These are top 10 stocks traded on the Robinhood UK platform in July

Introduction & Market Context

ANGI Homeservices Inc (NASDAQ:ANGI) unveiled its Q1 2025 performance metrics on May 7, highlighting strategic changes to key performance indicators as the company prepares for its upcoming spin-off scheduled for March 31, 2025. The presentation comes after ANGI reported better-than-expected Q4 2024 results, where revenue reached $267.9 million, exceeding forecasts of $254.41 million.

The company’s stock has responded positively to recent developments, with premarket trading showing a 14.58% increase to $12.89, building on momentum from the 15.03% surge following its Q4 earnings announcement. This investor confidence comes despite ANGI reporting declining volume metrics across several categories, suggesting the market is responding favorably to the company’s quality-over-quantity approach.

Quarterly Performance Highlights

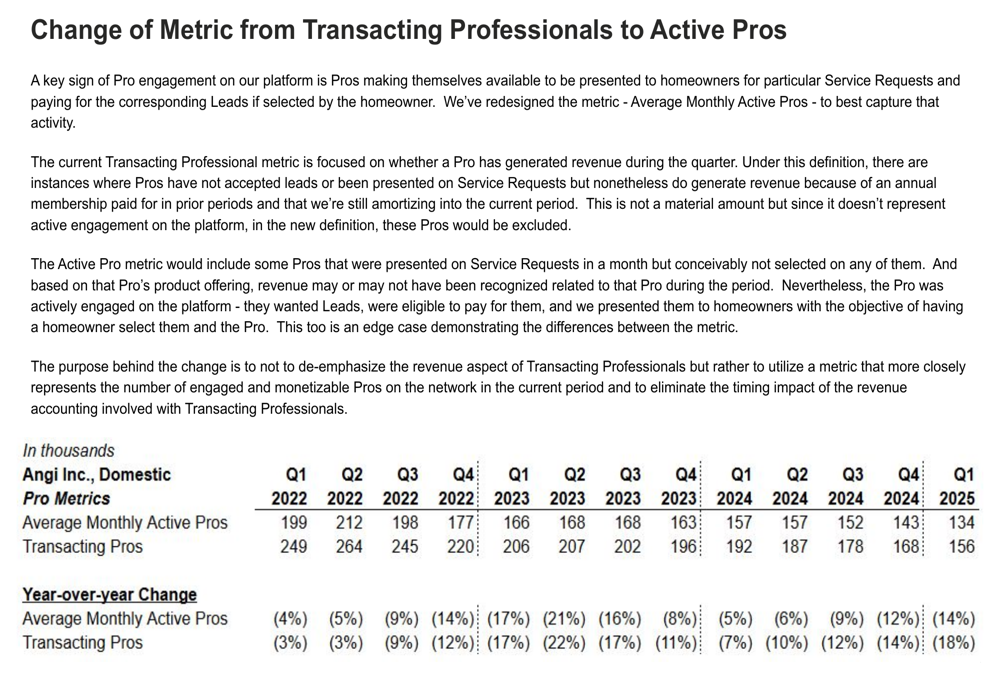

A central focus of ANGI’s presentation was the company’s transition from "Transacting Professionals" to "Active Pros" as a key metric. This change aims to better capture professional engagement on the platform beyond simple transactions.

As shown in the following detailed metrics comparison:

The data reveals that ANGI had 134,000 Average Monthly Active Pros in Q1 2025, representing a 14% year-over-year decline. Similarly, Transacting Pros (the previous metric) stood at 156,000, down 18% from the previous year. While these declines might appear concerning at first glance, they align with ANGI’s strategic pivot toward higher-quality engagement and improved retention.

