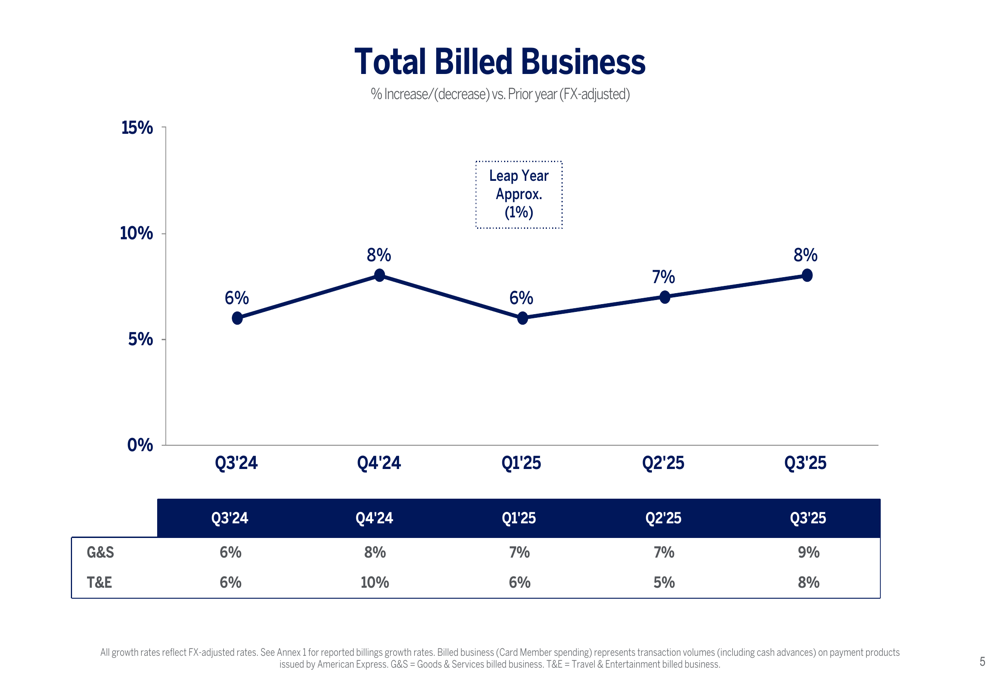

Billed business, a key indicator of customer spending, grew 8% year-over-year on an FX-adjusted basis. Growth was balanced across goods and services (9%) and travel and entertainment (8%), suggesting healthy consumer and business spending patterns despite economic uncertainties.

