US stock futures edge lower after S&P 500 hits record high; PCE data in focus

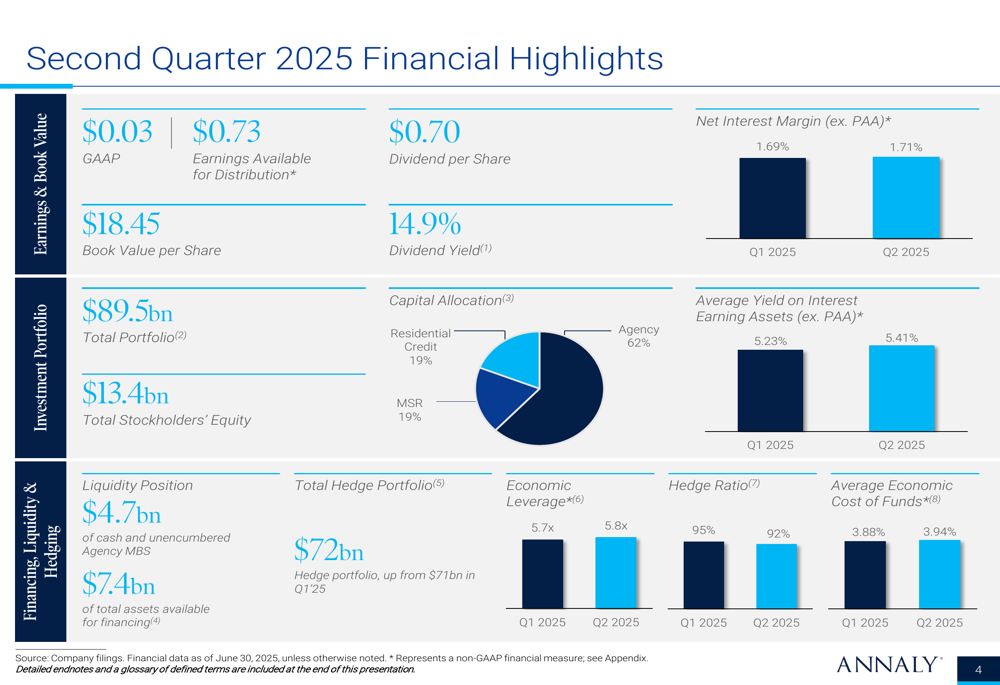

Annaly Capital Management (NYSE:NLY) presented its second quarter 2025 earnings results on July 23, showing earnings available for distribution (EAD) of $0.73 per share that exceeded its dividend despite a decline in book value. The mortgage REIT maintained its strategic focus on Agency mortgage-backed securities while continuing to diversify across residential credit and mortgage servicing rights.

Quarterly Performance Highlights

Annaly reported EAD of $0.73 per average common share for Q2 2025, comfortably covering its declared quarterly dividend of $0.70 per share. However, the company’s book value per common share declined to $18.45, down from $19.02 in the previous quarter. Economic return, which combines dividend and book value change, was 0.7% for the second quarter and 3.7% for the first half of 2025.

"Our portfolio is diversified, liquid and actively managed," CEO David Finkelstein had noted during the previous quarter’s earnings call, a strategy that appears to have continued into Q2.

As shown in the following financial highlights chart, Annaly maintained a strong dividend yield of 14.9% while slightly increasing its economic leverage to 5.8x from 5.7x in the previous quarter:

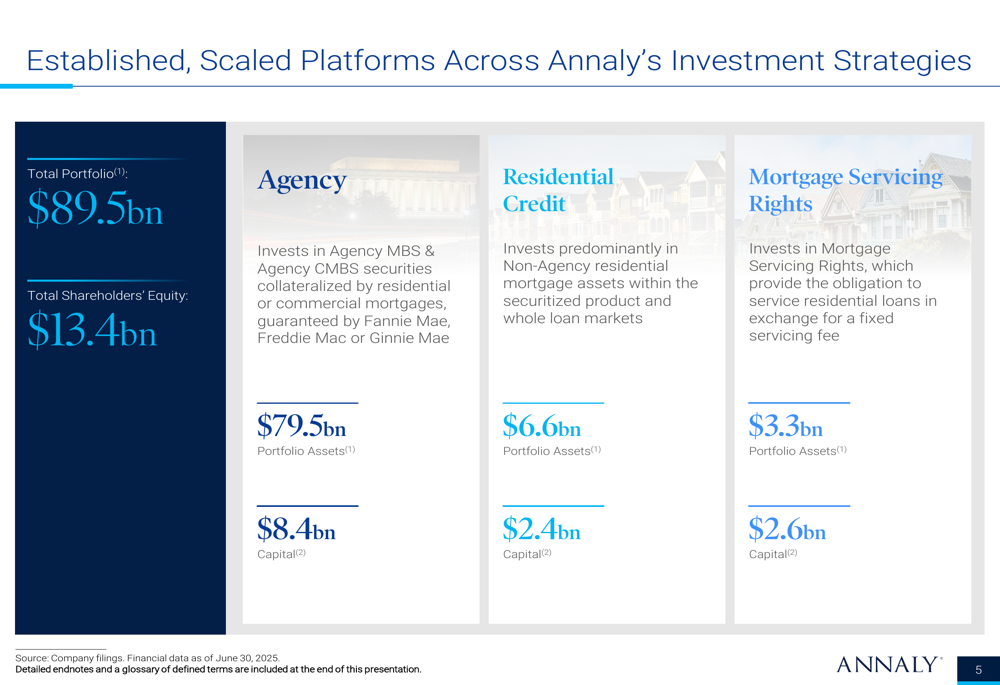

The company’s total portfolio stood at $89.5 billion at quarter-end, with Agency MBS representing 89% of total assets and 62% of dedicated capital. Notably, the Agency portfolio increased by 6% during the quarter, while the Residential Credit and MSR portfolios remained unchanged at $6.6 billion and $3.3 billion, respectively.

Strategic Positioning Across Investment Platforms

Annaly continues to operate across three distinct investment strategies, each with its own risk-return profile and market dynamics. The company’s established platforms demonstrate its scale and diversification approach:

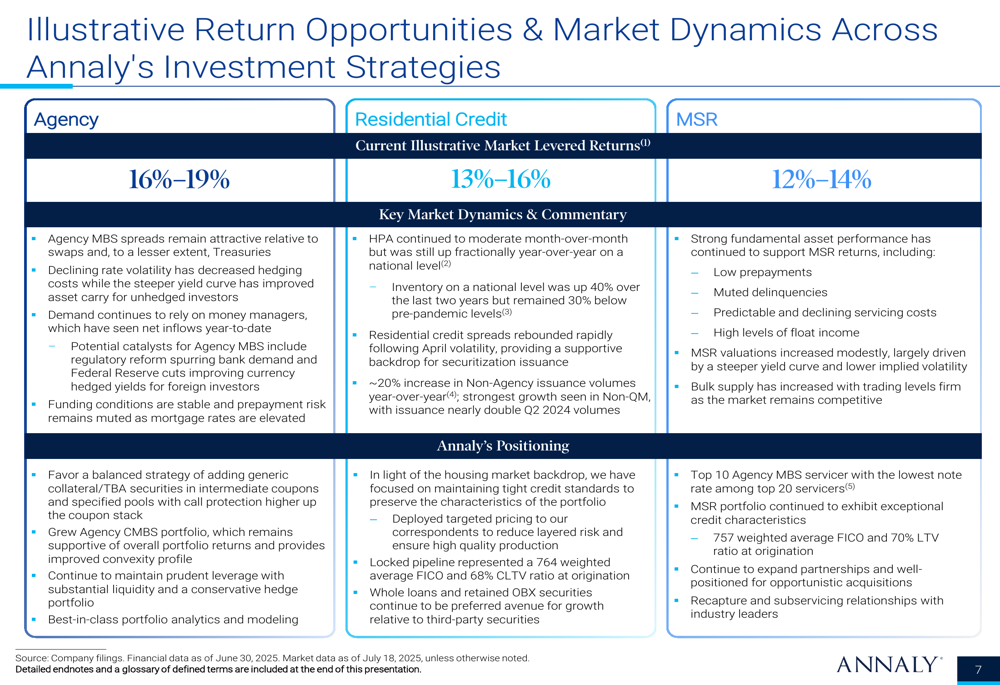

In the current market environment, Annaly sees attractive return opportunities across all three strategies. Agency MBS offers the highest illustrative market levered returns at 16%-19%, supported by attractive spreads, decreased rate volatility, and demand from money managers. Residential Credit offers returns of 13%-16%, while MSR provides returns of 12%-14%.

