EUR/USD likely to find a peak near 1.25: UBS

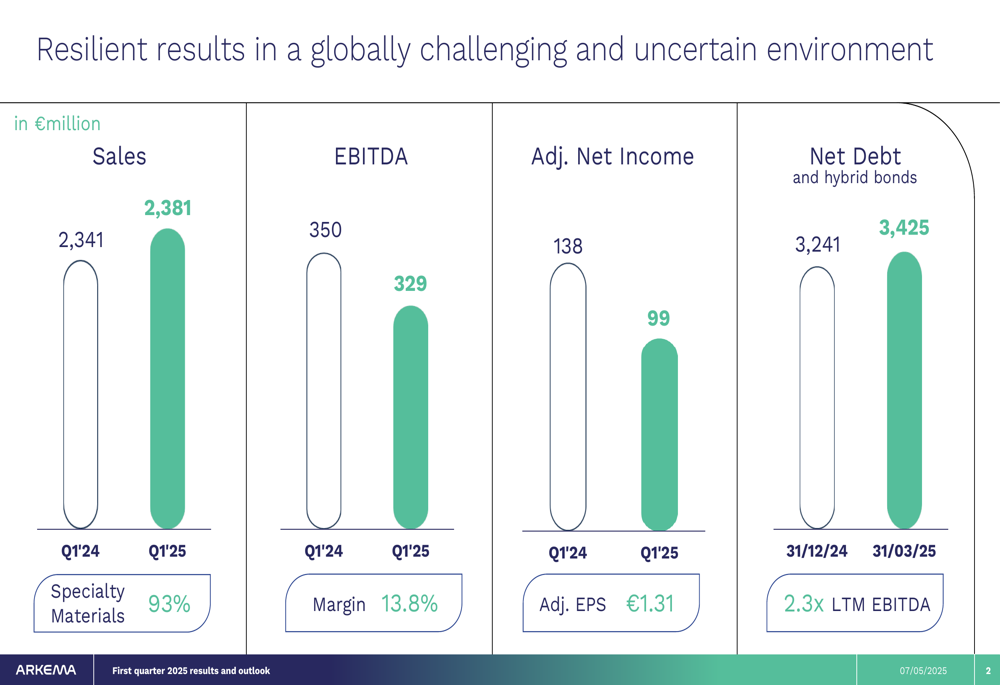

French specialty chemicals company Arkema SA (EPA:AKE) reported modest sales growth but declining profitability in its first quarter 2025 results presentation released on May 7. The company achieved a 1.7% year-over-year sales increase to €2,381 million, while EBITDA declined 6.0% to €329 million amid what the company described as a "globally challenging and uncertain environment."

