EUR/USD likely to find a peak near 1.25: UBS

Introduction & Market Context

A.O. Smith Corporation (NYSE:AOS) released its second quarter 2025 results on July 24, 2025, showing resilience in a challenging market environment. The water technology company’s stock jumped 7.75% following the announcement, as investors responded positively to margin improvements and steady earnings growth despite modest sales declines.

The company maintained its full-year guidance while highlighting its focus on operational excellence, innovation, and strategic portfolio management. This quarter’s performance builds on trends seen in Q1, where the company also exceeded analyst expectations despite facing headwinds in key markets.

Quarterly Performance Highlights

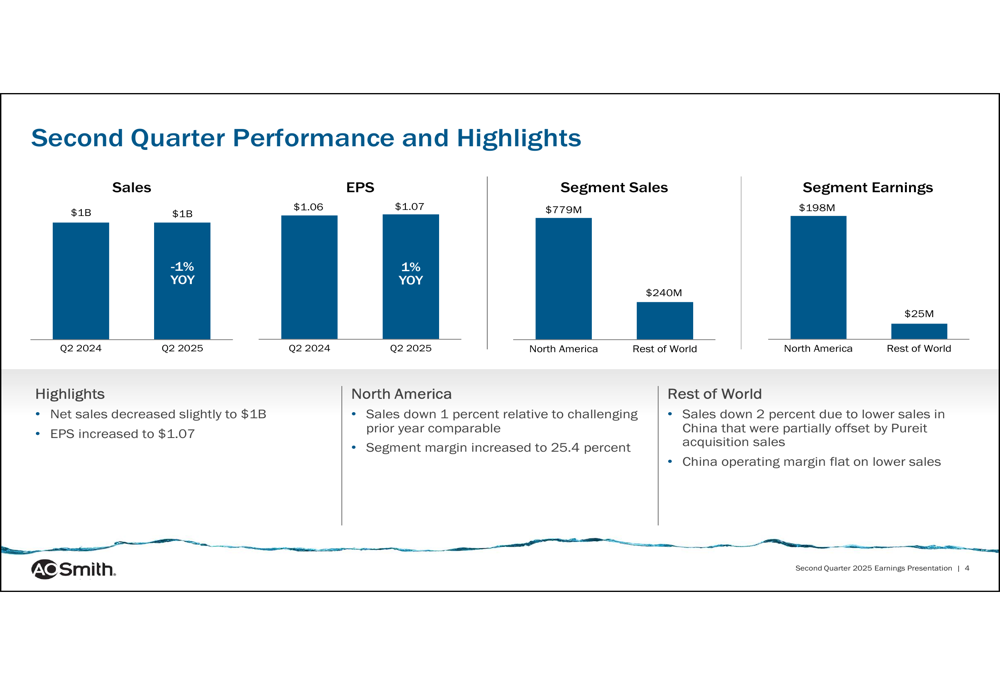

A.O. Smith reported second quarter sales of $1 billion, representing a slight 1% year-over-year decrease, while earnings per share increased 1% to $1.07. The company demonstrated its ability to protect profitability despite volume challenges, particularly in its North American water heater business and continued weakness in China.

As shown in the following quarterly performance summary:

The company’s North America segment generated $779 million in sales and $198 million in earnings, while the Rest of World segment contributed $240 million in sales and $25 million in earnings. These results reflect A.O. Smith’s continued focus on operational efficiency and margin improvement despite challenging market conditions.

Segment Analysis

North America

The North America segment, which remains A.O. Smith’s largest market, saw sales decrease by 1% to $779 million compared to the same period last year. Despite this decline, the segment achieved a margin of 25.4%, an increase of 30 basis points year-over-year. This improvement was primarily driven by a more favorable product mix, with growth in high-efficiency water heaters and a shift toward more profitable channels in water treatment.

The detailed breakdown of North America’s performance is illustrated here:

While water heater volumes declined, boiler sales increased by 6%, demonstrating strength in the commercial and residential heating segment. The company also benefited from favorable steel costs and productivity gains, which helped offset the negative impact of tariffs.