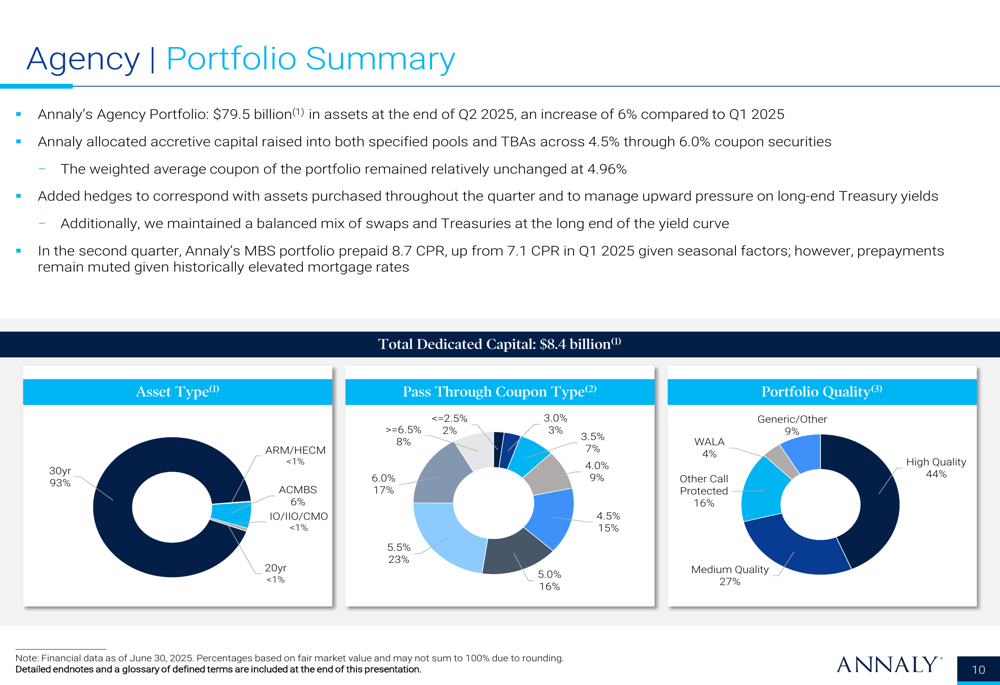

The Agency business segment remains Annaly’s largest, with $79.5 billion in assets and $8.4 billion in dedicated capital. The company maintained its overweight position in Agency MBS due to robust relative returns while keeping leverage low and liquidity ample. The portfolio quality remains high with a weighted average coupon of 4.96%.

Detailed Financial Analysis

Annaly’s financial performance showed mixed results in Q2 2025. While EAD remained strong at $0.73 per share, GAAP earnings declined to just $0.03 per share, down from previous quarters. This significant difference between GAAP and EAD metrics highlights the impact of mark-to-market adjustments on the company’s reported results.

The company’s net interest margin (excluding premium amortization adjustment) improved slightly to 1.71% from 1.69% in Q1 2025. Similarly, the average yield on interest-earning assets increased to 5.41% from 5.23%. However, the average economic cost of funds also rose to 3.94% from 3.88%, partially offsetting the yield improvement.

