Street Calls of the Week

Ameriprise Financial (NYSE:AMP) reported solid second-quarter 2025 results despite market volatility, with shares trading down 2.4% in Thursday’s premarket following the earnings release. The financial services giant delivered 7% growth in adjusted operating earnings per share while maintaining strong margins across its business segments.

Quarterly Performance Highlights

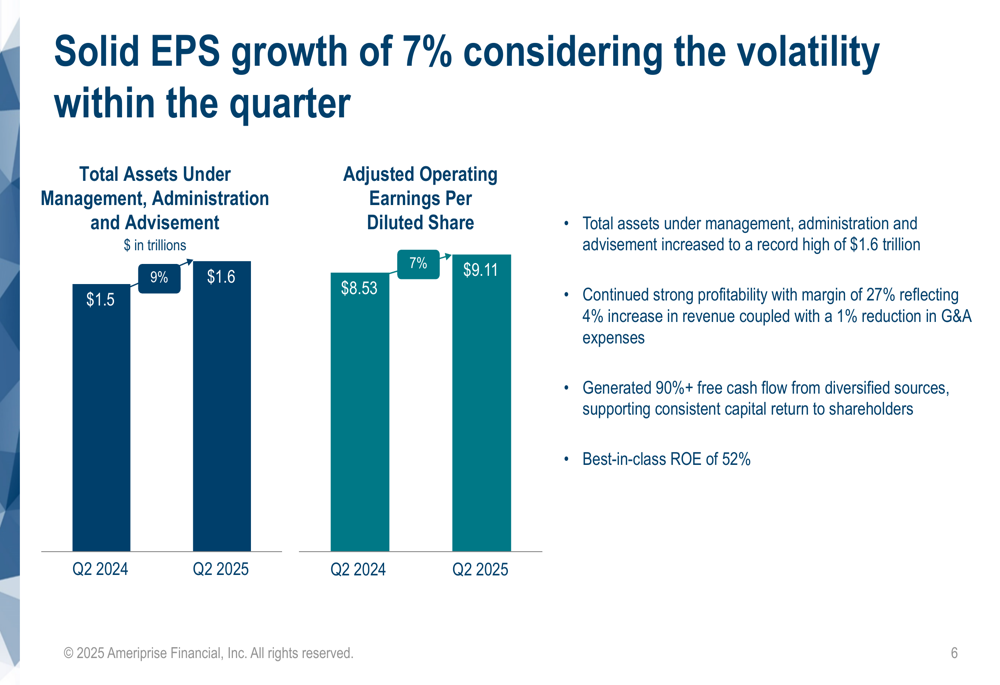

Ameriprise reported adjusted operating earnings per diluted share of $9.11 for Q2 2025, a 7% increase from $8.53 in the same period last year. Adjusted operating net revenues rose 4% to $4.3 billion, while the company maintained a strong 27% margin.

Total (EPA:TTEF) assets under management, administration and advisement reached a record $1.6 trillion, representing a 9% year-over-year increase from $1.5 trillion in Q2 2024.

As shown in the following chart comparing key financial metrics between Q2 2024 and Q2 2025:

"Ameriprise delivered solid performance in a volatile environment," stated Walter Berman, Chief Financial Officer, during the company’s earnings presentation. The company highlighted its expense discipline with year-to-date G&A expenses improving 3% and its ability to generate over 90% free cash flow from diversified sources.

However, the 7% EPS growth in Q2 represents a slowdown from the 13% year-over-year growth reported in Q1 2025, potentially contributing to the negative premarket reaction.