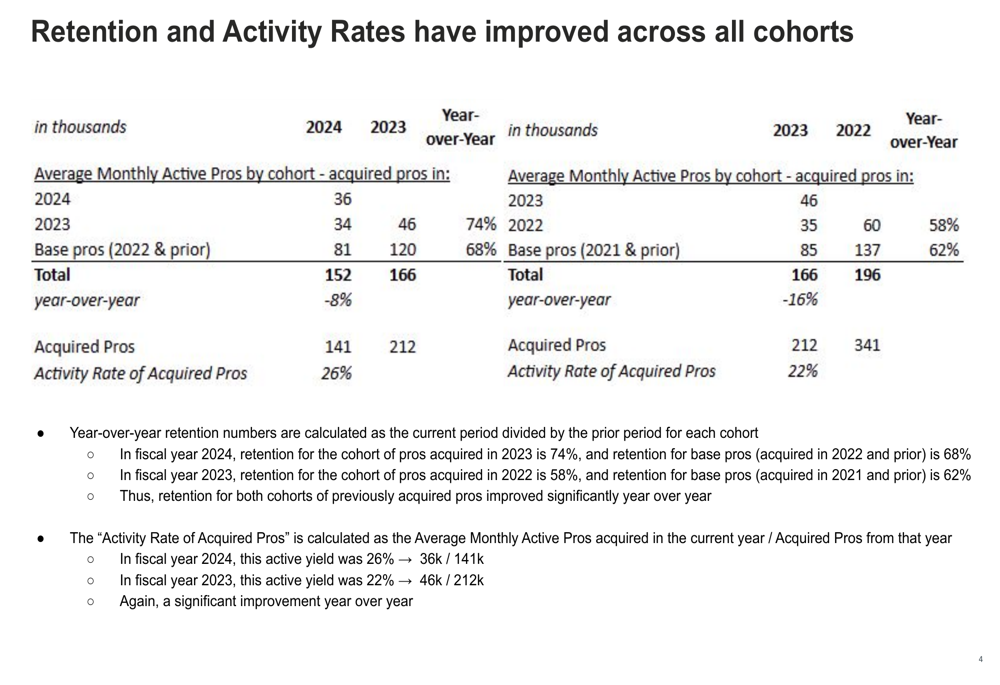

This strategic shift is further illustrated in the company’s cohort analysis, which shows significant improvements in retention rates:

The retention data demonstrates that despite having fewer total professionals on the platform, ANGI has substantially improved its ability to retain existing pros. The 2023 cohort showed a 74% retention rate in 2024, compared to just 58% for the 2022 cohort in 2023. Similarly, base pros (those acquired in 2022 and prior) had a 68% retention rate in 2024, compared to 62% for base pros in 2023.

Additionally, the Activity Rate of Acquired Pros improved to 26% in fiscal year 2024, up from 22% in fiscal year 2023, indicating better engagement among newly onboarded professionals.

Strategic Initiatives

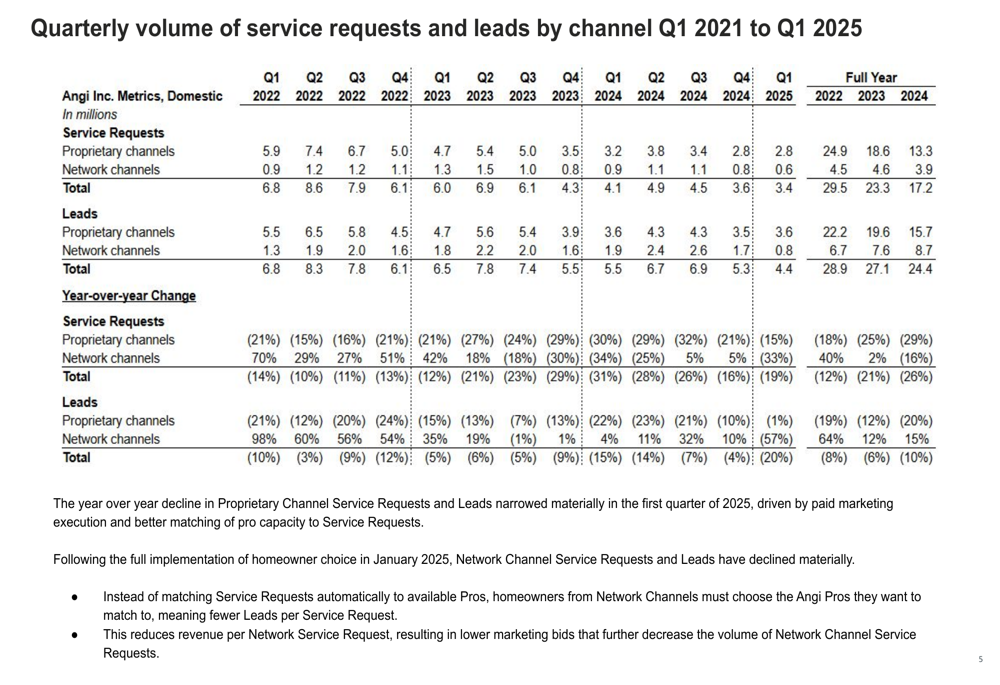

ANGI’s presentation revealed the impact of its Consumer Choice platform implementation, which was fully deployed in January 2025. This strategic initiative has significantly affected the company’s channel metrics, as shown in the following data:

The implementation of homeowner choice has led to a material decline in Network Channel metrics, with Service Requests dropping to 0.6 million in Q1 2025 from 0.9 million in Q1 2024, and Leads falling more dramatically to 0.8 million from 1.9 million in the same period.