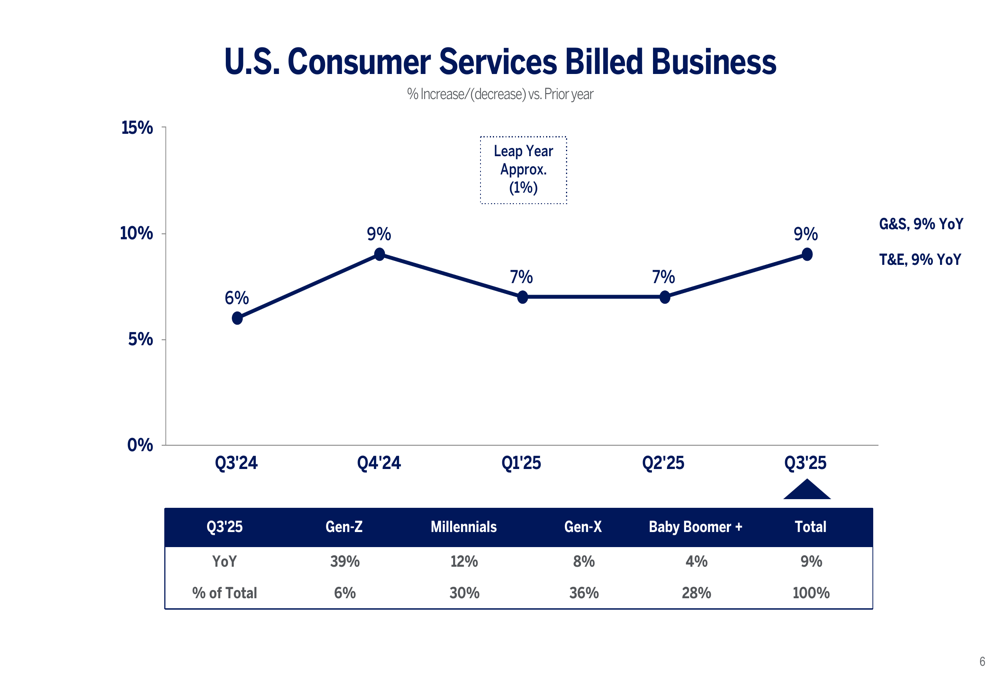

American Express’s growth was distributed across all major segments. U.S. Consumer Services billed business increased 9% year-over-year, with particularly strong performance among younger demographics. Gen-Z cardholders demonstrated exceptional engagement with 39% year-over-year growth, though they currently represent only 6% of total U.S. Consumer billed business.

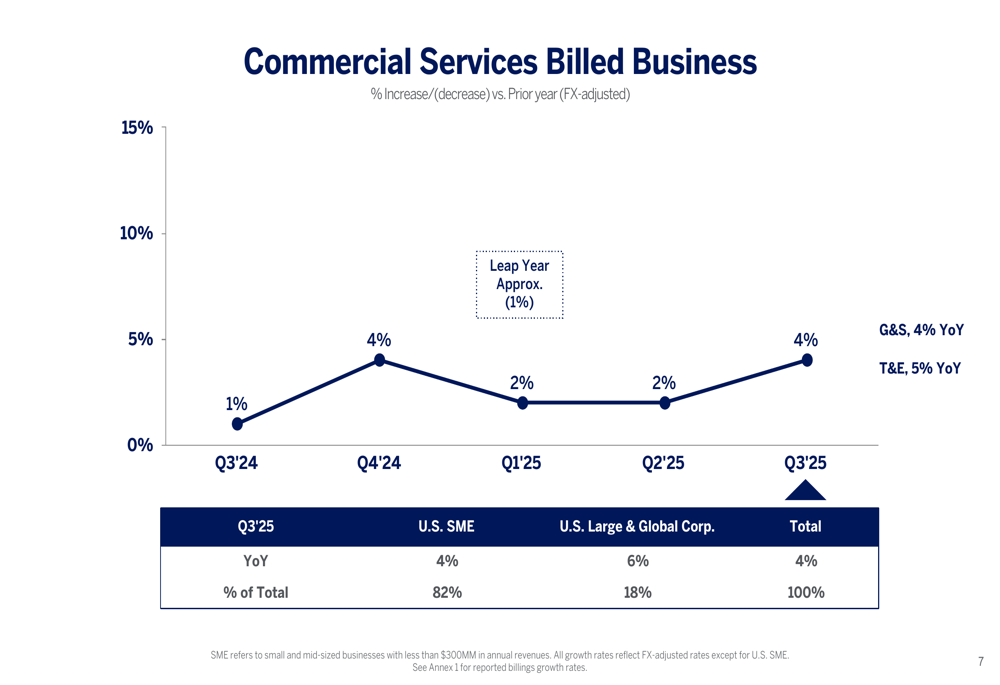

Commercial Services billed business grew 4% year-over-year, with U.S. Small and Medium-sized Enterprises (SMEs) contributing 82% of the segment’s volume. Meanwhile, International Card Services showed the strongest growth at 13% year-over-year, with consumer cards outperforming business cards.

