AZTR receives NYSE delisting warning over equity requirement

Introduction & Market Context

Ariston Holding NV (ARIS) presented its second quarter and first half 2025 results on July 31, 2025, revealing continued organic growth despite challenging market conditions. The company’s shares declined 4.12% following the presentation, trading at €4.55, down from the previous close of €4.75.

The thermal comfort and water heating solutions provider demonstrated resilience in its core European markets while advancing strategic initiatives to strengthen its global footprint, particularly in North America through a new joint venture with Lennox.

Quarterly Performance Highlights

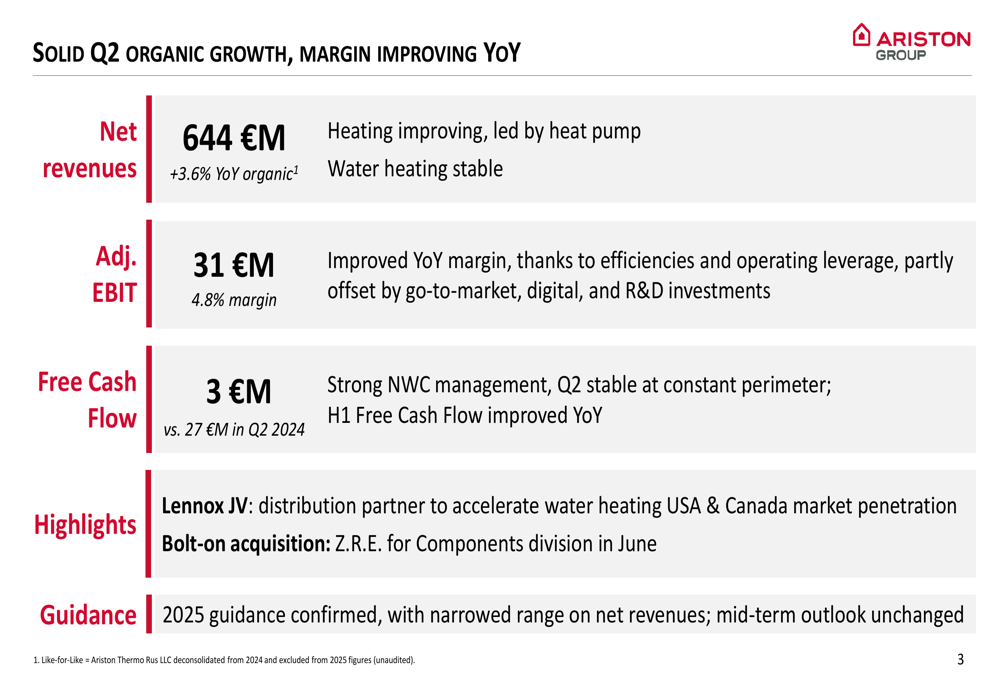

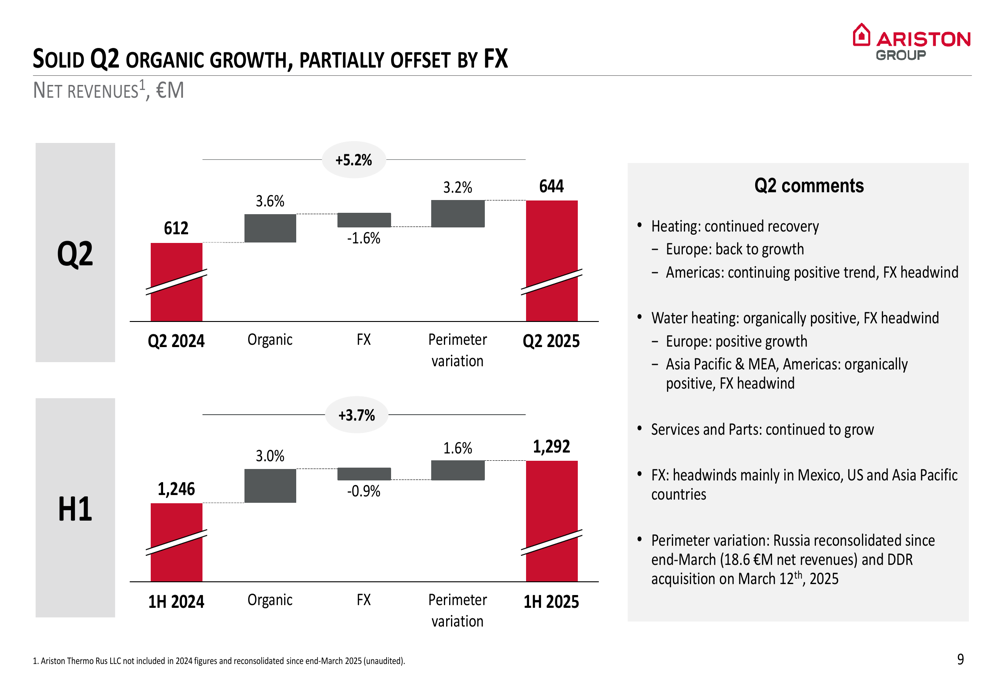

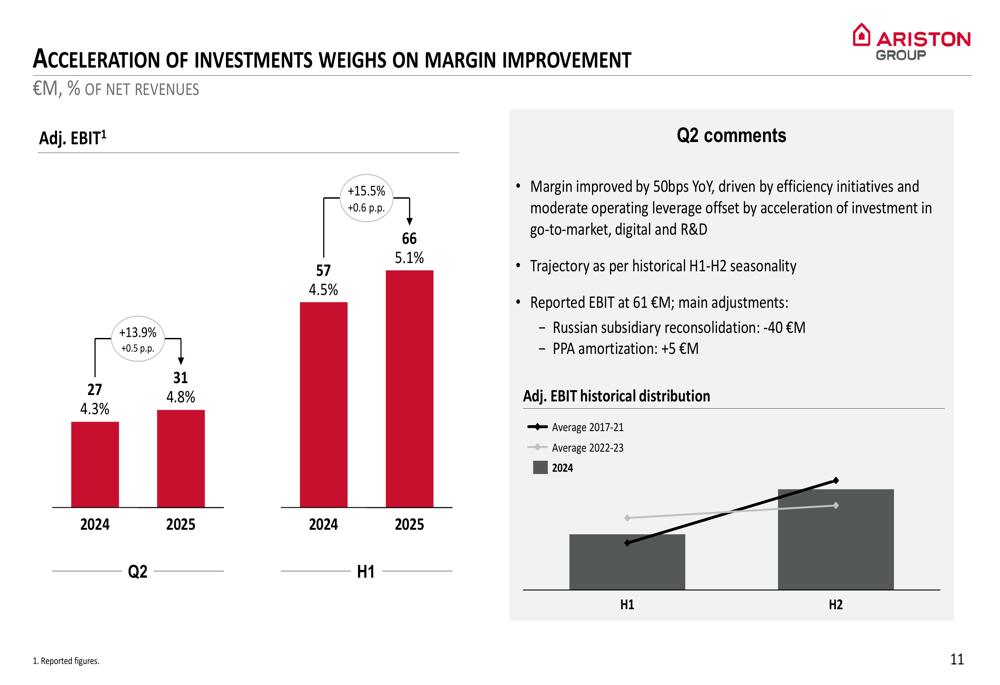

Ariston reported Q2 2025 net revenues of €644 million, representing a 3.6% year-over-year organic growth. Adjusted EBIT reached €31 million with a 4.8% margin, showing a 50 basis point improvement from Q2 2024. However, free cash flow declined to €3 million compared to €27 million in the same period last year.

As shown in the following performance summary:

For the first half of 2025, the company achieved net revenues of €1,292 million with 3.0% organic growth and adjusted EBIT of €66 million, representing a 5.1% margin compared to 4.5% in H1 2024.

