Powell’s speech, Nvidia’s chips, Meta deal - what’s moving markets

Introduction & Market Context

Aramark (NYSE:ARMK), a global provider of food, facilities, and uniform services, released its Q2 fiscal 2025 earnings results on May 6, 2025, showing continued growth across key metrics despite some temporary headwinds. The company reported a 2% increase in revenue (3% organic growth) and a 15% rise in GAAP EPS compared to the same period last year.

The results come as Aramark continues to build on its strong performance from fiscal 2024, when the company achieved 10% organic revenue growth and a 35% increase in adjusted EPS. The stock closed at $34.20 on May 5, up 1.69% ahead of the earnings release, and was trading slightly lower in premarket at $34.01.

Quarterly Performance Highlights

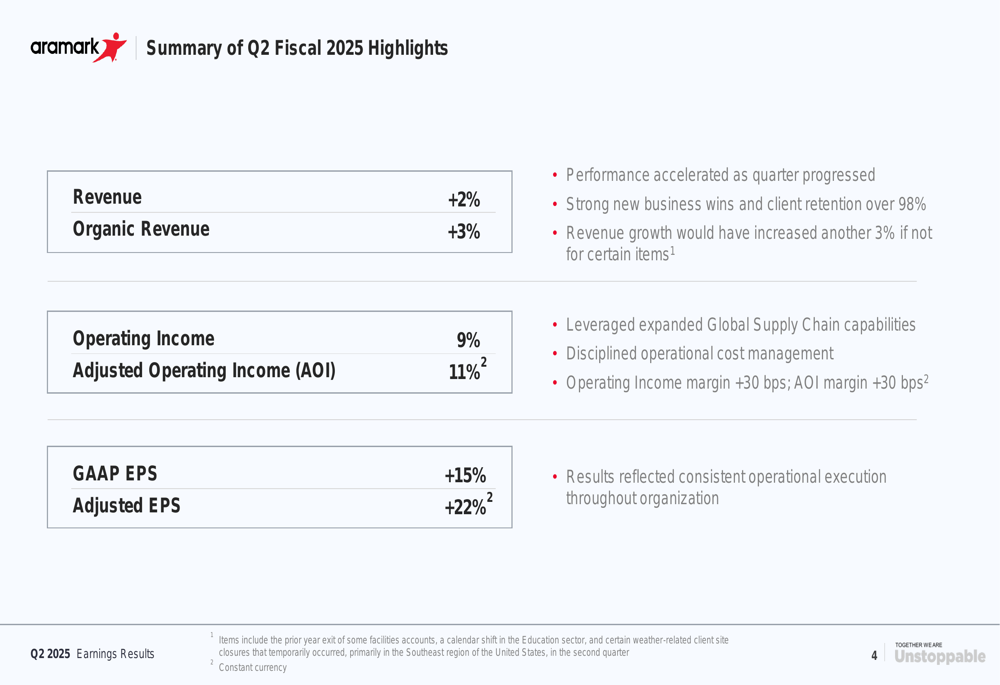

Aramark’s Q2 fiscal 2025 results demonstrated solid performance across key financial metrics, with growth in both revenue and profitability. The company highlighted that performance accelerated as the quarter progressed, supported by strong new business wins and exceptional client retention.

As shown in the following summary of Q2 highlights:

Revenue grew 2% as reported and 3% organically compared to the prior year. The company noted that revenue growth would have been approximately 3% higher if not for certain items, including prior year exits of some facilities accounts, a calendar shift in the Education sector, and weather-related client site closures primarily in the Southeast United States.

Operating income increased by 9%, while adjusted operating income (AOI) rose by 11% on a constant currency basis. This growth was attributed to expanded Global Supply Chain capabilities and disciplined operational cost management, resulting in operating income margin expansion of 30 basis points.

GAAP EPS grew by 15%, with adjusted EPS increasing by 22% on a constant currency basis, reflecting consistent operational execution throughout the organization.

