Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

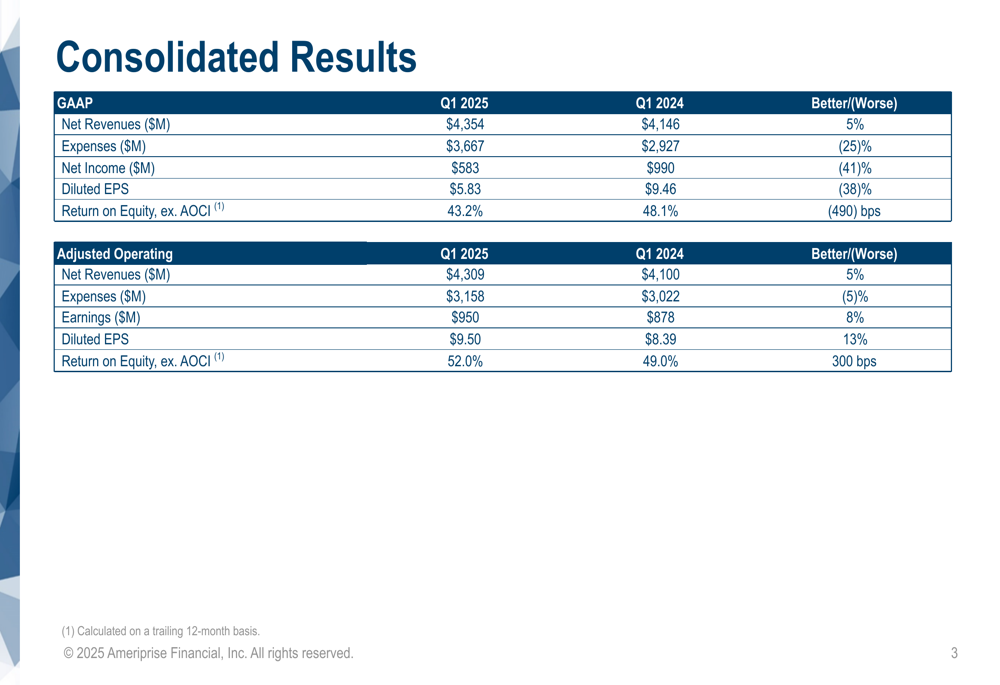

Ameriprise Financial (NYSE:AMP) presented its first quarter 2025 results on April 24, showing solid growth across its diversified business segments. The company reported adjusted operating earnings per diluted share of $9.50, representing a 13% increase compared to $8.39 in the first quarter of 2024, despite challenges including interest rate reductions since September.

