How are energy investors positioned?

Introduction & Market Context

American Tower Corporation (NYSE:AMT) presented its second quarter 2025 earnings results on July 29, revealing a mixed performance characterized by modest revenue growth but a significant decline in net income. The real estate investment trust, which specializes in wireless communications infrastructure, saw its stock decline 2.46% to $224.21 in the previous session, with premarket trading showing a further 0.28% dip to $223.59.

The company’s presentation highlighted solid global demand driving mid-single-digit tenant billings growth, particularly in international markets, while simultaneously raising its full-year 2025 outlook across key financial metrics. However, these positive developments were overshadowed by a 59.3% year-over-year decline in net income attributable to common stockholders.

Quarterly Performance Highlights

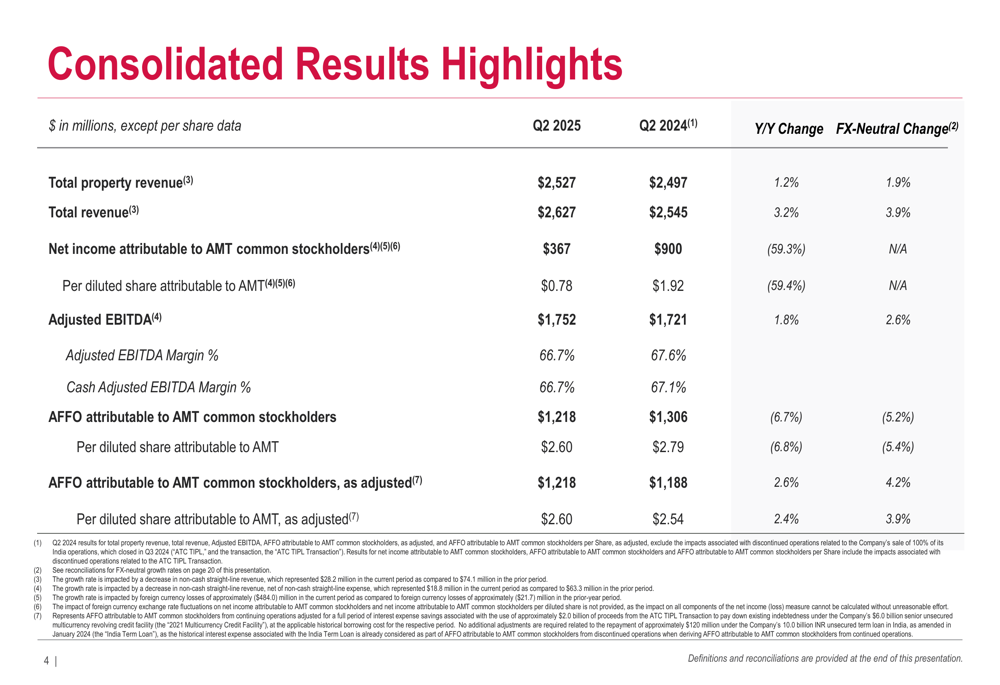

American Tower reported total revenue of $2.63 billion for Q2 2025, representing a 3.2% increase year-over-year (3.9% on an FX-neutral basis). Property revenue, which constitutes the bulk of the company’s income, grew at a more modest 1.2% to $2.53 billion, or 1.9% when adjusted for currency effects.

As shown in the following consolidated results summary:

The company’s net income attributable to common stockholders plummeted 59.3% year-over-year to $367 million. This significant decline follows the Q1 2025 earnings miss, where EPS fell short of expectations at $1.04 versus a forecast of $1.60.

Despite the profit decline, Adjusted EBITDA showed improvement, rising 1.8% to $1.75 billion with a cash margin of 66.7%, slightly below the 67.1% reported in Q2 2024. Adjusted Funds From Operations (AFFO) attributable to common stockholders declined 6.7% year-over-year to $1.22 billion, though the company noted this was up 2.6% on an adjusted basis that accounts for prior year India contributions, which included over $65 million in revenue reserve reversals.