Segment Performance Analysis

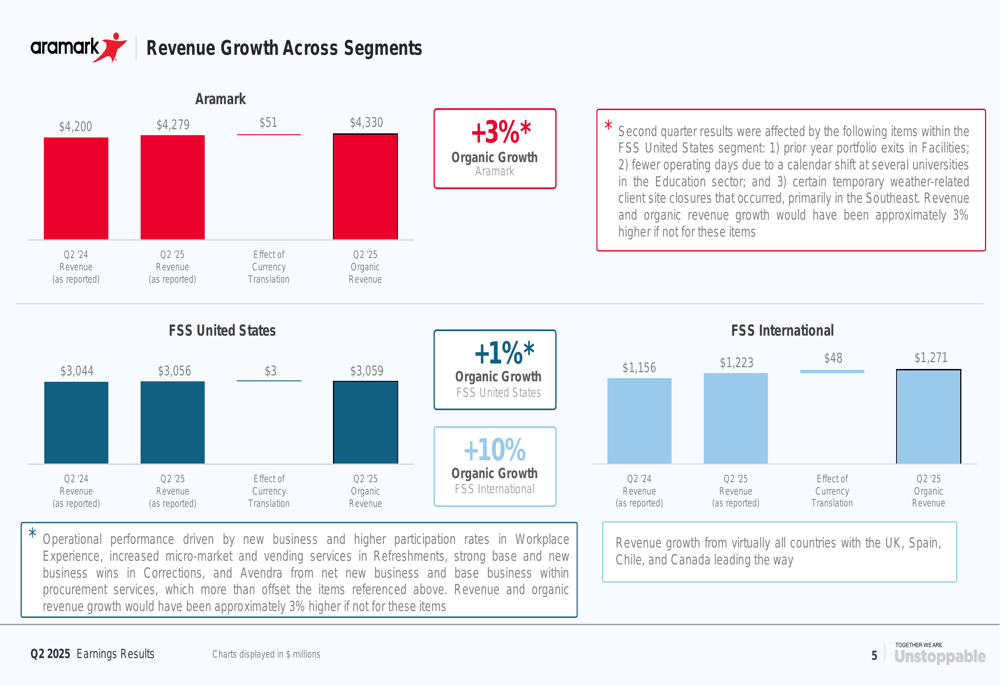

Aramark’s performance varied across its business segments, with particularly strong results in its international operations. The following chart breaks down revenue growth by segment:

The FSS United States segment reported 1% organic growth, while the FSS International segment delivered impressive 10% organic growth. The international growth was driven by strong performance across virtually all countries, with the UK, Spain, Chile, and Canada leading the way.

