Gold prices tick higher on fresh US tariff threats, Fed rate cut hopes

Introduction & Market Context

Appian Corporation (NASDAQ:APPN) released its first quarter 2025 earnings presentation on May 8, highlighting continued growth in cloud subscription revenue alongside positive adjusted EBITDA. The low-code automation platform provider, led by Founder and CEO Matt Calkins and Interim CFO Mark Lynch, emphasized its strategic positioning at the intersection of process automation and artificial intelligence.

The company’s stock has experienced volatility in recent trading, with shares down 0.85% in the previous session to $30.41, and showing additional pressure in premarket trading with a 2.01% decline to $29.80. Appian’s shares currently trade well below their 52-week high of $43.33, reflecting ongoing market challenges for growth-oriented technology companies.

Quarterly Performance Highlights

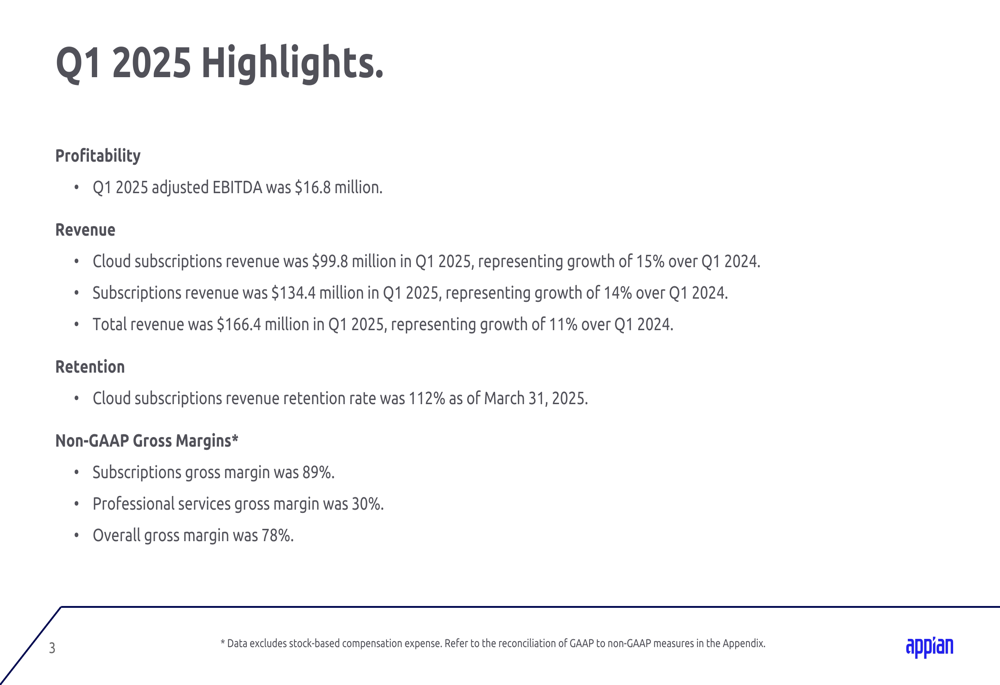

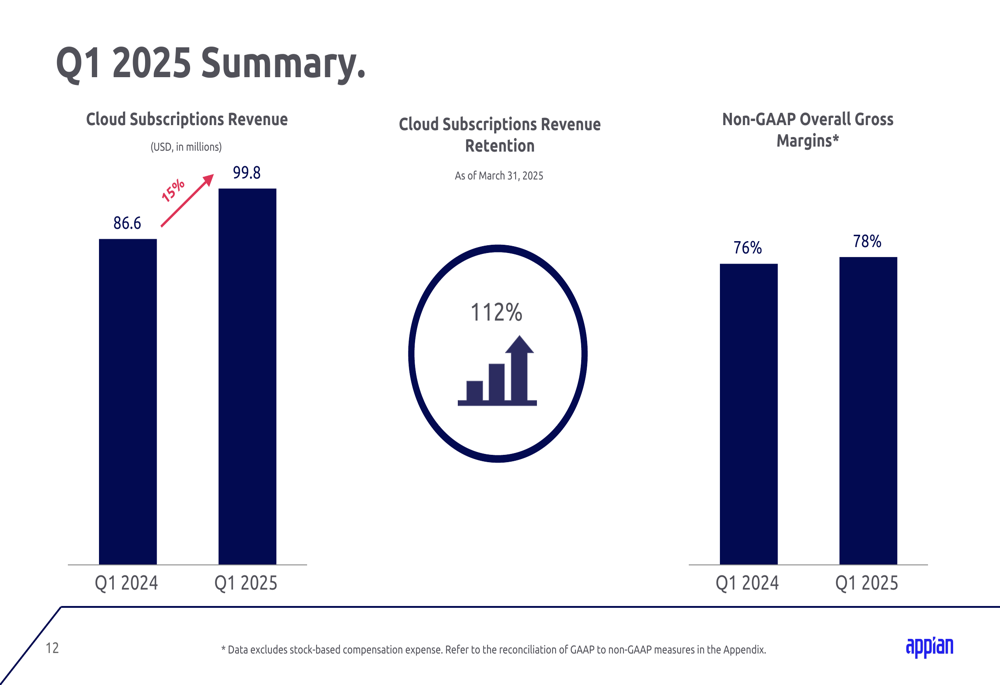