Regional Performance Analysis

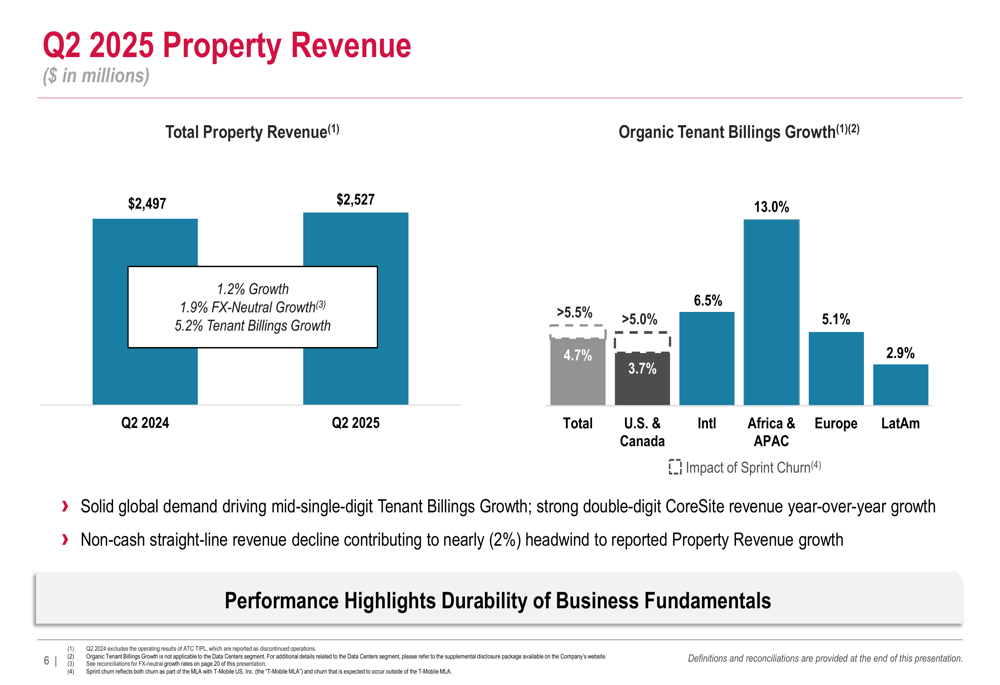

American Tower’s performance showed significant regional disparities, with international markets outperforming the domestic business. Organic tenant billings growth, a key industry metric that reflects recurring revenue from existing sites, reached 4.7% overall but varied substantially by region.

The following chart illustrates these regional differences:

Africa & Asia-Pacific emerged as the standout performer with 13.0% organic tenant billings growth, followed by Europe at 5.1%. The U.S. & Canada region, which represents American Tower’s largest market, grew at a more modest 3.7%. The company attributed the slower U.S. growth to "commencement timing associated with a customer," suggesting deployment delays from one of its major telecommunications clients.

Latin America showed the weakest performance with 2.9% growth, though this still represents positive momentum in a challenging market environment. The company highlighted that solid global demand is driving mid-single-digit tenant billings growth overall, while its CoreSite data center business achieved strong double-digit revenue growth year-over-year.

