Tyson Foods to close major Nebraska beef plant amid cattle shortage - WSJ

Introduction & Market Context

Antero Resources (NYSE:AR) presented its second quarter 2025 earnings results on July 31, highlighting significant operational efficiency improvements and strategic positioning in the natural gas market. Despite reporting strong financial results, including $262 million in free cash flow, the stock fell 2.54% in aftermarket trading to $31.81, suggesting investors may have expected even stronger performance or reacted to broader market trends.

The natural gas producer operates in a market anticipating substantial demand growth, with approximately 8 Bcf/d of new LNG export capacity expected between 2025 and 2027, alongside increasing regional power demand driven by data centers and other infrastructure projects.

Operational Efficiency Highlights

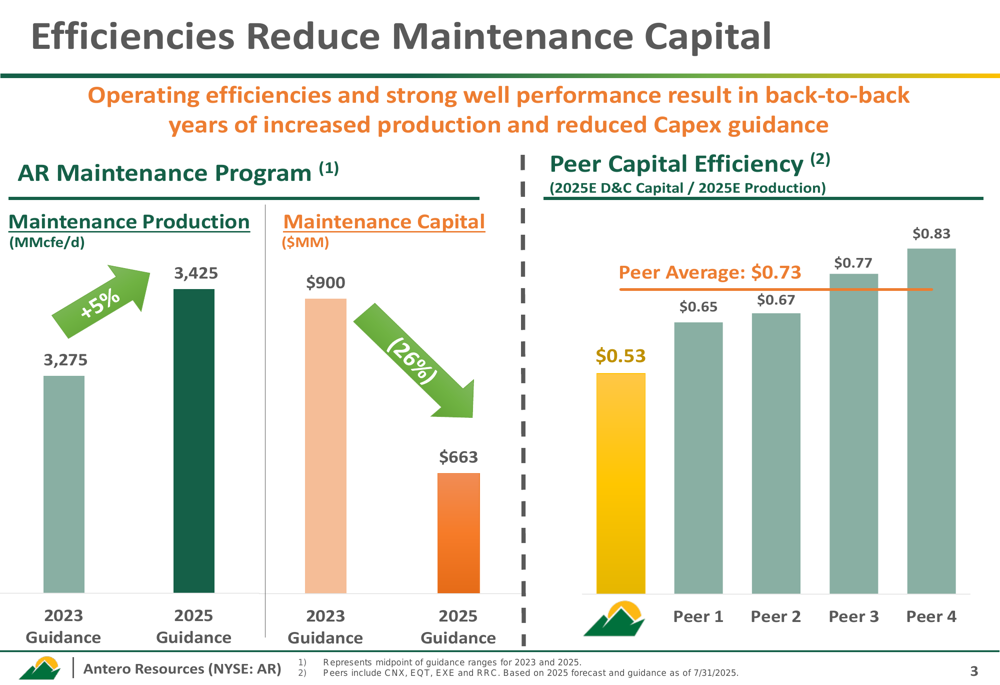

A key focus of Antero's presentation was the company's improved operational efficiency, which has enabled it to reduce capital requirements while increasing production. The company has achieved a 5% increase in maintenance production while simultaneously reducing maintenance capital by 26% compared to 2023 guidance.

As shown in the following chart of maintenance program improvements:

This efficiency gain positions Antero competitively within the industry, though its capital efficiency metric of $0.83 remains slightly higher than the peer average of $0.73. The company compares its performance against peers including CNX, EQT, EXE, and RRC based on 2025 forecasts.