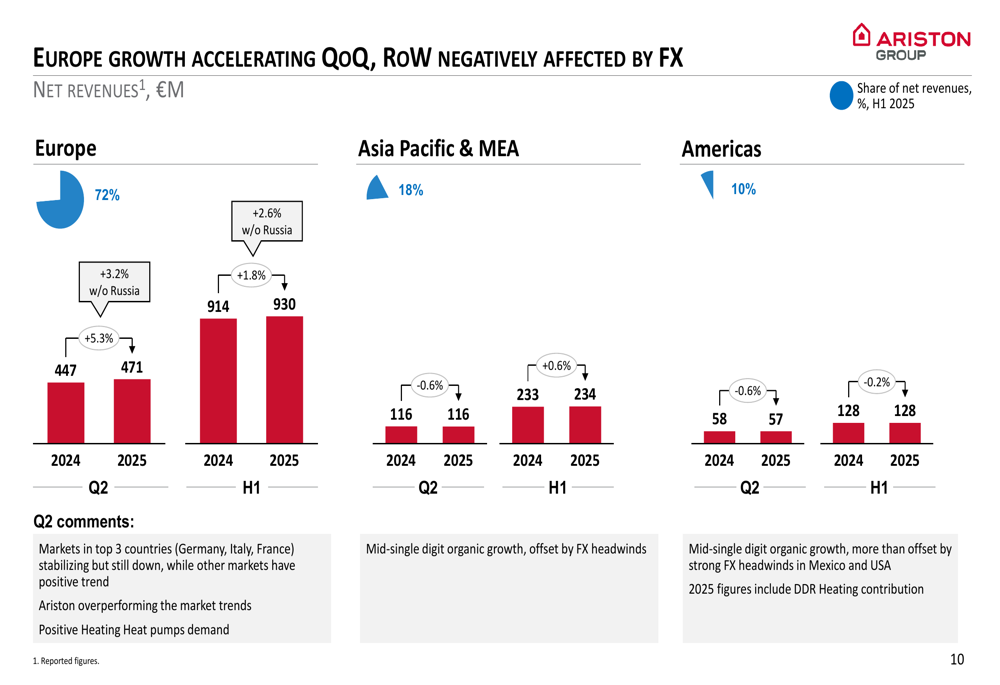

The organic growth was partially offset by foreign exchange headwinds of -1.6% in Q2, while perimeter variation contributed positively at 3.2%, which includes the reconsolidation of the Russian subsidiary since late March 2025.

Strategic Initiatives

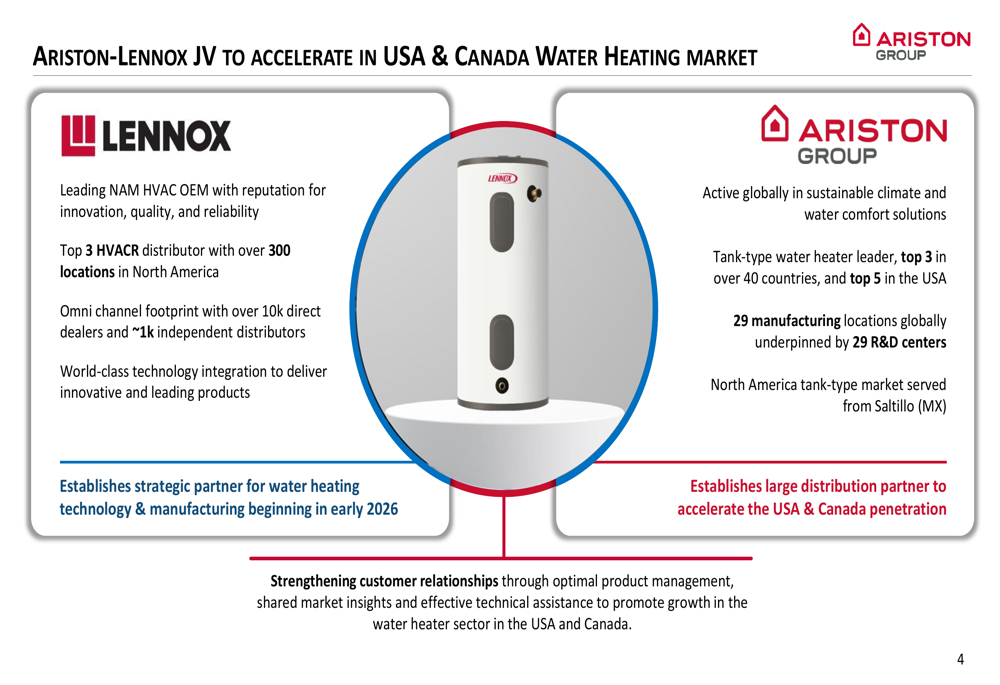

A centerpiece of Ariston’s growth strategy is the newly announced joint venture with Lennox, a leading North American HVAC manufacturer and distributor. This partnership aims to accelerate Ariston’s penetration in the USA and Canadian water heating markets beginning in early 2026.