Revised 2025 Outlook

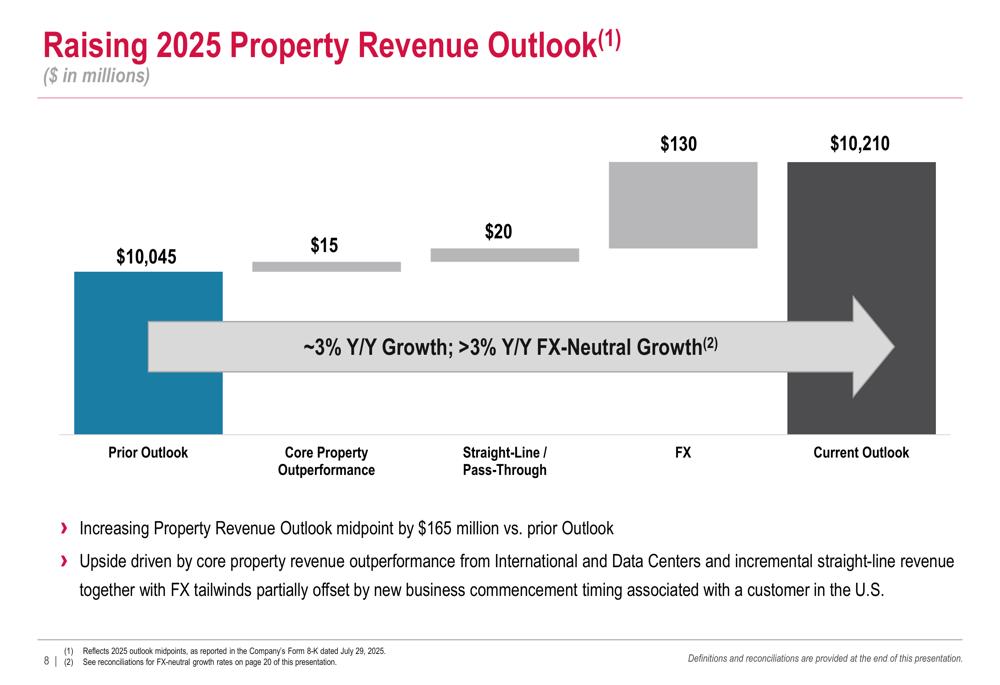

A significant portion of the presentation focused on American Tower’s improved financial outlook for 2025. The company raised its property revenue guidance from $10.05 billion to $10.21 billion, citing core property outperformance, increased straight-line revenue, and favorable foreign exchange movements.

The following chart details these upward revisions:

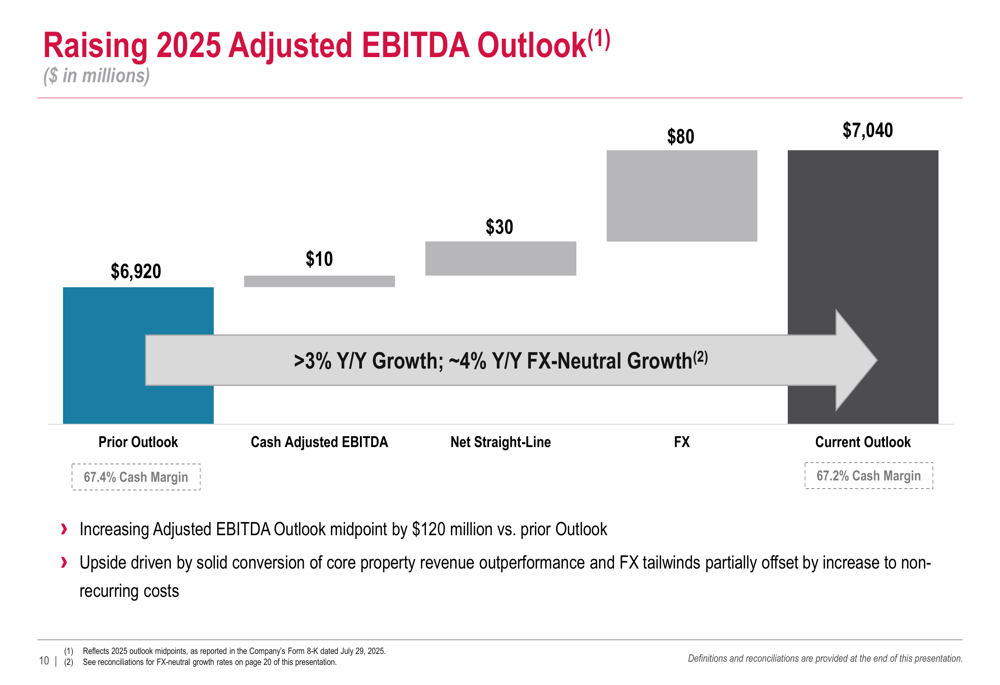

Similarly, the company increased its Adjusted EBITDA outlook from $6.92 billion to $7.04 billion, representing over 3% year-over-year growth, or approximately 4% on an FX-neutral basis:

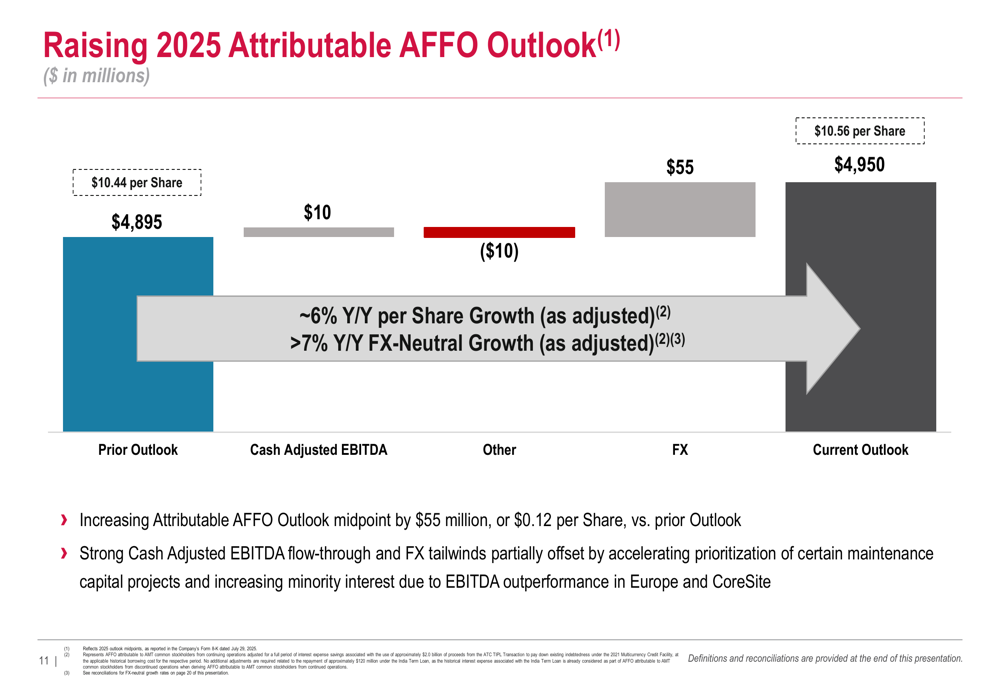

American Tower also raised its Attributable AFFO outlook from $4.90 billion ($10.44 per share) to $4.95 billion ($10.56 per share), projecting approximately 6% year-over-year per share growth on an adjusted basis:

The company noted that while core property revenue outperformance and FX tailwinds are driving these upward revisions, they are partially offset by accelerated maintenance capital projects and increased minority interest expenses due to EBITDA outperformance in Europe and CoreSite.

Capital Allocation & Strategic Initiatives

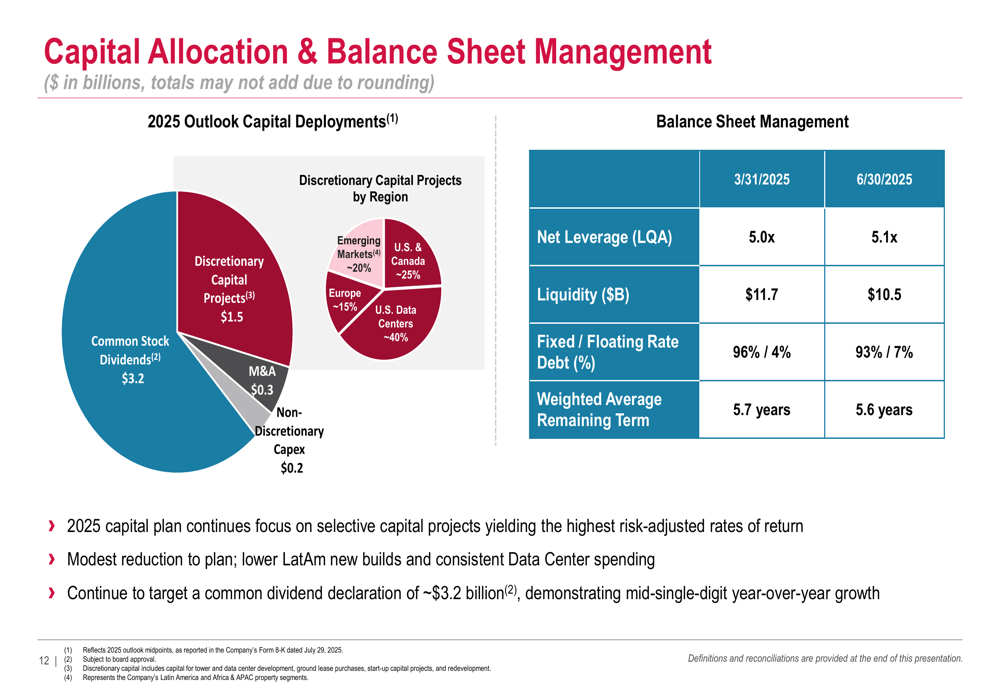

American Tower outlined its capital allocation strategy for 2025, with a continued focus on shareholder returns and selective growth investments. The company plans to distribute approximately $3.2 billion in common stock dividends, representing mid-single-digit year-over-year growth.