Strategic Market Positioning

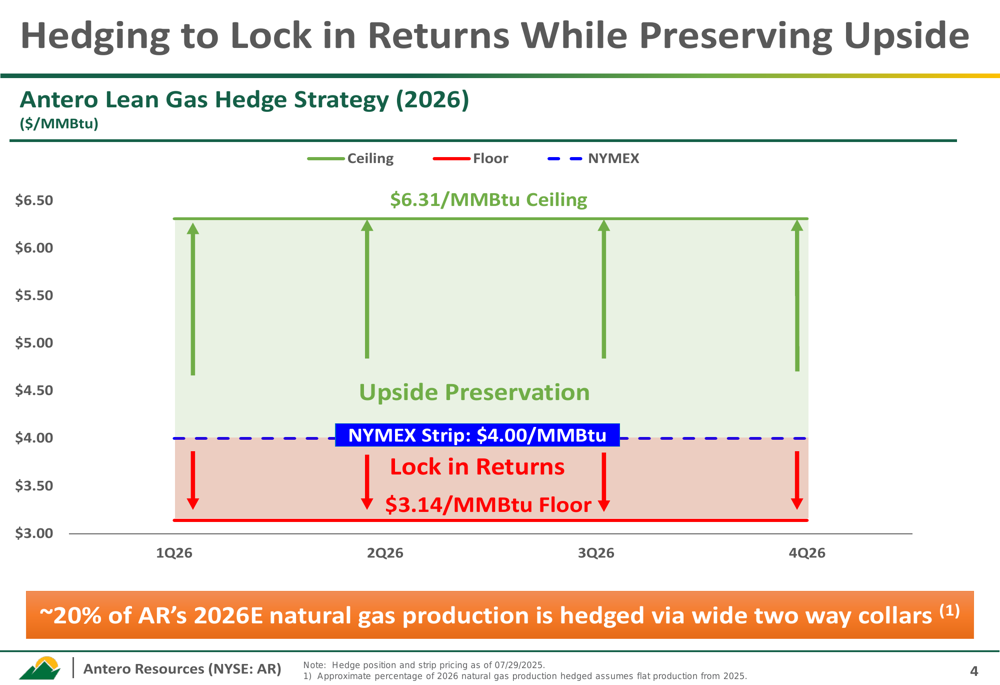

Antero has implemented a strategic hedging approach to lock in returns while preserving upside potential. For 2026, the company has hedged approximately 20% of its expected natural gas production using wide two-way collars with a ceiling of $6.31/MMBtu and a floor of $3.14/MMBtu, compared to the current NYMEX strip of $4.00/MMBtu.

The following chart illustrates this hedging strategy:

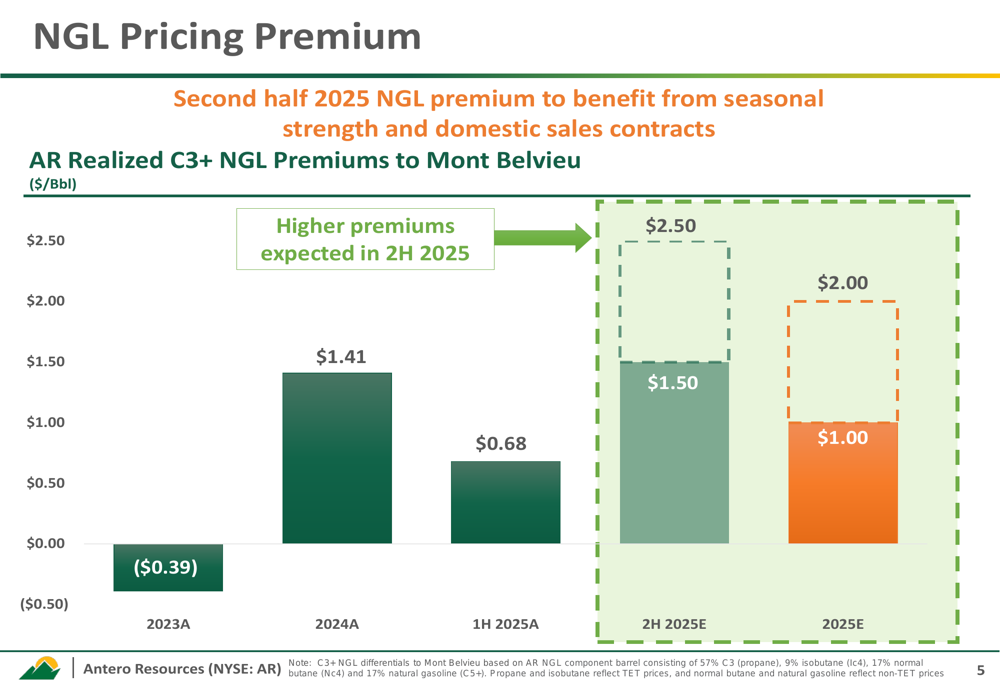

The company also highlighted its advantageous position regarding NGL (natural gas liquids) pricing, with expected premiums to Mont Belvieu benchmark prices. After realizing a $0.68/Bbl premium in the first half of 2025, Antero projects a $2.50/Bbl premium for the second half of the year, resulting in a full-year 2025 premium of $1.00/Bbl.