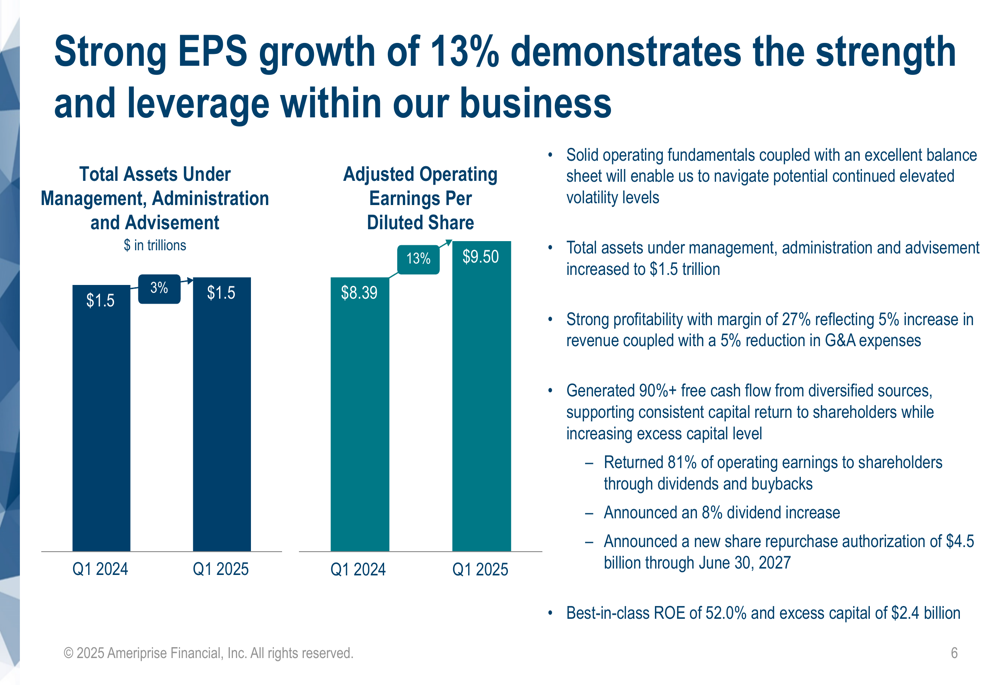

The financial services provider maintained strong fundamentals with total assets under management, administration, and advisement reaching $1.5 trillion, a 3% increase from the prior year. The company’s stock closed at $471.85 on April 23, 2025, and showed modest premarket activity with a 0.55% increase to $474.46.

Quarterly Performance Highlights

Ameriprise delivered strong profitability with a 27% margin, reflecting a 5% increase in revenue coupled with a 5% reduction in G&A expenses. The company’s adjusted operating total net revenue increased to $4.31 billion in Q1 2025, up 5% from $4.10 billion in Q1 2024.

As shown in the following consolidated results chart, Ameriprise’s adjusted operating earnings grew 8% to $950 million, while adjusted operating return on equity excluding AOCI improved to 52.0%, up 300 basis points from 49.0% in the prior year:

The company’s strong EPS growth of 13% demonstrates the strength and leverage within its business model. This performance was achieved despite fewer fee and trading days in the quarter, and the impact of federal funds rate reductions since September 2024.

The following chart illustrates the growth in total assets and adjusted operating earnings per diluted share:

Segment Analysis

Wealth Management

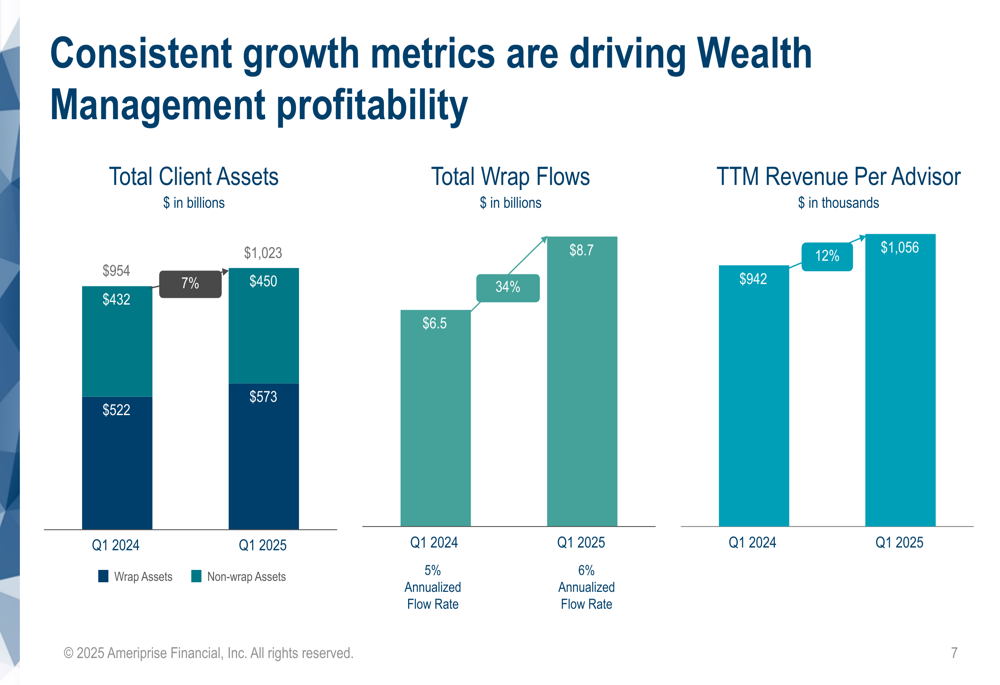

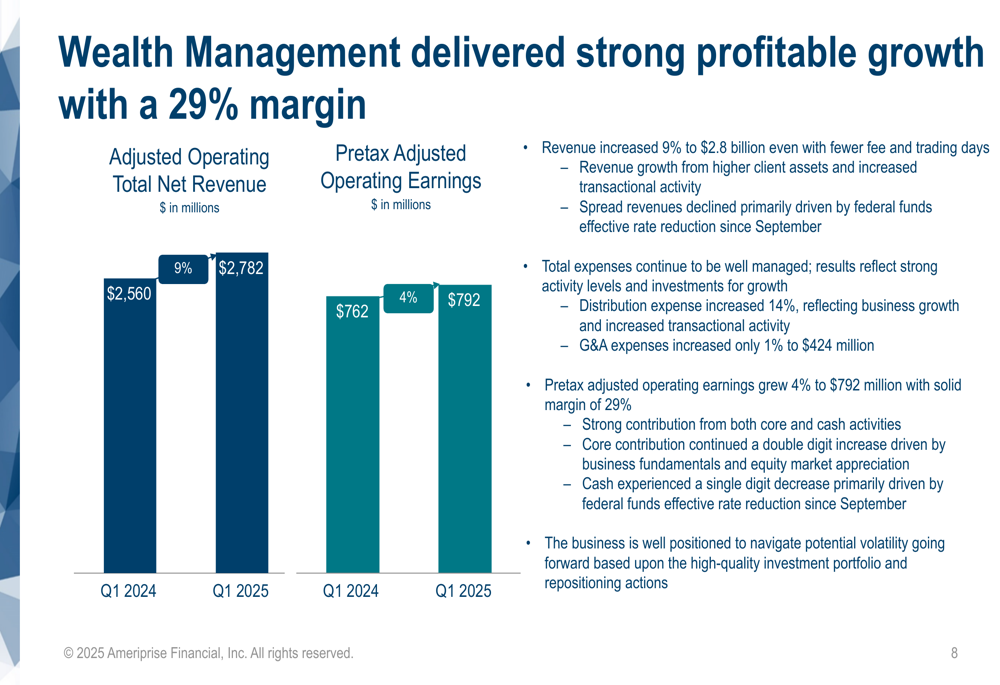

Wealth Management continued to be Ameriprise’s strongest performing segment, with total client assets growing 7% to $1.02 trillion. The segment’s adjusted operating total net revenue increased 9% to $2.78 billion, while pretax adjusted operating earnings grew 4% to $792 million, maintaining a solid margin of 29%.

The following chart shows the consistent growth in Wealth Management metrics:

Total (EPA:TTEF) wrap flows increased 34% to $8.7 billion, with an annualized flow rate of 6%, up from 5% in Q1 2024. Revenue per advisor on a trailing twelve-month basis grew 12% to $1.06 million.

The segment’s revenue growth was driven by higher client assets and increased transactional activity, despite spread revenues declining primarily due to federal funds effective rate reduction since September:

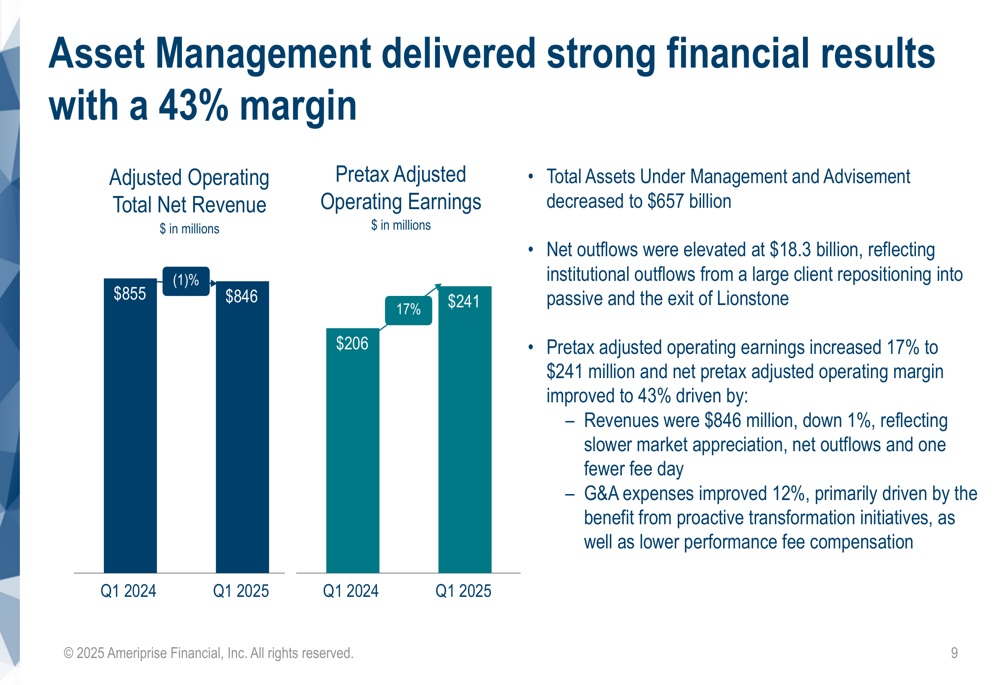

Asset Management

Asset Management showed significant margin expansion despite slight revenue challenges. While adjusted operating total net revenue decreased 1% to $846 million, pretax adjusted operating earnings increased 17% to $241 million, with net pretax adjusted operating margin improving to 43%.

Total Assets Under Management and Advisement decreased to $657 billion, with net outflows of $18.3 billion, reflecting institutional outflows from a large client repositioning into passive investments and the exit of Lionstone. G&A expenses improved 12%, primarily driven by benefits from proactive transformation initiatives and lower performance fee compensation:

Retirement & Protection Solutions

Retirement & Protection Solutions delivered consistent earnings and free cash flow generation. Pretax adjusted operating earnings increased 8% to $215 million, reflecting the benefit of stronger interest earnings and higher equity markets.

Sales remained strong at $1.2 billion, fueled by continued demand for structured variable annuities and variable universal life products. The segment maintained an estimated RBC ratio of 615% and hedge effectiveness of 99%, highlighting its risk management capabilities.

Capital Return and Balance Sheet Strength

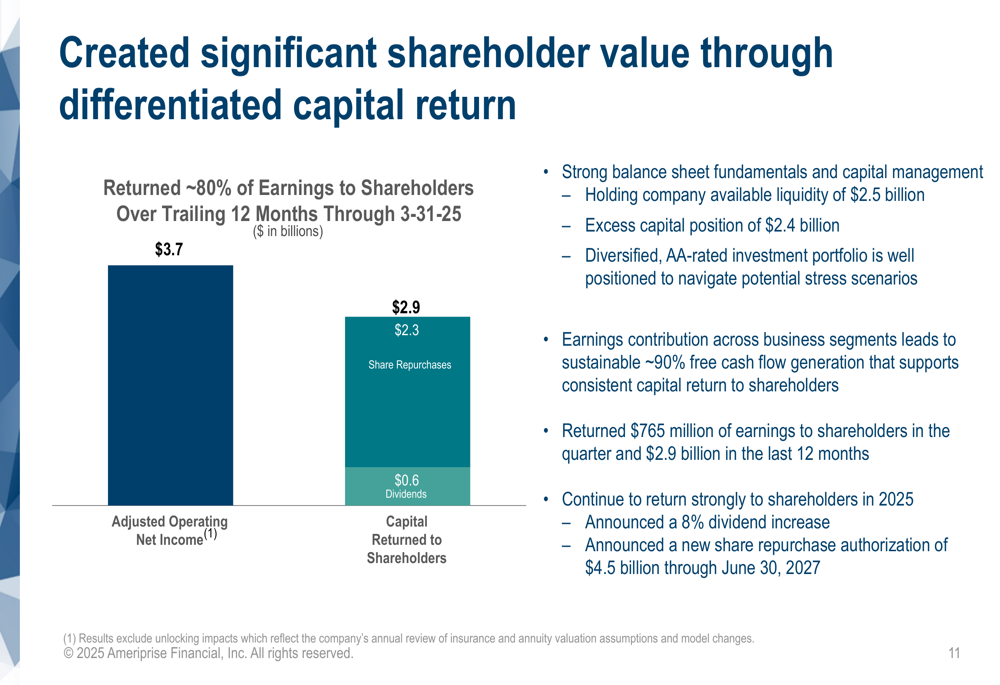

Ameriprise continued its strong track record of returning capital to shareholders while maintaining balance sheet strength. The company returned approximately 80% of earnings to shareholders over the trailing 12 months through March 31, 2025, including $2.3 billion in share repurchases and $0.6 billion in dividends.

