Trump administration authorizes CIA for covert action in Venezuela - Bloomberg

Introduction & Market Context

Anora Group Oyj (HEL:ANORA) reported its second quarter 2025 results on August 15, showing a continued sales decline but improved gross margins as the Nordic alcoholic beverage company navigates challenging market conditions. The company maintained its full-year guidance despite acknowledging that current performance levels are "not sufficient."

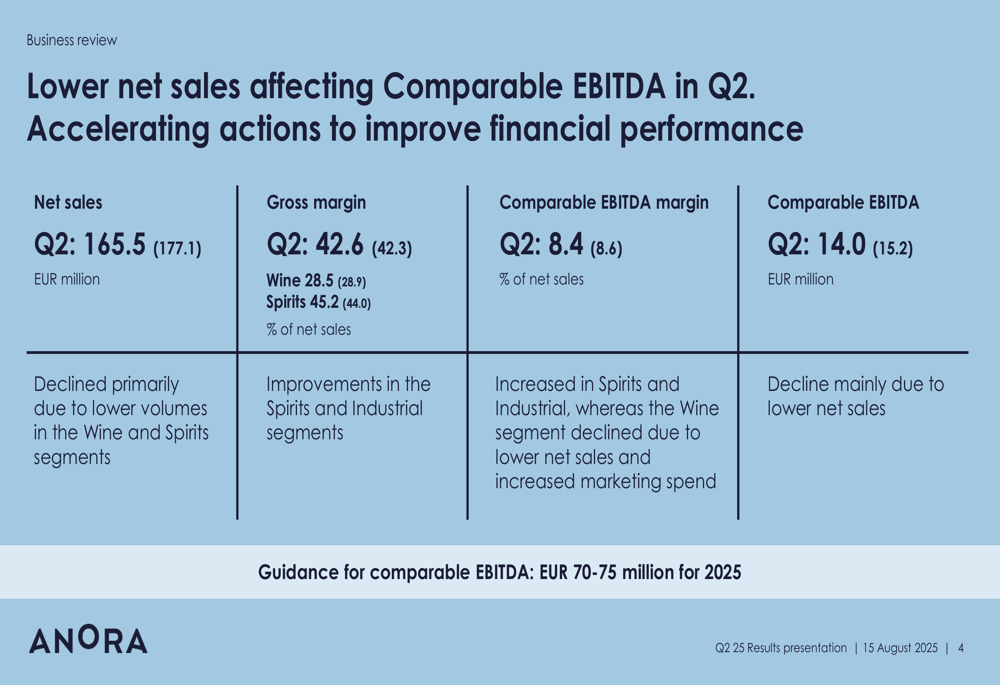

The Q2 results presentation revealed net sales of €165.5 million, down 6.6% from €177.1 million in the same period last year, with the decline primarily attributed to lower volumes in the Wine and Spirits segments. This represents a steeper decline compared to the 3.8% drop reported in Q1 2025, indicating worsening sales trends.

Quarterly Performance Highlights

Anora’s comparable EBITDA for Q2 2025 was €14.0 million (8.4% of net sales), down from €15.2 million (8.6%) in Q2 2024. Despite the overall revenue decline, the company achieved a gross margin of 42.6%, a 30 basis point improvement from 42.3% in the same period last year.

As shown in the following financial results summary, the company’s performance across key metrics shows a mixed picture of challenges and improvements:

The company highlighted several positive developments during the quarter, including market share growth for wines in Sweden by 0.9 percentage points, strong performance of the Koskenkorva brand with double-digit growth in liqueurs, and the launch of operations in Lithuania, securing Anora’s presence across Baltic countries.

Segment Analysis

Anora’s business is divided into three main segments: Wine, Spirits, and Industrial. All segments showed varying performance in Q2 2025.