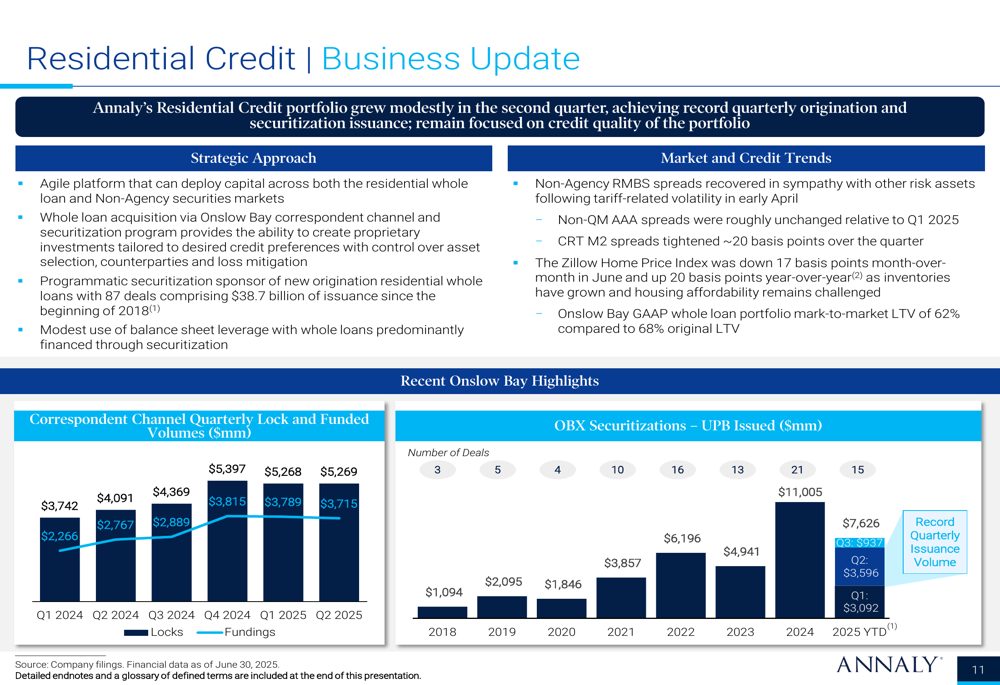

Annaly’s Residential Credit business achieved record quarterly origination and securitization issuance while maintaining focus on credit quality. The company settled $4.1 billion in whole loans and priced 15 securitizations totaling $7.6 billion, establishing itself as the largest non-bank issuer of Prime Jumbo & Expanded Credit MBS.