Strategic Initiatives

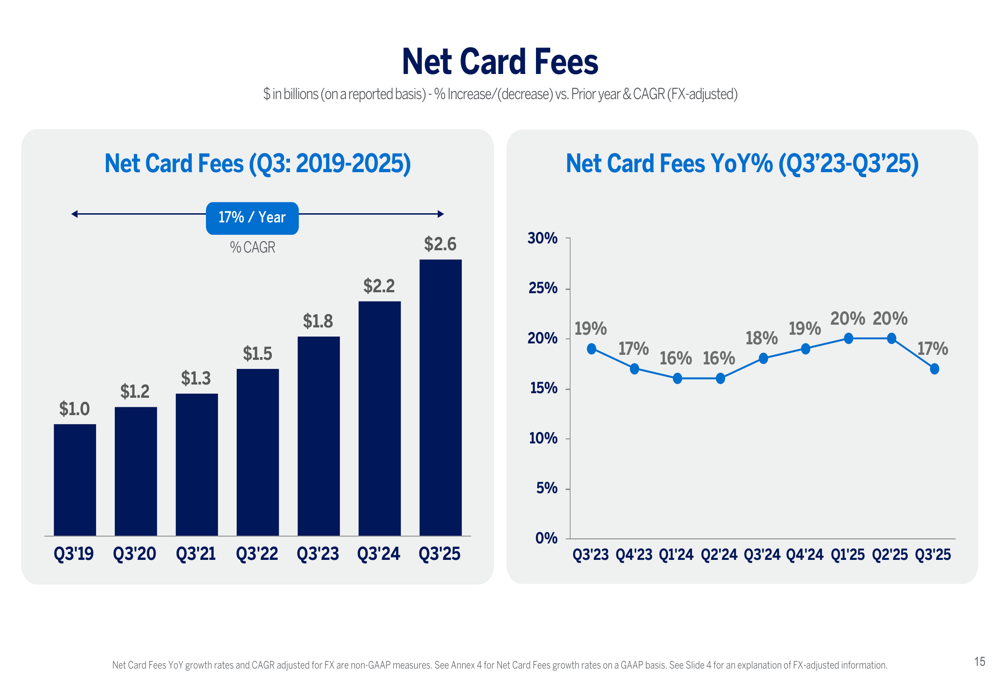

A cornerstone of American Express’s strategy has been its focus on premium card products, which continues to deliver strong results. Net card fees increased 18% year-over-year to $2.55 billion in Q3 2025, maintaining a 17% compound annual growth rate (CAGR) since 2019. This growth underscores the success of the company’s value proposition for premium cardholders.

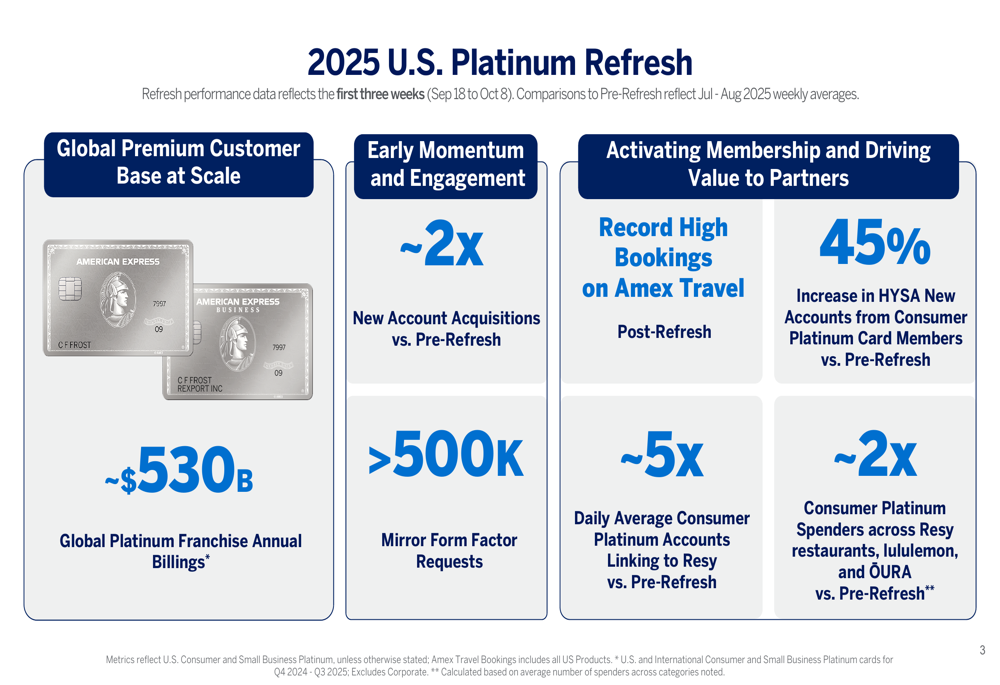

The recently refreshed U.S. Platinum Card is showing early positive momentum, with new account acquisitions doubling compared to pre-refresh levels. The company reported over 500,000 requests for the new mirror form factor card, indicating strong consumer interest in the refreshed product.