Quarterly Performance Highlights

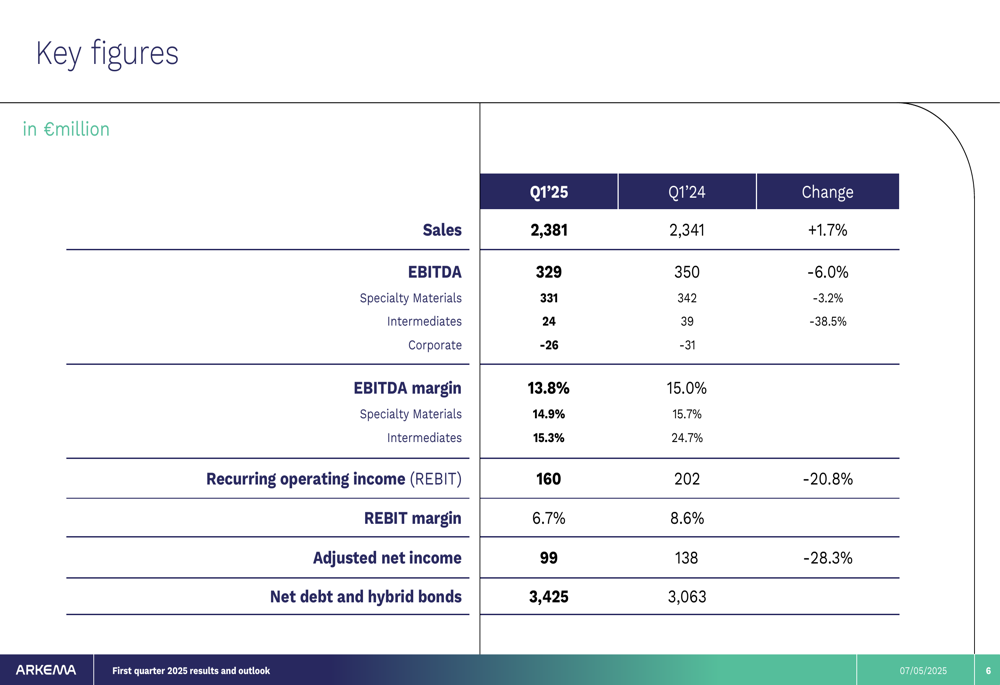

Arkema’s Q1 2025 results revealed contrasting performance across business segments and geographic regions. Sales grew slightly to €2,381 million, up 1.7% from Q1 2024, with Specialty Materials representing 93% of total sales. However, EBITDA fell 6.0% to €329 million, resulting in a margin compression to 13.8% from 15.0% in the prior-year period. Adjusted net income declined more significantly, falling 28.3% to €99 million (€1.31 per share).

As shown in the following financial highlights chart:

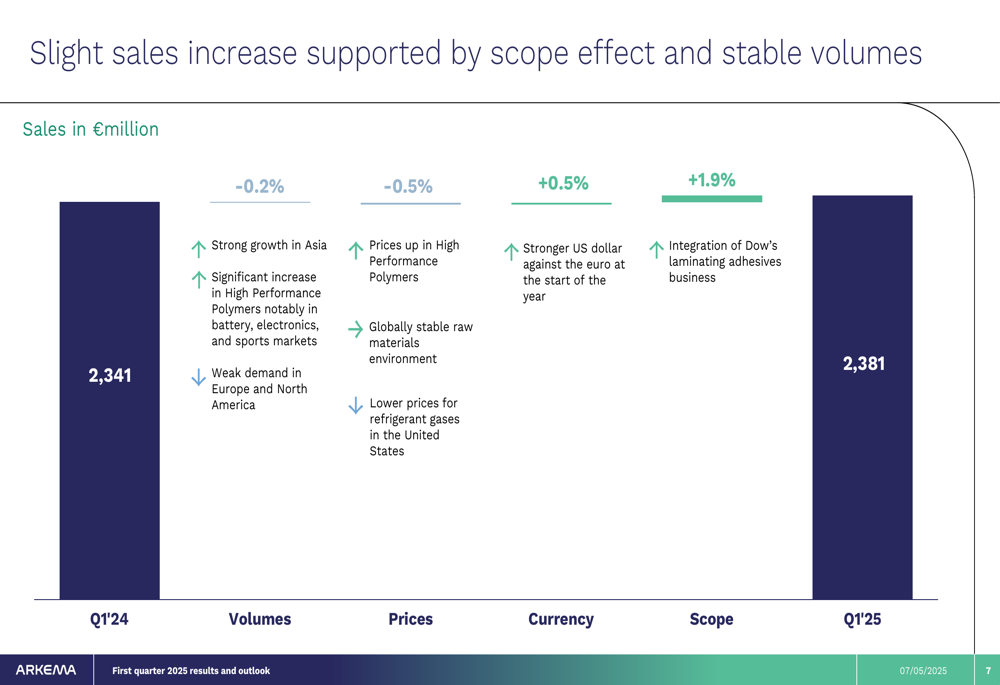

The company’s performance was supported by stable volumes (-0.2%) with strong growth in High Performance Polymers and significant growth in Asia offsetting weak demand in Europe and North America. Price effects were limited to a negative 0.5%, while the integration of Dow’s laminating adhesives business contributed a positive 1.9% scope effect.

