TPI Composites files for Chapter 11 bankruptcy, plans delisting from Nasdaq

Introduction & Market Context

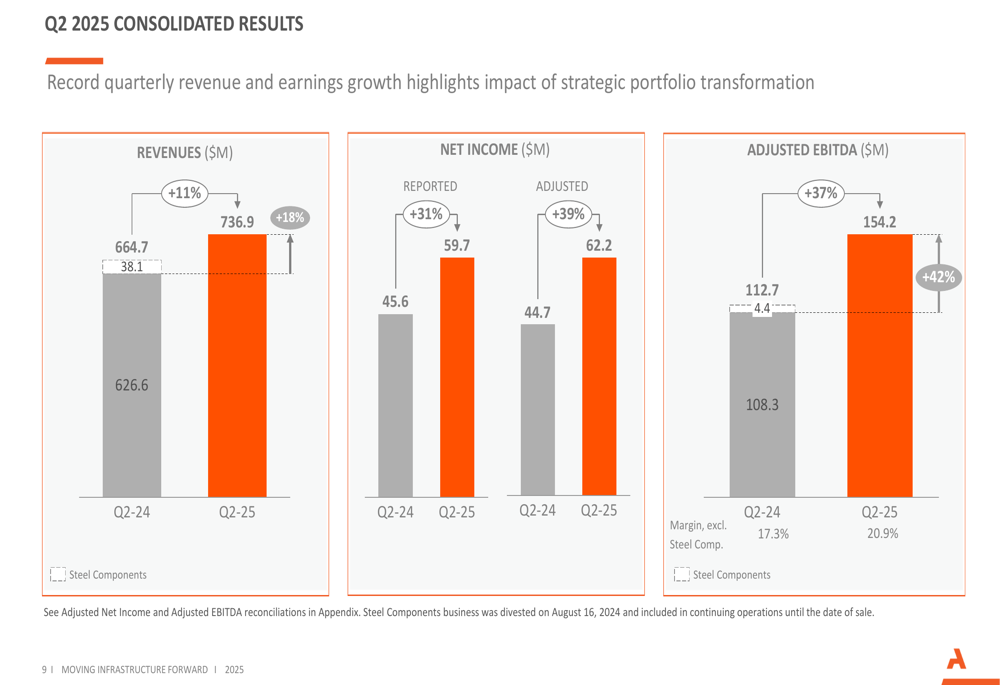

Arcosa Inc (NYSE:ACA) reported record second-quarter results on August 8, 2025, showcasing significant margin expansion and continued progress on its strategic transformation. The infrastructure company’s stock rose 4.91% to $89.28 following the earnings release, reflecting positive investor sentiment toward the strong performance and tightened full-year guidance.

The results come amid a supportive infrastructure spending environment, bolstered by federal funding from the Infrastructure Investment and Jobs Act (IIJA), though the company noted that timing of interest rate reductions and macroeconomic uncertainty are slowing recovery in residential and commercial end-markets.

Quarterly Performance Highlights

Arcosa delivered impressive financial results for Q2 2025, with Adjusted EBITDA growth of 42% significantly outpacing revenue growth of 18%. The company achieved a record consolidated Adjusted EBITDA margin of 20.9%, representing a substantial 360 basis point improvement year-over-year.

As shown in the following consolidated results chart, revenues reached $736.9 million, up 11% from Q2 2024, while net income increased 31% to $59.7 million:

The strong performance was driven by both organic growth and the accretive impact of the Stavola acquisition, which contributed $90.3 million in revenues during the quarter. Organic margin expansion of approximately 110 basis points was led by the Engineered Structures segment, while aggregates pricing increased by 8%, driving a 15% gain in cash unit profitability.

