Gold bars to be exempt from tariffs, White House clarifies

Introduction & Market Context

Anika Therapeutics (NASDAQ:ANIK) released its second quarter 2025 earnings presentation on July 30, revealing continued challenges as the company reported an 8% year-over-year revenue decline. The stock reacted negatively, falling 6.27% in premarket trading to $10.46, approaching its 52-week low of $10.47.

The medical technology company, which specializes in joint preservation and restoration solutions, continues to face headwinds in its OEM business while working to advance its commercial product portfolio and pipeline candidates. This follows a disappointing Q1 2025, when the company missed both earnings and revenue forecasts.

Quarterly Performance Highlights

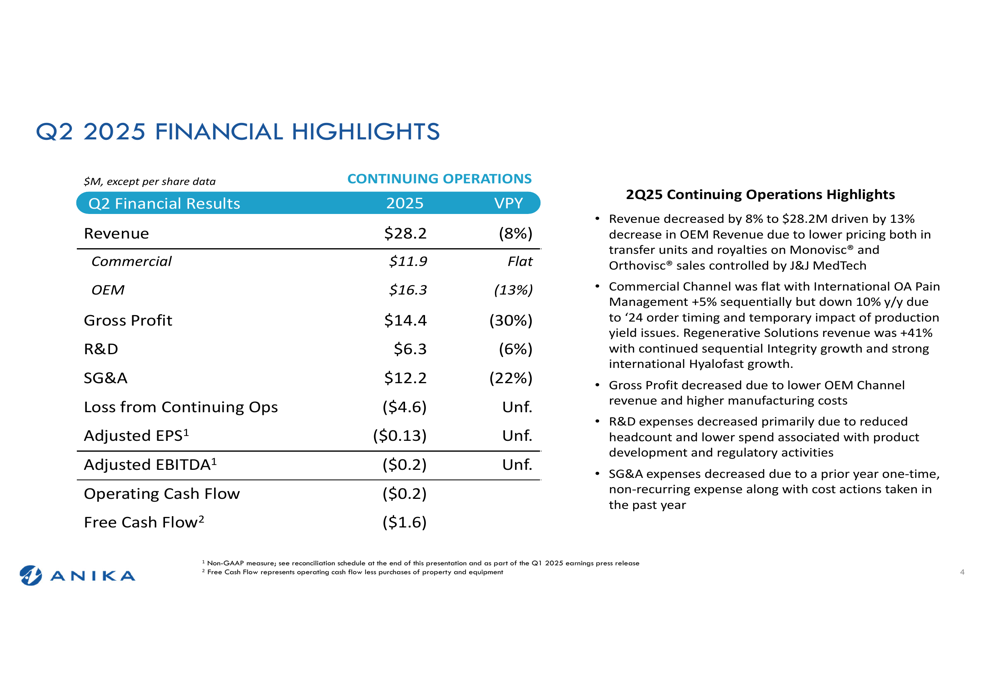

Anika reported Q2 2025 revenue of $28.2 million, down 8% compared to the same period last year. The decline was primarily driven by weakness in the OEM channel, which fell 13% year-over-year to $16.3 million, while the Commercial channel remained flat at $11.9 million.

As shown in the following financial highlights:

Profitability metrics showed significant pressure, with gross profit declining 30% to $14.4 million. The company reported a loss from continuing operations of $4.6 million and adjusted EPS of -$0.13. Adjusted EBITDA was slightly negative at -$0.2 million, while free cash flow was -$1.6 million.