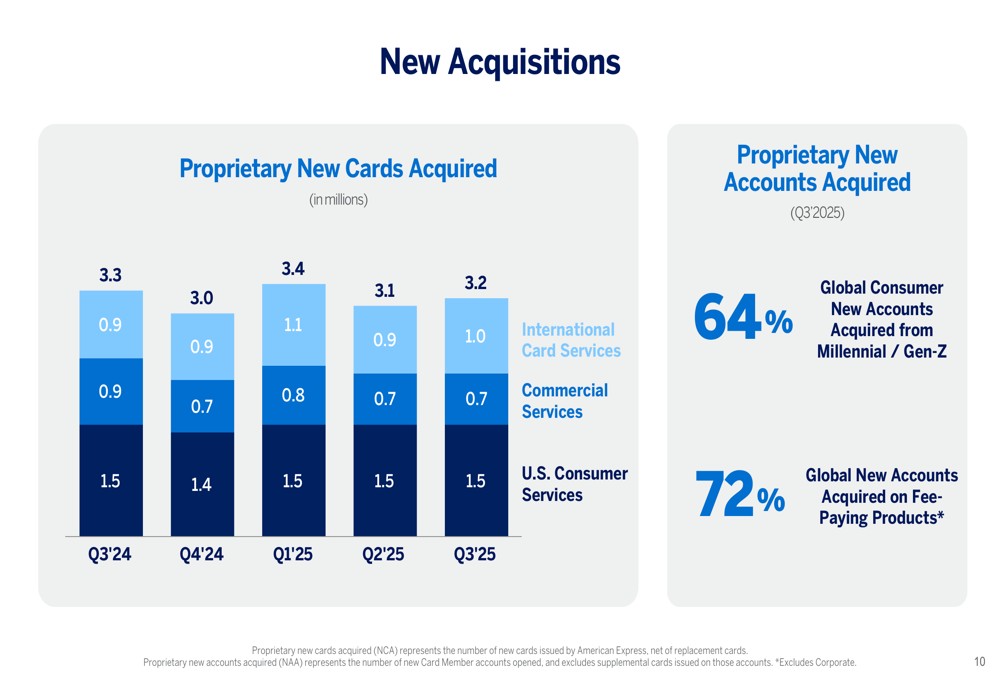

American Express continues to expand its customer base while maintaining a focus on premium products and younger demographics. The company acquired 3.2 million new proprietary cards in Q3 2025, with 64% of global consumer new accounts coming from Millennials and Gen-Z cardholders. Additionally, 72% of new accounts were on fee-paying products, supporting the company’s premium strategy.