Segment Analysis

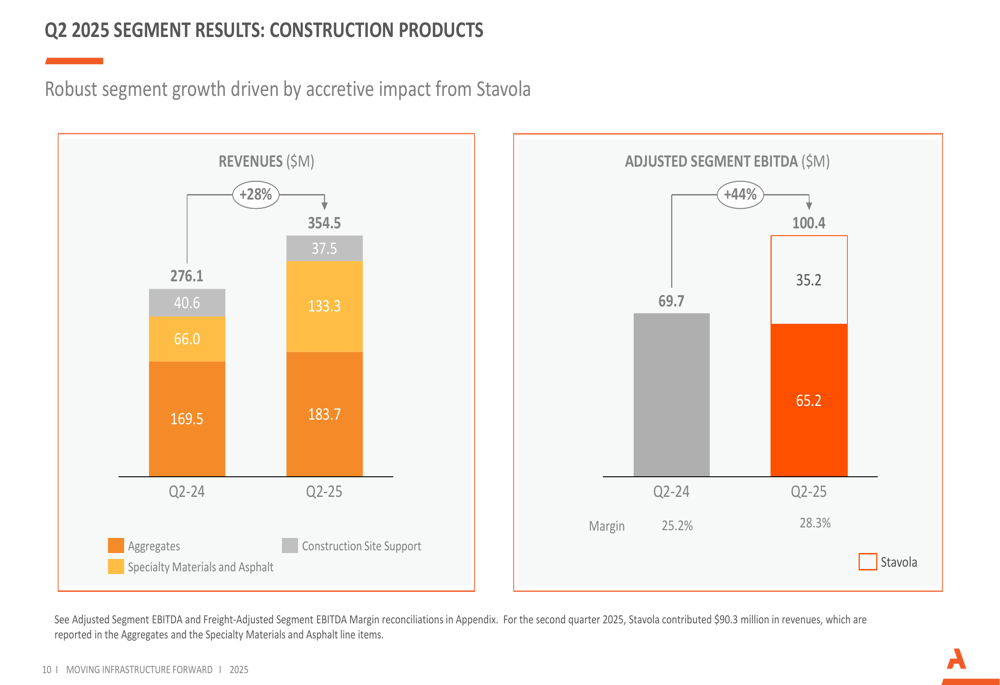

The Construction Products segment, which now represents the largest portion of Arcosa’s business, delivered exceptional results with revenues of $354.5 million, up 28% year-over-year. Adjusted segment EBITDA increased 44% to $100.4 million, with margins expanding to 28.3% from 25.2% in the prior year period.

The segment breakdown shows strong performance across aggregates and specialty materials, with the Stavola acquisition significantly boosting the specialty materials and asphalt category:

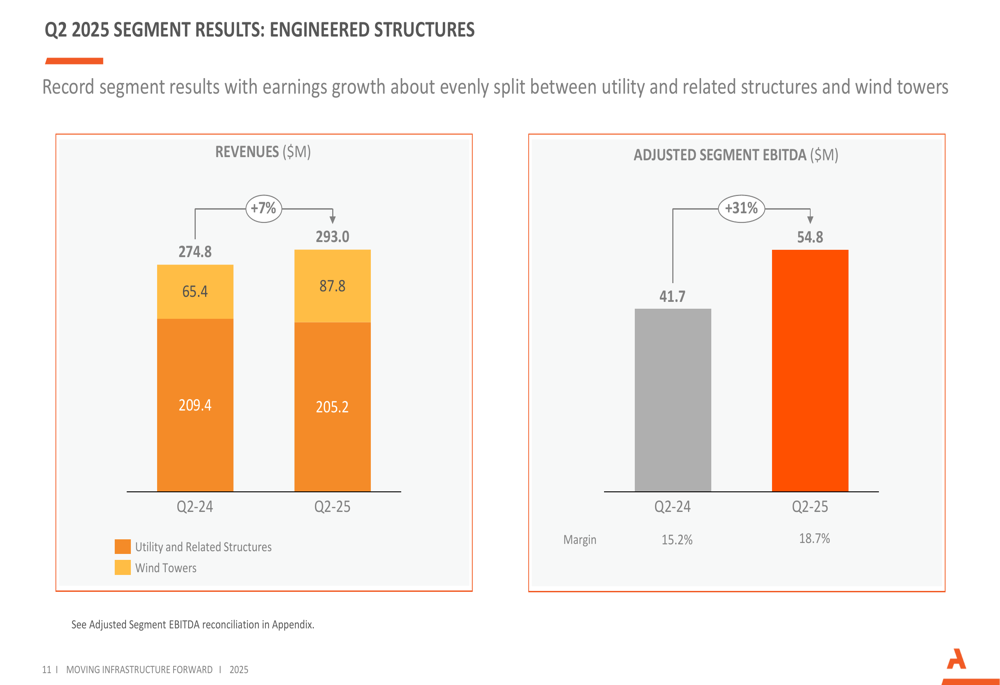

The Engineered Structures segment also demonstrated robust performance, with revenues increasing 7% to $293.0 million and Adjusted segment EBITDA growing 31% to $54.8 million. Margins in this segment expanded significantly from 15.2% to 18.7%, reflecting operational efficiencies and strong demand for utility structures.

