FTSE 100 today: Index flat at open, European markets mixed; pound weakens

Introduction & Market Context

Amphastar Pharmaceuticals (NASDAQ:AMPH) released its August 2025 corporate presentation highlighting the company’s strategic shift toward higher-margin proprietary and biosimilar products. The presentation comes after a challenging first quarter where the company missed earnings expectations, with Q1 2025 EPS of $0.51 falling short of the forecasted $0.694 and revenue of $170.5 million missing the $174.35 million projection.

Despite these near-term challenges, Amphastar’s presentation outlines a compelling long-term growth strategy focused on leveraging its technical capabilities and integrated business model. The company’s stock currently trades at $21.62, up 3.84% in the most recent session but significantly below its 52-week high of $53.96, suggesting investor caution despite the optimistic outlook presented by management.

Strategic Initiatives

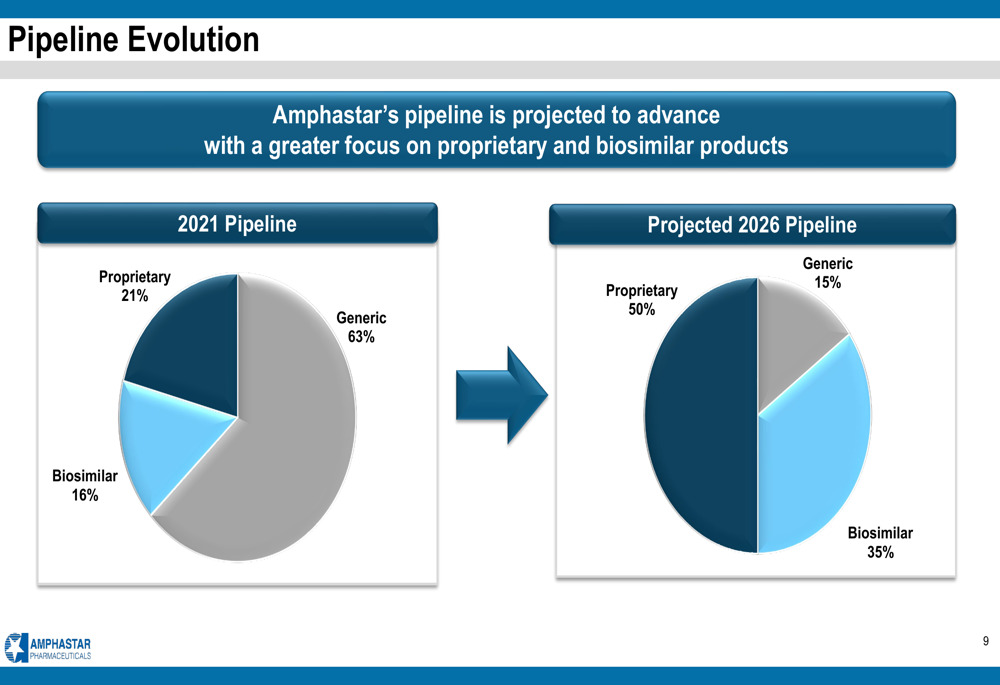

Amphastar’s presentation emphasizes a strategic evolution from a predominantly generic drug manufacturer to a company focused on proprietary and biosimilar products. This shift is illustrated in the company’s pipeline composition projections.

As shown in the following chart of Amphastar’s pipeline evolution:

The company plans to dramatically reduce its reliance on generic products from 63% of its pipeline in 2021 to just 15% by 2026, while increasing proprietary products from 21% to 50% and biosimilars from 16% to 35%. This strategic pivot aims to capture higher margins and create more sustainable competitive advantages.