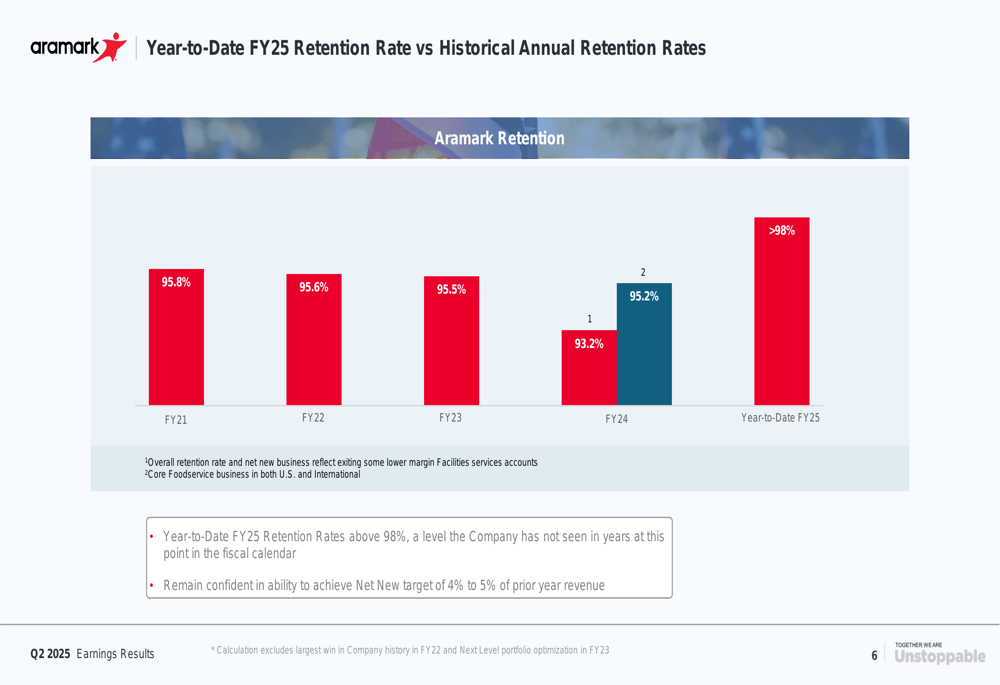

The company achieved record client retention rates in the quarter, exceeding 98% - a level not seen in years at this point in the fiscal calendar. This strong retention performance supports Aramark’s confidence in achieving its net new business target of 4% to 5% of prior year revenue.

The following chart illustrates Aramark’s retention rate improvement:

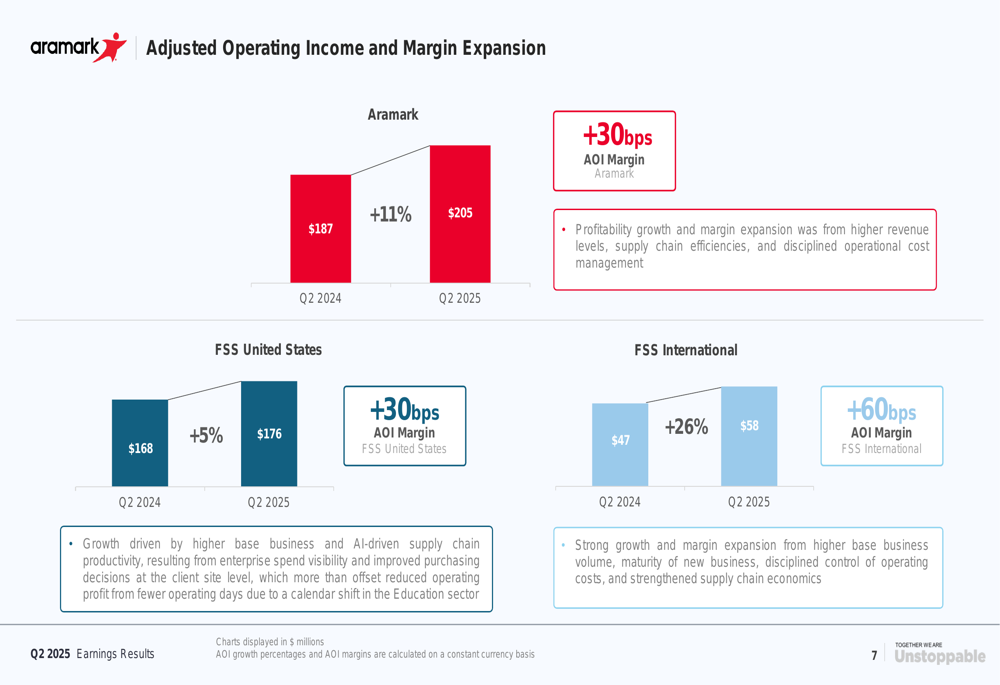

Profitability improved across all segments, with margin expansion driven by higher revenue levels, supply chain efficiencies, and disciplined operational cost management:

Adjusted operating income increased by 11% overall, with the FSS United States segment growing by 5% and the FSS International segment delivering 26% growth. AOI margins expanded by 30 basis points overall, with the International segment showing particularly strong improvement with a 60 basis point expansion.

