Wang & Lee Group board approves 250-to-1 reverse share split

Introduction & Market Context

Amplify Energy Corp (NYSE:AMPY) released its May 2025 investor presentation highlighting the company’s strategic focus on Beta field development amid recent financial challenges. The oil and gas producer, currently trading at $2.89 per share, has seen its stock struggle following a disappointing Q4 2024 performance where it reported an EPS of -$0.19, missing the forecasted $0.30.

The presentation comes at a critical time for Amplify, as the company reported negative free cash flow of $7 million in Q1 2025, continuing a challenging trend after its Q4 2024 results triggered an 11.94% stock drop in after-hours trading. Despite these headwinds, the company maintains that its diversified, low-decline asset base positions it well for future growth.

Executive Summary

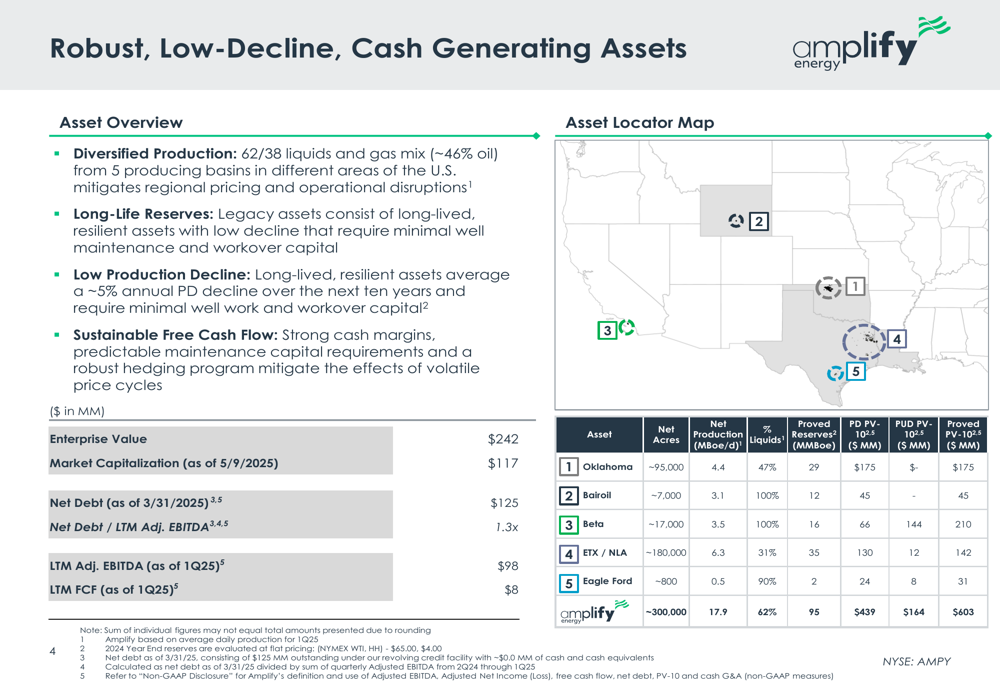

Amplify Energy’s presentation emphasizes its portfolio of robust, low-decline assets across five producing basins, with a 62/38 liquids and gas mix. The company highlighted its progress in debt reduction, lowering leverage from 2.0x at year-end 2022 to 1.3x in Q1 2025, while delivering approximately $19 million in Adjusted EBITDA for the quarter.