The following chart illustrates the company’s capital return to shareholders:

In the first quarter alone, Ameriprise returned $765 million to shareholders. The company also announced an 8% dividend increase and a new share repurchase authorization of $4.5 billion through June 30, 2027.

Ameriprise maintained a strong balance sheet with holding company available liquidity of $2.5 billion and an excess capital position of $2.4 billion. The company’s diversified business model generated approximately 90% free cash flow, supporting consistent capital return while increasing excess capital levels.

Long-Term Performance and Outlook

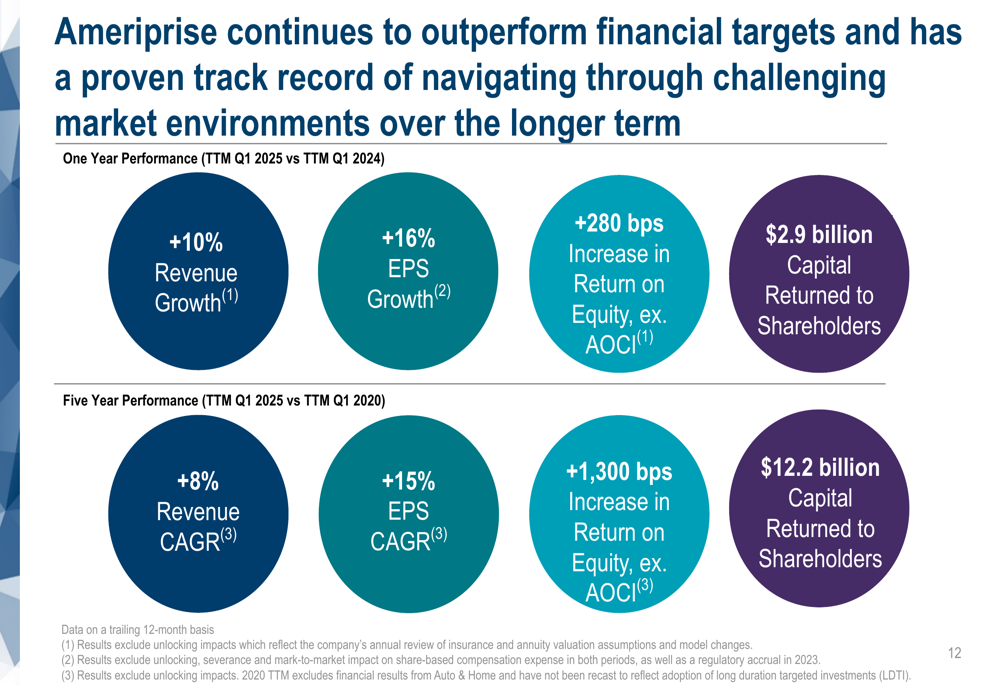

Ameriprise has demonstrated consistent outperformance over both short and long-term periods. Over the past five years (TTM Q1 2025 vs. TTM Q1 2020), the company achieved:

- 8% revenue CAGR

- 15% EPS CAGR

- 1,300 basis points increase in return on equity, excluding AOCI

- $12.2 billion capital returned to shareholders

The following chart highlights this consistent outperformance:

Looking forward, Ameriprise emphasized that its solid operating fundamentals coupled with an excellent balance sheet will enable the company to navigate potential continued elevated volatility levels. The company’s diversified business mix, advice-based value proposition, and strong client relationships position it well for continued success in evolving market conditions.

Management highlighted that the business is well-positioned based upon its high-quality investment portfolio and repositioning actions, with significant flexibility to be opportunistic in the current environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.