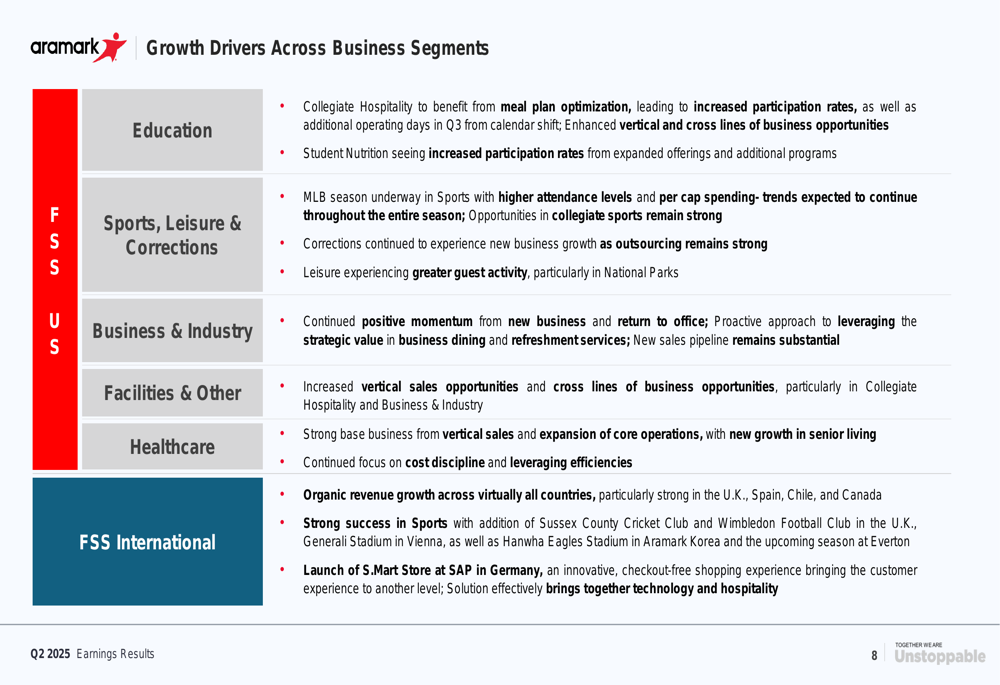

Growth Drivers Across Business Segments

Aramark highlighted several growth drivers across its various business segments that contributed to the quarter’s performance and are expected to support future growth:

In Education, the company expects to benefit from meal plan optimization leading to increased participation rates, as well as additional operating days in Q3 from the calendar shift that affected Q2. Student Nutrition is seeing increased participation rates from expanded offerings and additional programs.

The Sports, Leisure & Corrections segment is benefiting from higher attendance levels and per capita spending in MLB venues, with these trends expected to continue throughout the season. The Corrections business continues to experience new business growth as outsourcing remains strong.

Business & Industry is seeing continued positive momentum from new business and return to office, with a substantial new sales pipeline. Healthcare is experiencing strong base business growth from vertical sales and expansion of core operations, with new growth in senior living.

The FSS International segment continues to focus on cost discipline and leveraging efficiencies, with strong success in Sports through new contracts including Sussex County Cricket Club, Wimbledon Football Club, and Generali (BIT:GASI) Stadium. The company also highlighted the innovative S.Mart Store at SAP in Germany, a checkout-free shopping experience that effectively combines technology and hospitality.