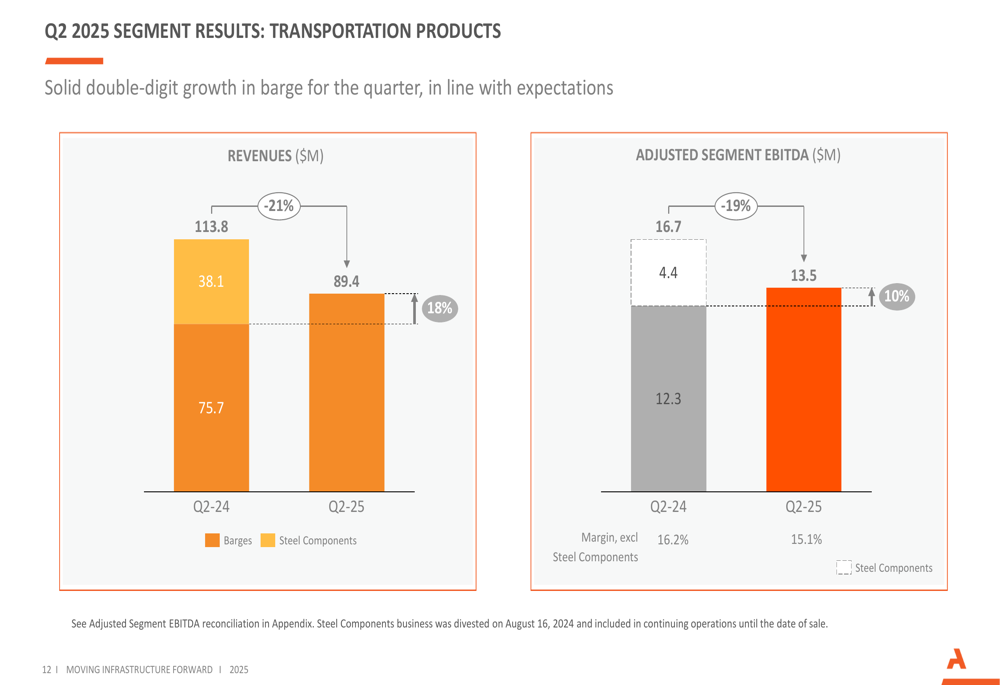

The Transportation Products segment, which has become a smaller part of Arcosa’s portfolio following the divestiture of the Steel Components business in August 2024, reported revenues of $89.4 million and Adjusted segment EBITDA of $13.5 million. While these figures represent year-over-year declines of 21% and 19% respectively, the comparison is affected by the divestiture.

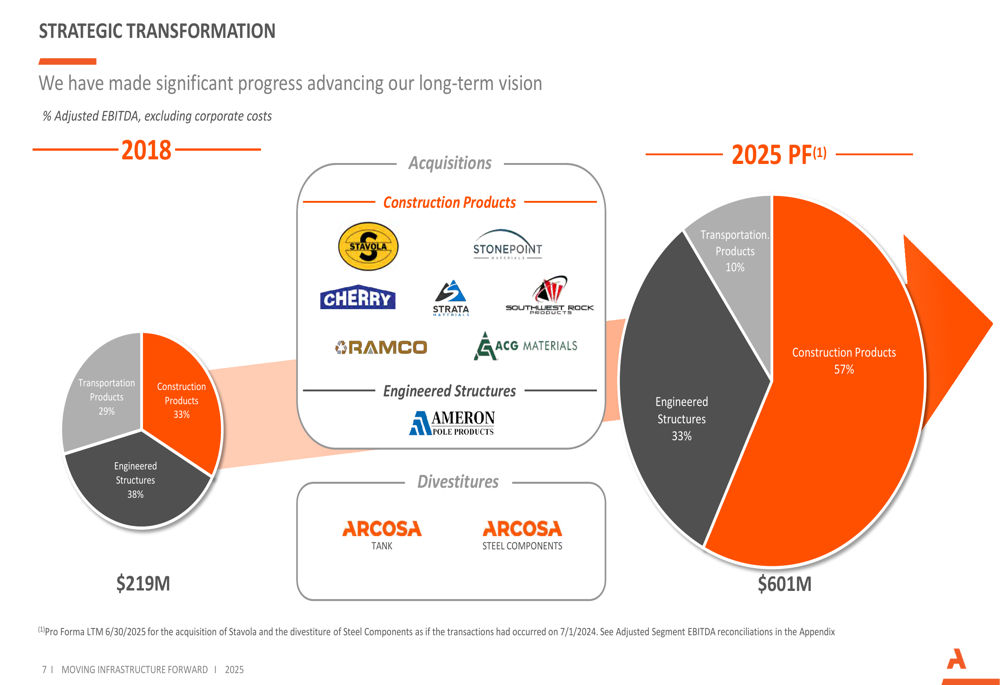

Strategic Transformation

Arcosa’s Q2 results highlight the company’s ongoing strategic transformation, which has significantly altered its business mix since 2018. The company has executed a deliberate shift toward less cyclical, higher-margin businesses, particularly in the Construction Products segment.