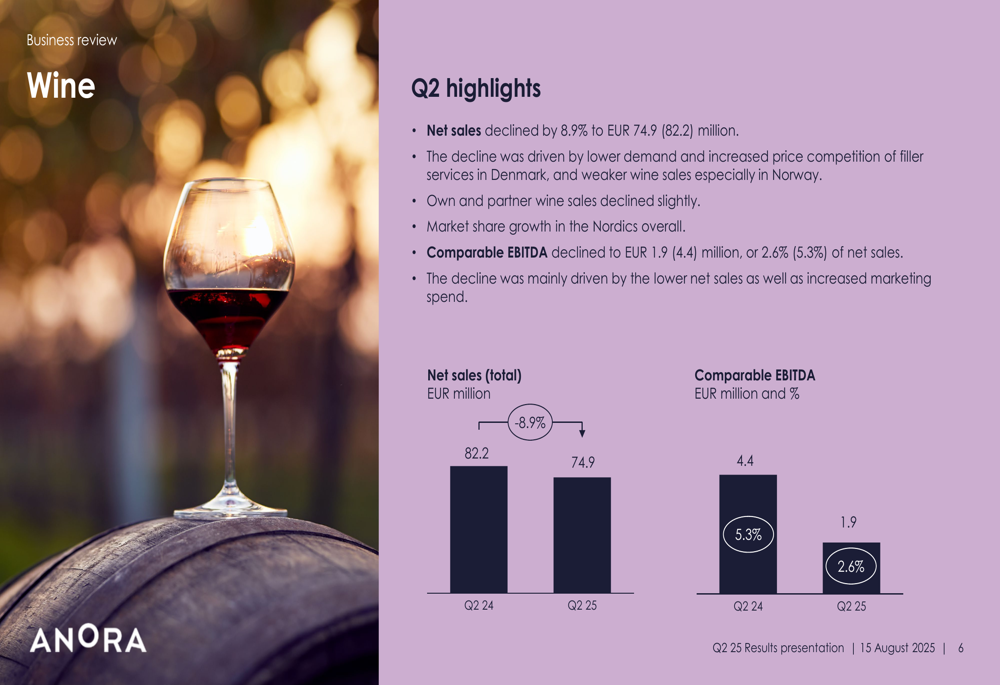

The Wine segment experienced an 8.9% decline in net sales to €74.9 million, driven by lower demand and increased price competition in filler services in Denmark, as well as weaker wine sales in Norway. Comparable EBITDA for the segment fell to €1.9 million (2.6% of net sales) from €4.4 million (5.3%) in Q2 2024, impacted by both lower sales and increased marketing spend.

As shown in the Wine segment performance chart:

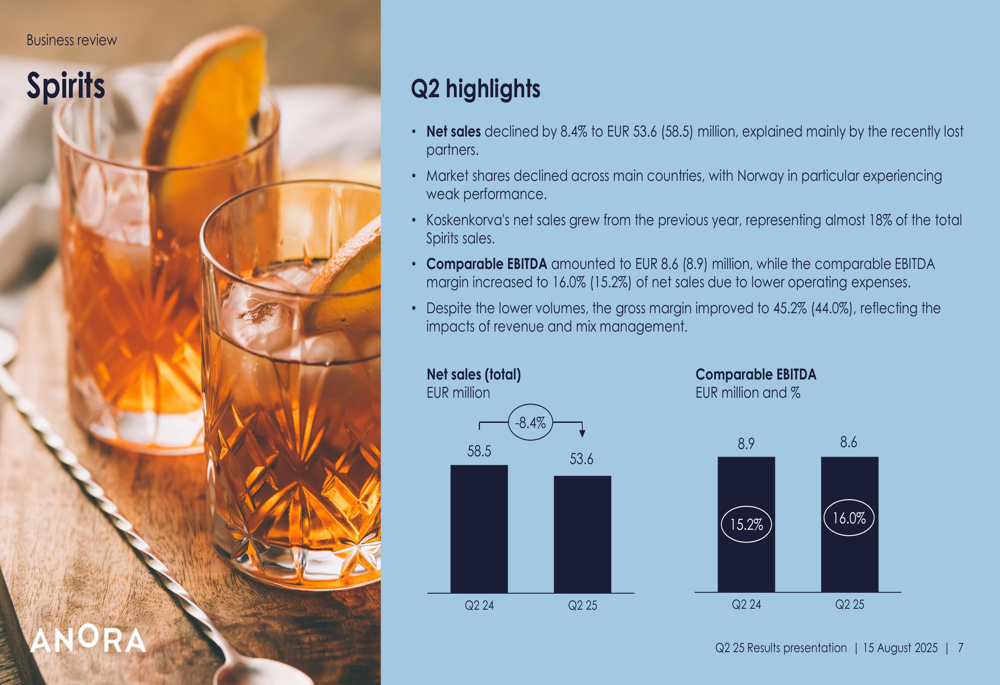

The Spirits segment saw net sales decline by 8.4% to €53.6 million, primarily due to recently lost partners. Despite this, the segment’s comparable EBITDA margin improved to 16.0% from 15.2% in the previous year, thanks to lower operating expenses. The company noted that Koskenkorva’s net sales grew from the previous year, representing almost 18% of total Spirits sales.

The following chart illustrates the Spirits segment performance:

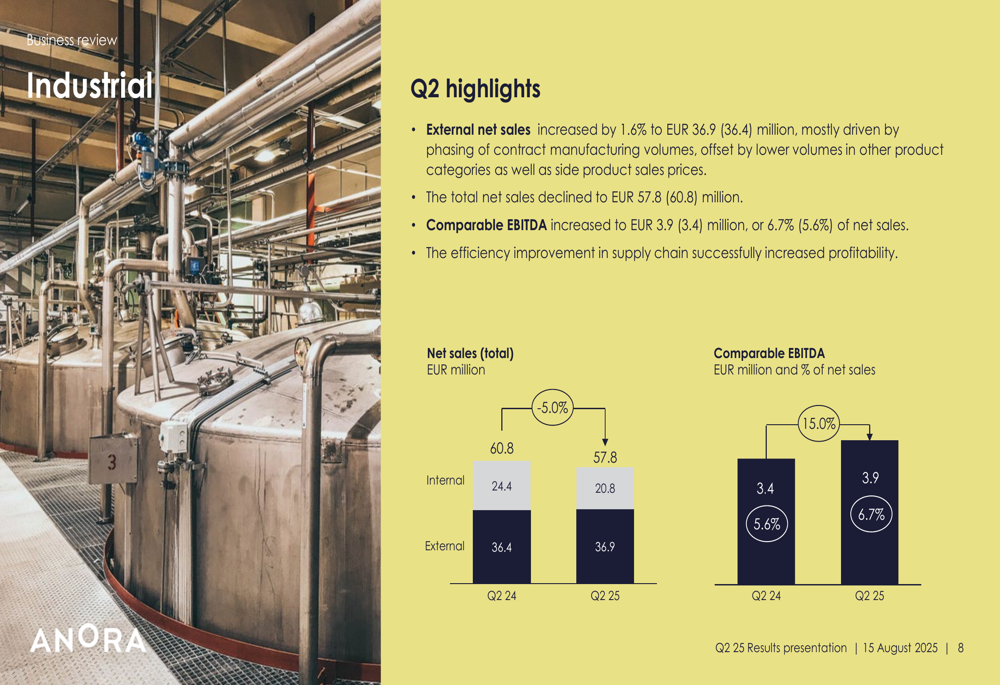

In contrast to the other segments, the Industrial segment showed some positive momentum, with external net sales increasing by 1.6% to €36.9 million. Comparable EBITDA improved to €3.9 million (6.7% of net sales) from €3.4 million (5.6%), with the company attributing this to efficiency improvements in the supply chain.