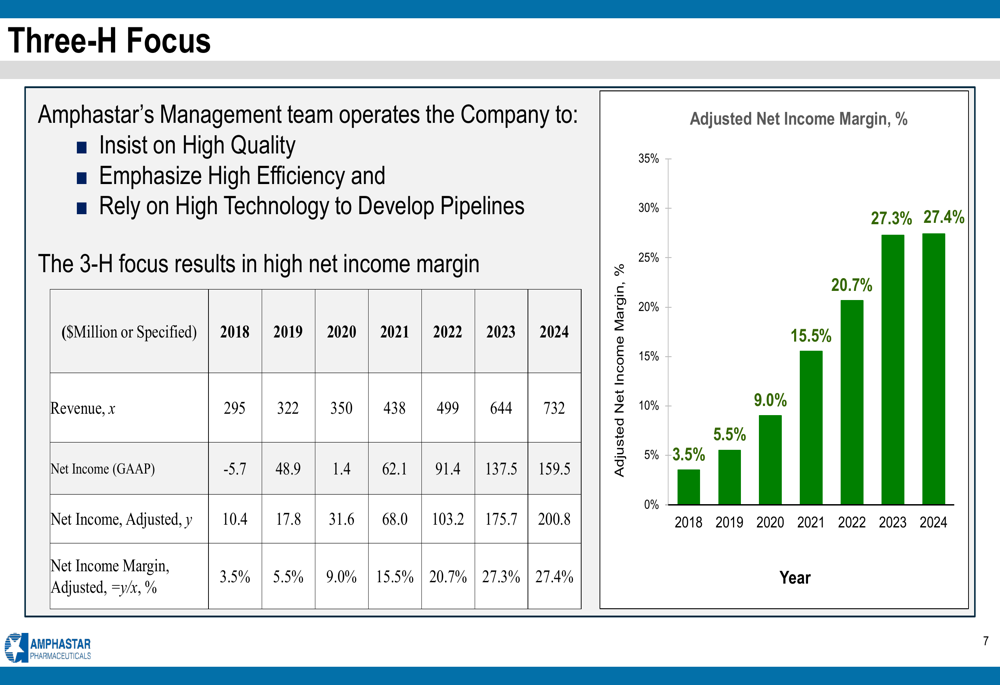

Amphastar’s business model is built around three key pillars: a "One-Stop" fully integrated approach covering R&D through distribution, a "Dual Strategies Growth Model" combining organic pipeline development with strategic acquisitions, and a "Three-H Focus" on high quality, efficiency, and technology.

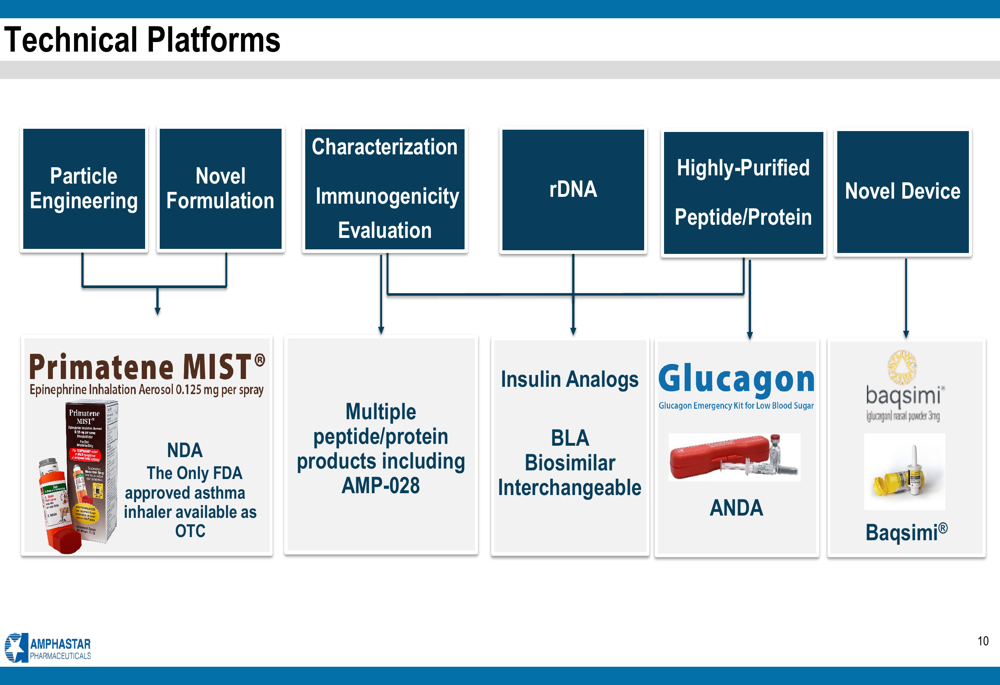

The company’s technical capabilities span multiple platforms, enabling development across various delivery methods and therapeutic areas:

Financial Performance Highlights

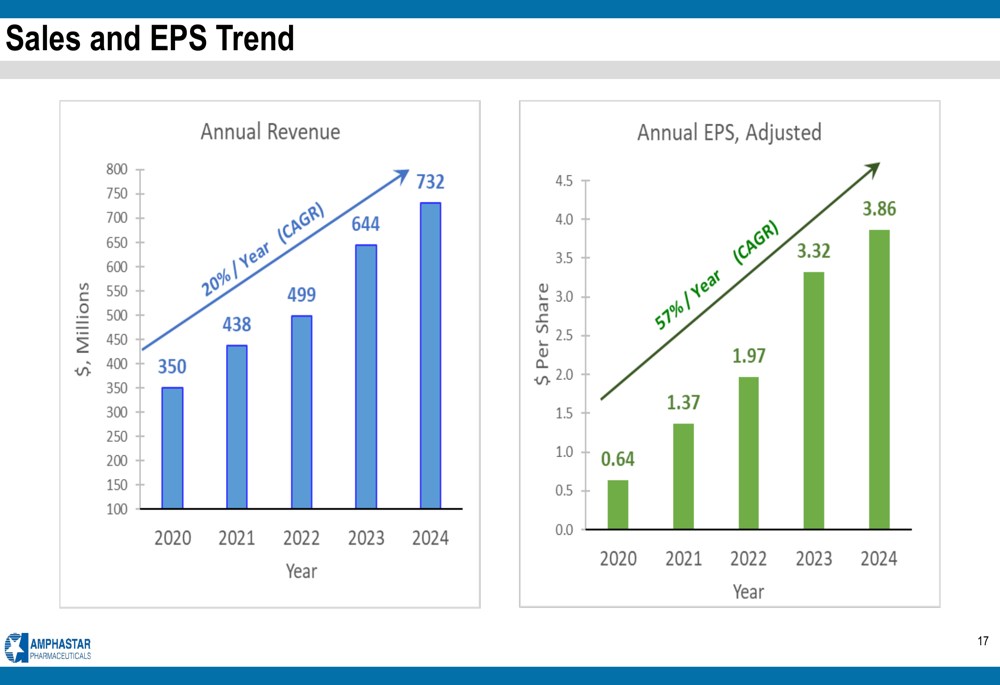

Amphastar’s presentation showcases impressive historical financial growth, though recent quarterly results suggest some moderation in this trajectory. The company has achieved a 20% compound annual growth rate (CAGR) in revenue and a remarkable 57% CAGR in adjusted EPS from 2020 through 2024.

The following chart illustrates this strong historical performance:

Particularly notable is the company’s margin expansion, with adjusted net income margin increasing from just 3.5% in 2018 to 27.4% in 2024:

However, this contrasts with Q1 2025 results, where gross margins declined to 50% from 52.4% in the previous year. The company has maintained substantial R&D investment, spending approximately $351 million over the past five years, though R&D as a percentage of revenue has decreased from 19.2% in 2020 to 10.1% in 2024 as revenue has grown.

