Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Antero Resources (NYSE:AR) presented its first quarter 2025 earnings results on May 1, highlighting operational efficiencies and strategic positioning despite falling short of analyst expectations. The natural gas producer reported earnings per share of $0.66, missing forecasts by $0.11, while revenue came in at $1.35 billion versus an expected $1.38 billion. Despite these misses, the company’s stock experienced only a minor decline of 0.29% following the announcement, suggesting investor confidence in Antero’s long-term strategy.

Operational Highlights

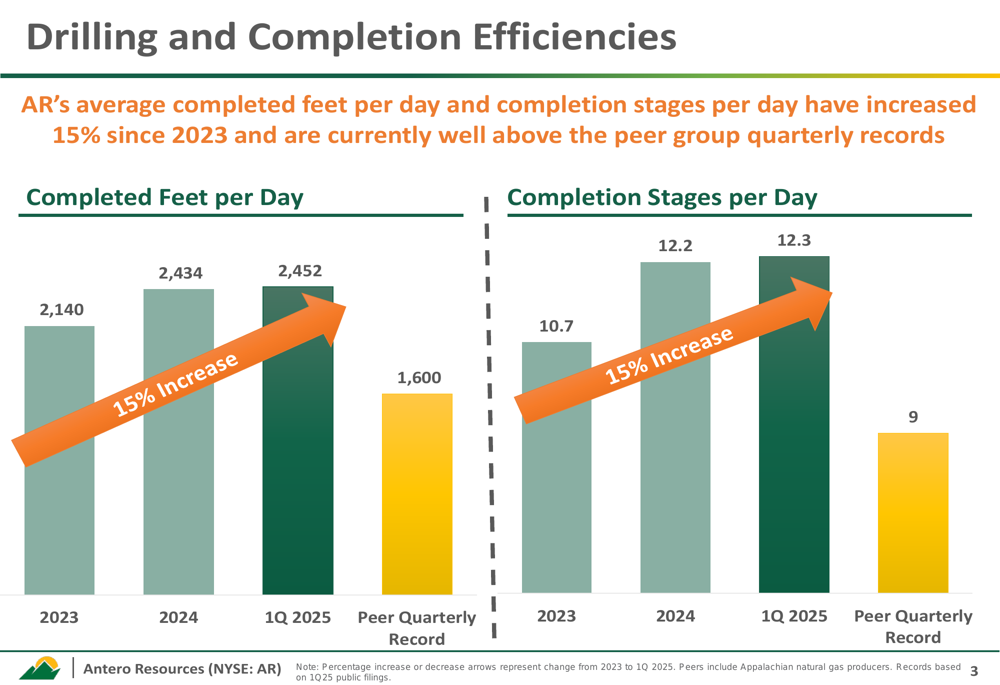

Antero showcased significant improvements in drilling and completion efficiencies, achieving a 15% increase from 2023 to Q1 2025. The company completed 2,452 feet per day in the first quarter, substantially outperforming the peer quarterly record of 1,600 feet per day. Similarly, completion stages per day reached 12.3 in Q1 2025, compared to the peer record of 9 stages.

As shown in the following chart of drilling and completion efficiencies:

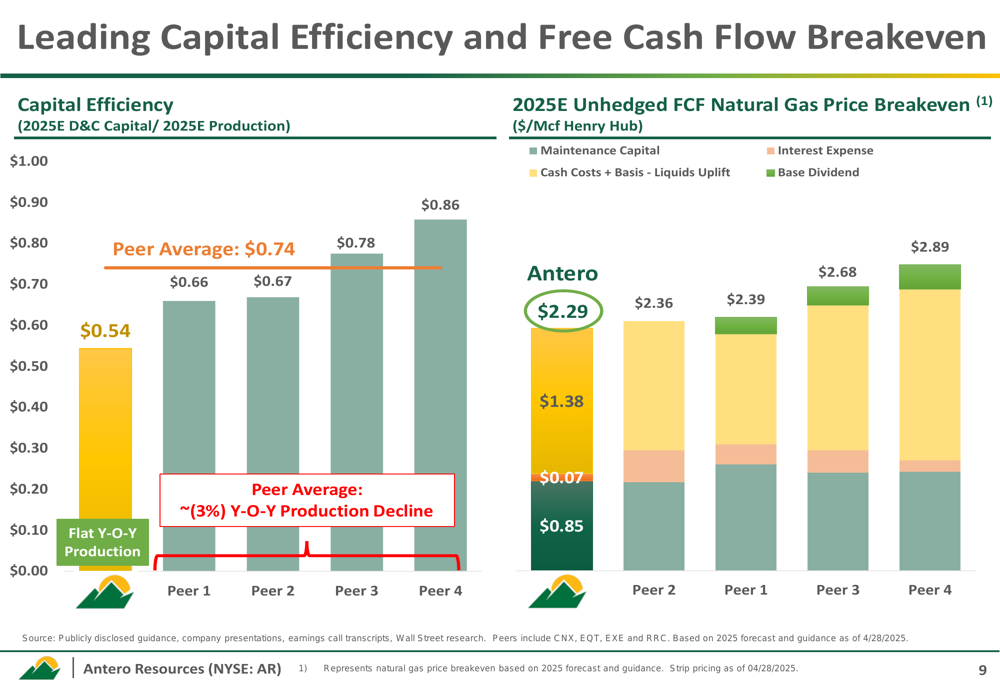

These operational improvements have contributed to Antero’s superior capital efficiency, with 2025E D&C capital per unit of production at $0.54, compared to the peer average of $0.74. The company has maintained flat year-over-year production, while peers are experiencing an average 3% decline.

The following chart illustrates Antero’s capital efficiency advantage and competitive breakeven price:

Financial Performance

Antero generated $336.6 million in free cash flow before changes in working capital during Q1 2025, enabling significant debt reduction and share repurchases. The company reported that it reduced debt by over $200 million in the quarter and repurchased $92 million in stock, representing nearly 1% of shares outstanding.

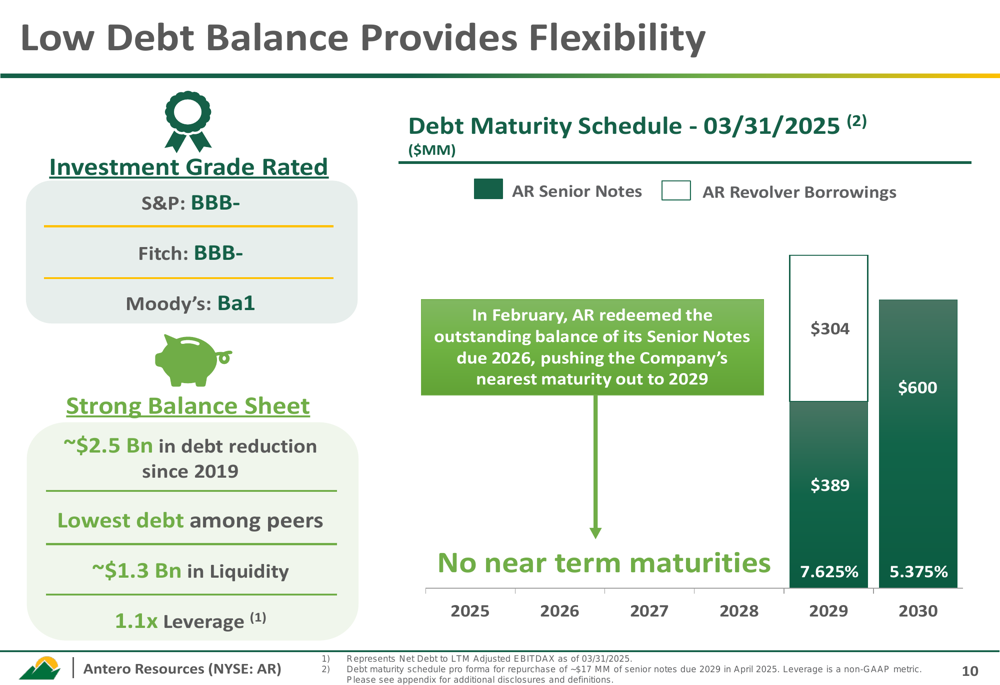

The company’s balance sheet strength is evident in its low leverage ratio of 1.1x and $1.3 billion in liquidity as of March 31, 2025. Antero has achieved a total debt reduction of $2.5 billion since 2019 and maintains investment-grade ratings from S&P and Fitch (BBB-).