The strategic rationale for the joint venture combines Lennox’s extensive distribution network of over 300 locations with Ariston’s global manufacturing capabilities and water heating expertise:

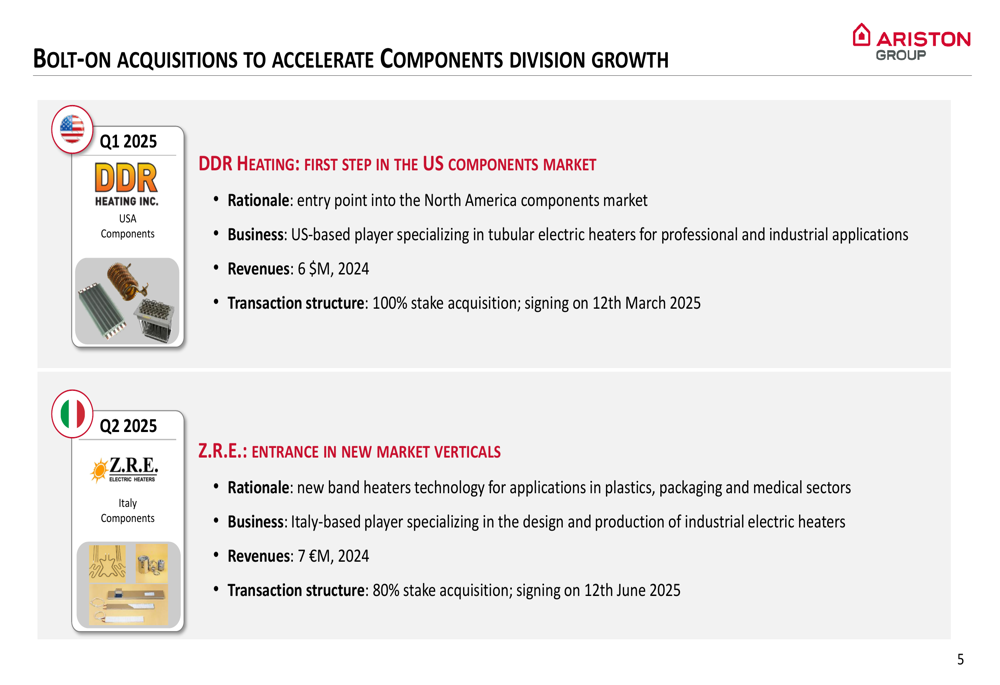

Additionally, Ariston completed two bolt-on acquisitions to strengthen its Components division. In Q1 2025, the company acquired DDR (NYSE:SITC) Heating, a US-based specialist in tubular electric heaters with annual revenues of $6 million. This was followed by the June 2025 acquisition of Z.R.E., an Italian manufacturer of industrial electric heaters with revenues of €7 million, bringing new band heaters technology for applications in plastics, packaging, and medical sectors.

Regional Performance

Europe, which accounts for 72% of Ariston’s net revenues, showed accelerating growth with Q2 2025 revenues increasing by 5.3% to €471 million compared to Q2 2024. This performance is particularly notable given the challenging conditions in key markets like Germany, Italy, and France, where Ariston claims to be outperforming market trends.