The Industrial segment performance is visualized here:

Financial Position

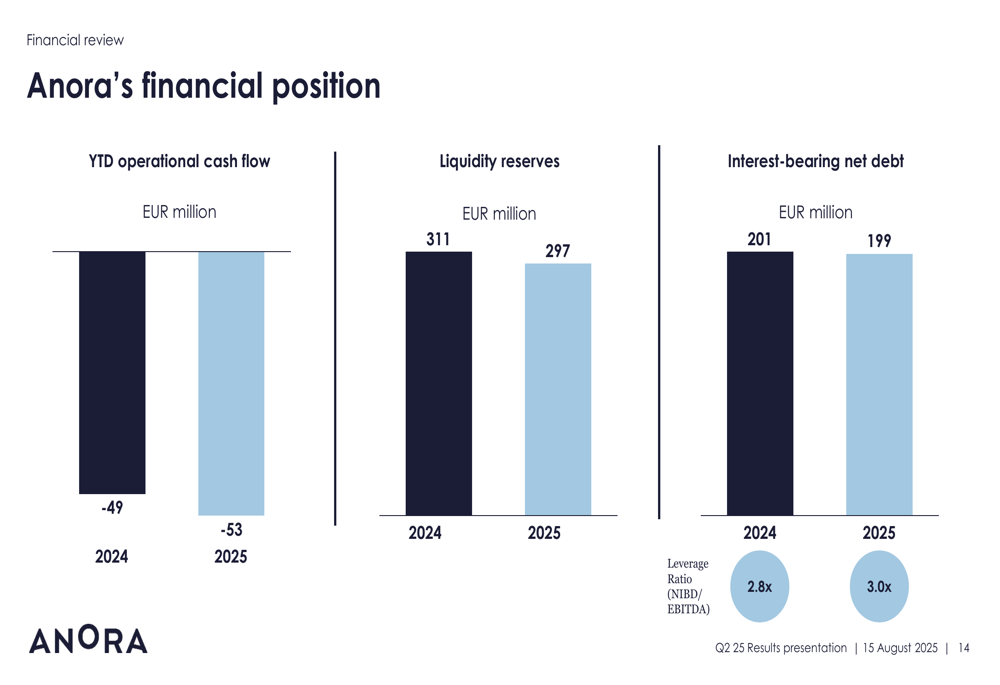

Anora’s financial position remained relatively stable, with net interest-bearing debt at €199 million, slightly down from €201 million in the previous year. However, the leverage ratio (NIBD/EBITDA) increased to 3.0x from 2.8x last year, reflecting the impact of lower EBITDA.

The company’s liquidity reserves stood at €297 million, compared to €311 million last year. Inventory levels decreased by €20.1 million, which the company attributed to improvements in the Industrial segment and reduction of partner inventory in both Wine and Spirits segments.

The following chart provides an overview of Anora’s financial position:

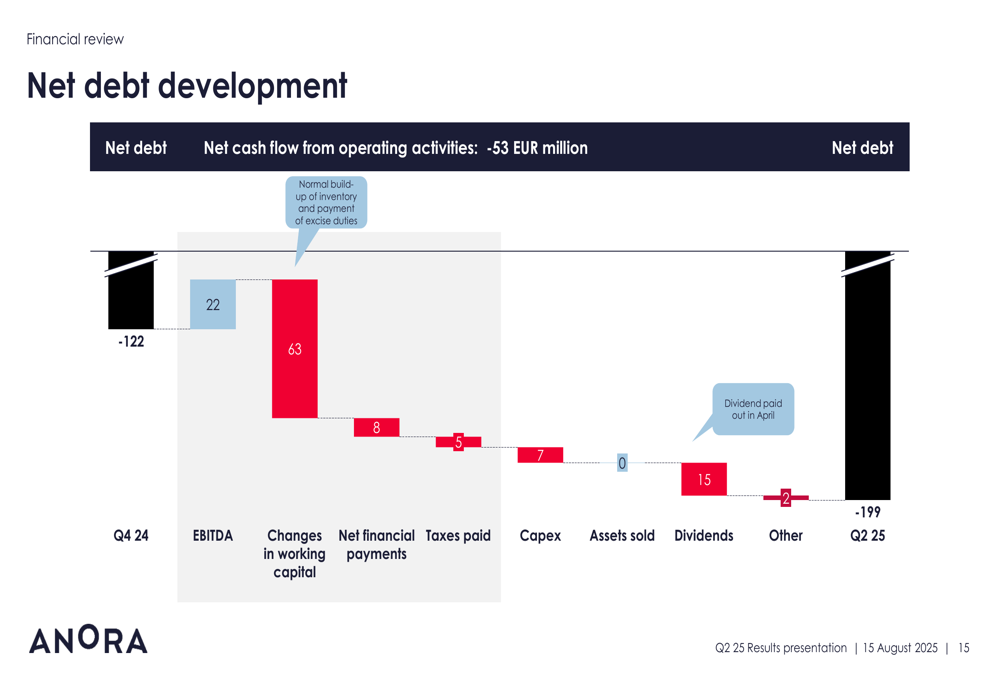

The company’s net debt development is illustrated in this waterfall chart, showing the various factors affecting the debt level:

CEO’s Strategic Outlook

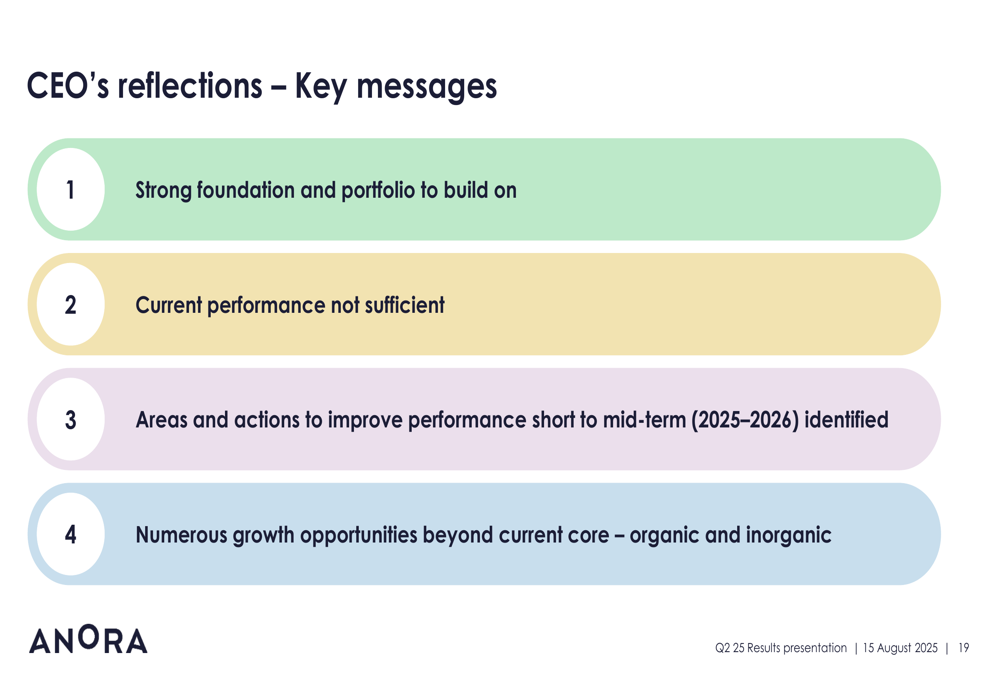

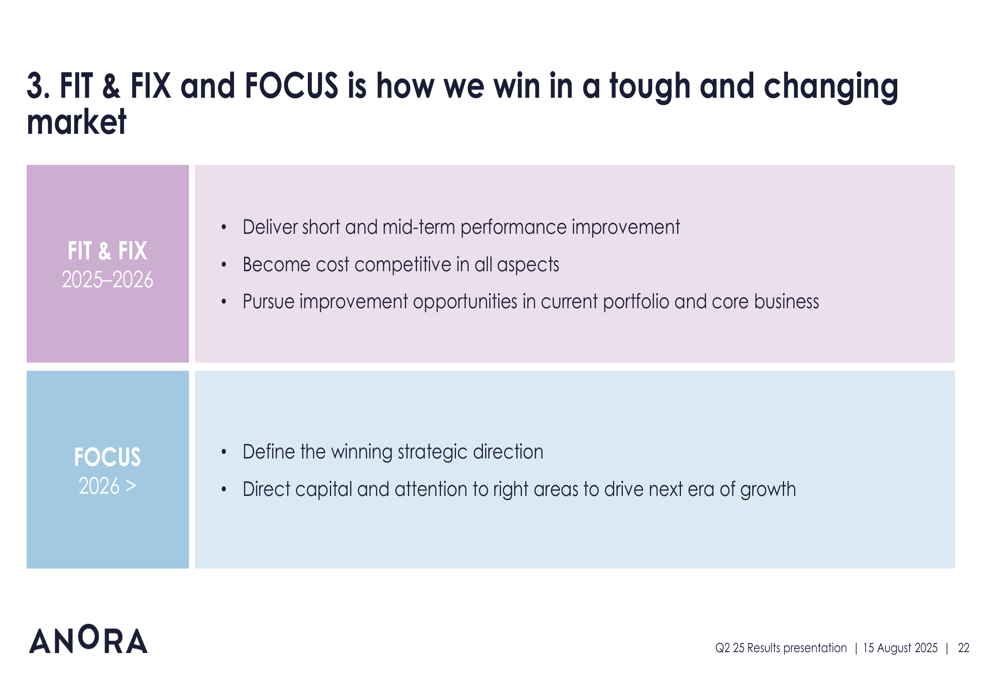

In her reflections, CEO Kirsi Puntila acknowledged that Anora’s current performance is "not sufficient" despite having a strong foundation and portfolio to build on. She outlined a two-phase strategic approach to address the challenges:

1. "FIT & FIX" for 2025-2026: Focused on delivering short and mid-term performance improvement, becoming cost competitive in all aspects, and pursuing improvement opportunities in the current portfolio and core business.

2. "FOCUS" for 2026 and beyond: Aimed at defining the winning strategic direction and directing capital and attention to the right areas to drive the next era of growth.

The CEO’s key messages are summarized in this slide:

Puntila identified several internal challenges, including overcapacity in the industrial system, cost levels not adjusting fast enough, untapped synergies from previous mergers, and incomplete product presence in key assortments. External challenges include slow growth of underlying demand, challenged monopoly channels, changing consumer behaviors, and a faster pace of innovation.

The company’s strategic approach is outlined as follows:

Forward-Looking Statements

Despite the challenges, Anora maintained its full-year guidance for comparable EBITDA of €70-75 million for 2025. The company announced it will hold a Capital Markets Day on November 5, 2025, where it plans to elaborate further on its strategic direction through 2028.

The company is also undertaking several operational initiatives, including a SAP implementation project to consolidate all operations into a single ERP system (expected completion in late Q4 2025), enhanced Power BI capabilities, a new cash management system, and legal entity streamlining.

In the near term, management is focused on cost competitiveness, operational efficiency, portfolio optimization, inventory and revenue management, accelerated product launches, and balance sheet efficiency as part of its "FIT & FIX" program.

As the company navigates these challenges, investors will be watching closely to see if the strategic initiatives can reverse the sales decline while maintaining the positive momentum in gross margins. The upcoming Capital Markets Day in November will be a crucial event for understanding Anora’s longer-term strategy and growth prospects in a challenging Nordic alcoholic beverage market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.