The NGL pricing premium trend is illustrated in this chart:

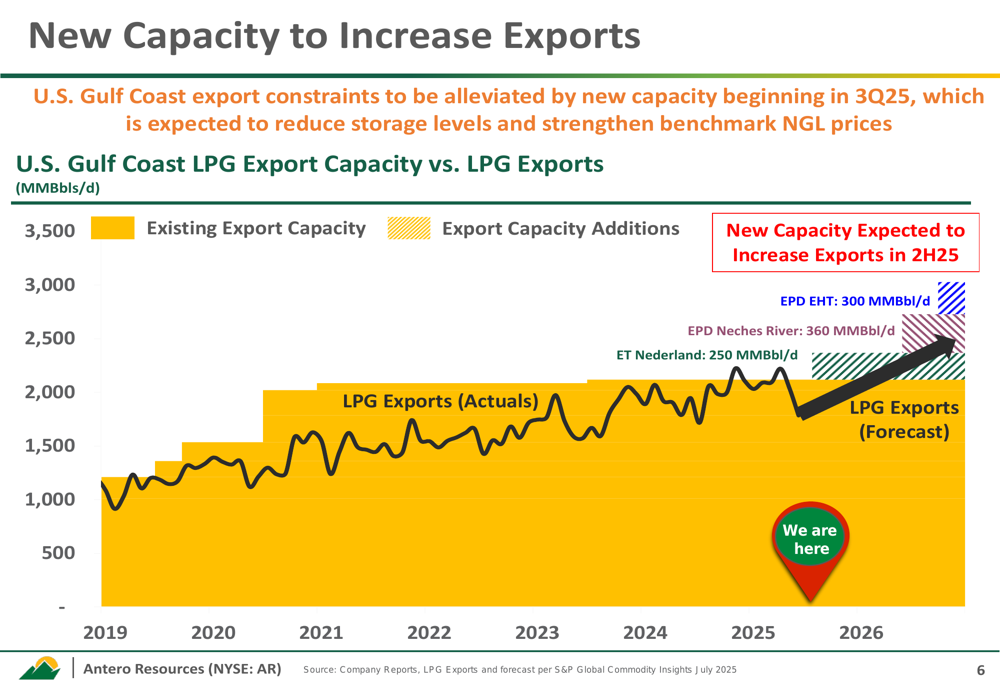

Antero expects to benefit from new Gulf Coast export capacity coming online in the third quarter of 2025, which should alleviate current export constraints and potentially improve pricing. Several major capacity additions are expected, including EPD EHT (300 MMBbl/d), EPD Neches River (360 MMBbl/d), and ET Nederland (250 MMBbl/d).

The following chart shows how these capacity additions relate to export volumes:

Financial Performance

Antero's financial results show substantial year-over-year improvement. The company reported Q2 2025 Adjusted EBITDAX of $379.5 million, a 150% increase from $151.4 million in Q2 2024. Free Cash Flow showed an even more dramatic turnaround, reaching $262.4 million compared to a negative $68.2 million in the same period last year.

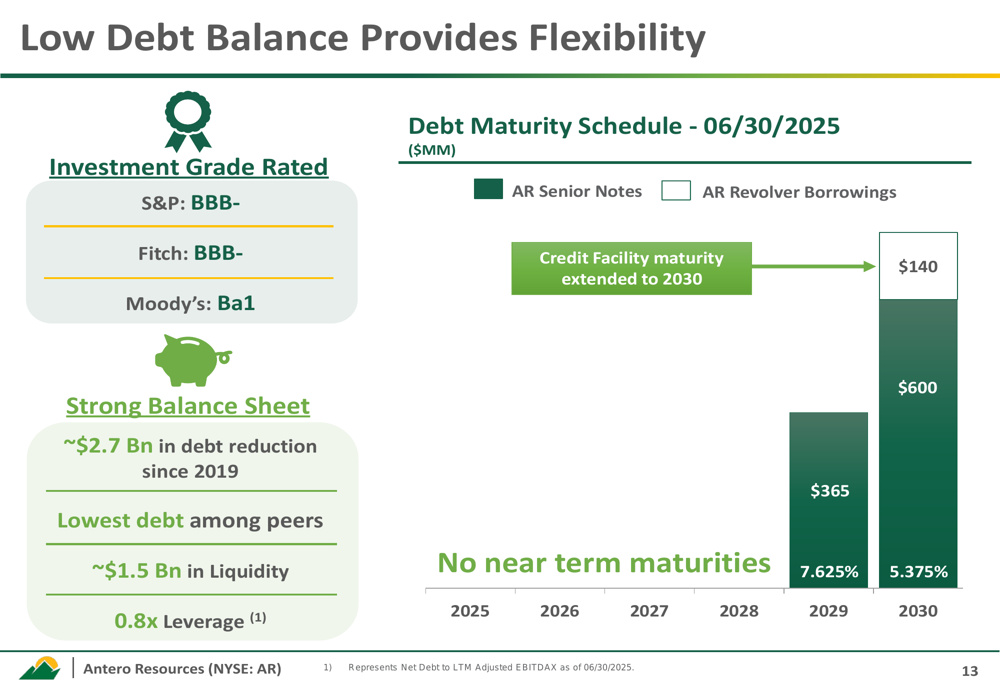

The company has maintained a strong balance sheet, with approximately $2.7 billion in debt reduction since 2019 and a current leverage ratio of 0.8x. Antero holds investment-grade credit ratings from S&P and Fitch (both BBB-) and a Ba1 rating from Moody's.