The company’s regional performance breakdown reveals the strength of European operations offsetting challenges in other regions:

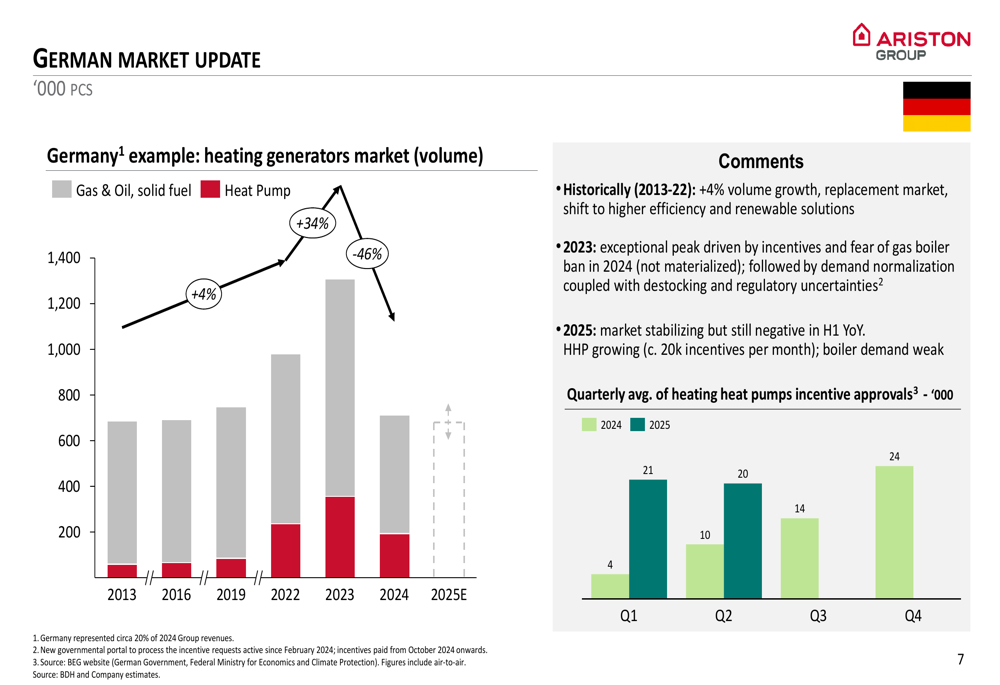

The German market, a crucial region for Ariston, is showing signs of stabilization in 2025 after experiencing significant volatility in recent years. The market saw exceptional growth of 34% in 2022 followed by a 46% decline in 2023, driven by changes in incentive programs for heating systems.

Margin and Efficiency

Ariston’s adjusted EBIT margin improved by 50 basis points year-over-year in Q2 2025, reaching 4.8%. This improvement came despite increased investments in go-to-market initiatives, digital transformation, and R&D, highlighting the effectiveness of the company’s efficiency programs.

The margin improvement trajectory follows historical seasonality patterns, with stronger performance expected in the second half of the year:

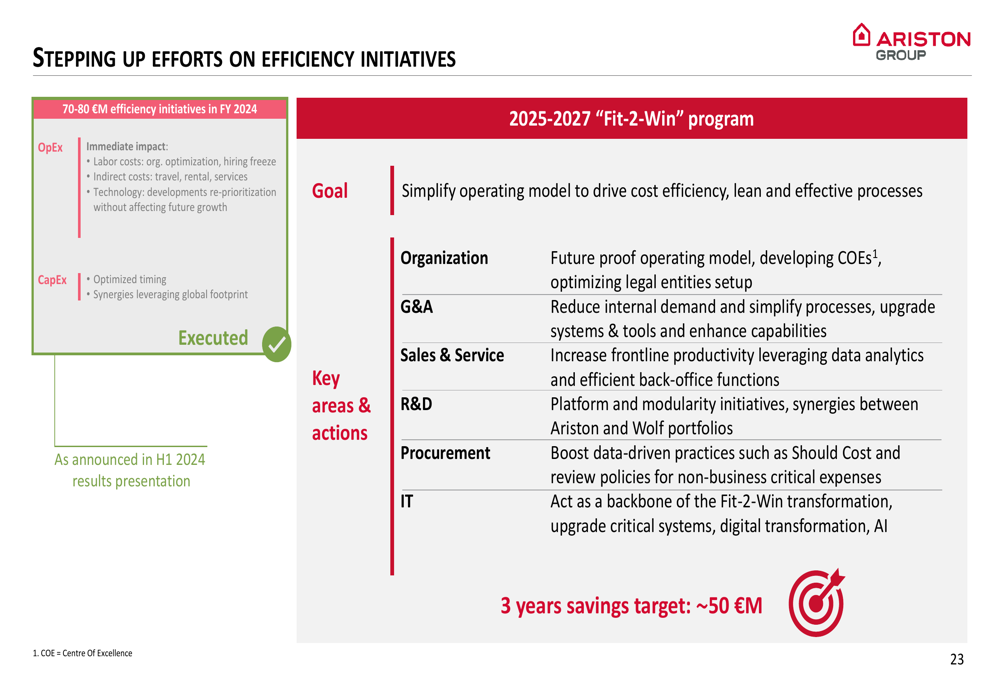

To drive further efficiencies, Ariston is implementing its "Fit-2-Win" program, which targets approximately €50 million in savings over three years. The initiative focuses on organizational optimization, process simplification, and data-driven procurement practices.

Net working capital discipline remains strong, with working capital as a percentage of rolling net revenues improving by 3.0 percentage points year-over-year at constant perimeter, reaching 15.1% as of June 30, 2025.

Forward-Looking Statements

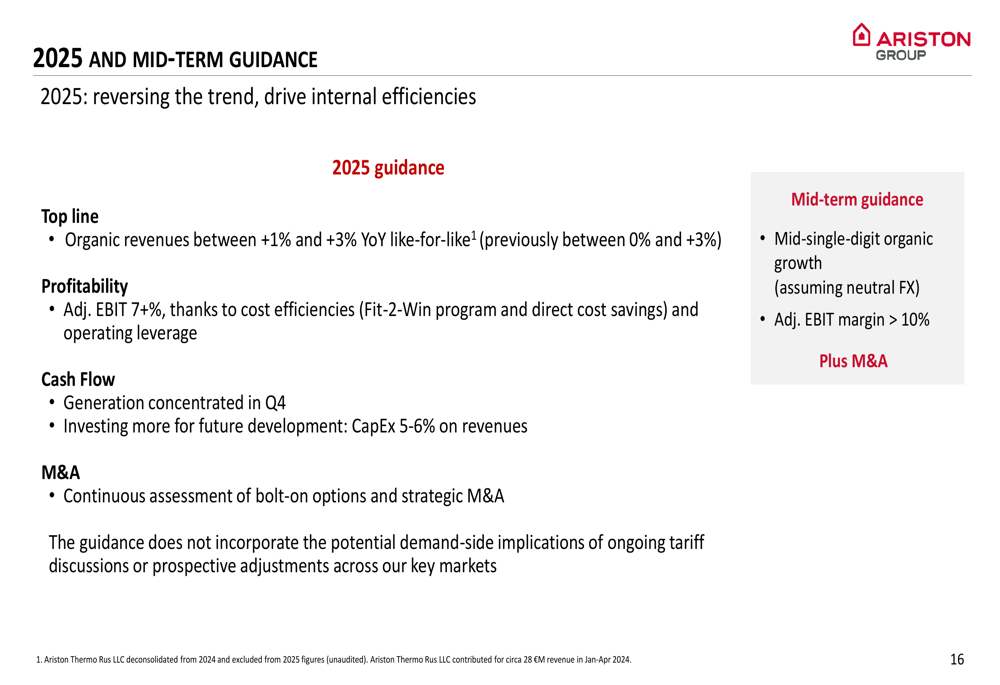

Ariston has narrowed its 2025 guidance, now projecting organic revenue growth between 1% and 3% year-over-year (previously 0% to 3%). The company maintains its adjusted EBIT margin target of 7+%, supported by cost efficiencies from the Fit-2-Win program and operating leverage.

For the medium term, Ariston continues to target mid-single-digit organic growth and an adjusted EBIT margin exceeding 10%, supplemented by strategic M&A activities:

Management noted that the guidance does not incorporate potential implications of ongoing tariff discussions or prospective adjustments across key markets, which could impact demand patterns.

Capital expenditure is expected to remain at 5-6% of revenues as the company continues to invest in future development, while also assessing bolt-on acquisition opportunities and strategic M&A to complement organic growth.

The company’s balanced approach to capital allocation, combined with its global presence in 40+ countries and leading market positions, positions Ariston to navigate market challenges while pursuing its long-term growth strategy in both thermal comfort and water heating segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.