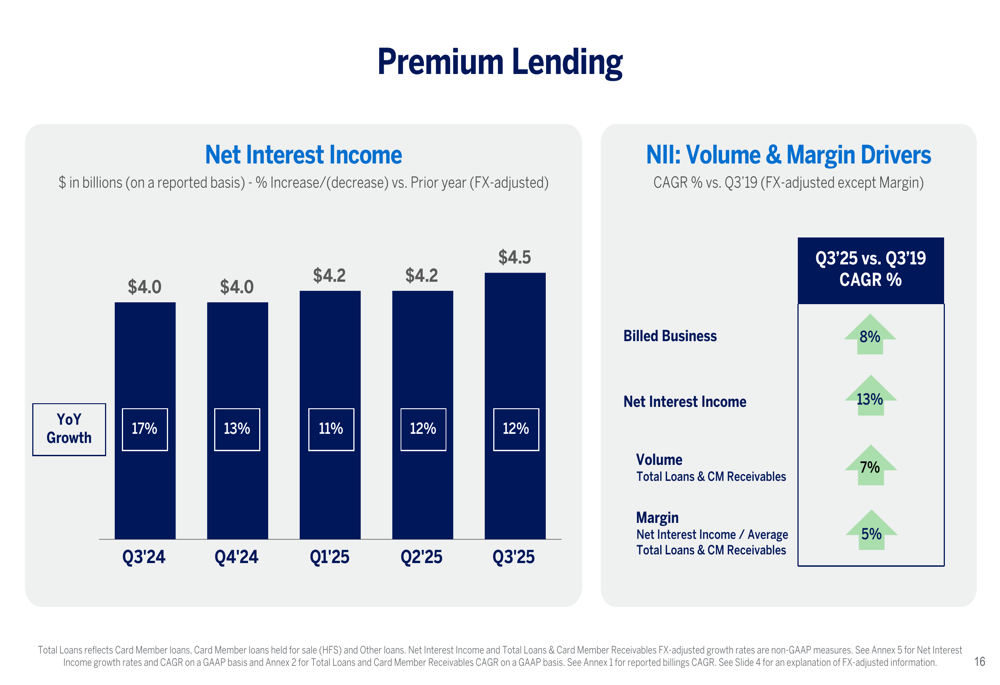

The company’s lending business also showed healthy growth, with net interest income increasing 12% year-over-year to $4.49 billion. This growth was driven by both volume expansion (7%) and margin improvement (5%), reflecting American Express’s ability to grow its lending business while maintaining disciplined risk management.

Risk Management & Credit Performance

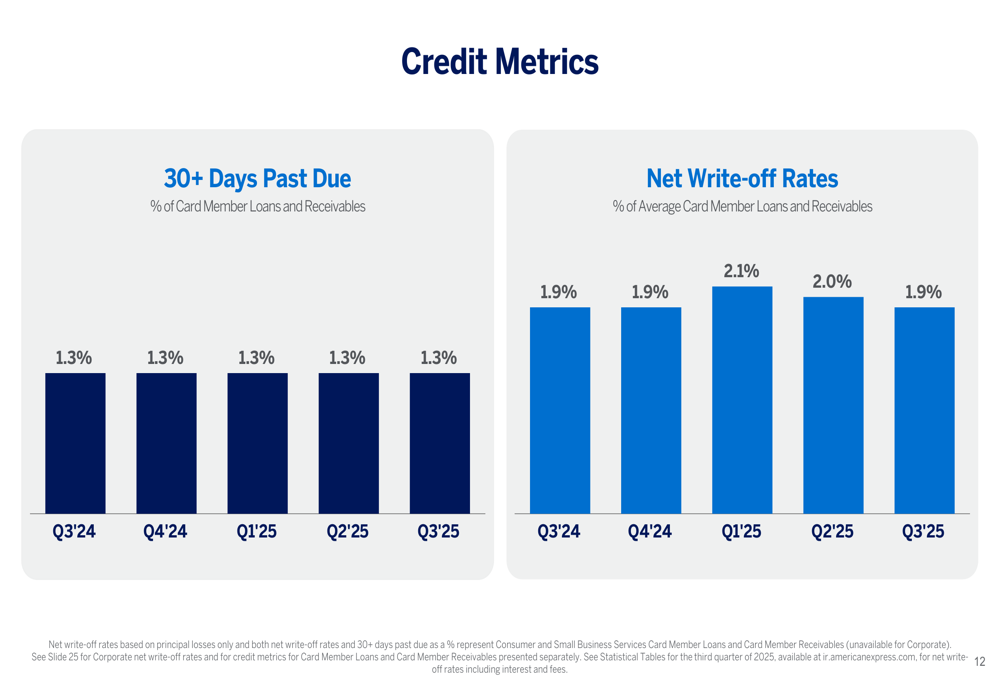

Despite the growth in lending, American Express maintained stable credit metrics, with 30+ days past due accounts remaining at 1.3% of total loans and receivables, unchanged from previous quarters. Net write-off rates were 1.9%, showing slight improvement from earlier in the year.