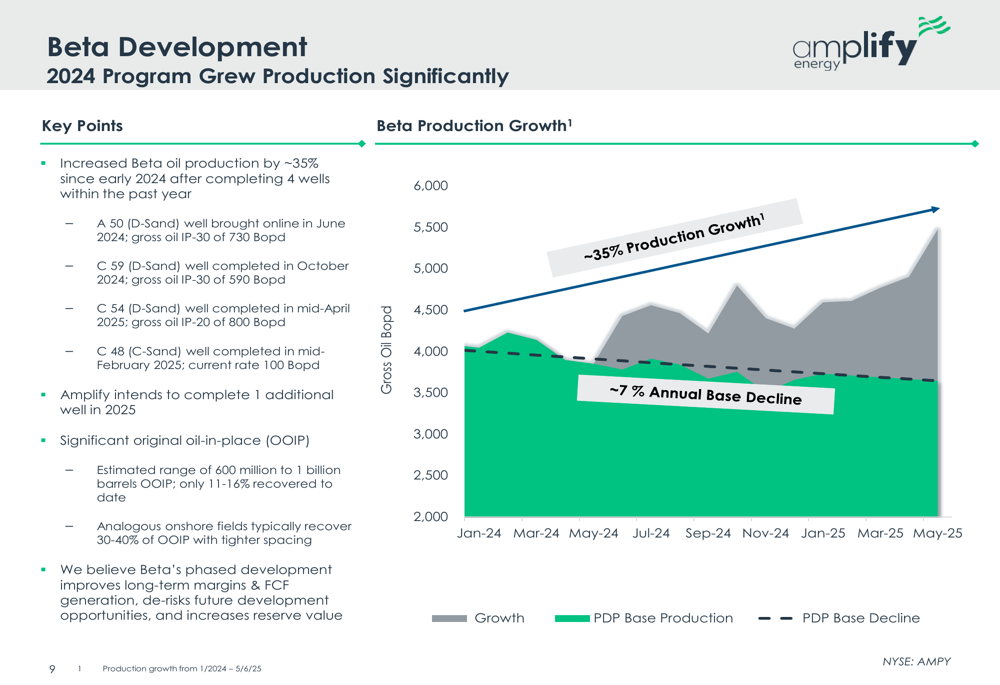

The most compelling aspect of the presentation focuses on the company’s Beta field development, where production has increased by approximately 35% since early 2024 after completing four wells. Management points to these results as evidence of significant untapped potential in the Beta field, which they claim offers lower breakeven prices than any resource play in the lower 48 states.

As shown in the following asset overview chart, Amplify’s diversified portfolio spans approximately 300,000 net acres across multiple basins, with total proved reserves of 95 MMBoe valued at $603 million (PV-10) at $65/$4.00 pricing:

Detailed Financial Analysis

Amplify’s financial position shows an enterprise value of $242 million, market capitalization of $117 million, and net debt of $125 million as of the presentation date. The company has reduced its net debt by approximately $65 million from year-end 2022 to Q1 2025, improving its leverage ratio to 1.3x from 2.0x.

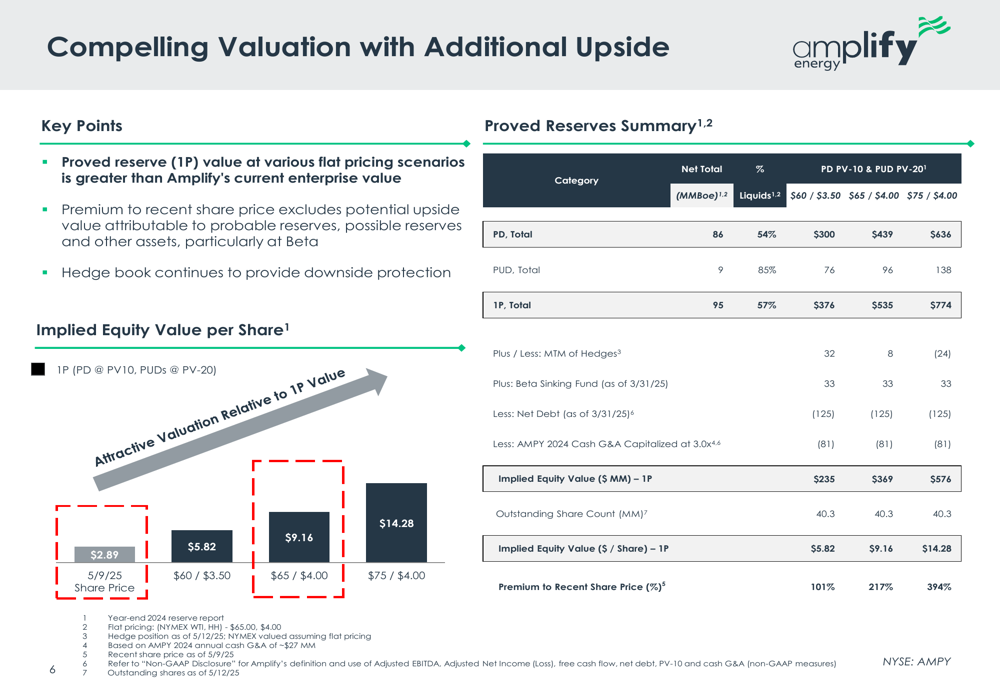

The presentation highlights a significant valuation gap, claiming that the company’s proved reserves value at various flat pricing scenarios substantially exceeds its current enterprise value. At $65/$4.00 pricing, Amplify calculates an implied equity value per share of $9.16, representing a 217% premium to its recent share price.