Appian reported solid financial results for Q1 2025, with cloud subscriptions revenue growing 15% year-over-year to $99.8 million. Total (EPA:TTEF) subscriptions revenue, which includes term licenses, increased 14% to $134.4 million, while total revenue rose 11% to $166.4 million compared to the same period last year.

The company achieved an adjusted EBITDA of $16.8 million for the quarter, demonstrating improved operational efficiency. Gross margins remained strong, with subscriptions gross margin at 89%, professional services gross margin at 30%, and overall gross margin at 78%.

As shown in the following chart of quarterly performance metrics:

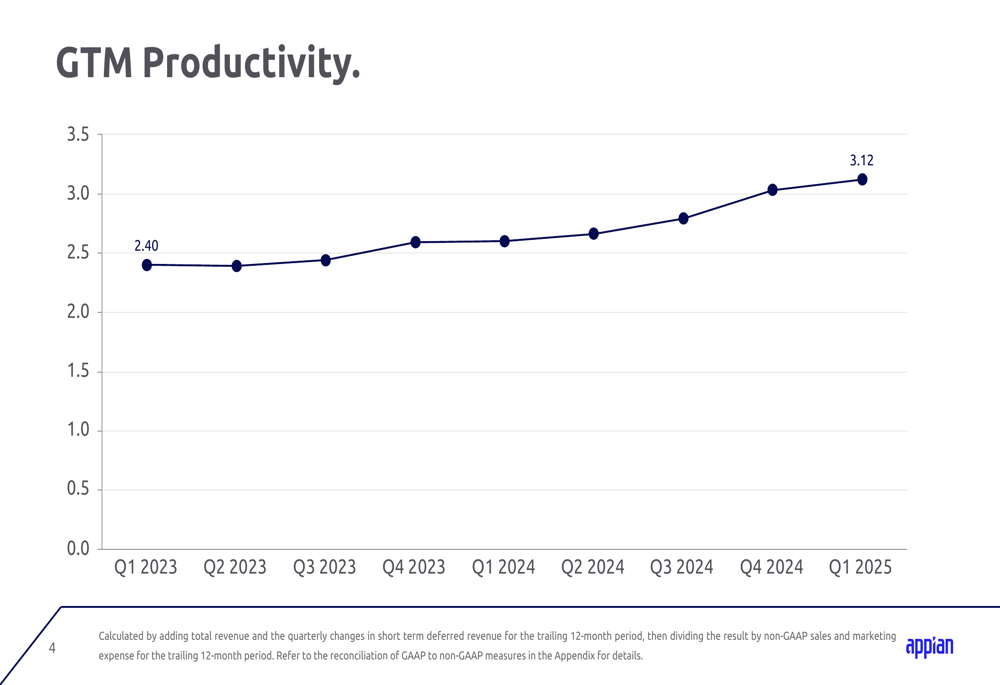

The company’s go-to-market efficiency has shown consistent improvement over the past two years, with GTM productivity (calculated as trailing 12-month revenue plus change in short-term deferred revenue divided by non-GAAP sales and marketing expense) increasing from 2.40 in Q1 2023 to 3.12 in Q1 2025.