Detailed Financial Analysis

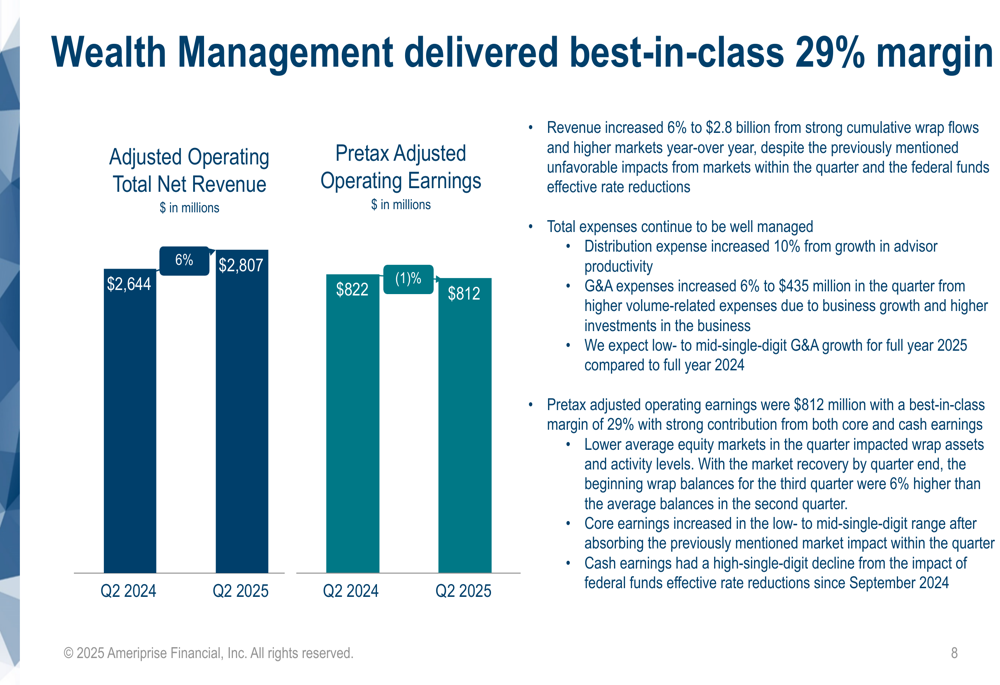

Ameriprise’s Wealth Management segment continued to demonstrate strong performance with a 6% increase in adjusted operating total net revenue to $2.8 billion. The segment maintained a best-in-class margin of 29%, though pretax adjusted operating earnings decreased slightly by 1% to $812 million compared to Q2 2024.

The following chart illustrates the Wealth Management segment’s performance:

Client assets in the Wealth Management segment grew 11% year-over-year to $1,084 billion, with wrap assets increasing 15% to $615 billion. Revenue per advisor also showed strong growth, rising 11% to $1,070,000 on a trailing twelve-month basis.

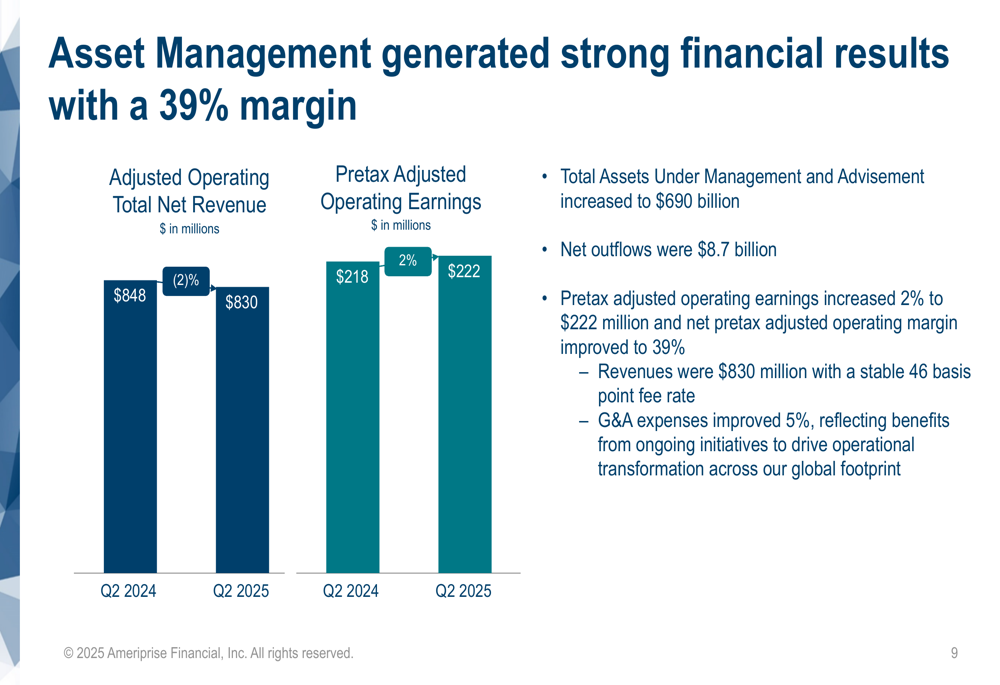

The Asset Management segment faced some challenges with net outflows of $8.7 billion during the quarter. Despite this, the segment generated strong financial results with pretax adjusted operating earnings increasing 2% to $222 million and an improved net pretax adjusted operating margin of 39%.

