Tyson Foods to close major Nebraska beef plant amid cattle shortage - WSJ

Introduction & Market Context

Arlo Technologies (NYSE:ARLO) showcased its transformation into a subscription-based software business during its November 6, 2025, investor presentation, highlighting strong third-quarter results that exceeded analyst expectations. Despite reporting an EPS of $0.16 against a forecast of $0.15 and revenue of $139.5 million slightly above the expected $138.69 million, the company's stock fell 4.35% to $17.58 in after-hours trading, reflecting investor concerns about future guidance.

The presentation emphasized Arlo's positioning in the $25 billion U.S. smart home security market, which remains largely underpenetrated with only 7% of U.S. homes subscribing to paid smart home security services. This market opportunity, combined with Arlo's rapid transformation into a subscription software business, forms the cornerstone of the company's growth strategy.

Quarterly Performance Highlights

Arlo reported impressive SaaS metrics for Q3 2025, achieving what it calls "Rule of 40+" performance for two consecutive quarters. The company highlighted its annual recurring revenue (ARR) of $323 million, representing 34% year-over-year growth, alongside a subscription and services gross margin of 85%.

As shown in the following snapshot of Arlo's key performance indicators:

The company's paid accounts reached 5.4 million, while subscriptions and services now represent 57% of total revenue. This shift toward a subscription-based model has significantly improved Arlo's financial profile, with the Rule of 40 metric (combining growth rate and profit margin) reaching 46% in the quarter.

Arlo's churn rate of just 1.0% stands out as a particular strength when compared to other popular subscription services:

This low churn rate underscores the essential nature of security services for consumers, with Arlo noting that security ranks first among subscriptions least likely to be canceled. This provides the company with a stable revenue base and predictable cash flows compared to entertainment-focused subscription businesses.

Detailed Financial Analysis

Arlo's financial transformation is evident in its growing paid account base and rapidly expanding ARR. As illustrated in the following chart, both metrics have shown consistent growth over the past two years:

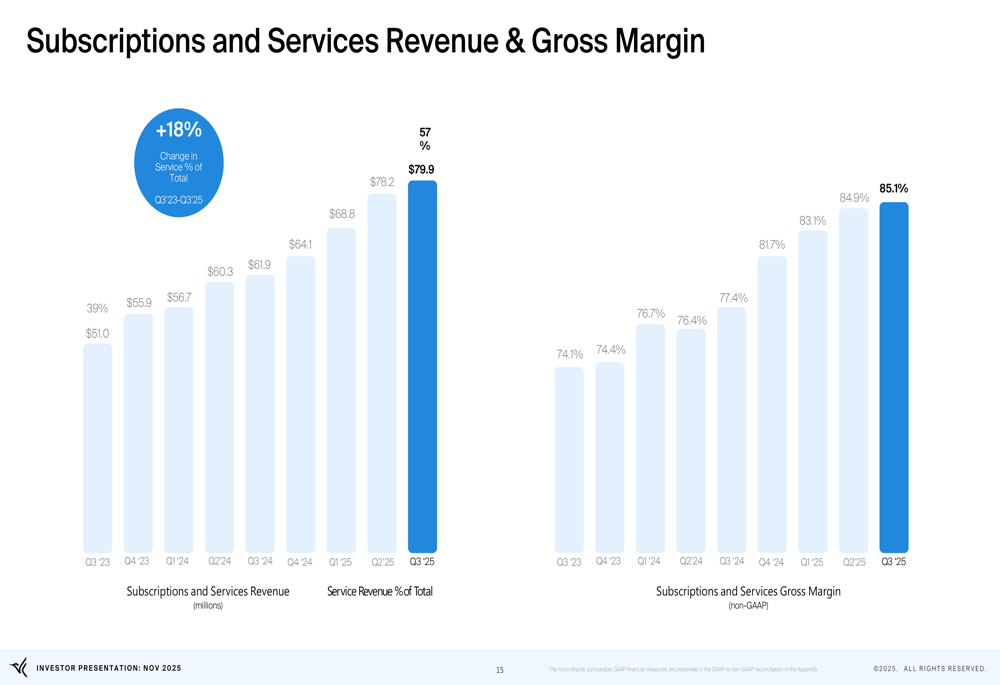

The company's subscription and services revenue has similarly shown strong growth, reaching $79.9 million in Q3 2025, a 29% increase year-over-year according to the earnings report. More importantly, the gross margin for this segment has expanded significantly, reaching 85.1% in Q3 2025 compared to 74.1% in Q3 2023:

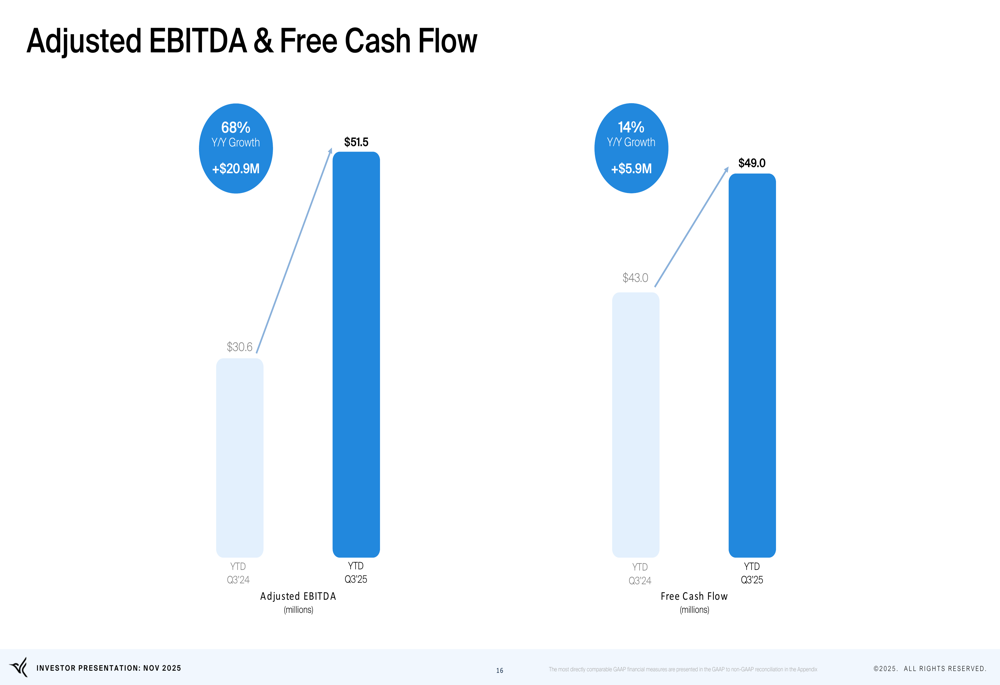

This margin expansion demonstrates the scalability of Arlo's platform and the improving economics of its subscription business. The company's profitability metrics have also shown substantial improvement, with adjusted EBITDA increasing 68% year-over-year to $51.5 million (YTD Q3'25) and free cash flow growing 14% to $49 million for the same period:

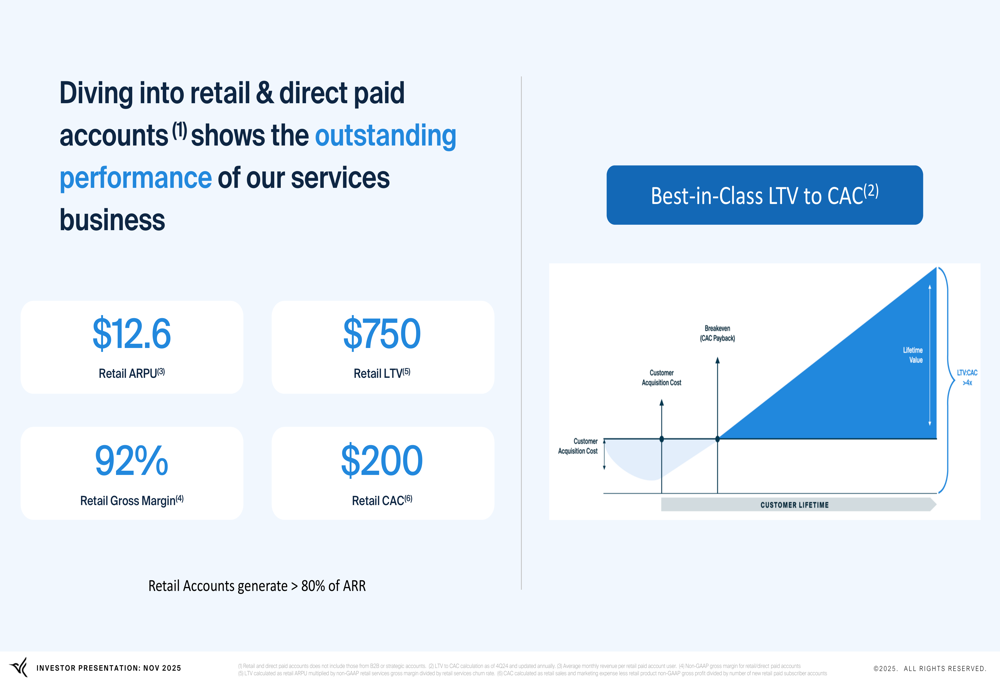

Retail accounts have emerged as a key driver of Arlo's business, generating over 80% of ARR with attractive unit economics. These accounts deliver a $12.6 average revenue per user (ARPU), a lifetime value of $750, and a gross margin of 92%, resulting in a lifetime value to customer acquisition cost ratio of nearly 4x:

Strategic Initiatives

Arlo's presentation emphasized its AI-powered SaaS platform as a key differentiator. The company's Arlo Intelligence features include sophisticated object and event detection capabilities:

These AI capabilities enable Arlo to deliver higher-value services that drive subscription adoption and ARPU growth. The company's platform processes over 170 billion AI alerts annually and manages over 1,700 hours of video per minute, demonstrating its robust technological infrastructure.

Arlo outlined its SaaS business model, which focuses on four interconnected strategies:

This model highlights Arlo's approach to customer acquisition through retail channels and strategic partnerships, conversion to paid accounts, ARPU expansion through AI-powered services, and revenue growth with high SaaS margins.