Customer Retention and Revenue Mix

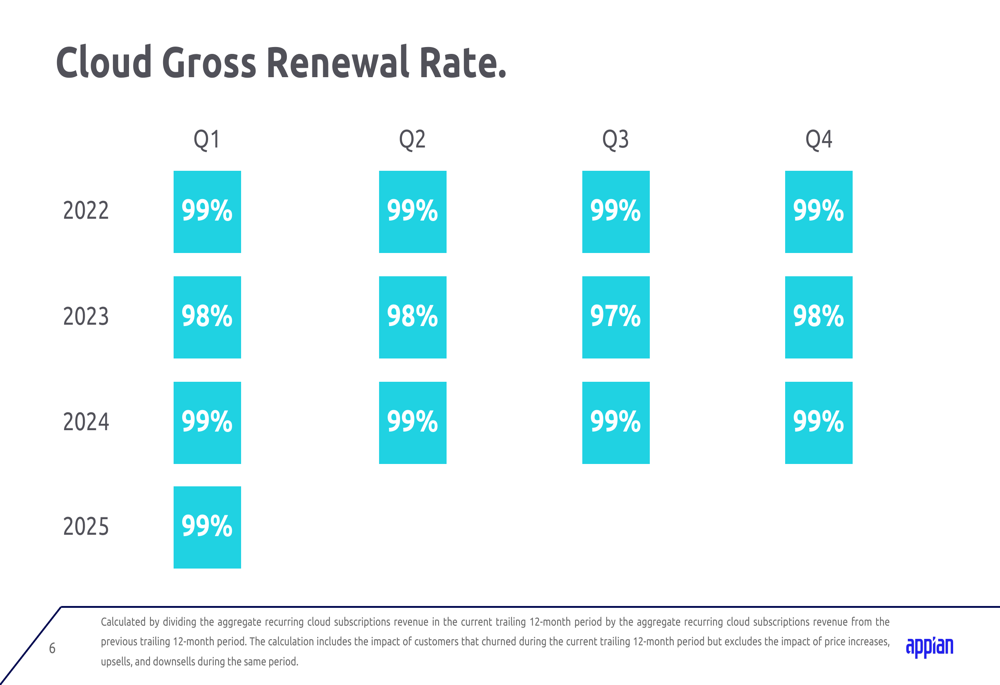

Appian maintained strong customer loyalty with a cloud gross renewal rate of 99% in Q1 2025, consistent with its performance throughout 2024. This metric reflects the company’s ability to retain its existing customer base.