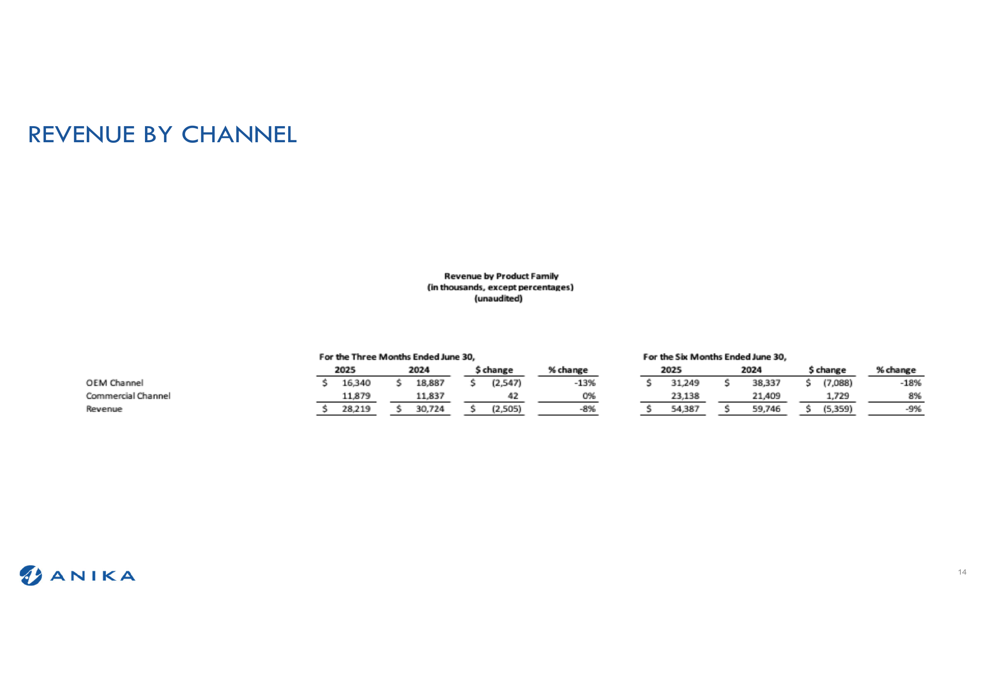

The revenue breakdown by channel provides additional context on the divergent performance:

While Q2 Commercial channel revenue was flat year-over-year, the six-month figures show 8% growth compared to the first half of 2024, indicating some momentum in this segment despite recent challenges. Meanwhile, the OEM channel’s decline accelerated in Q2, contributing to an 18% drop for the first half of 2025.

Strategic Initiatives

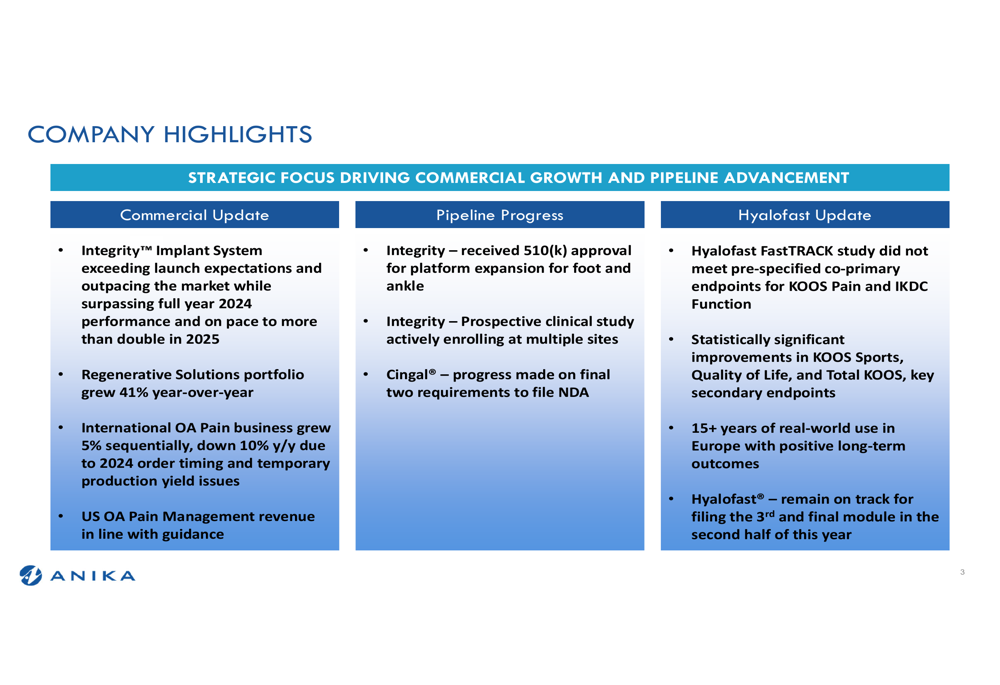

Despite overall financial challenges, Anika highlighted several bright spots in its commercial portfolio and pipeline progress. The company’s strategic focus remains on driving commercial growth and advancing key pipeline products.

The company’s presentation emphasized these key developments:

The Integrity™ Implant System stands out as a particular success, reportedly exceeding launch expectations and on pace to more than double in 2025. Additionally, the Regenerative Solutions portfolio grew 41% year-over-year, providing a counterbalance to challenges in other segments.

