Stifel bumps Nvidia stock target, sees attractive valuation

Introduction & Market Context

Arkema SA (EPA:AKE) released its second quarter 2025 results on July 31, showing continued pressure on financial performance amid challenging market conditions. The French specialty chemicals company reported declining sales and profitability compared to the same period last year, reflecting persistent weakness in demand across most end-markets, particularly in Europe and the US, alongside unfavorable currency effects.

Despite these headwinds, Arkema continues to advance its strategic initiatives, including investments in bio-based materials and capacity expansions, while implementing cost-cutting measures to navigate the difficult environment.

The company’s stock closed at €61.55 on July 30, down 1.83% ahead of the earnings release, and has declined significantly from its 52-week high of €88.40.

Quarterly Performance Highlights

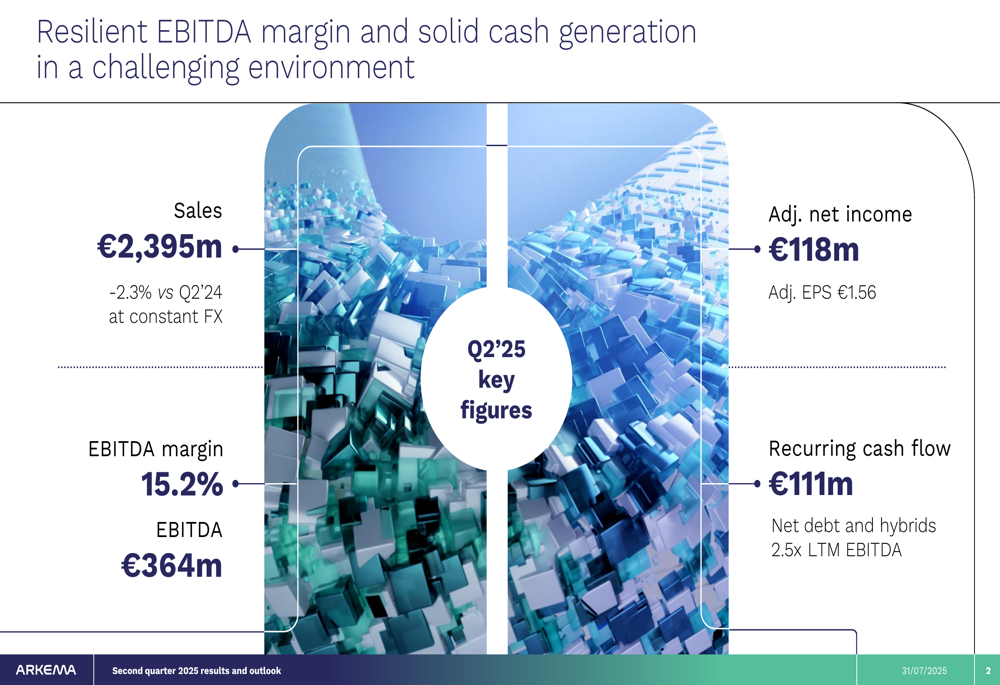

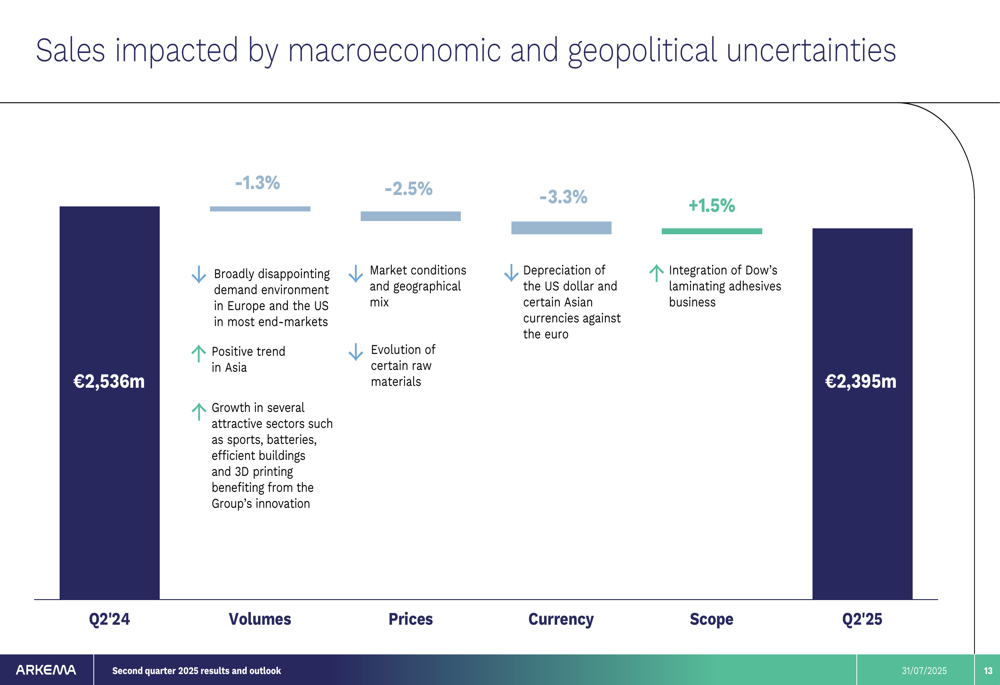