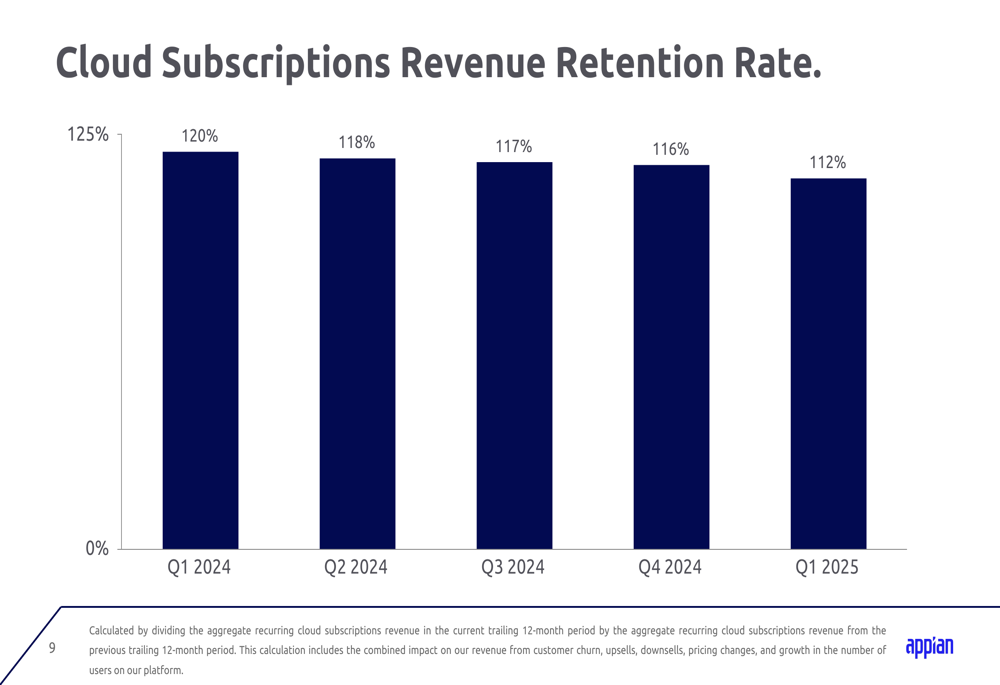

However, the cloud subscriptions revenue retention rate, which measures expansion within existing accounts, has declined from 120% in Q1 2024 to 112% in Q1 2025, indicating a potential slowdown in upselling and cross-selling activities.

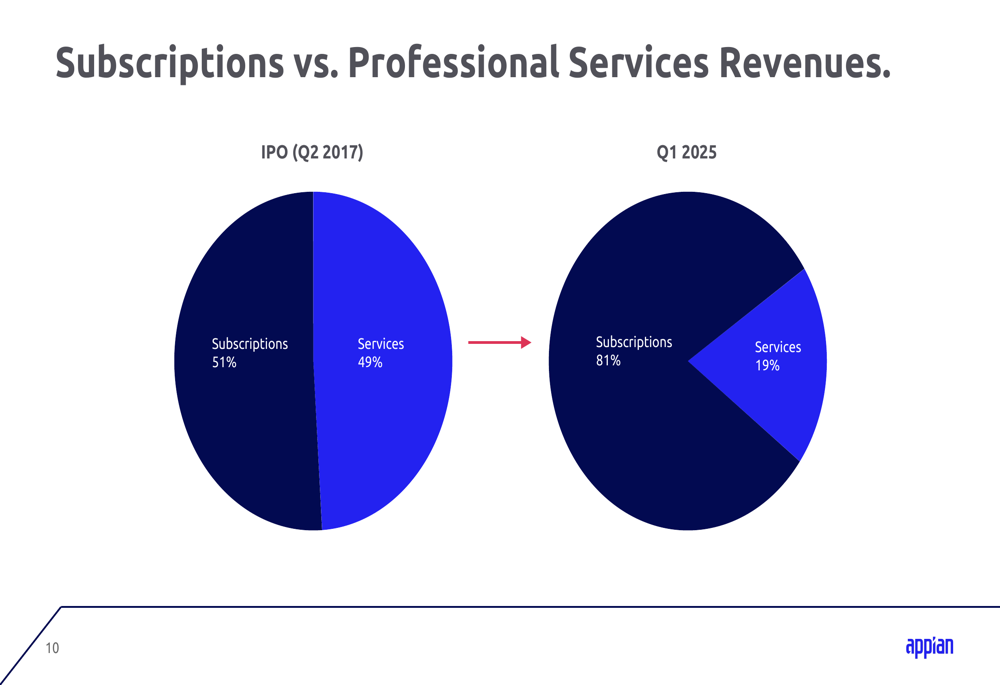

A significant long-term trend for Appian has been the evolution of its revenue mix. Since its IPO in Q2 2017, the company has strategically shifted from a balanced model (51% subscriptions, 49% services) to a predominantly subscription-based business (81% subscriptions, 19% services) in Q1 2025. This transition has positively impacted overall profitability due to the higher margins associated with subscription revenue.