Rest of World

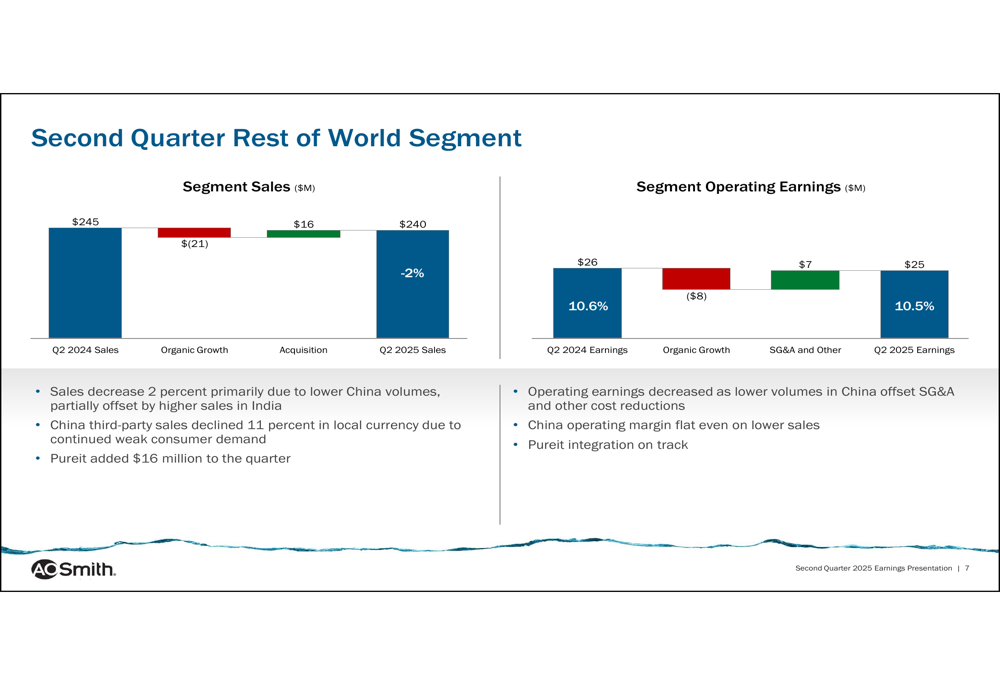

The Rest of World segment, which includes operations in China, India, and other international markets, reported sales of $240 million, a 2% decrease compared to Q2 2024. This decline was primarily due to continued weakness in China, where third-party sales fell 11% in local currency amid persistent weak consumer demand.

The segment’s performance is detailed in the following chart:

Despite the challenging environment in China, A.O. Smith maintained a stable operating margin of 10.5% in this segment, just slightly below the 10.6% achieved in the same period last year. The company noted that the Pureit acquisition contributed $16 million to quarterly sales, helping to partially offset the decline in China. Management also indicated that the Pureit integration remains on track.

Product Innovation and Strategic Initiatives

A.O. Smith continues to emphasize innovation as a key driver of long-term growth. During the quarter, the company introduced several new products designed to address evolving customer needs and regulatory requirements.

The company’s innovation pipeline is highlighted in this product showcase:

Key product introductions include the Adapt™ SC Standard Condensing Tankless water heater featuring industry-first integrated scale prevention technology, the HomeShield™ Whole House Water Filter certified to reduce PFAS to less than 4 ng/L for 500,000 gallons, and the Cyclone® FLEX with AiQ Adaptive Gas Technology for improved efficiency and flexibility.

Additionally, management announced plans to initiate an assessment of the China business to ensure it is well-positioned for future growth, signaling a strategic review of operations in this challenging market.

