Daiichi Sankyo and Merck report phase 2 trial results for lung cancer drug

Introduction & Market Context

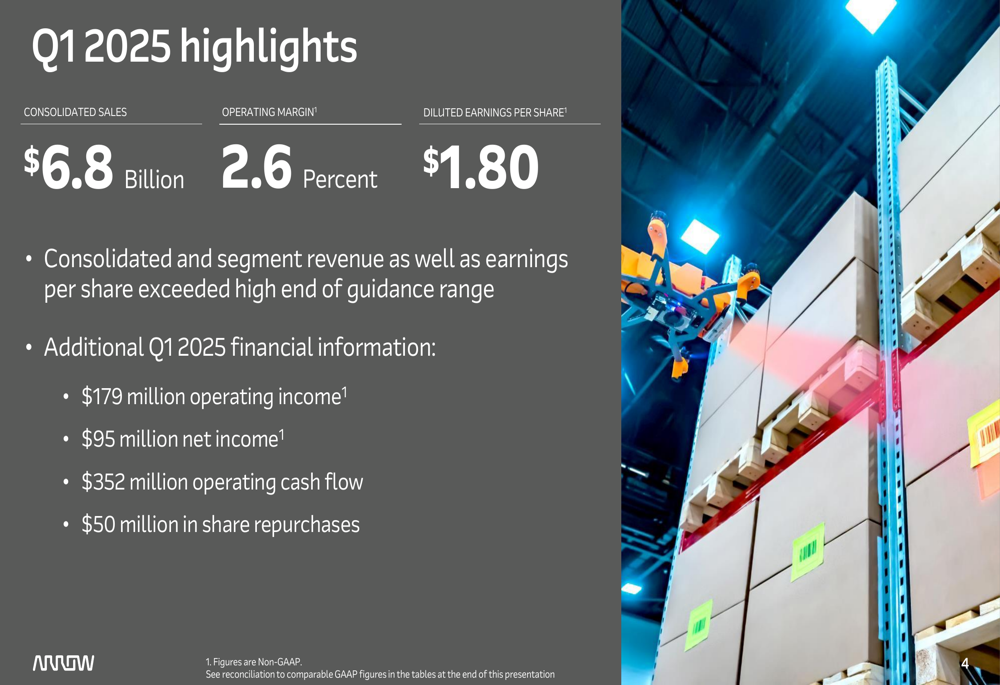

Arrow Electronics Inc. (NYSE:ARW) presented its first quarter 2025 earnings results on May 1, 2025, reporting consolidated sales of $6.8 billion and non-GAAP earnings per share of $1.80, exceeding Wall Street expectations of $1.44. The company’s stock responded positively with a modest 0.75% increase, trading at $112.19 following the announcement.

The results demonstrate Arrow’s resilience in navigating a challenging market environment, with the Enterprise Computing Solutions (ECS) segment’s strong performance helping to offset continued softness in the Global Components business. Management highlighted improving demand trends and positive momentum across both segments.

Quarterly Performance Highlights

Arrow Electronics delivered $6.8 billion in consolidated sales for Q1 2025, representing a 2% year-over-year decline but exceeding analyst expectations. The company reported non-GAAP operating income of $179 million with an operating margin of 2.6%, along with non-GAAP net income of $95 million.

As shown in the following financial highlights slide:

The company generated strong operating cash flow of $352 million and continued its shareholder return program with $50 million in share repurchases during the quarter. While the operating margin of 2.6% represents a decline from 3.6% in the same quarter last year, it reflects the current market challenges in the components sector.