AI Strategy and Positioning

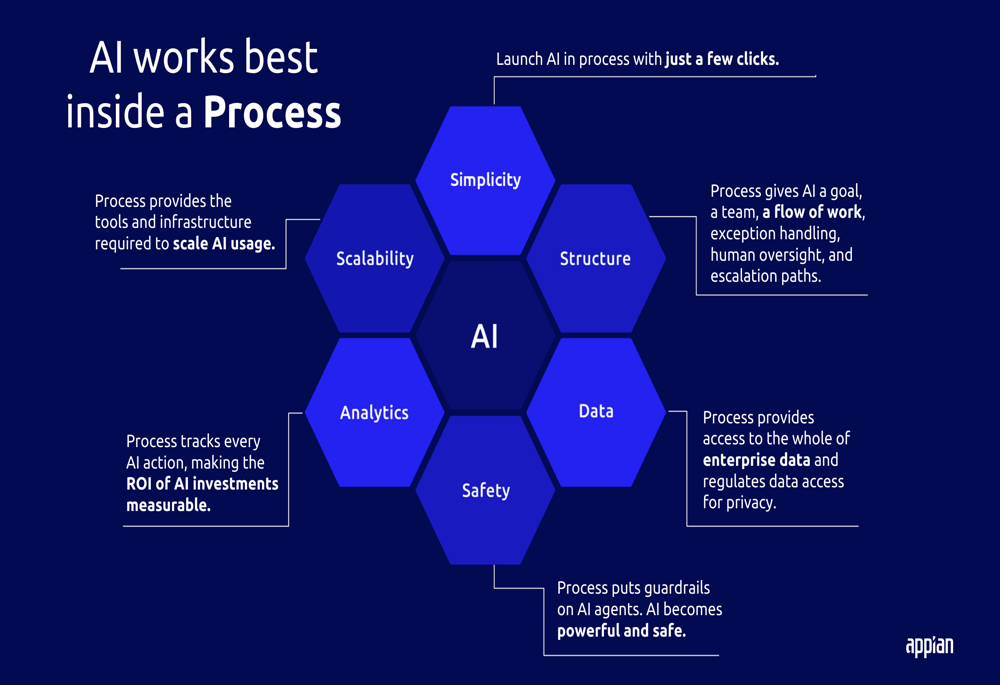

Appian continues to emphasize its strategic positioning in the AI market, focusing on integrating artificial intelligence capabilities within structured business processes. The company argues that AI works best within process frameworks that provide scalability, analytics for ROI measurement, safety mechanisms, and access to enterprise data.

The following diagram illustrates Appian’s approach to AI integration within business processes:

This strategy aligns with Appian’s core competency in process automation and positions the company to capitalize on the growing demand for practical, enterprise-grade AI applications that deliver measurable business value.

Margin Performance

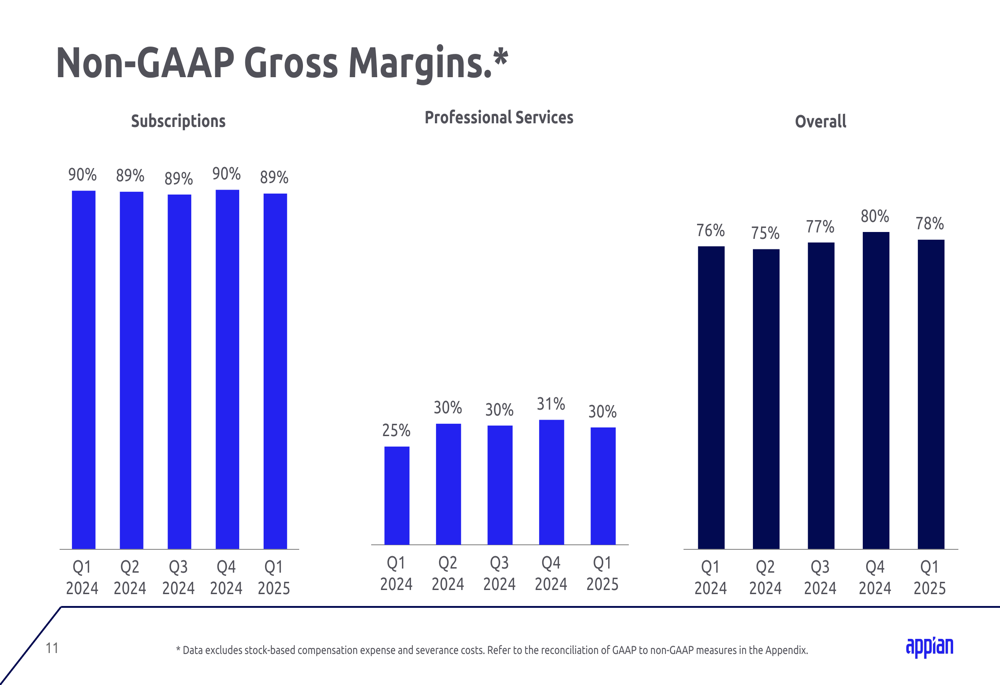

Appian’s gross margins have remained relatively stable across its business segments. Subscriptions gross margin was 89% in Q1 2025, consistent with previous quarters. Professional services gross margin showed improvement at 30%, while overall gross margin held steady at 78%.