The debt maturity schedule shows no near-term maturities, with the next significant obligations being $365 million in 2029 (7.625%) and $600 million in 2030 (5.375%). The company has approximately $1.5 billion in liquidity and has extended its credit facility maturity to 2030.

This debt profile is illustrated in the following chart:

Competitive Industry Position

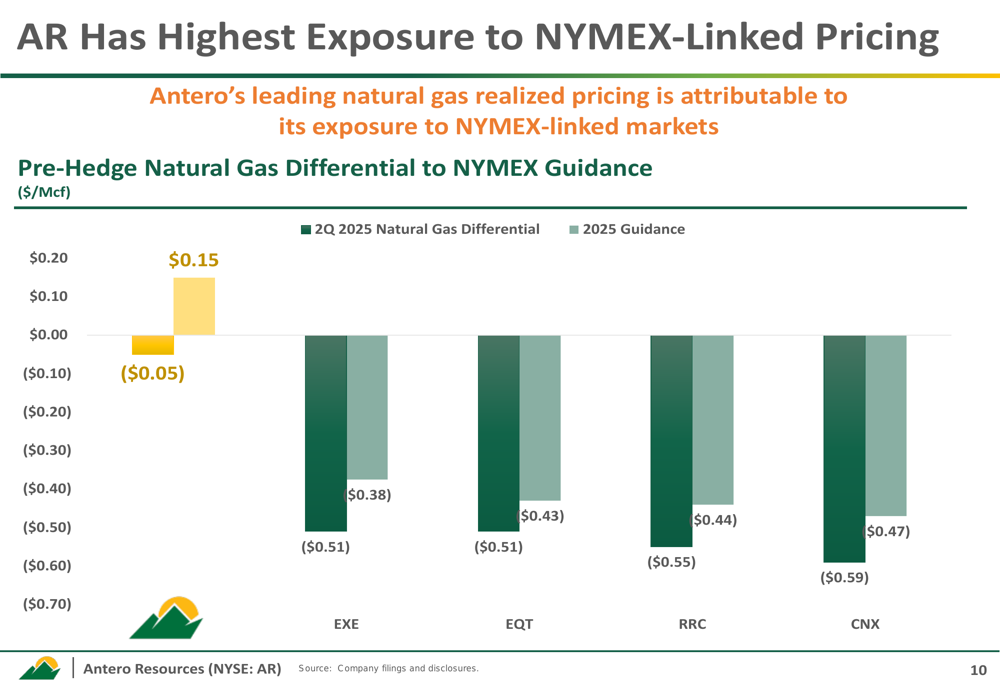

Antero emphasized its advantageous position regarding natural gas pricing differentials compared to peers. For Q2 2025, the company reported a positive differential to NYMEX of $0.15, significantly outperforming peers who reported negative differentials ranging from -$0.38 to -$0.47.

The following chart illustrates Antero's pricing advantage:

This pricing advantage stems partly from Antero's transportation portfolio, with 75% of its 2024 expected production linked to Henry Hub pricing. The company highlighted that 68% of its production has access to Tier 1/TGP 500L transportation, providing more favorable pricing than competitors with less advantageous transportation arrangements.

Forward Outlook

Looking ahead, Antero is positioned to benefit from several market developments:

1. Increasing regional natural gas demand, with approximately 5.0 Bcf/d of new power demand expected between 2026 and 2030+, driven significantly by data center projects.

2. New LNG export capacity additions that should strengthen natural gas pricing, particularly for producers like Antero with favorable transportation arrangements.

3. Continued operational efficiencies that should maintain the company's reduced capital requirements while supporting production levels.

According to the earnings call transcript, CEO Paul Rady emphasized the company's flexibility, noting, "We have over 10 years of dry gas drilling inventory where we could accelerate activity to grow volumes in a short time frame." CFO Michael Kennedy highlighted the company's strategic hedging approach, stating, "We're only 20% hedged but have upside to $7. That was a good trade."

Despite the positive operational and financial metrics presented, investors should note that Antero's stock declined in aftermarket trading following the earnings release. This may reflect broader market concerns about natural gas prices or indicate that investors expected even stronger results. The stock remains within its 52-week range of $25.36 to $44.02, suggesting continued market volatility in the natural gas sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.