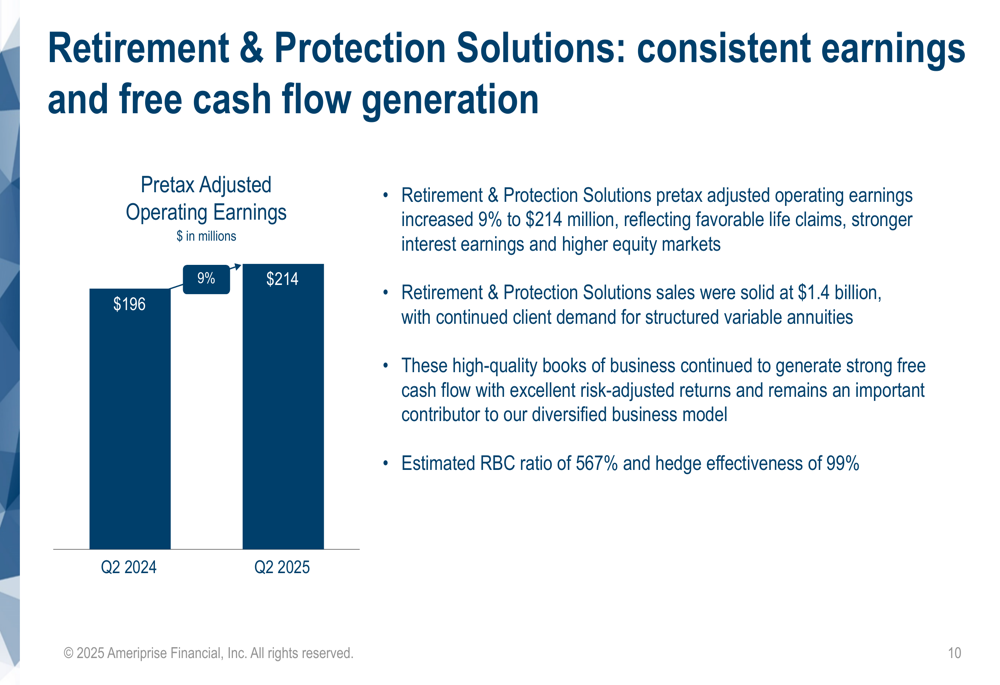

The Retirement & Protection Solutions segment delivered consistent earnings and free cash flow generation, with pretax adjusted operating earnings increasing 9% to $214 million. Sales remained solid at $1.4 billion for the quarter.