The following chart details the company’s non-GAAP gross margins by segment:

Forward Guidance and Outlook

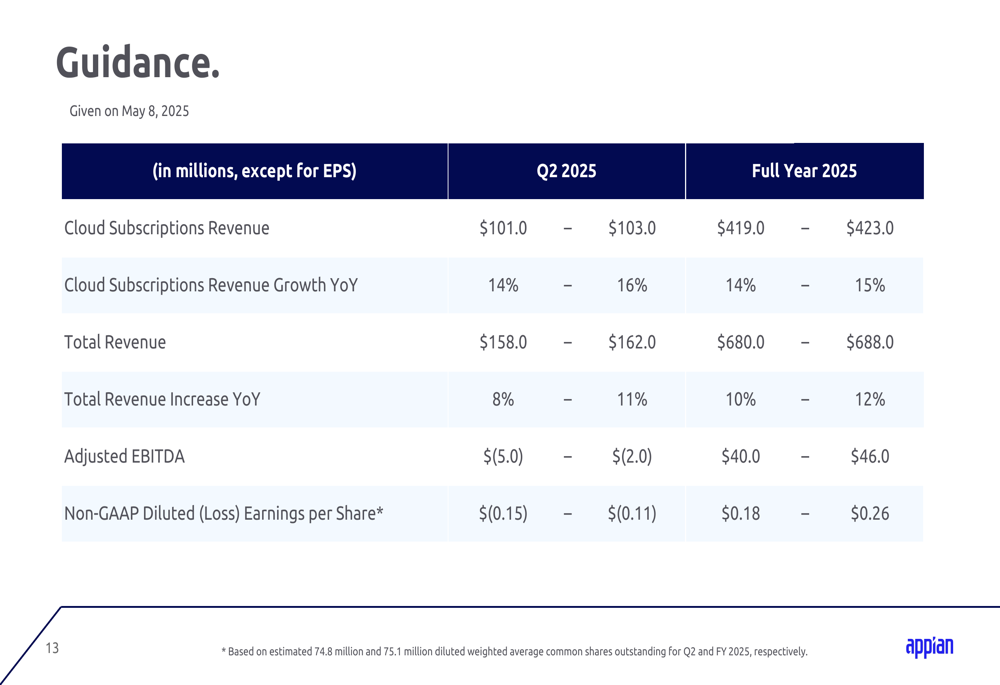

Looking ahead, Appian provided guidance for Q2 2025 and the full fiscal year. For Q2, the company expects cloud subscriptions revenue between $101.0 million and $103.0 million, representing 14% to 16% year-over-year growth. Total revenue is projected to be $158.0 million to $162.0 million, an increase of 8% to 11% compared to Q2 2024.

For the full year 2025, Appian forecasts cloud subscriptions revenue of $419.0 million to $423.0 million (14% to 15% growth) and total revenue of $680.0 million to $688.0 million (10% to 12% growth). The company expects positive adjusted EBITDA of $40.0 million to $46.0 million for the year, with non-GAAP earnings per share between $0.18 and $0.26.

However, investors should note that Appian anticipates a temporary return to negative adjusted EBITDA in Q2 2025, projecting a loss of $5.0 million to $2.0 million for the quarter.

Summary and Outlook

Appian’s Q1 2025 results demonstrate continued growth in cloud subscription revenue and improved profitability, though at a slower pace compared to previous quarters. The company’s strategic shift toward a subscription-based model continues to enhance margins, while its focus on integrating AI within business processes positions it to address emerging enterprise needs.

Key metrics for the quarter are summarized in the following chart:

While the declining cloud subscriptions revenue retention rate may raise concerns about future growth momentum, Appian’s consistent gross renewal rate and positive adjusted EBITDA suggest underlying business stability. The company’s guidance indicates confidence in maintaining double-digit revenue growth throughout 2025, with improved profitability on an annual basis despite expected quarterly fluctuations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.