Interestingly, while Proprietary Channel Service Requests remained flat year-over-year at 2.8 million, Leads through this channel actually increased to 3.6 million from 3.5 million in Q4 2024. This suggests that ANGI’s strategic focus on its proprietary channels may be starting to yield results in terms of conversion rates, even as overall volume metrics decline.

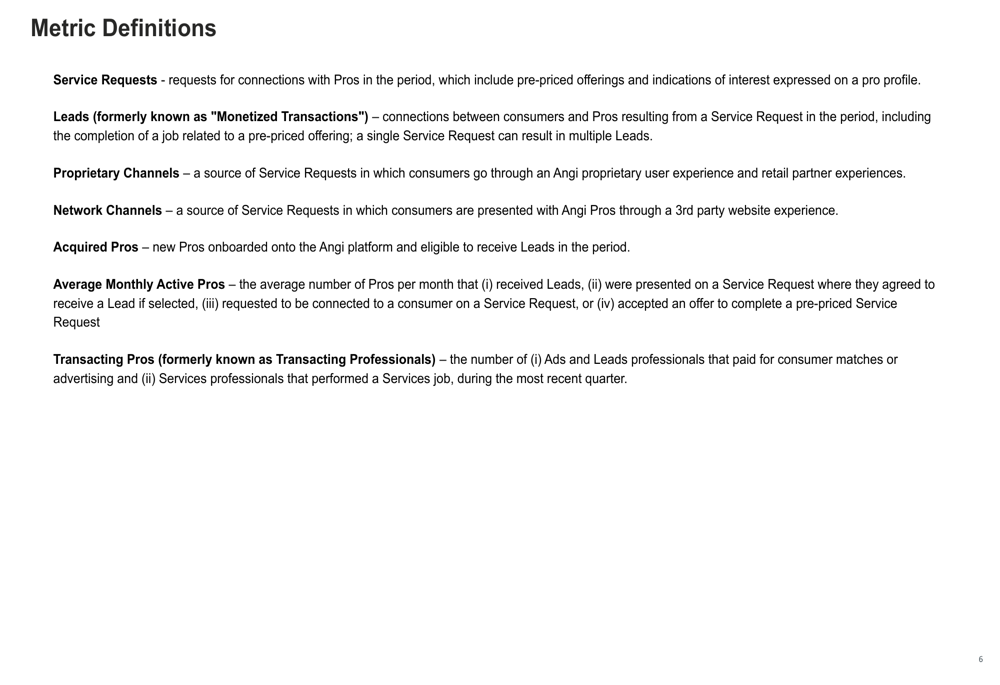

The company defines these metrics as follows:

Forward-Looking Statements

As ANGI approaches its scheduled spin-off on March 31, 2025, the company appears to be positioning itself for growth in 2026 by focusing on quality metrics rather than raw volume numbers. This aligns with CEO Joey Levin’s recent statement that "We’re back on offense," indicating a proactive approach toward future growth and market competitiveness.

The improved retention rates and activity metrics suggest that while ANGI may be working with fewer professionals overall, those remaining on the platform are more engaged and likely more productive. This quality-focused approach could potentially lead to better monetization per transaction, which would explain how the company exceeded revenue expectations in Q4 2024 despite declining volume metrics.

ANGI’s strategic shift toward its Proprietary Channels and away from Network Channels through the Consumer Choice implementation represents a significant pivot in its business model. While this has resulted in a material decline in Network Channel metrics, it may position the company for more sustainable growth with higher-quality customer and professional interactions.

As the company prepares for its spin-off, investors will be watching closely to see if these strategic changes translate into improved financial performance and whether the quality-over-quantity approach can drive long-term growth in the competitive home services market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.