The detailed breakdown of sales drivers illustrates these factors:

Segment Performance Analysis

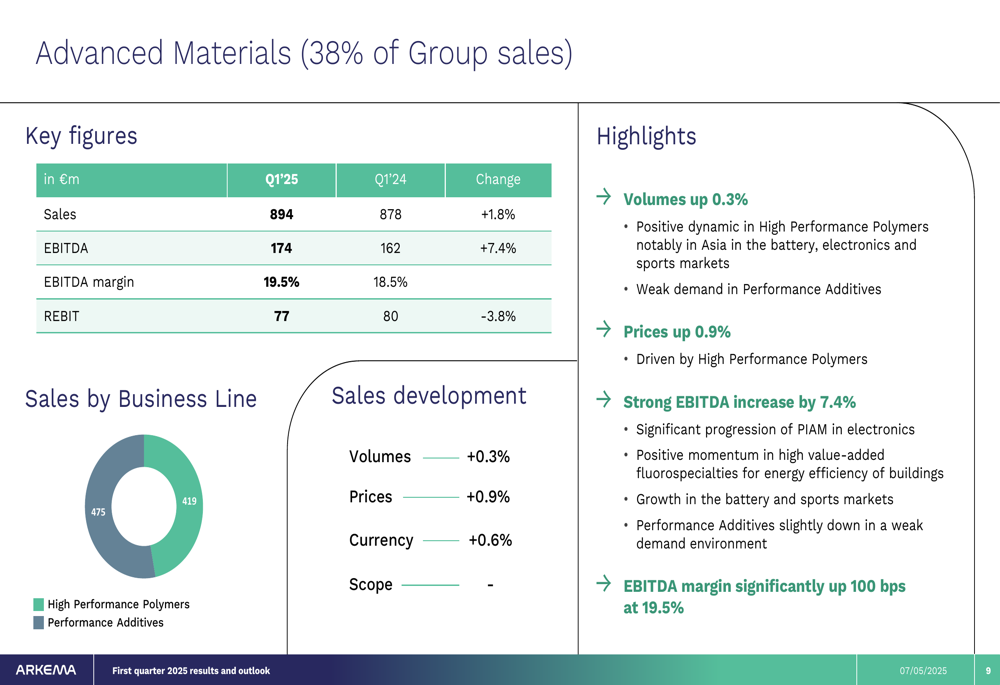

Arkema’s business segments showed dramatically different performance trajectories in Q1 2025. Advanced Materials emerged as the standout performer, while other segments faced more significant challenges.

Advanced Materials (38% of Group sales) delivered strong results with EBITDA increasing 7.4% to €174 million and margins expanding to 19.5%. This segment benefited from slight volume growth (+0.3%) and positive pricing (+0.9%).

In contrast, Adhesive Solutions (30% of Group sales) saw EBITDA decline 5.7% to €99 million despite a 5.1% sales increase that was primarily driven by the integration of Dow’s laminating adhesives business. Volumes declined 2.5% in this segment.

Coating Solutions (25% of Group sales) experienced the most significant profitability decline among the specialty materials segments, with EBITDA falling 22.7% to €58 million and margins compressing to 9.6% from 12.2%. This performance reflected weak demand with volumes down 2.5%.

The Intermediates segment, while representing only 7% of Group sales, saw EBITDA plummet 38.5% to €24 million despite volume growth of 15.8%, as prices fell 11.4% primarily due to lower refrigerant gas prices in the United States.

The following table provides a comprehensive view of the company’s financial performance:

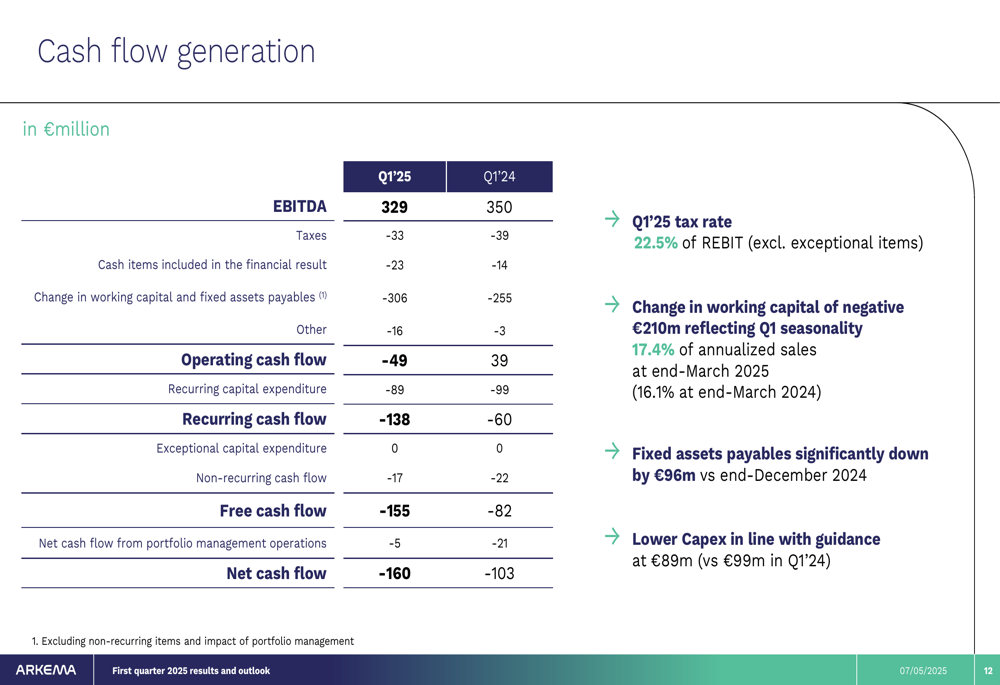

Cash Flow and Balance Sheet

Arkema’s cash generation was negative in Q1 2025, with recurring cash flow at negative €138 million compared to negative €60 million in Q1 2024. This decline was primarily due to lower EBITDA and a more significant increase in working capital, reflecting typical Q1 seasonality and a substantial €96 million reduction in fixed assets payables.

The detailed cash flow statement reveals these trends:

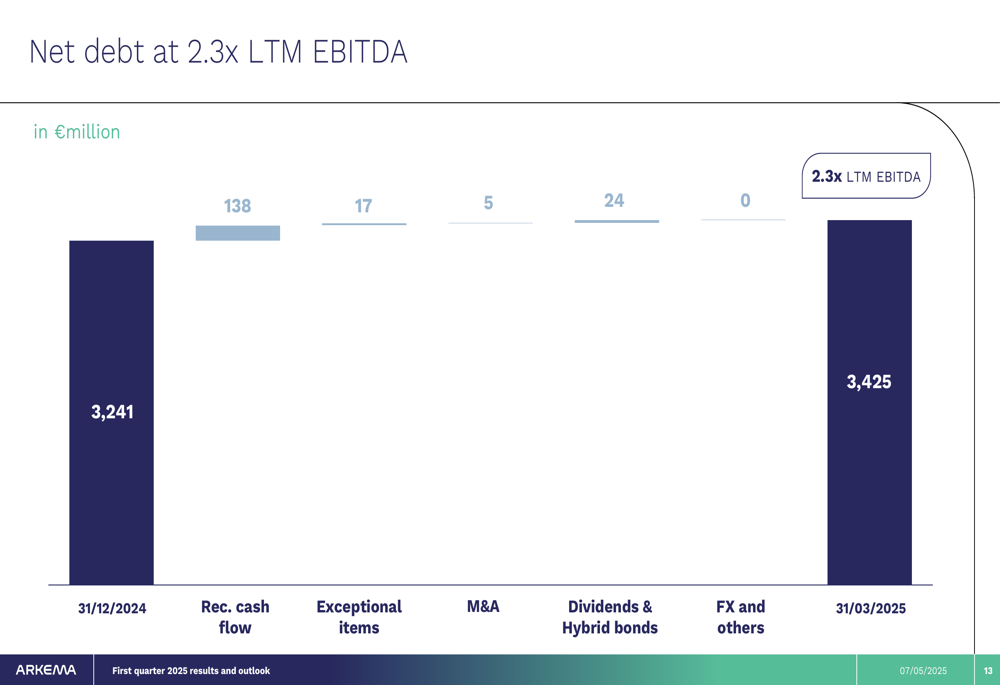

Net debt increased to €3,425 million as of March 31, 2025, up from €3,241 million at year-end 2024, resulting in a net debt to LTM EBITDA ratio of 2.3x. The following chart illustrates the drivers of this debt increase:

Strategic Initiatives

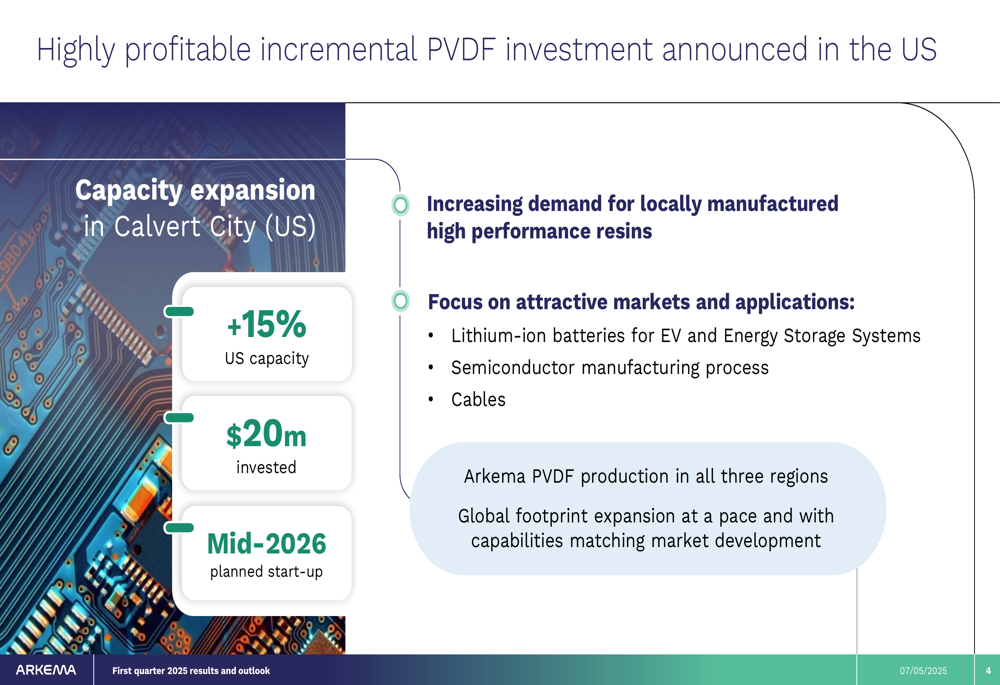

Despite financial headwinds, Arkema continues to invest in strategic growth initiatives and sustainability projects. The company announced a $20 million investment to expand PVDF capacity at its Calvert City, US facility by 15%, with planned start-up in mid-2026. This expansion targets high-growth applications including lithium-ion batteries for electric vehicles, semiconductor manufacturing, and cables.

Arkema also announced a new biomethane supply agreement with ENGIE covering four sites in France. The 8-year contract will provide 25 GWh/year of biomethane, covering 85% of the gas consumption of Arkema’s major Bostik sites in France. This agreement follows a larger 300 GWh/year contract signed in early 2023 for the Advanced Materials segment, underscoring the company’s commitment to decarbonization.

Outlook and Guidance

Looking ahead, Arkema described the global economic environment as "remaining uncertain and marked by weak demand outside of Asia." The company expects Q2 2025 to show relative continuity with Q1 trends, while highlighting two specific concerns: customer hesitation linked to tariff announcements and the evolution of exchange rates.

For full-year 2025, Arkema aims to achieve EBITDA at least equal to last year’s level at constant exchange rates and significantly increase recurring cash flow to approximately €600 million. This guidance appears more cautious than the €1.53-1.67 billion EBITDA range provided in the Q4 2024 earnings report.

The stock has faced pressure recently, trading at €65.10 as of May 6, 2025, down 2.62% and significantly below its 52-week high of €102.30. This continues a challenging trend following the company’s Q4 2024 earnings miss, when the stock dropped 4.67% after reporting EPS of €1.27 versus an expected €1.65.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.