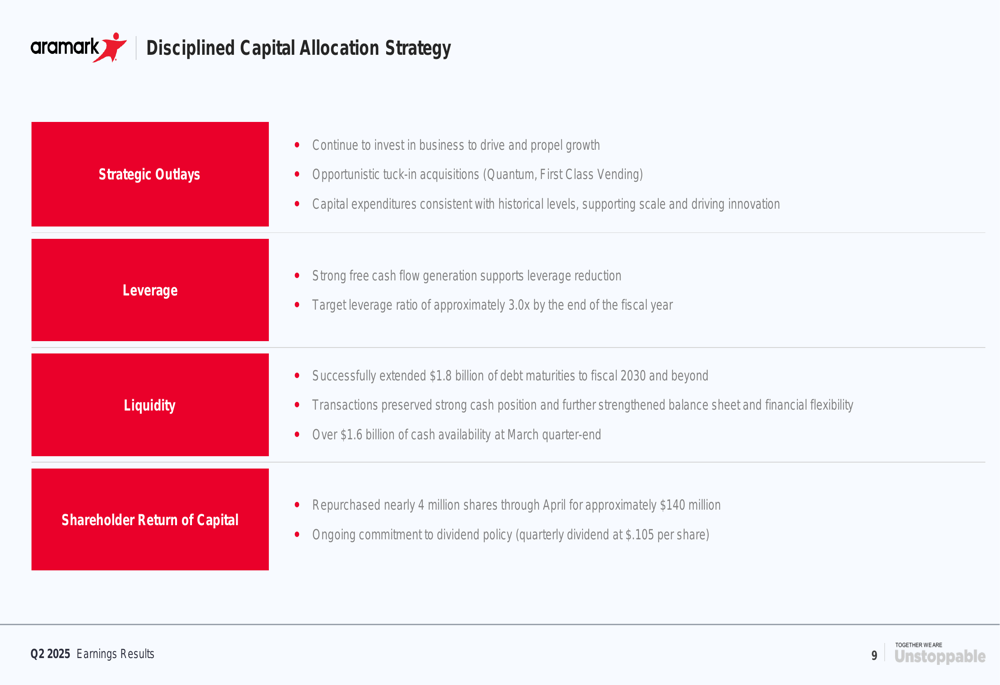

Capital Allocation and Balance Sheet

Aramark outlined its disciplined capital allocation strategy, focusing on strategic investments, leverage reduction, and shareholder returns:

The company continues to invest in business growth while pursuing opportunistic tuck-in acquisitions, such as Quantum and First Class Vending. Capital expenditures remain consistent with historical levels, supporting scale and driving innovation.

Strong free cash flow generation is supporting leverage reduction, with a target leverage ratio of approximately 3.0x by the end of the fiscal year. The company successfully extended $1.8 billion of debt maturities to fiscal 2030 and beyond, preserving its strong cash position and enhancing financial flexibility.

Aramark reported over $1.6 billion of cash availability at the March quarter-end. The company has also been actively returning capital to shareholders, repurchasing nearly 4 million shares through April for approximately $140 million and maintaining its quarterly dividend at $0.105 per share.

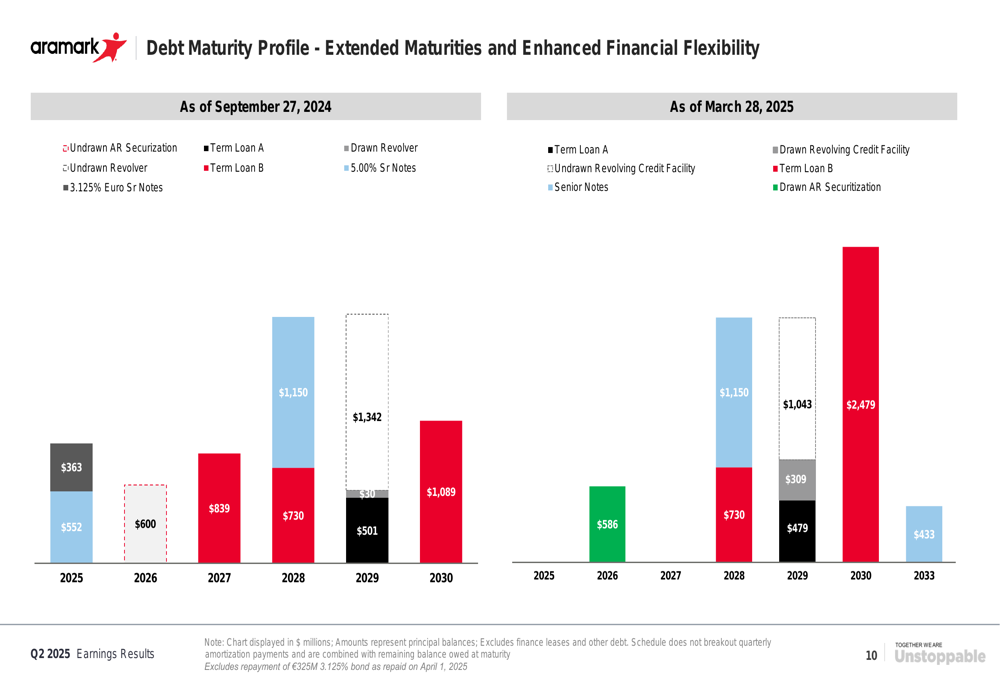

The company has improved its debt maturity profile, as illustrated in the following chart:

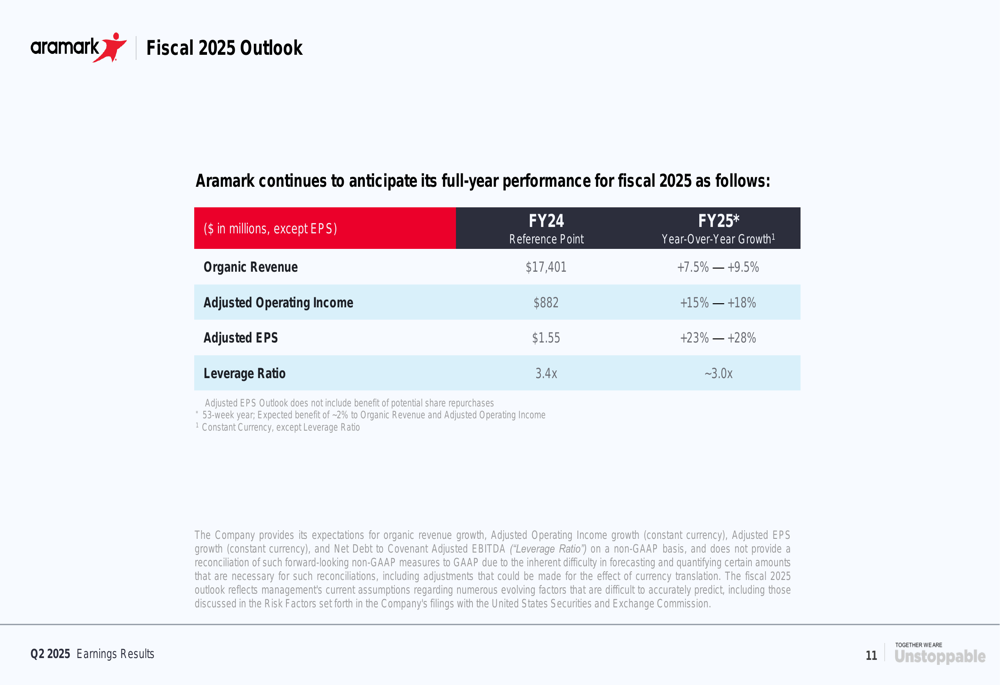

Forward Guidance

Aramark maintained its fiscal 2025 outlook, projecting continued strong growth across key financial metrics:

The company expects organic revenue growth of 7.5% to 9.5% for the full fiscal year, with adjusted operating income growth of 15% to 18% and adjusted EPS growth of 23% to 28%. Aramark also anticipates achieving its target leverage ratio of approximately 3.0x by the end of the fiscal year.

These projections align with the guidance provided in the previous earnings call and reflect management’s confidence in the company’s ability to execute its growth strategy despite temporary headwinds experienced in Q2.

Conclusion

Aramark’s Q2 fiscal 2025 results demonstrate the company’s ability to deliver consistent growth and margin expansion through operational excellence and strategic initiatives. The record client retention rate above 98% highlights strong customer satisfaction, while the impressive 10% organic growth in the international segment showcases the company’s global growth potential.

The company’s disciplined approach to capital allocation, including strategic investments, debt management, and shareholder returns, positions it well for sustainable long-term growth. With a clear outlook for fiscal 2025 and strong momentum across most business segments, Aramark appears well-positioned to continue its growth trajectory and achieve its financial targets for the year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.