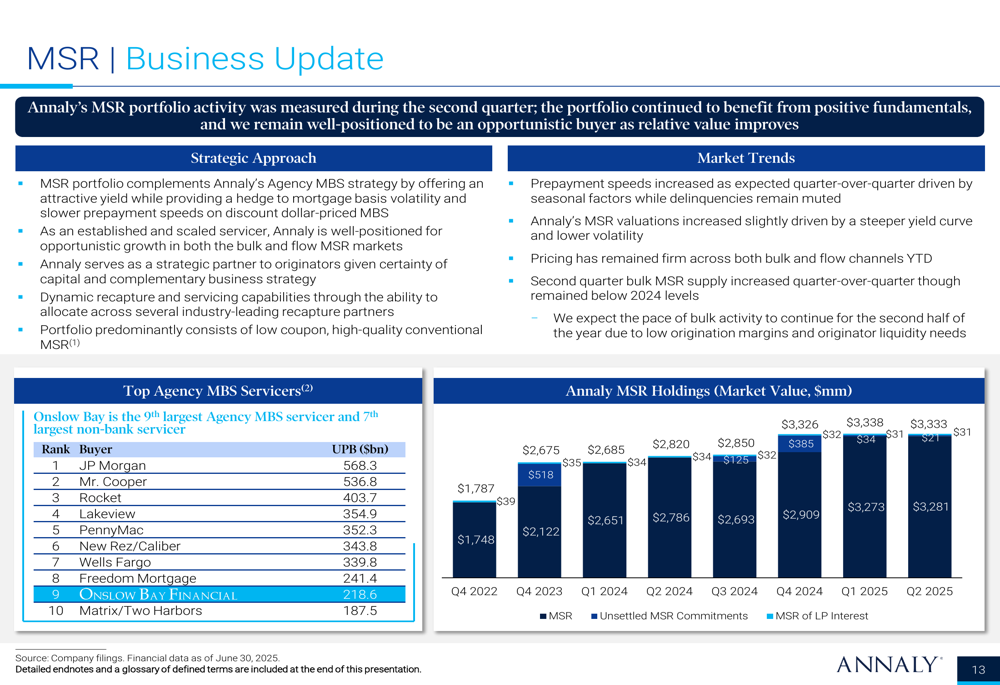

The MSR portfolio, valued at $3.3 billion with dedicated capital of $2.6 billion, saw measured activity during the second quarter. The portfolio continues to benefit from positive fundamentals, including its significantly out-of-the-money position and exceptional credit characteristics. Onslow Bay committed to purchase $30 million in market value ($2 billion in UPB) during the quarter.

Macroeconomic Context and Forward Outlook

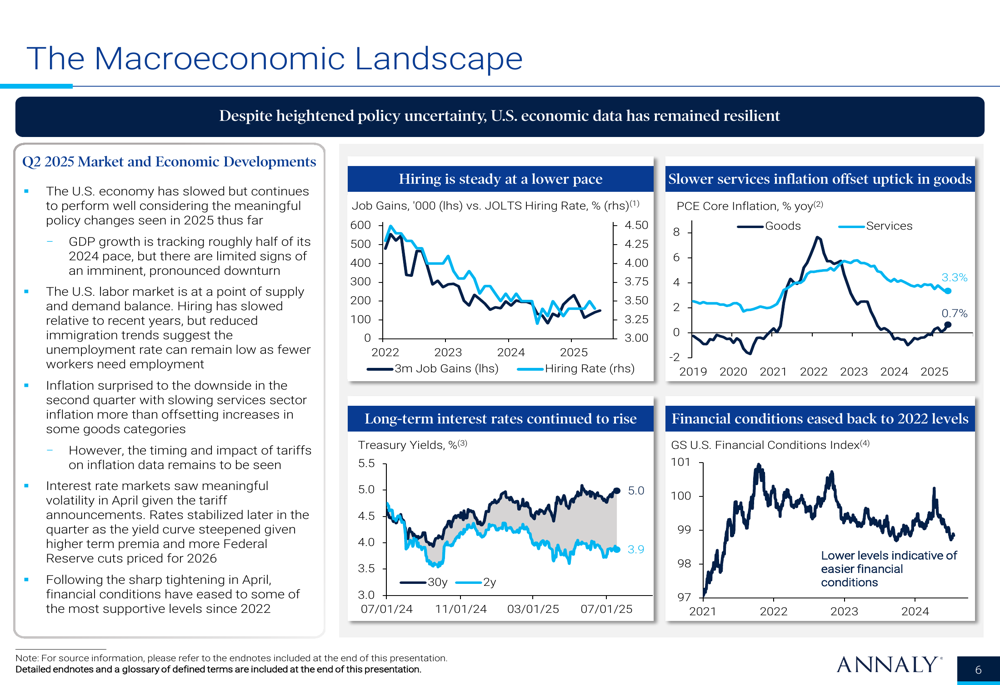

Annaly’s presentation highlighted that despite heightened policy uncertainty, U.S. economic data has remained resilient. The economy has slowed but continues to perform well, with GDP growth tracking at roughly half of its 2024 pace. The labor market appears to be at a point of supply and demand balance, while inflation surprised to the downside in the second quarter.

Looking ahead, Annaly appears well-positioned to navigate the current market environment. The company maintains a strong liquidity position with $4.7 billion in cash and unencumbered Agency MBS, providing flexibility to capitalize on market opportunities. With total assets available for financing of $7.4 billion and a total hedge portfolio of $72 billion, Annaly has taken steps to mitigate interest rate risk.

The company’s interest rate and MBS spread sensitivity analysis suggests a relatively balanced portfolio with manageable exposure to market movements. This positioning aligns with management’s previous statements about maintaining a cautious approach to leverage due to market volatility.

In after-hours trading following the earnings release, Annaly’s stock price increased by 0.39% to $20.48, suggesting a cautiously positive market reaction to the results. The stock remains within its 52-week range of $16.60 to $22.11, indicating relative stability despite the challenging market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.