Strategic Initiatives & Capital Management

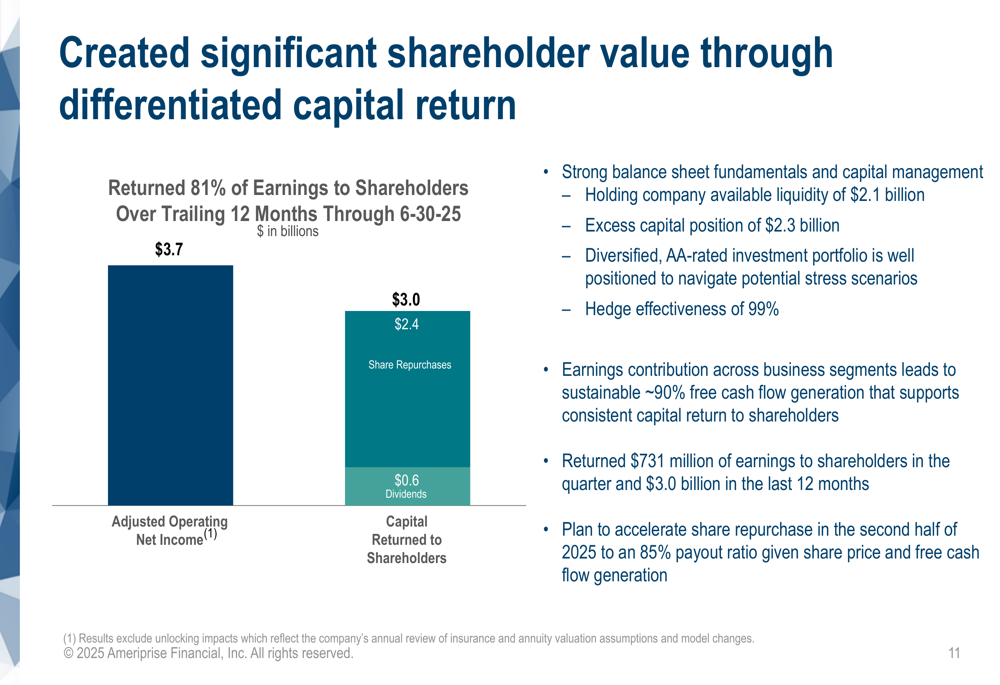

Ameriprise continued its strong capital return to shareholders, returning 81% of earnings over the trailing twelve months through June 30, 2025. This amounted to $3.0 billion, consisting of $2.4 billion in share repurchases and $0.6 billion in dividends.

The following chart details the company’s capital return strategy:

The company maintained a strong balance sheet with $2.3 billion in excess capital and $2.1 billion in holding company available liquidity. This represents a slight decrease from the $2.4 billion excess capital position reported in Q1 2025.

Notably, Ameriprise plans to accelerate share repurchases in the second half of 2025, targeting an 85% payout ratio, up from the current 81%.

Long-Term Performance & Outlook

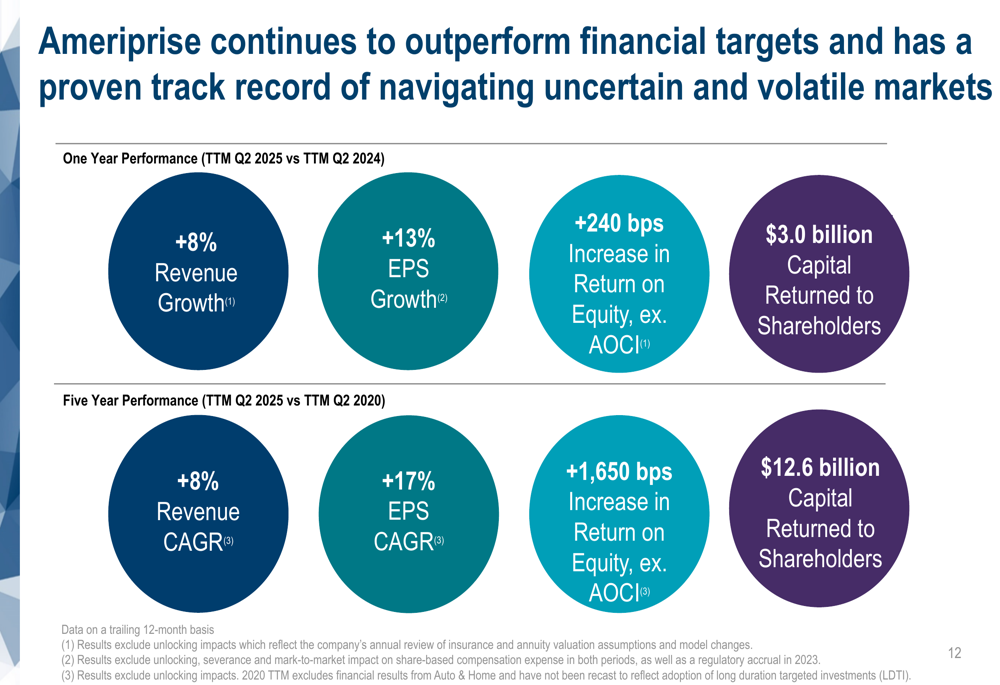

Ameriprise highlighted its consistent outperformance against financial targets over both one-year and five-year timeframes. Over the past year, the company achieved 8% revenue growth and 13% EPS growth, while the five-year performance showed 8% revenue CAGR and an impressive 17% EPS CAGR.

The company’s return on equity excluding AOCI improved by 240 basis points year-over-year to 51.5%, and by 1,650 basis points over the five-year period from 35.6% in Q2 2020.

As illustrated in the following performance metrics:

Despite the solid quarterly results, Ameriprise shares were trading down 2.4% at $524.06 in Thursday’s premarket session. The stock had closed at $536.96 on Wednesday, near the middle of its 52-week range of $385.74 to $582.05.

The market reaction suggests investors may be concerned about the sequential slowdown in EPS growth from Q1 to Q2 and the net outflows in the Asset Management segment, despite the company’s strong overall financial performance and increased capital return plans.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.