The following slide demonstrates Antero’s debt profile and financial flexibility:

Strategic Positioning

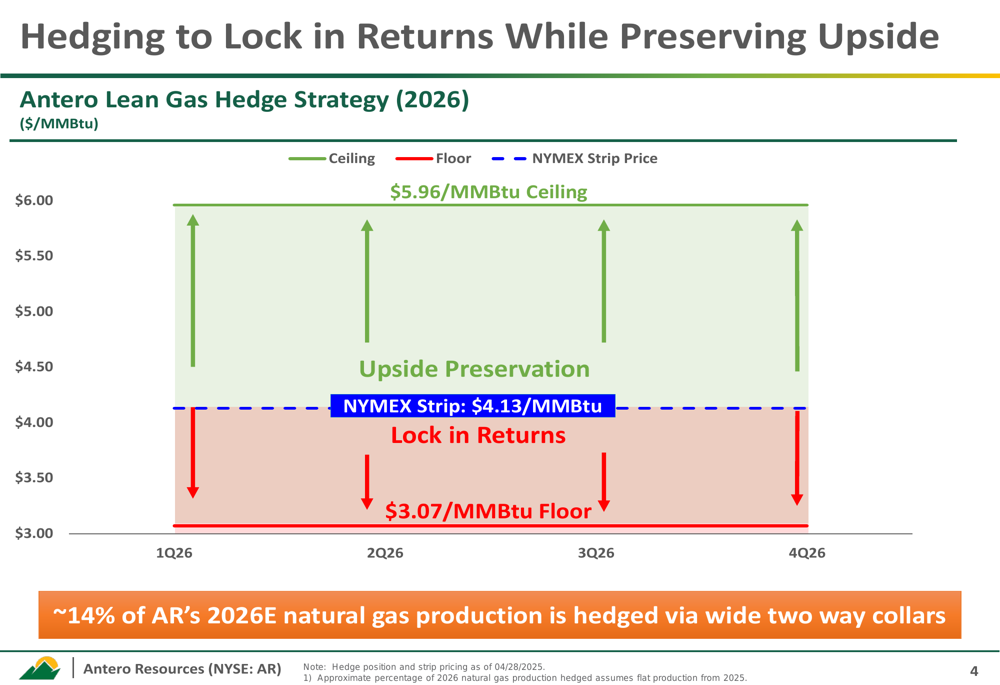

Antero has implemented a strategic hedging program for 2026 that provides downside protection while preserving upside potential. The company has hedged approximately 14% of its 2026 estimated natural gas production with wide two-way collars, establishing a floor price of $3.07/MMBtu and a ceiling of $5.96/MMBtu.

As illustrated in this hedging strategy chart:

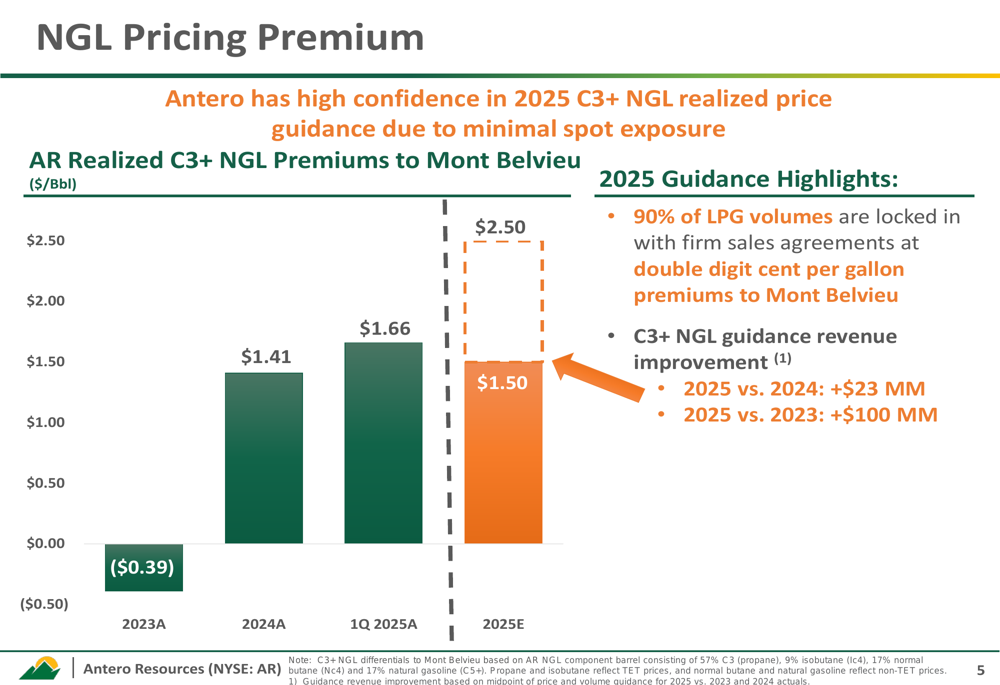

A key competitive advantage for Antero is its improving NGL pricing premiums. The company’s realized C3+ NGL premium to Mont Belvieu has increased from -$0.39/Bbl in 2023 to $1.66/Bbl in Q1 2025, with 2025 guidance projecting a premium of $2.50/Bbl. This improvement is expected to generate an additional $23 million in revenue compared to 2024 and $100 million compared to 2023.