The presentation detailed the following capital deployment plan:

Discretionary capital projects account for $1.5 billion of planned expenditures, though the company mentioned a "modest reduction to plan" with lower new builds in Latin America, indicating a more cautious approach in that region. Mergers and acquisitions are allocated a relatively modest $0.3 billion, suggesting limited appetite for major expansion through acquisitions in the current environment.

The balance sheet remains relatively stable with net leverage at 5.1x as of June 30, 2025, slightly up from 5.0x at the end of the previous quarter. Liquidity decreased from $11.7 billion to $10.5 billion during the same period, while the company maintains a conservative debt profile with 93% fixed-rate debt.

Forward-Looking Statements

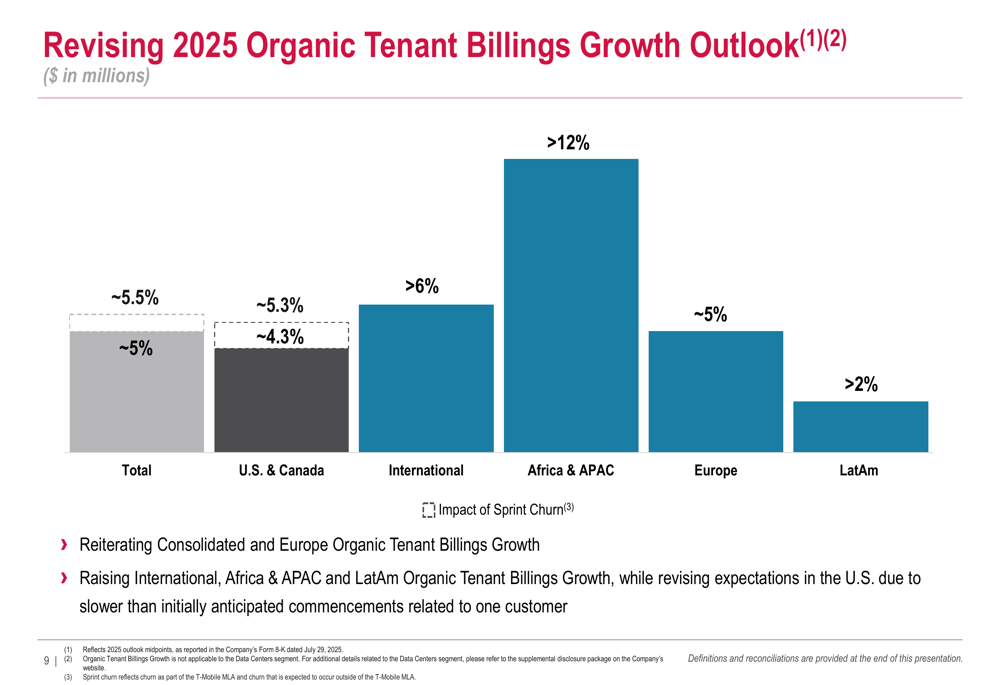

Looking ahead, American Tower reiterated its confidence in long-term growth prospects while acknowledging near-term challenges. The company revised its regional organic tenant billings growth outlook, maintaining its overall projection of approximately 5% growth but adjusting expectations across markets:

The company is raising growth expectations for international markets, particularly in Africa & APAC where it now projects over 12% growth. However, it has revised U.S. expectations downward due to "slower than initially anticipated commencements related to one customer."

In summary, American Tower emphasized its positioning for "durable, long-term growth" through core property outperformance, globalization, efficiency initiatives, and selective capital deployment. The company’s focus on its CoreSite data center business appears to be yielding positive results, providing diversification beyond traditional tower assets.

While the significant net income decline raises concerns, the company’s ability to raise guidance across key metrics suggests confidence in its underlying business fundamentals despite macroeconomic challenges and customer-specific deployment delays in the U.S. market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.