Key Product Performance

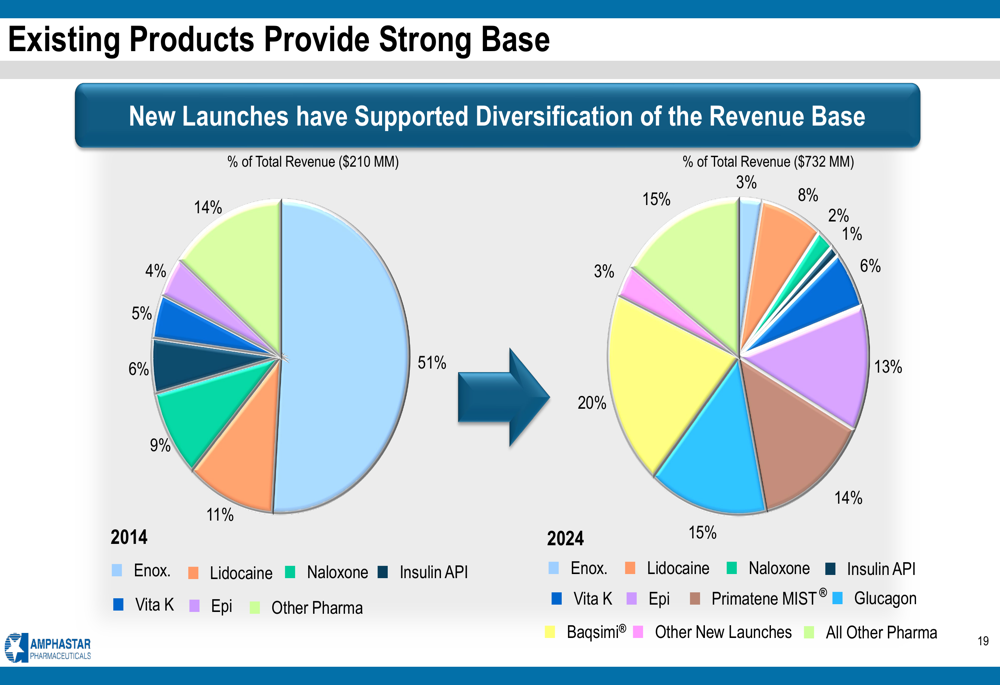

Amphastar has successfully diversified its revenue base over the past decade, reducing dependence on any single product. In 2014, enoxaparin represented 51% of the company’s $210 million total revenue, while by 2024, the company’s $732 million revenue was spread across a much broader portfolio:

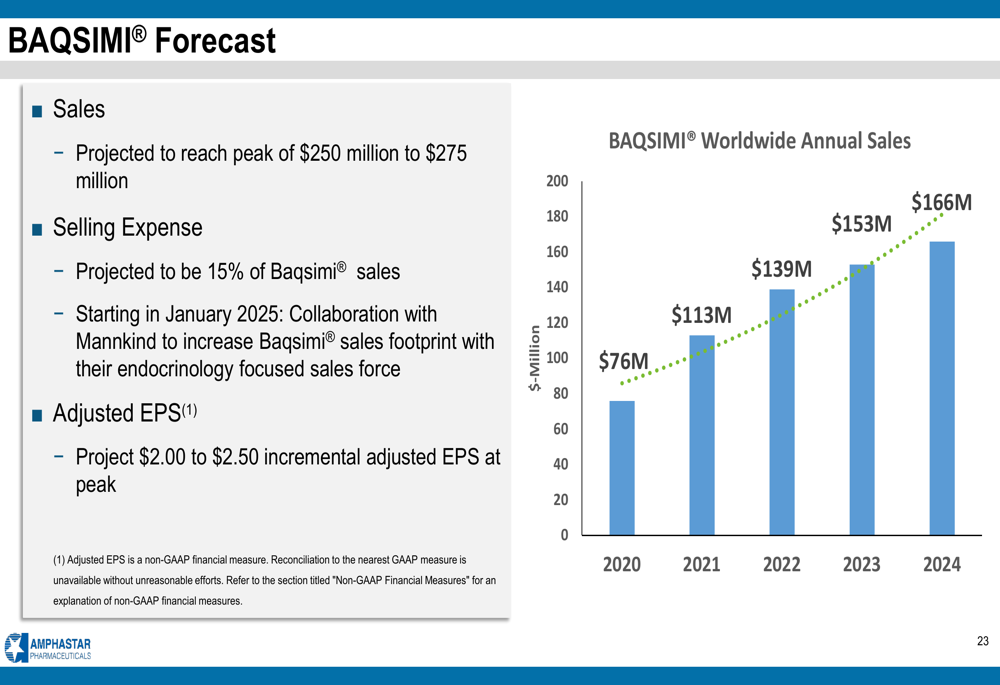

Two key proprietary products driving growth are Baqsimi and Primatene MIST. Baqsimi, a nasal glucagon powder acquired from another manufacturer, is projected to reach peak sales of $250-275 million. The product has shown steady growth, with sales increasing from $76 million in 2020 to $166 million in 2024:

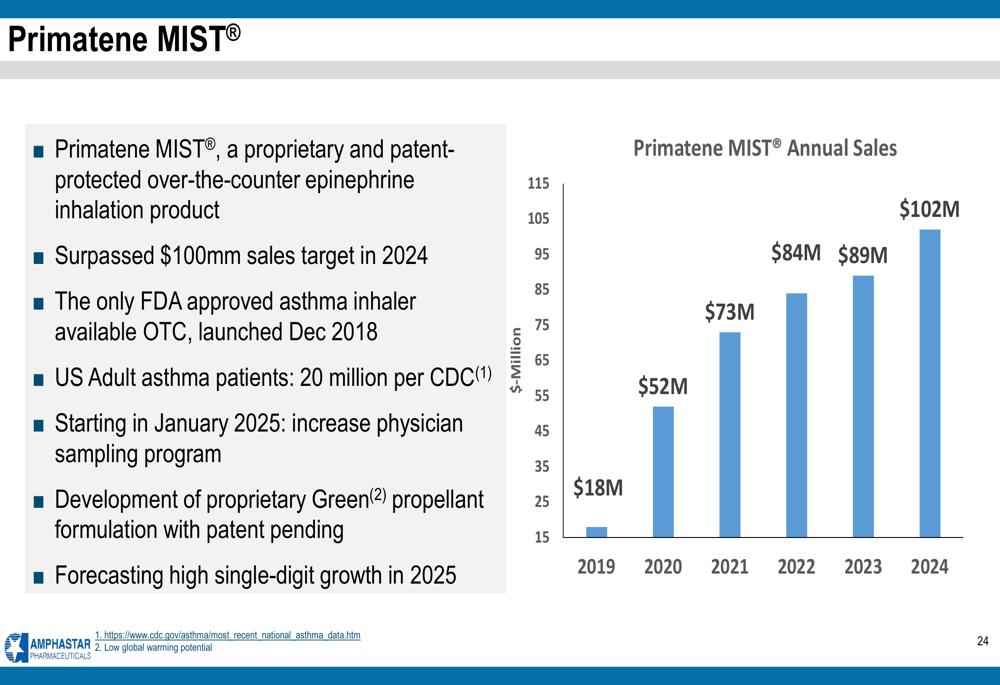

Primatene MIST, an over-the-counter epinephrine inhalation product, has exceeded the company’s $100 million sales target in 2024, growing consistently since its launch:

However, the recent earnings report indicated challenges for some key products, with declining sales in Glucagon and Epinephrine noted in the Q1 2025 results.