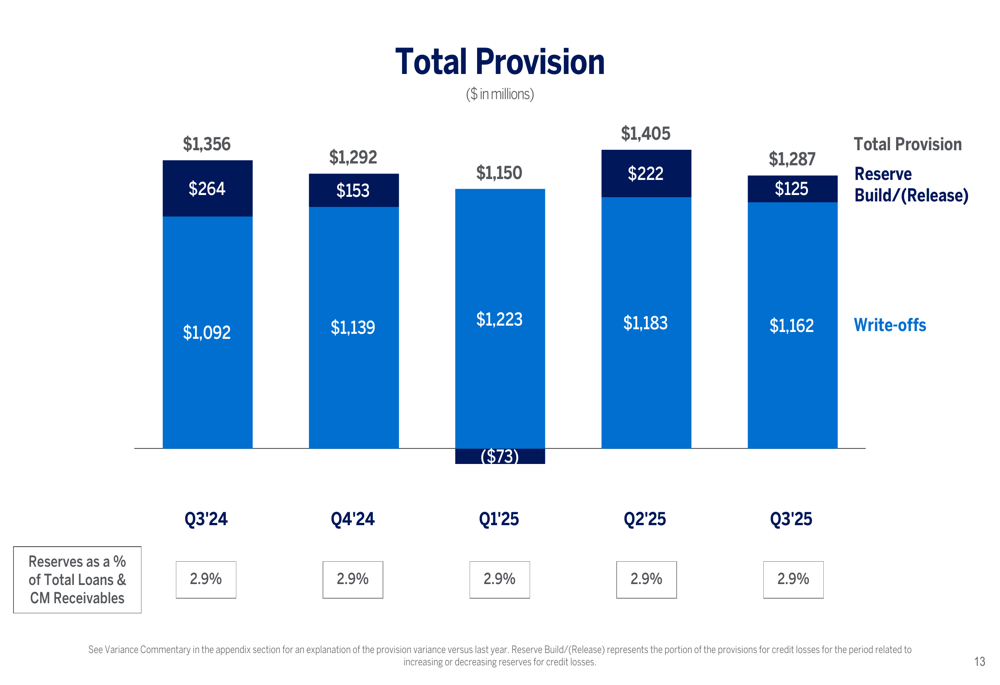

Total provision for credit losses was $1.29 billion in Q3 2025, a decrease of 5% compared to the same period last year. This included $1.16 billion in write-offs and a $125 million reserve build, reflecting the company’s prudent approach to credit risk management in the current economic environment.