Arkema reported Q2 2025 sales of €2,395 million, representing a 2.3% year-over-year decrease at constant exchange rates. The decline was driven by slightly lower volumes (-1.3%), negative price effects (-2.5%), and significant currency headwinds (-3.3%), partially offset by a positive scope effect (+1.5%) from the integration of Dow’s laminating adhesives business.

As shown in the following key financial figures:

EBITDA fell to €364 million, down 19.3% compared to Q2 2024, resulting in an EBITDA margin of 15.2% versus 17.8% in the prior-year period. Adjusted net income declined sharply to €118 million (€1.56 per share), representing a 44.9% decrease from Q2 2024.

The sales decline was influenced by multiple factors, as illustrated in this breakdown:

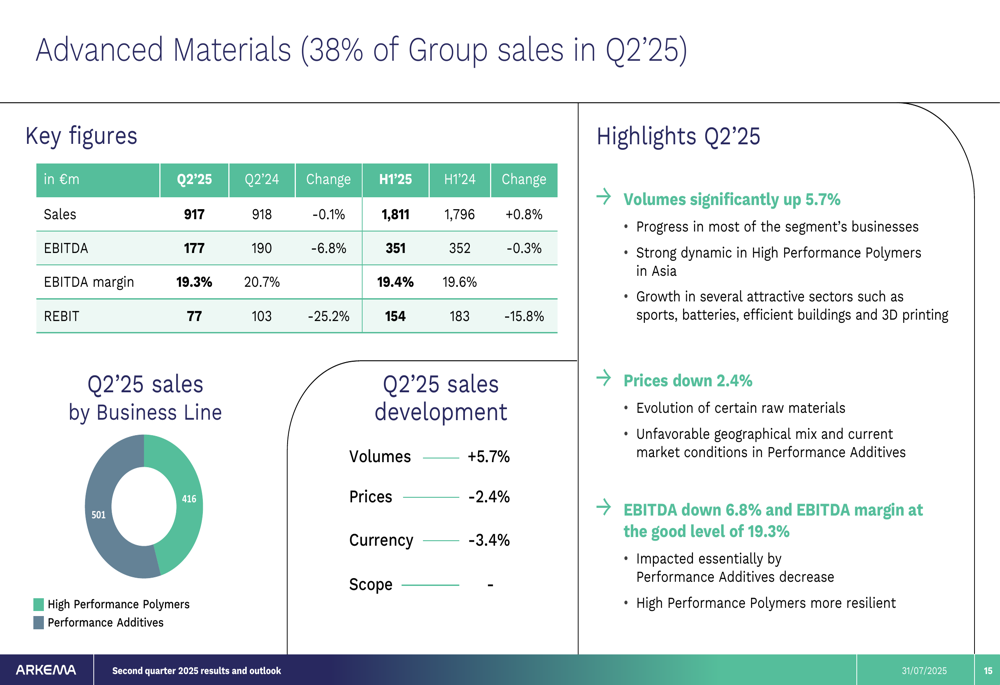

Performance varied significantly across business segments. Advanced Materials (38% of Group sales) demonstrated resilience with volumes up 5.7%, though EBITDA declined 6.8% to €177 million. Adhesive Solutions (30% of sales) maintained a solid EBITDA margin of 14.4% despite a 5.5% drop in EBITDA to €103 million. However, Coating Solutions and Intermediates experienced more substantial declines, with EBITDA falling 41.8% and 35.7%, respectively.