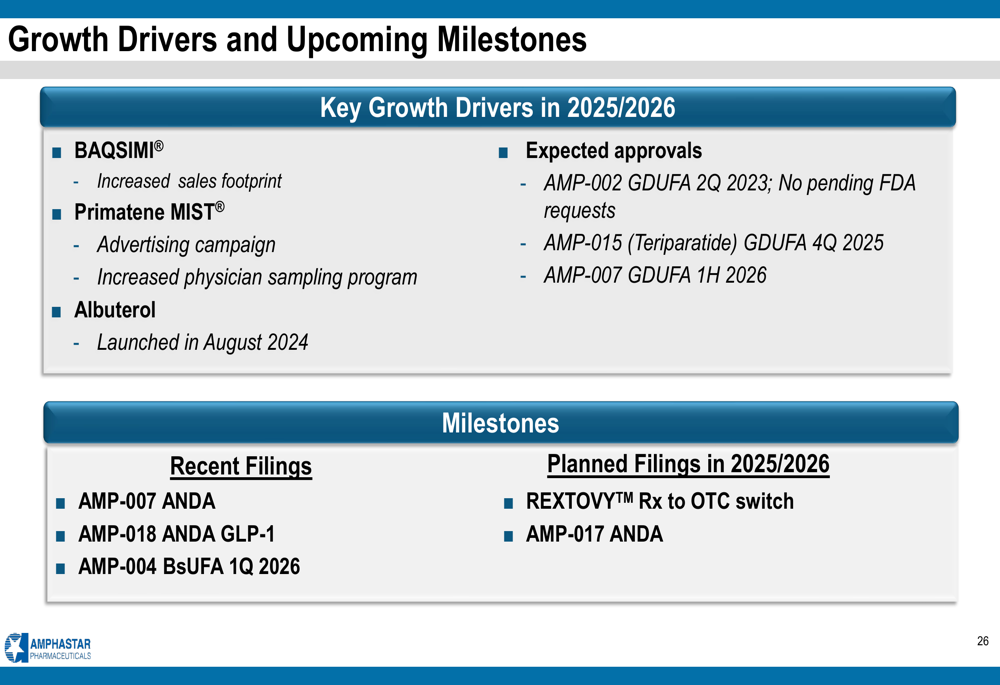

Pipeline and Growth Catalysts

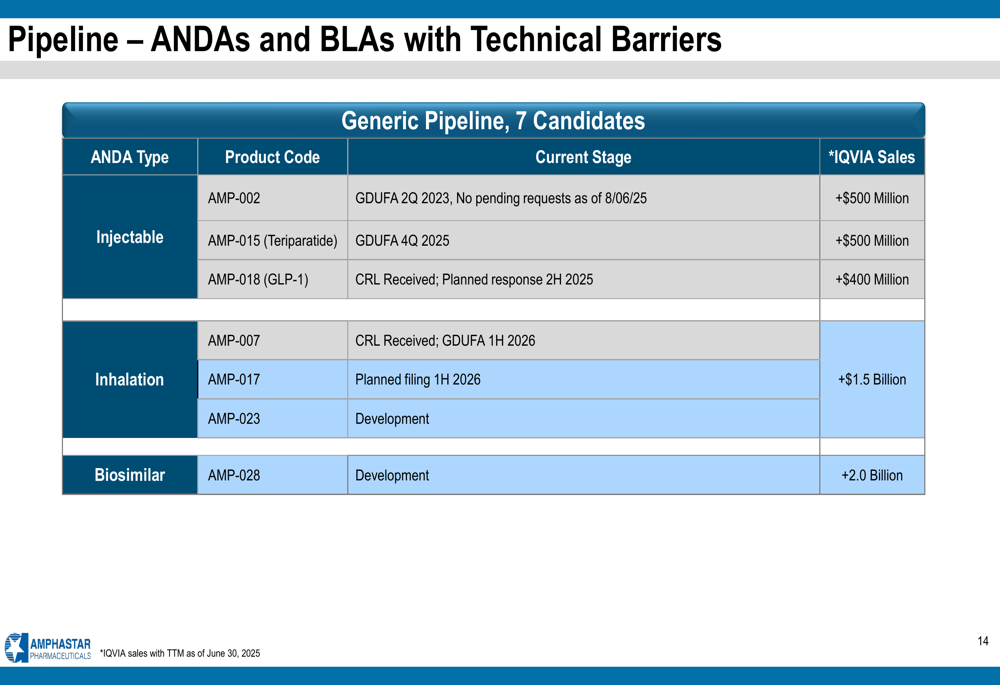

Amphastar’s pipeline includes seven candidates with combined market potential exceeding $5 billion. The company has several products awaiting FDA decisions and others in development:

The company’s diabetes portfolio is particularly robust, including commercialized products like Glucagon Injection Kit and Baqsimi, as well as pipeline candidates including a GLP-1 ANDA (AMP-018) and several insulin products. This positions Amphastar to compete across the full spectrum of diabetes care.

Key upcoming milestones include:

Forward-Looking Statements

While Amphastar’s presentation paints an optimistic picture of long-term growth, the company faces several near-term challenges. During the recent earnings call, management indicated expectations for flat revenue in 2025, a notable contrast to the strong growth trajectory highlighted in the presentation.

CFO Bill Peters emphasized the company’s focus on becoming the first to offer interchangeable biosimilar insulin products, while SVP Dan Dishner acknowledged that "transitioning from a generic-driven business model to a more diversified portfolio... is a process that requires time and strategic effort."

The company’s ability to navigate competitive pressures in the generic market, secure FDA approvals for pipeline products, and successfully execute its strategic shift will be critical factors for investors to monitor. Despite current headwinds, Amphastar maintains strong financial health with a current ratio of 3.07, providing flexibility to fund ongoing growth initiatives.

Amphastar’s presentation demonstrates a clear long-term vision, but investors should balance this against the recent quarterly performance and recognize that the strategic transformation may take time to fully materialize in financial results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.