The following valuation analysis illustrates this claimed upside potential across different commodity price scenarios:

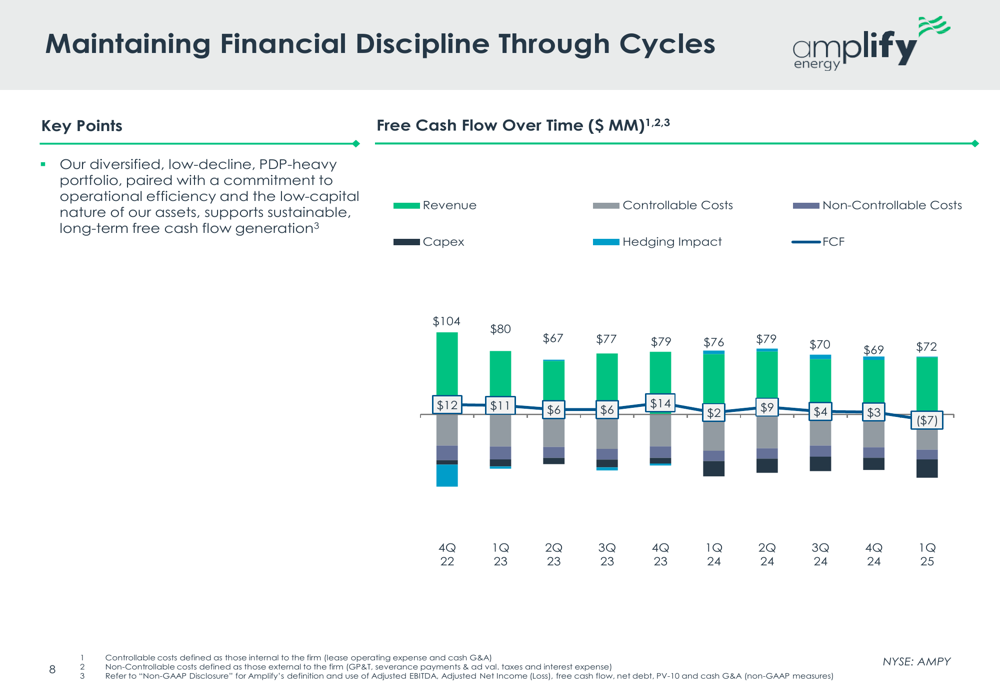

However, this valuation narrative contrasts with recent financial performance. Free cash flow has been inconsistent, with Q1 2025 showing negative $7 million, following modest positive results in previous quarters ($3 million in Q4 2024, $4 million in Q3 2024). This trend raises questions about the company’s ability to achieve its 2025 FCF guidance of $10-20 million.

The company’s free cash flow performance over recent quarters is illustrated in this chart:

Strategic Initiatives

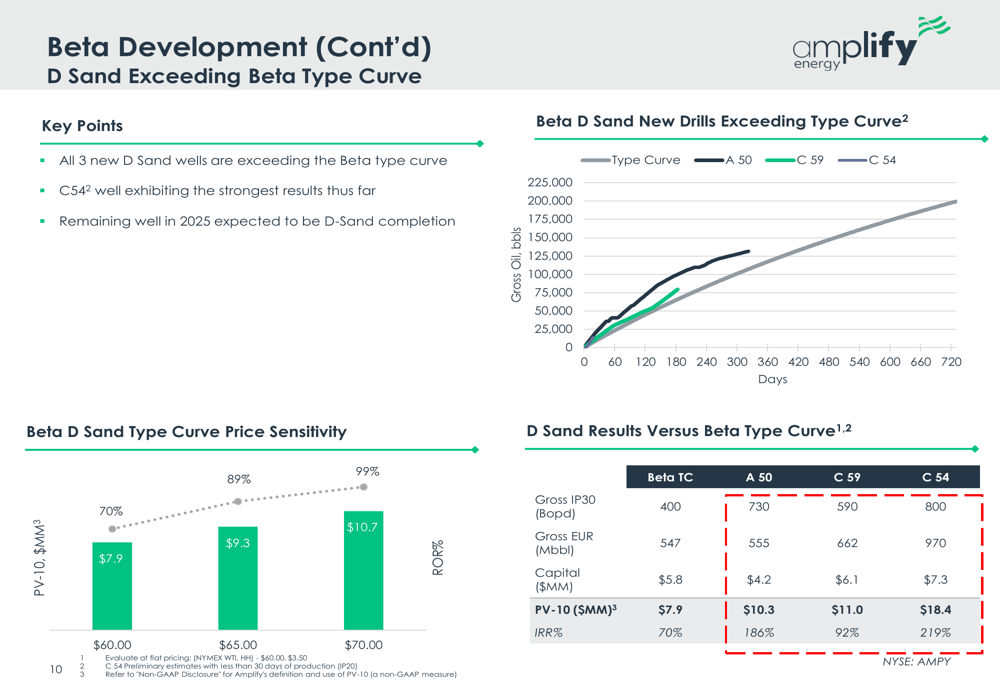

Beta field development emerges as the centerpiece of Amplify’s growth strategy. The company reports that all three new D-Sand wells are exceeding the Beta type curve, with the C54 well exhibiting the strongest results thus far, achieving a gross oil IP-20 of approximately 800 barrels of oil per day in mid-April 2025.

The presentation showcases the Beta production growth trajectory, highlighting a 35% increase since early 2024:

Amplify claims its recent D-Sand wells are significantly outperforming type curves, with impressive internal rates of return ranging from 92% to 219%. The company provides the following comparison of actual well performance versus type curve expectations:

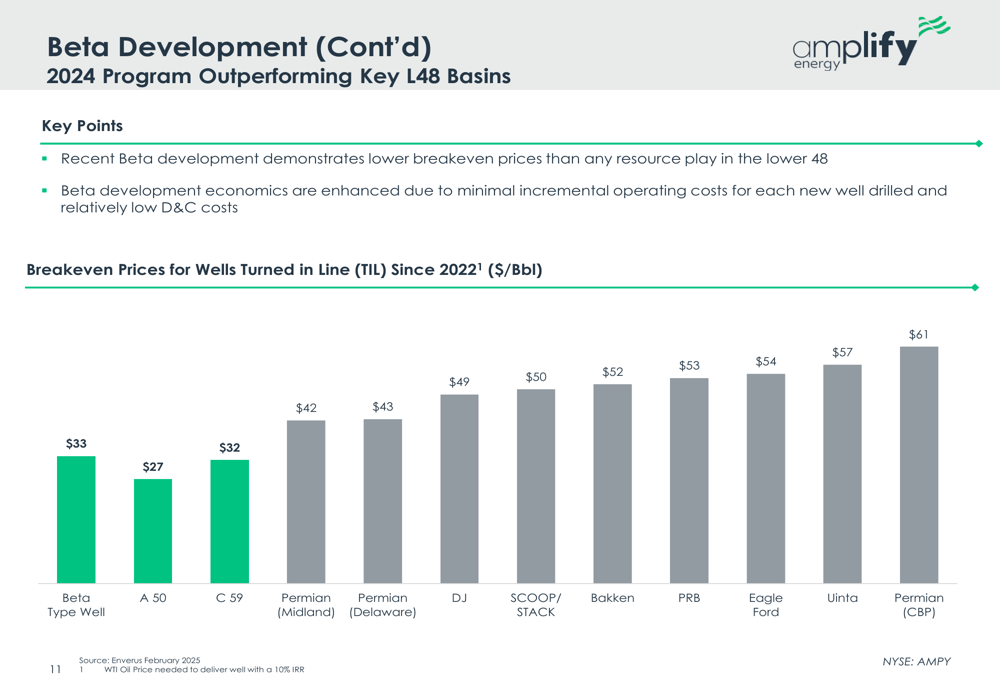

A key competitive advantage highlighted is the Beta field’s superior economics compared to other U.S. basins. The company presents data showing Beta’s average breakeven price of $33 per barrel is substantially lower than major U.S. shale plays:

Forward-Looking Statements

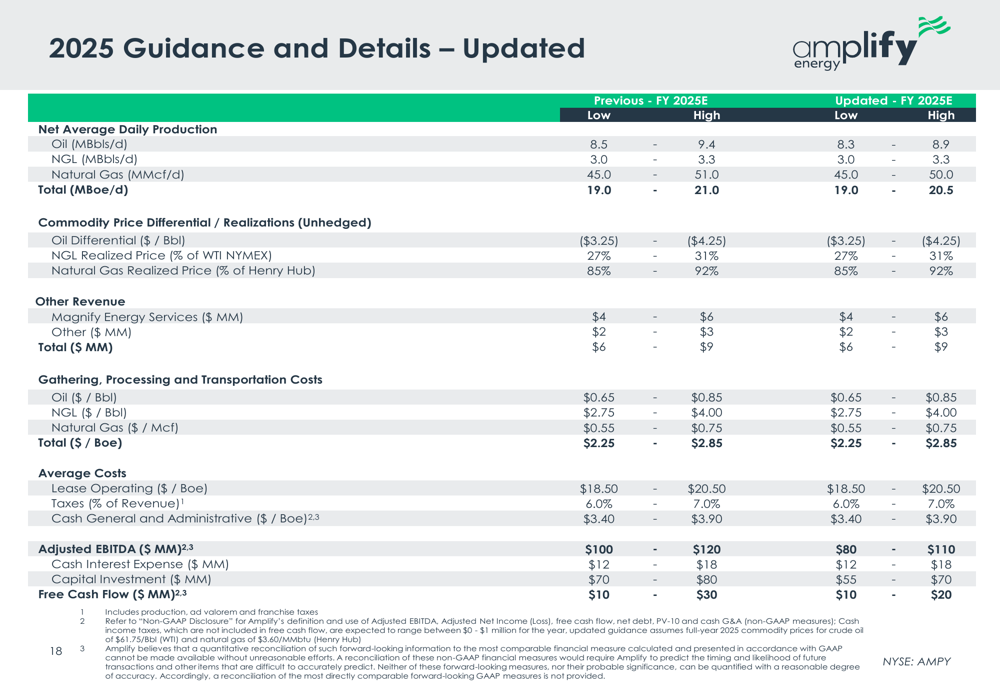

For 2025, Amplify projects total production of 19.0 to 20.5 Mboe/d, Adjusted EBITDA of $80-110 million, capital investments of $55-70 million, and free cash flow of $10-20 million. This guidance comes despite recent oil price volatility and the negative free cash flow reported in Q1 2025.

The company’s detailed 2025 guidance is presented in the following table:

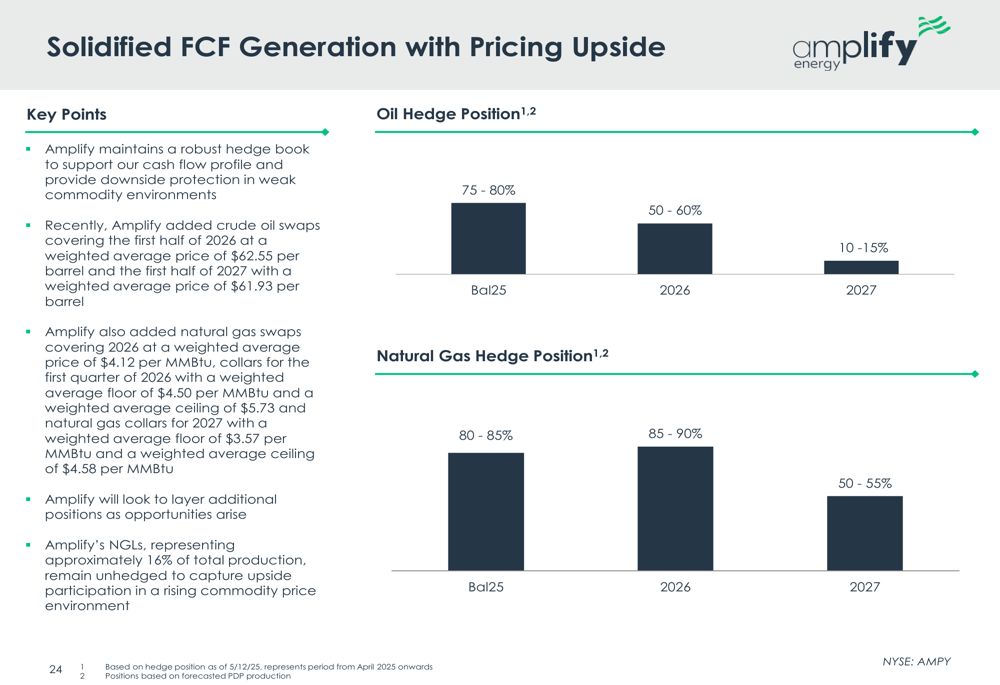

To protect its cash flow profile, Amplify maintains a robust hedging program, with 75-80% of its oil production and 80-85% of its natural gas production hedged for the remainder of 2025. The company’s hedging positions extend through 2027, providing downside protection in weak commodity environments:

ESG Initiatives

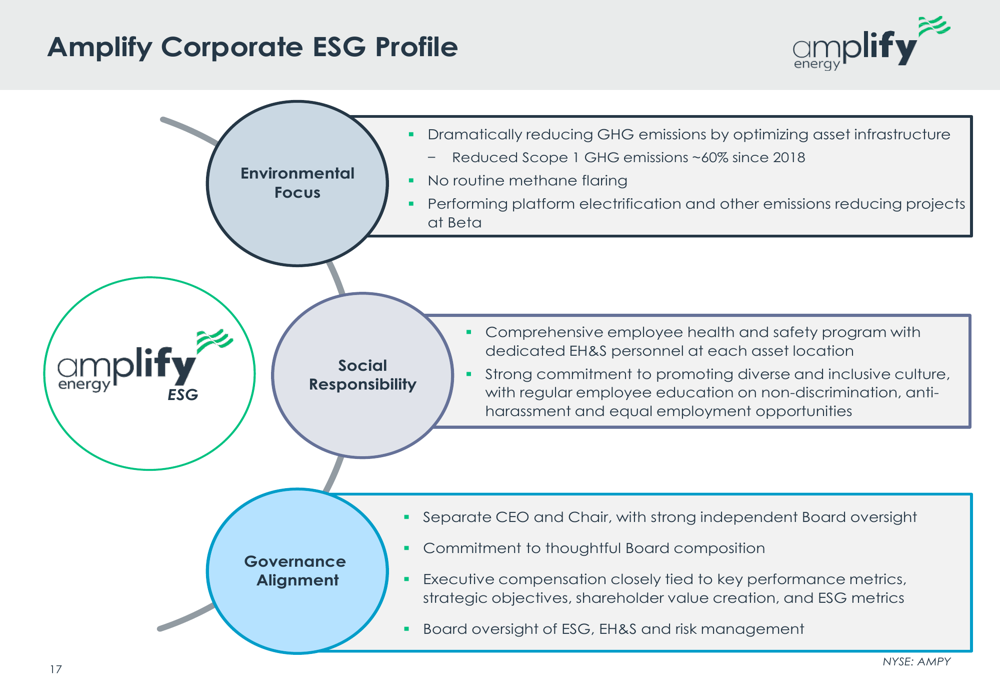

Amplify also highlighted its environmental, social, and governance efforts, noting a 60% reduction in Scope 1 greenhouse gas emissions since 2018. The company emphasized its commitment to optimizing asset infrastructure, eliminating routine methane flaring, and performing platform electrification at Beta.

The company’s ESG profile is summarized in this diagram:

Conclusion

Amplify Energy’s May 2025 presentation makes a compelling case for significant untapped value in its portfolio, particularly in the Beta field development. However, investors should weigh this potential against recent financial challenges, including negative free cash flow in Q1 2025 and the disappointing Q4 2024 results.

While management projects free cash flow of $10-20 million for 2025 and points to a substantial valuation gap between current share price and implied value, the company’s ability to execute on these projections remains uncertain given recent performance. The success of the Beta field development program, with its promising early results and claimed superior economics, will likely be crucial to Amplify’s efforts to bridge this valuation gap and restore investor confidence.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.