Capital Management & Shareholder Returns

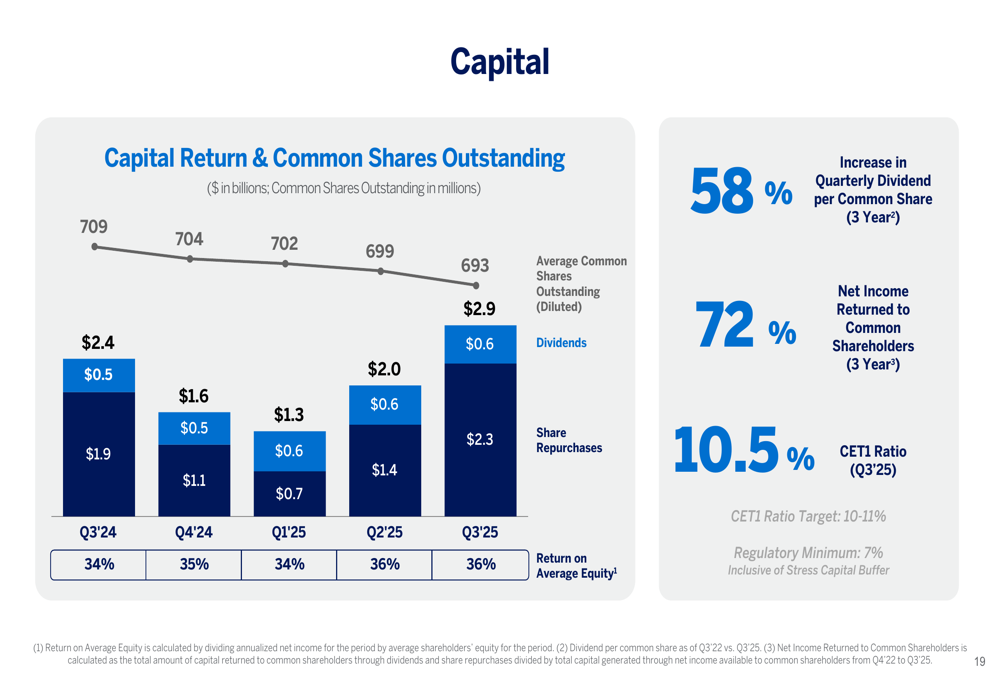

American Express maintained a strong capital position with a CET1 ratio of 10.5% in Q3 2025. The company continued its share repurchase program, buying back $2.3 billion worth of shares during the quarter and reducing common shares outstanding to 693 million. Combined with $0.6 billion in dividends, American Express returned significant capital to shareholders while maintaining financial flexibility.

Forward-Looking Statements

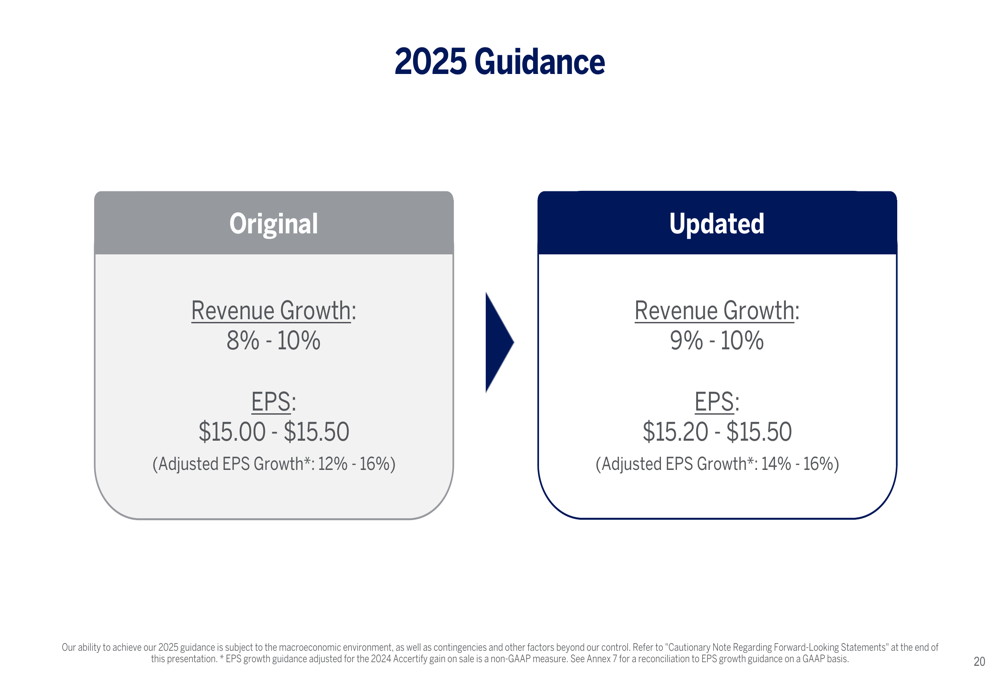

Based on the strong year-to-date performance, American Express raised its full-year 2025 guidance. The company now expects revenue growth of 9-10%, narrowed from the previous range of 8-10%. Earnings per share guidance was also raised to $15.20-$15.50, compared to the previous range of $15.00-$15.50, representing adjusted EPS growth of 14-16%.

"We are fortunate to have a global premium customer base that is unmatched in the industry," stated CEO Steve Squeri in the earnings call, highlighting the company’s strong market position. CFO Kristina Fink added, "We feel good about our momentum year to date, and we are very pleased with the initial demand and engagement following the Platinum refresh."

Conclusion

American Express’s Q3 2025 results demonstrate the continued success of its premium card strategy and ability to attract younger demographics while maintaining strong credit performance. The company’s raised guidance reflects confidence in its business model and growth trajectory despite potential macroeconomic challenges.

With its expanding merchant network, now reaching an estimated 160 million locations worldwide, and continued innovation in digital capabilities, American Express appears well-positioned to sustain its momentum through the remainder of 2025 and beyond. The company’s ability to grow revenue, expand margins, and return capital to shareholders while investing in future growth initiatives presents a compelling narrative for investors.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.