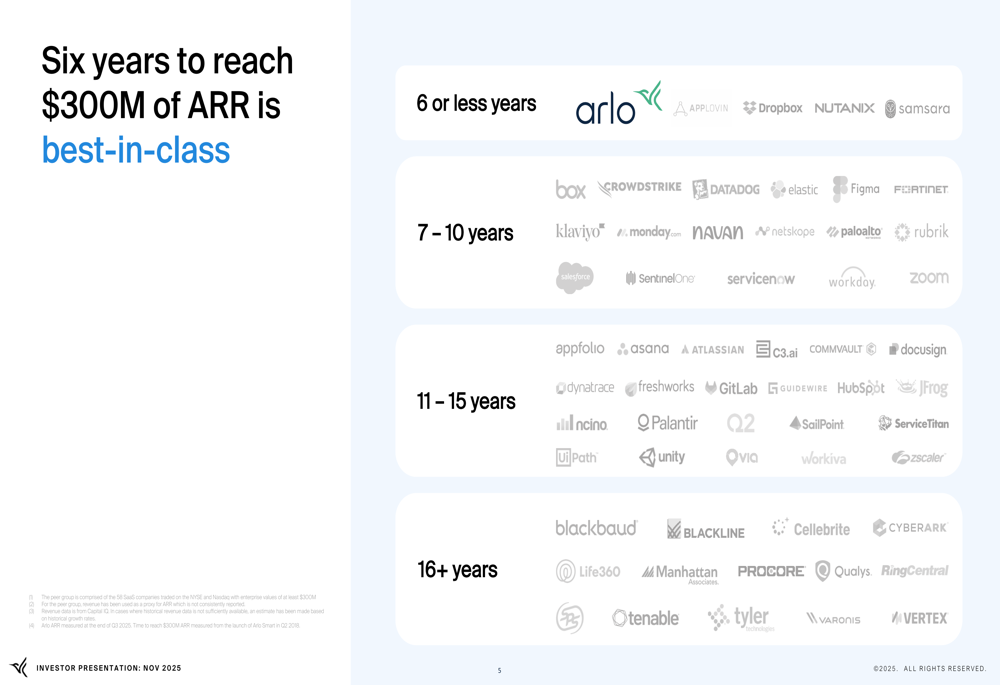

The company also benchmarked its growth against other SaaS companies, noting that it reached $300 million in ARR in six years or less, placing it among "best-in-class" performers:

Forward-Looking Statements

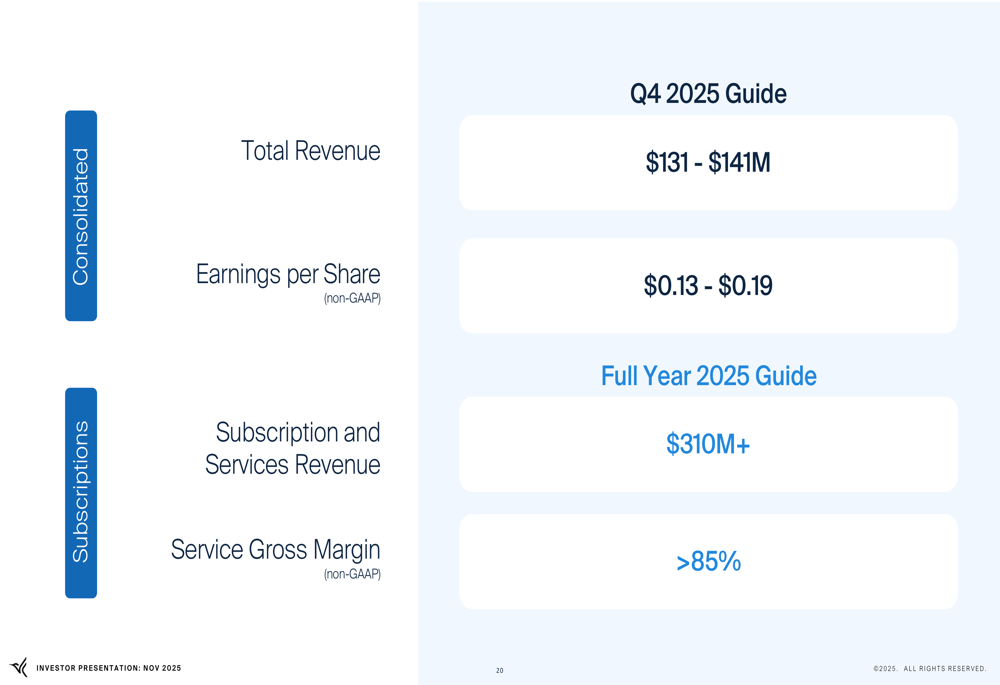

For Q4 2025, Arlo provided revenue guidance of $131-141 million and non-GAAP earnings per share between $0.13 and $0.19:

For the full year 2025, the company expects subscription and services revenue to exceed $310 million with service gross margins remaining above 85%. This guidance, particularly the Q4 revenue projection being potentially lower than Q3 results, may have contributed to the stock's decline despite the earnings beat.

Looking further ahead, Arlo has updated its long-range plan with ambitious targets for 2030, including 10 million paid accounts (double the original goal), $700 million in ARR, and an adjusted EBITDA margin exceeding 25%. These targets represent significant increases from the original plan announced in March 2022.

CEO Matthew McRae highlighted the company's dual capabilities in software services and hardware devices during the earnings call, stating, "There are very few companies in the world that have successfully developed world-class capabilities in both segments." However, investors may be concerned about challenges including tariff impacts on product margins, market saturation, and competitive pressures from established brands in retail channels.

As Arlo continues its transformation into a subscription-based business, its ability to maintain growth while improving margins will be crucial for meeting its ambitious long-term targets and convincing investors of its SaaS valuation potential.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.