As illustrated in the strategic transformation chart, Construction Products now represents 57% of the company’s revenue, up from 33% in 2018, while Transportation Products has decreased from 29% to 10%:

This transformation has been achieved through strategic acquisitions, including the recent Stavola purchase, and divestitures like the Steel Components business. The company’s Adjusted EBITDA has grown from $219 million in 2018 to a projected $601 million in 2025 (pro forma), demonstrating the financial benefits of this strategic shift.

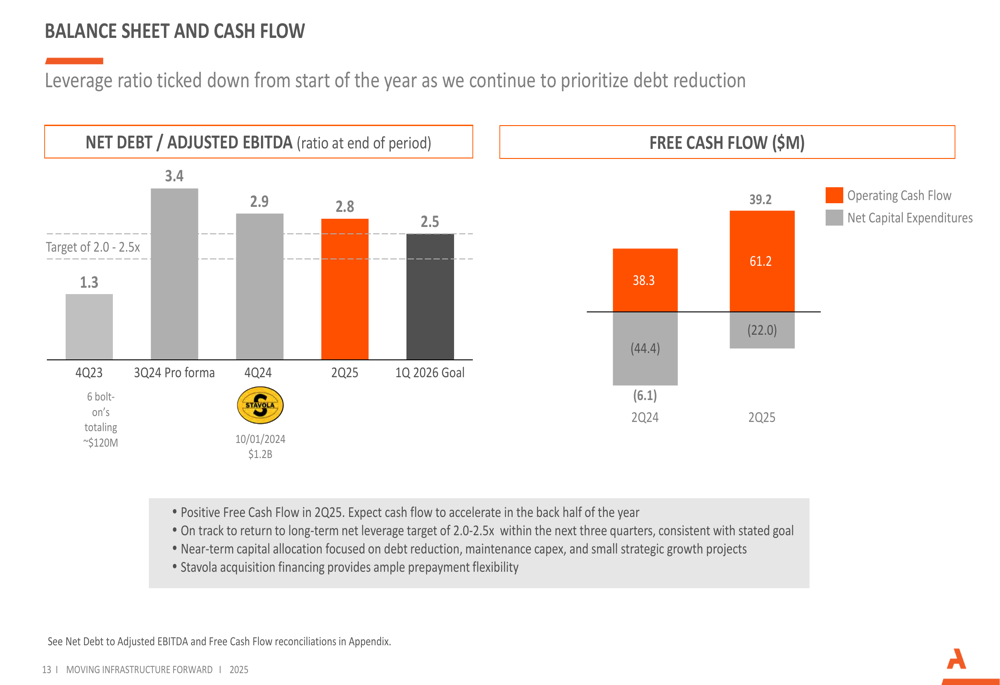

Balance Sheet and Outlook

Arcosa reported progress in reducing leverage following the Stavola acquisition, with Net Debt to Adjusted EBITDA improving to 2.8x, down from 2.9x at the end of Q4 2024. The company remains committed to returning to its long-term net leverage target of 2.0-2.5x within the next three quarters.

Free Cash Flow improved significantly, turning positive at $39.2 million in Q2 2025 compared to negative $6.1 million in Q2 2024, as shown in the following chart:

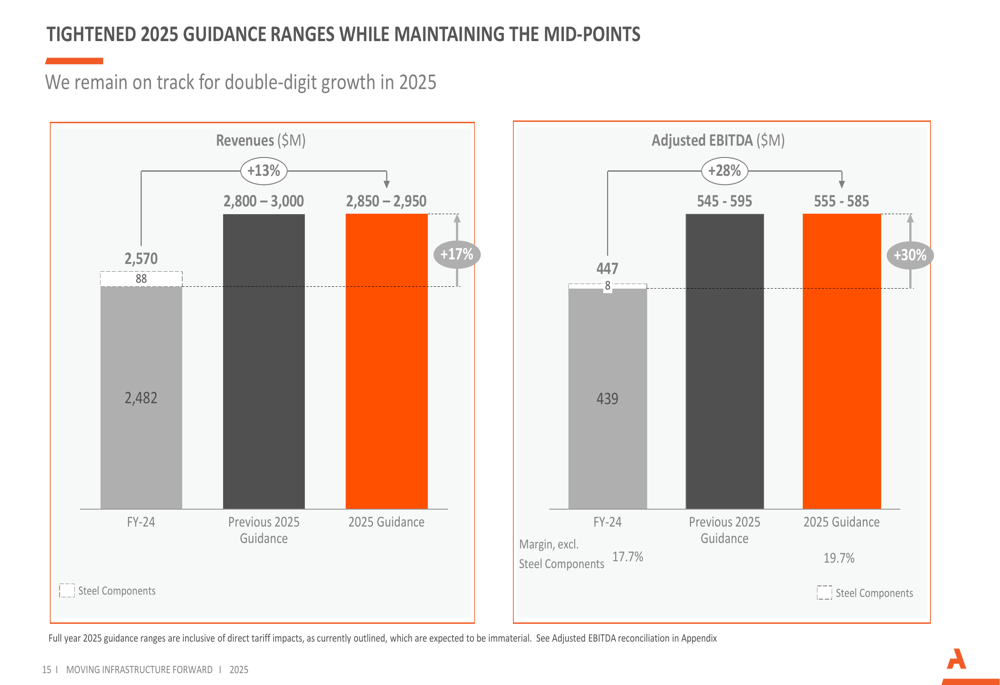

Looking ahead, Arcosa tightened its full-year 2025 guidance, maintaining the midpoint of its previous ranges while narrowing the bands. The company now expects revenues of $2.85-2.95 billion (up 17% year-over-year) and Adjusted EBITDA of $555-585 million (up 30% year-over-year), with margin expansion of approximately 200 basis points.

The updated guidance is visualized in the following chart:

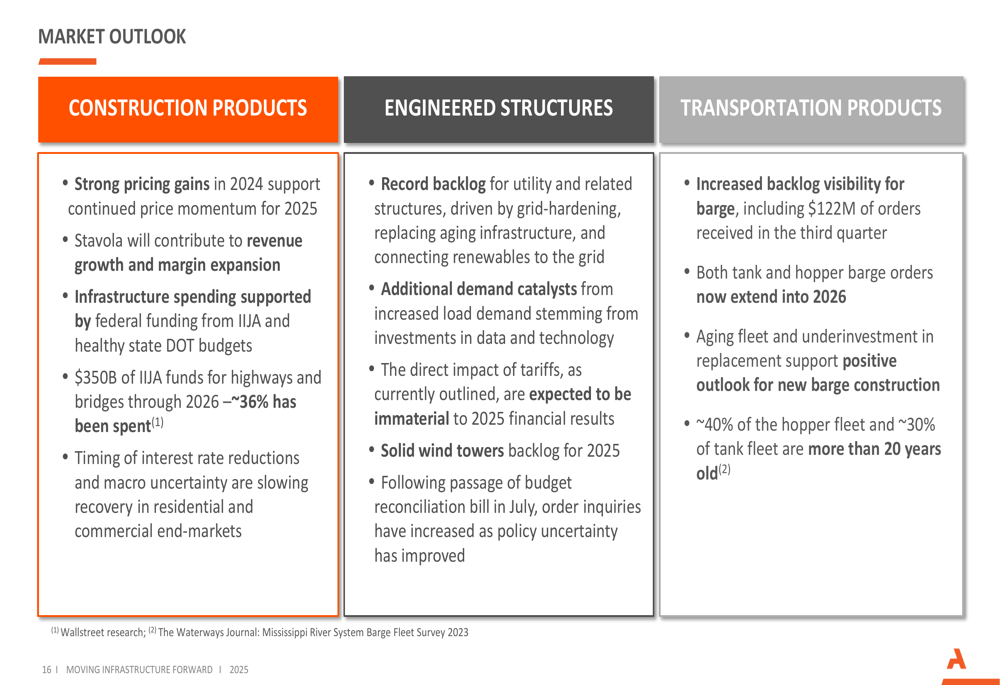

The company’s market outlook remains positive across its segments, with strong pricing momentum in Construction Products, record backlog in utility structures, and increased order visibility in barges. Infrastructure spending continues to be supported by federal funding, with approximately 36% of the $350 billion IIJA funds for highways and bridges having been spent through 2026.

With its strategic transformation progressing well, strong operational performance, and positive market outlook, Arcosa appears well-positioned to continue delivering growth and margin expansion through 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.