On the pipeline front, Anika received 510(k) approval for platform expansion of the Integrity system for foot and ankle applications. However, the company faced a setback with its Hyalofast program, as the FastTRACK study did not meet pre-specified co-primary endpoints for KOOS Pain and IKDC Function, though it did achieve statistically significant improvements in several secondary endpoints.

Forward-Looking Statements

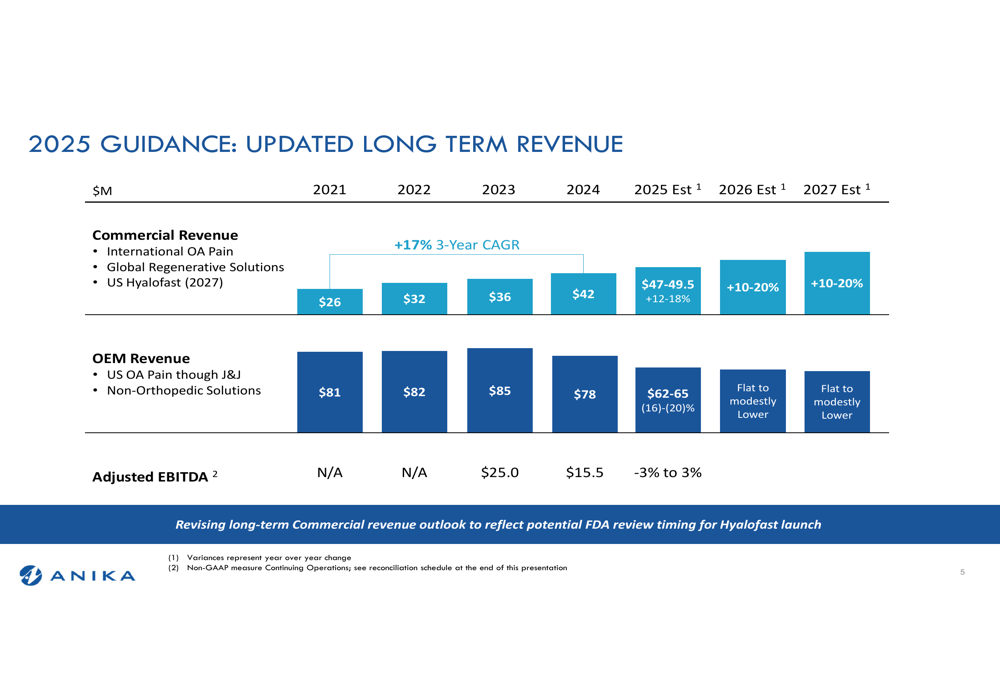

Anika updated its guidance for 2025 and provided a longer-term outlook for revenue growth:

The company projects 2025 Commercial Revenue of $47-49.5 million, representing 12-18% growth, while OEM Revenue is expected to decline 16-20% to $62-65 million. Looking further ahead, Anika anticipates Commercial Revenue growth of 10-20% in both 2026 and 2027, targeting a three-year CAGR of 17%.