Strategic Initiatives

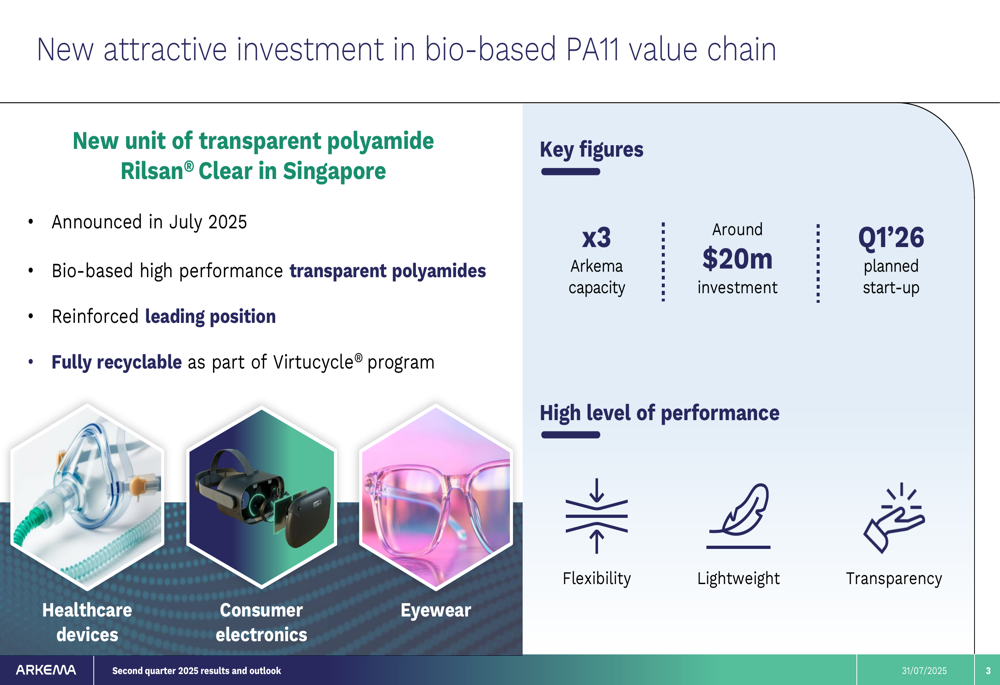

Despite current market challenges, Arkema continues to execute its long-term growth strategy focused on specialty materials and sustainability. The company announced new investments in high-performance materials, including:

A new bio-based PA11 value chain investment in Singapore, specifically for transparent polyamide Rilsan® Clear, as detailed below:

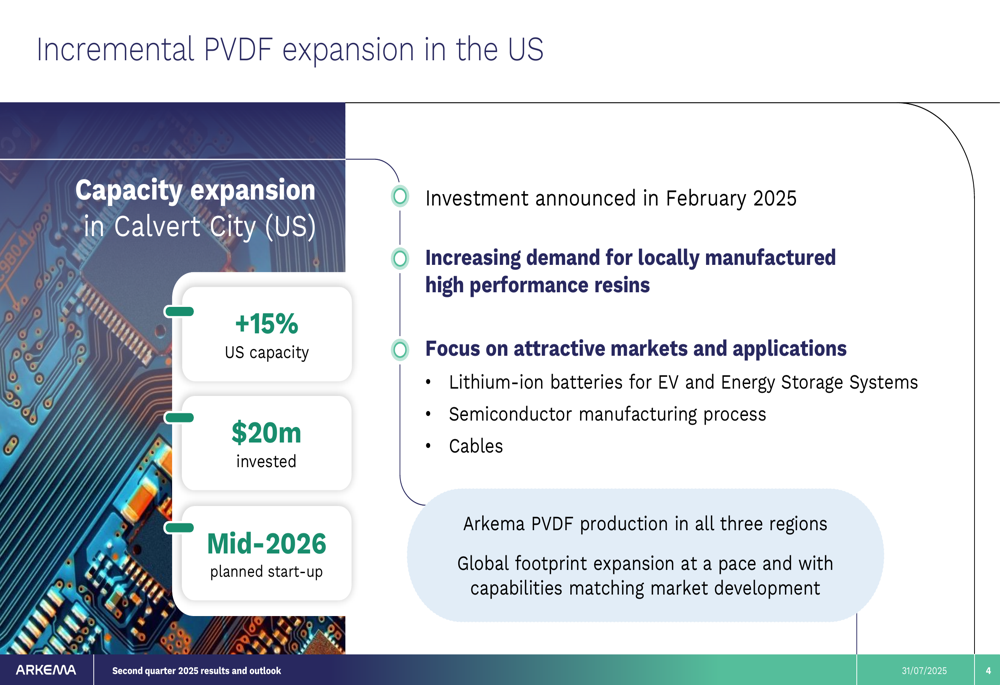

Additionally, Arkema is expanding its PVDF (Polyvinylidene Fluoride) capacity in the United States to meet increasing demand for locally manufactured high-performance resins used in lithium-ion batteries, semiconductor manufacturing, and cables:

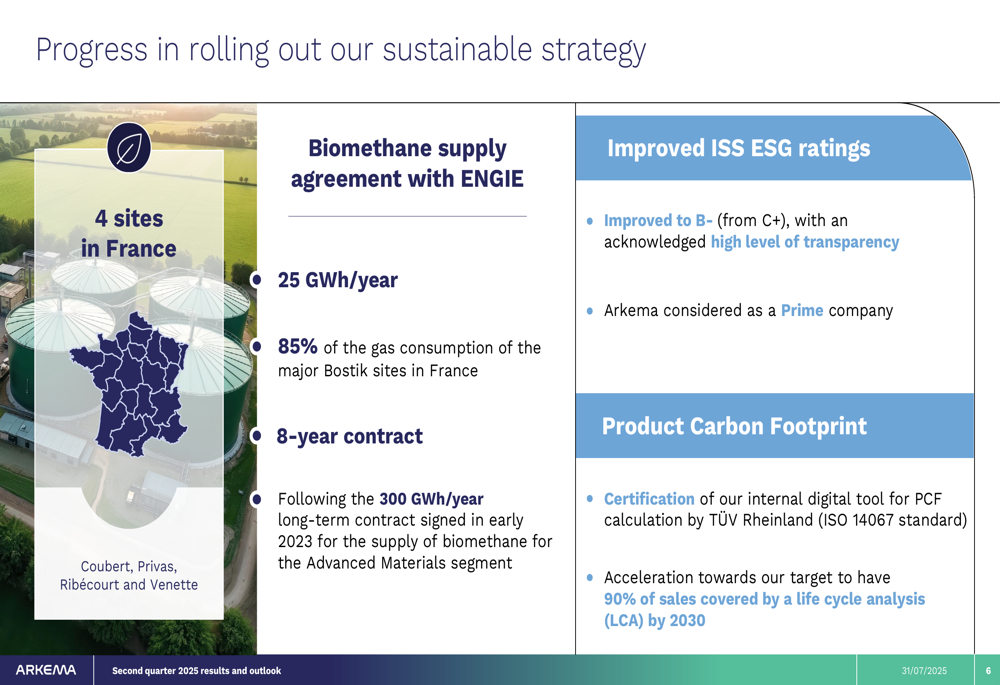

The company continues to make progress on its sustainable strategy, including a biomethane supply agreement with ENGIE covering four sites in France, improved ESG ratings, and advancements in product carbon footprint certification:

Arkema’s strategic roadmap includes the gradual ramp-up of major projects that are expected to contribute over €400 million in additional EBITDA by 2028 compared to 2024:

Financial Position

Despite challenging market conditions, Arkema maintained solid cash generation with recurring cash flow of €111 million in Q2 2025, though this represents a decline from €132 million in Q2 2024:

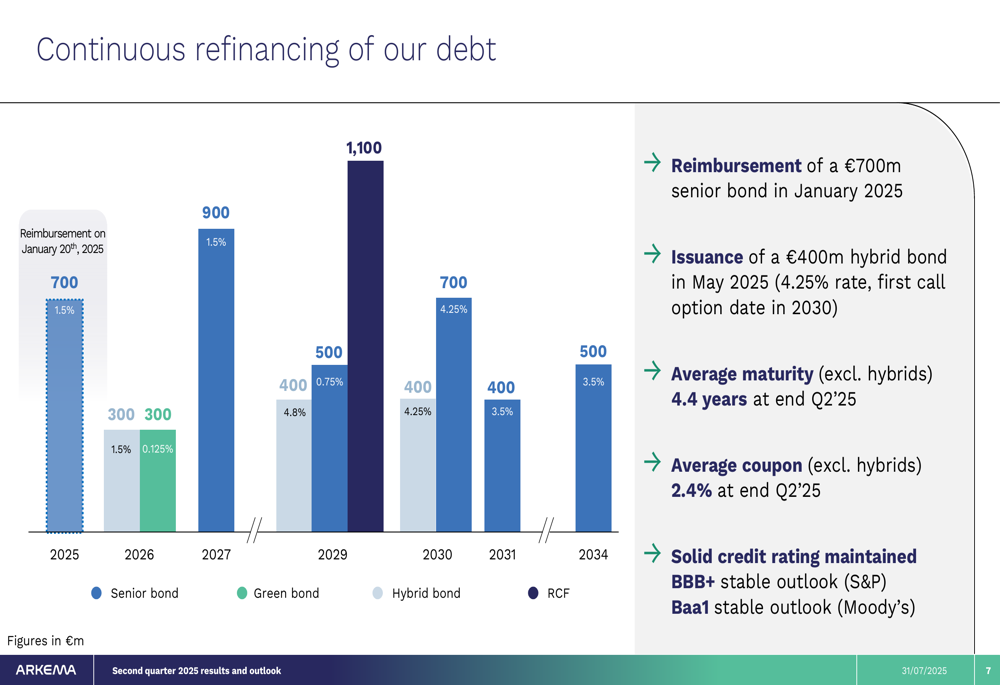

The company continues to manage its debt profile actively, having reimbursed a €700 million senior bond in January 2025 and issued a €400 million hybrid bond in May 2025. As of Q2 2025, Arkema’s average debt maturity (excluding hybrids) stood at 4.4 years with an average coupon of 2.4%, while maintaining solid credit ratings:

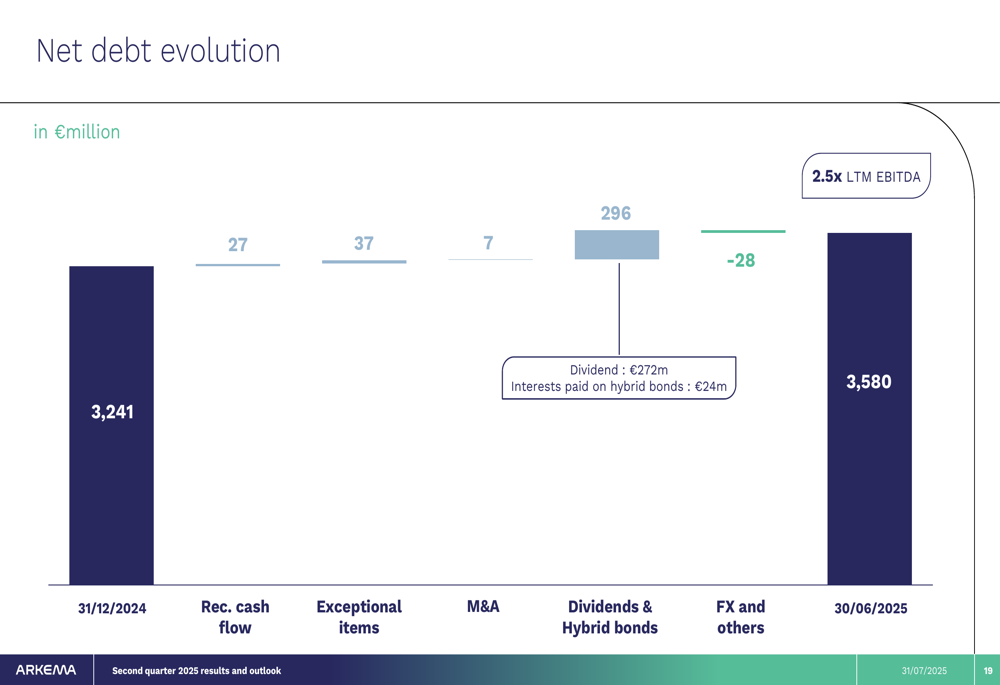

Net debt and hybrid bonds totaled €3,580 million at the end of Q2 2025, representing 2.5x last twelve months EBITDA, an increase from €3,241 million at the end of 2024:

Forward-Looking Statements

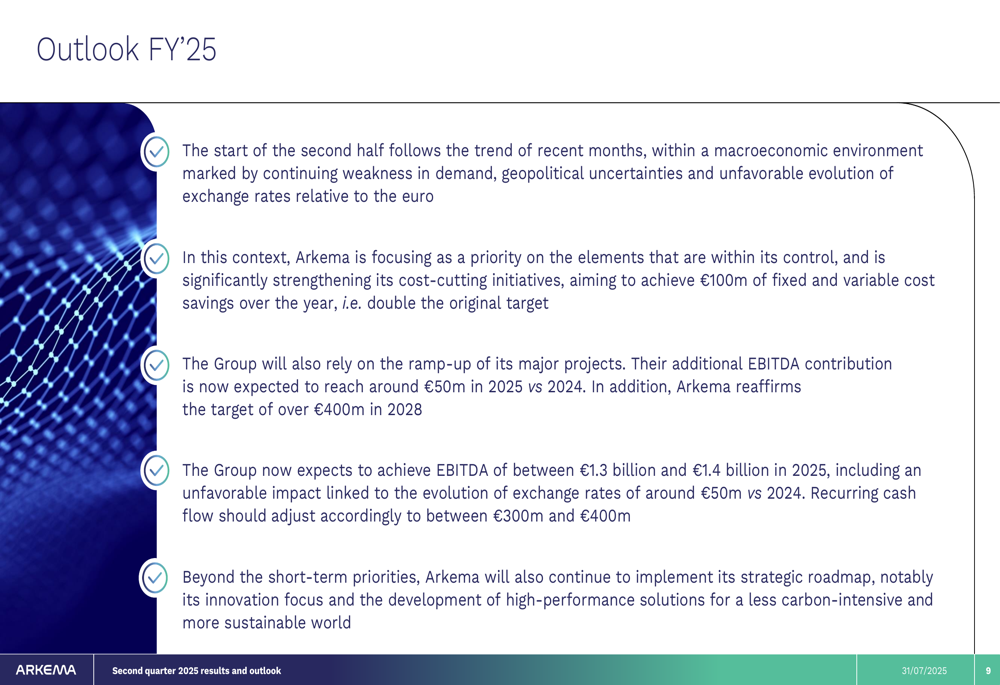

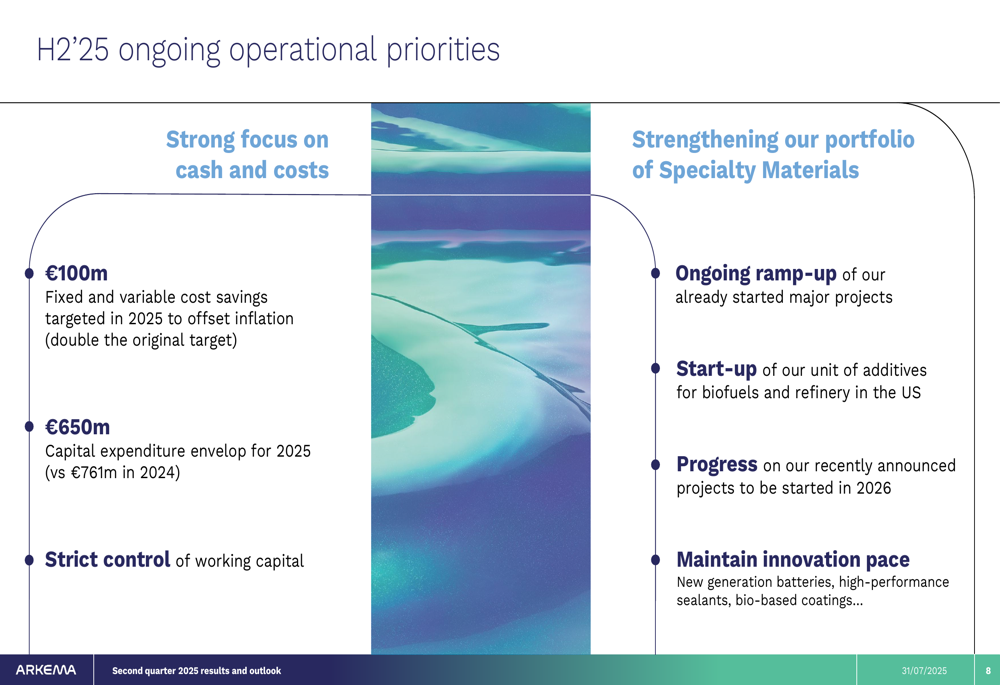

Looking ahead, Arkema expects the challenging market environment to persist in the second half of 2025, with continuing weakness in demand, geopolitical uncertainties, and unfavorable exchange rates. In response, the company is strengthening its cost-cutting initiatives, targeting €100 million in fixed and variable cost savings in 2025 to offset inflation.

For the full year 2025, Arkema forecasts:

The company’s operational priorities for H2 2025 include a strong focus on cash and costs, with strict control of working capital and a €650 million capital expenditure envelope for the year. Arkema will also continue strengthening its portfolio of specialty materials through the ramp-up of major projects and maintaining innovation momentum:

While near-term challenges persist, Arkema remains committed to its long-term strategic roadmap focused on high-performance specialty materials and sustainable solutions, positioning the company to benefit from eventual market recovery and growth in attractive sectors such as batteries, sports goods, and bio-based materials.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.