The following chart shows the positive trend in NGL pricing premiums:

Antero is also strategically positioned to benefit from growing natural gas demand driven by data center expansion in the Midwest and Eastern United States. The company highlighted significant investments by tech giants including Amazon (NASDAQ:AMZN) ($7.8 billion in Central Ohio), Meta (NASDAQ:META) ($800 million in Wood County, Ohio), and Competitive Power Ventures ($3 billion in West Virginia).

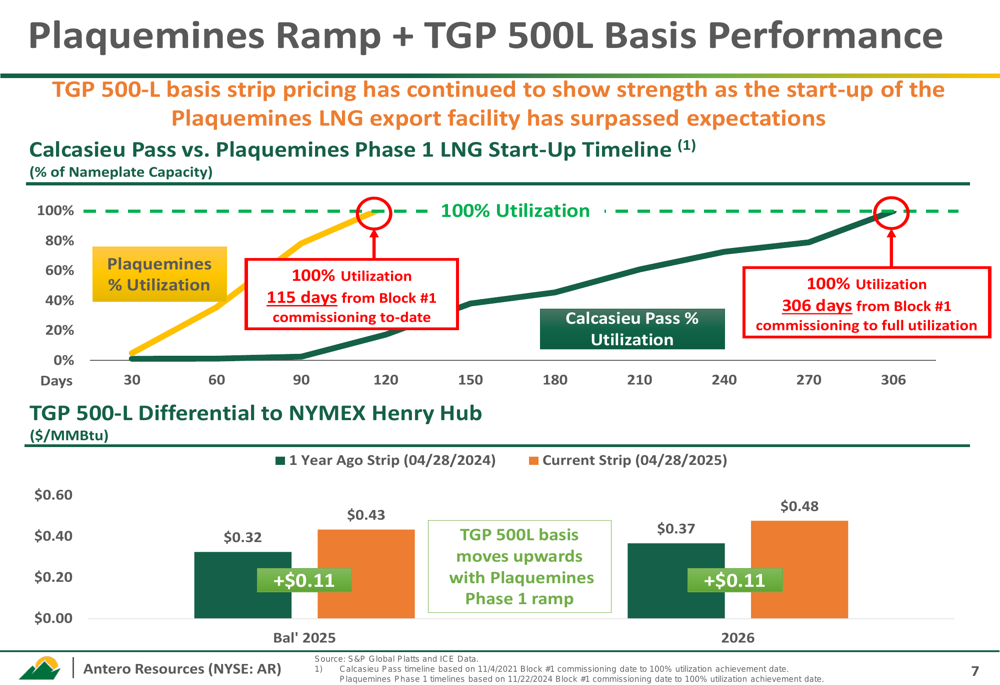

The rapid ramp-up of LNG export facilities, particularly the Plaquemines facility which reached 100% utilization in just 115 days compared to 306 days for Calcasieu Pass, further supports Antero’s market outlook. This accelerated timeline suggests stronger-than-expected demand for LNG exports.

As shown in this chart of the Plaquemines ramp and basis performance:

Forward Outlook

Antero maintained its 2025 production guidance of 3.35-3.45 Bcfe/d, with natural gas production of 2.16-2.20 Bcf/d and C3+ NGL production of 113,000-117,000 Bbl/d. The company projects cash production expenses of $2.45-$2.55/Mcfe and D&C capital expenditures of $650-700 million.

During the earnings call, CFO Mike Kennedy expressed optimism about the natural gas market, stating, "We’ve never really seen a better setup from a natural gas demand growth over the coming quarters, years versus supply." He also reaffirmed the company’s commitment to shareholder value through continued share repurchases.

With an unhedged free cash flow breakeven natural gas price of $2.29/Mcf for 2025, Antero is well-positioned to generate positive returns even in a challenging price environment. The company’s focus on operational efficiency, strategic marketing of NGLs, and financial discipline provides a solid foundation for navigating market volatility while delivering shareholder value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.