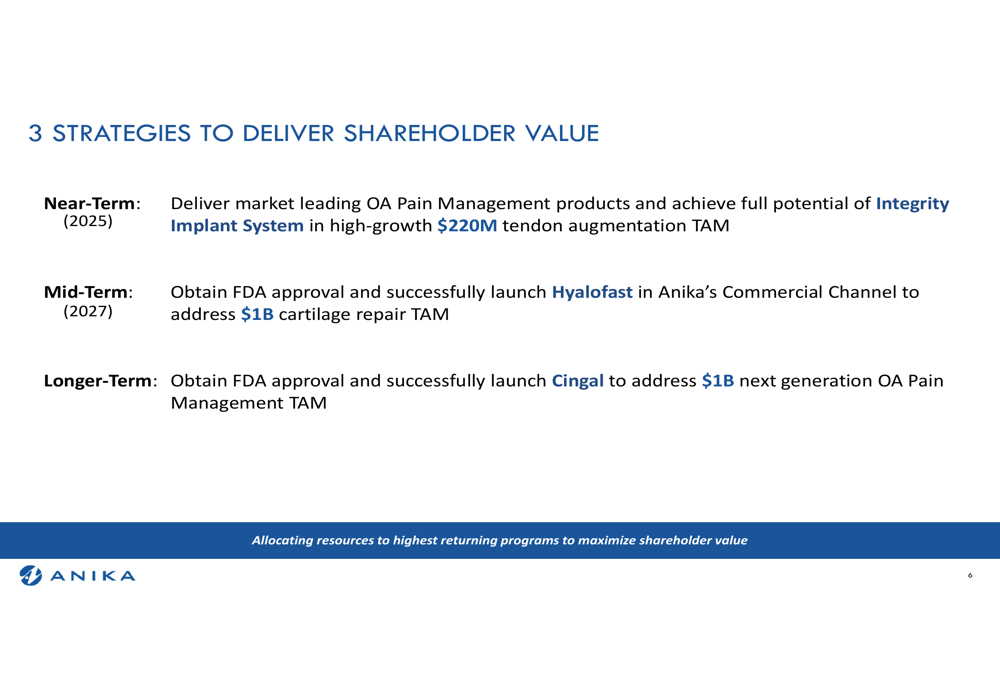

Anika’s strategy to deliver shareholder value focuses on three time horizons:

The near-term focus centers on maximizing the potential of the Integrity Implant System in the $220 million tendon augmentation market, while mid-term goals include obtaining FDA approval and launching Hyalofast to address a $1 billion cartilage repair opportunity. Longer-term, the company aims to secure FDA approval for Cingal to compete in the $1 billion next-generation OA Pain Management market.

Detailed Financial Analysis

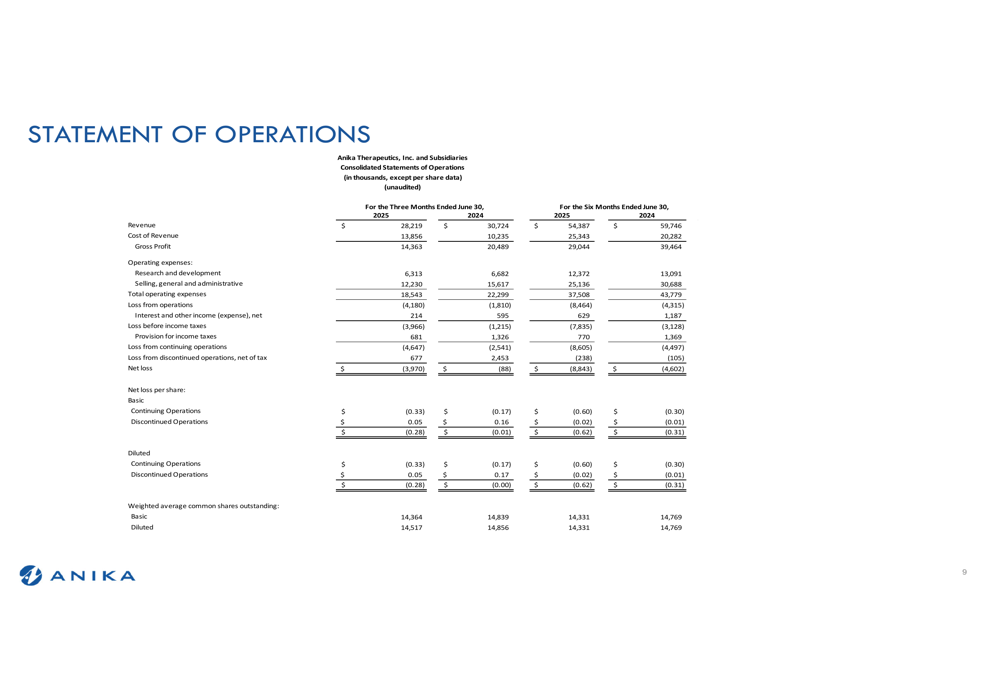

A closer examination of Anika’s financial statements reveals the extent of the company’s current challenges. The consolidated statement of operations shows the year-over-year comparison:

The decline in gross profit margin is particularly concerning, as it indicates increasing cost pressures alongside revenue challenges. Research and development expenses decreased by 6% to $6.3 million, while selling, general, and administrative expenses fell 22% to $12.2 million, reflecting cost-cutting measures.

These results continue a challenging trend for Anika, following Q1 2025’s disappointing performance when the company reported an EPS of -$0.06 against expectations of -$0.04, and revenue of $26.17 million versus a forecast of $28.13 million.

The company’s balance sheet remains relatively stable, though cash flow metrics have weakened. With the stock now trading near its 52-week low, investors appear increasingly concerned about Anika’s ability to return to growth and profitability in the near term, despite management’s optimistic outlook for the commercial segment and pipeline opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.