Financial Position and Capital Allocation

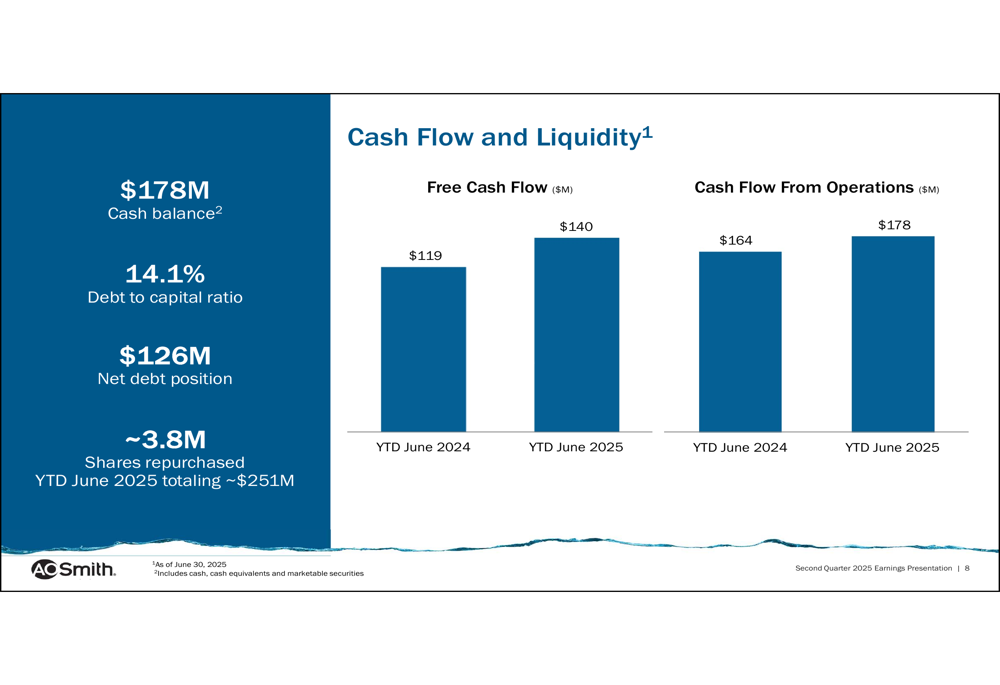

A.O. Smith maintained a strong financial position with $178 million in cash and cash equivalents as of June 30, 2025. The company reported a debt-to-capital ratio of 14.1% and a net debt position of $126 million, reflecting its conservative financial management approach.

Free cash flow improved to $140 million for the first half of 2025, compared to $119 million in the same period last year, as shown in this cash flow summary:

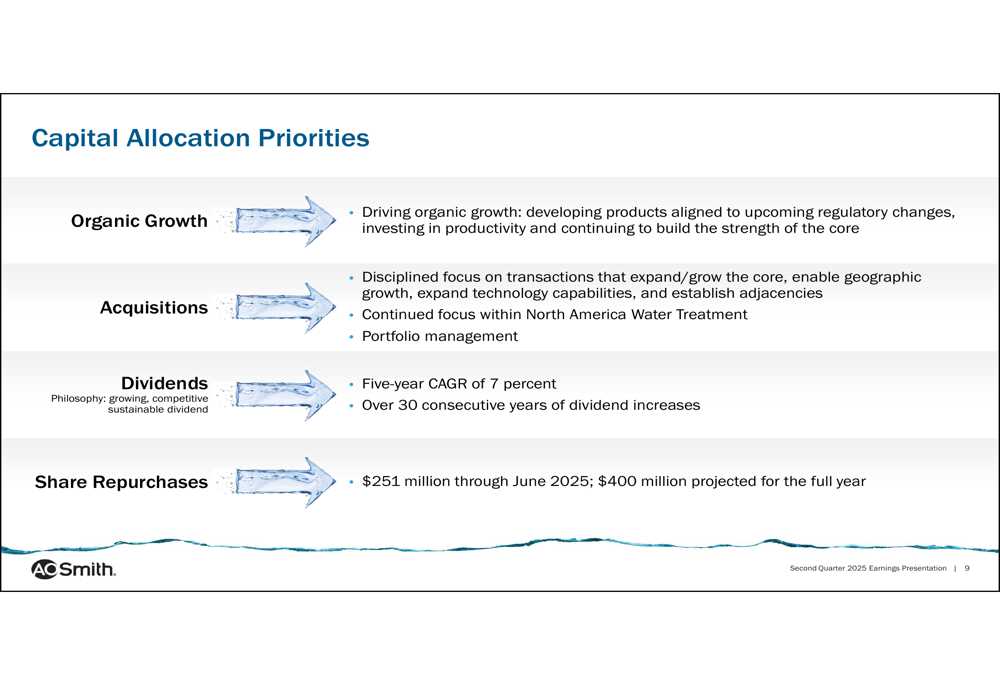

The company continues to prioritize shareholder returns, repurchasing approximately 3.8 million shares year-to-date for a total of $251 million. A.O. Smith projects total share repurchases of $400 million for the full year 2025. The company also highlighted its track record of over 30 consecutive years of dividend increases, with a five-year dividend CAGR of 7%.

The capital allocation strategy is outlined in this framework:

2025 Outlook and Forward-Looking Statements

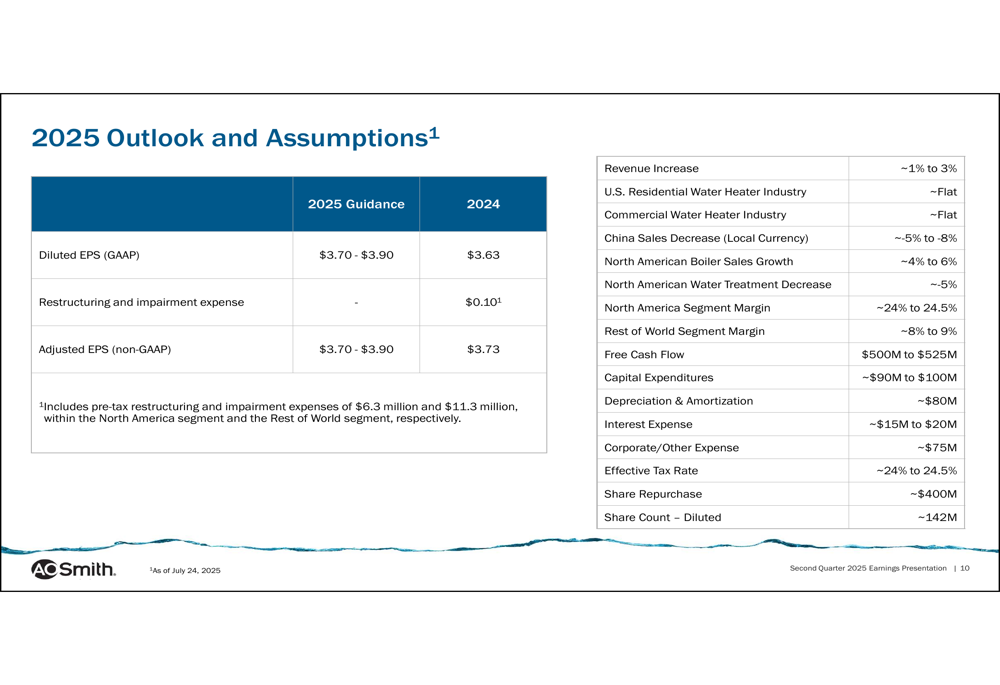

A.O. Smith maintained its full-year 2025 guidance, projecting earnings per share of $3.70 to $3.90 and revenue growth of approximately 1% to 3%. The company expects North America segment margins to range between 24% and 24.5%, while Rest of World segment margins are projected at 8% to 9%.

The detailed outlook is presented in this comprehensive guidance table:

Management anticipates flat industry conditions for both residential and commercial water heaters in the United States. For China, the company projects a sales decrease of 5% to 8% in local currency, reflecting continued market challenges. Conversely, North American boiler sales are expected to grow by 4% to 6%, while North American water treatment sales are projected to decrease by approximately 5%.

The company expects to generate free cash flow of $500 million to $525 million for the full year, with capital expenditures ranging from $90 million to $100 million. A.O. Smith plans to maintain its focus on operational excellence, innovation, and strategic portfolio management to drive long-term value creation despite near-term market challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.