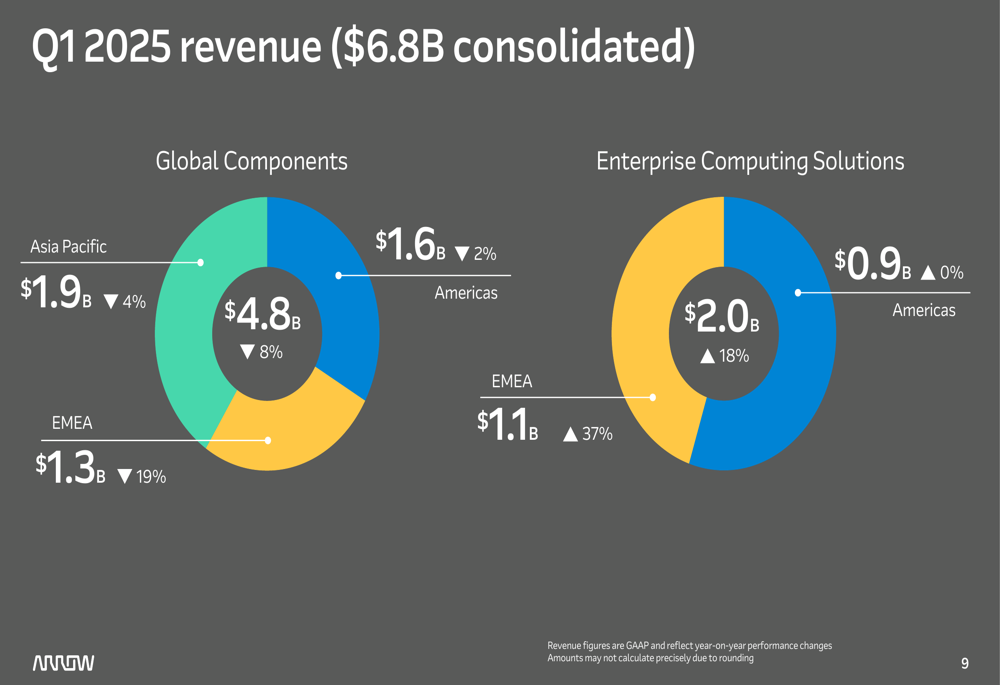

A detailed breakdown of revenue by segment and region reveals divergent performance:

The Global Components segment, which accounts for approximately 70% of total revenue, generated $4.8 billion in sales, down 8% year-over-year. In contrast, the Enterprise Computing Solutions segment delivered $2.0 billion, representing an 18% increase compared to Q1 2024.

Segment Analysis

The Global Components segment faced ongoing challenges but showed signs of stabilization. According to management, all three regions performed ahead of typical seasonal patterns, with key leading indicators showing improvement.

In the components business, Arrow noted that regional book-to-bill ratios were at or above parity, with growing backlog and customer inventory trending toward replenishment. The EMEA region demonstrated particular strength in industrial applications, transportation, and aerospace & defense sectors.

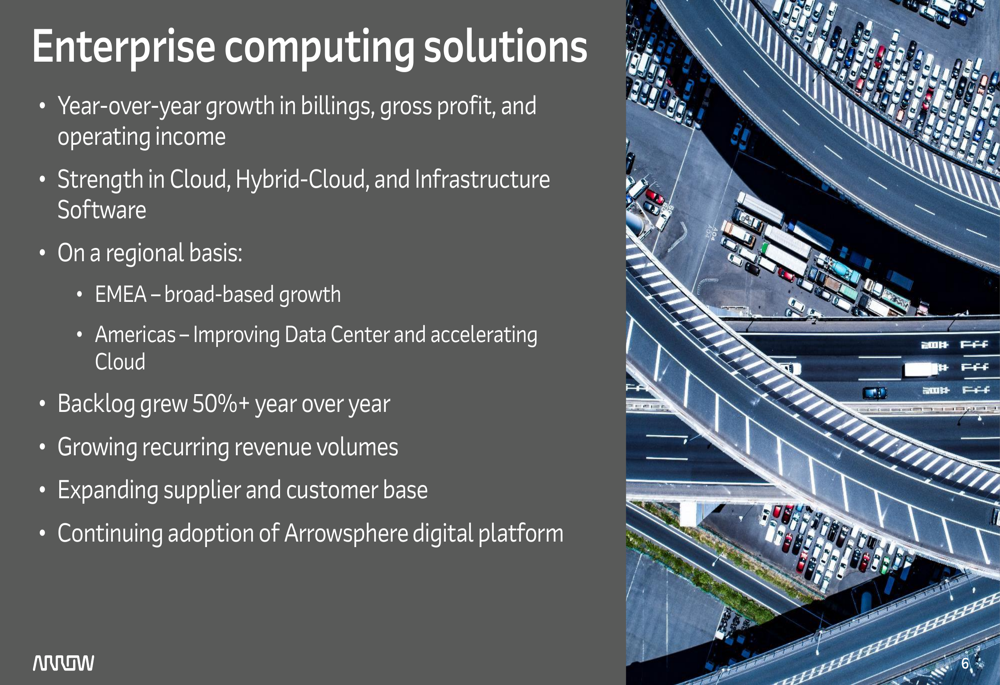

Meanwhile, the Enterprise Computing Solutions segment continued its strong performance trajectory:

The ECS business saw broad-based growth, particularly in Cloud, Hybrid-Cloud, and Infrastructure Software (ETR:SOWGn). The segment’s backlog grew by more than 50% year-over-year, with EMEA showing broad-based growth and Americas improving in Data Center and accelerating Cloud adoption. The company also highlighted growing recurring revenue volumes and continued adoption of its Arrowsphere digital platform.

Financial Position

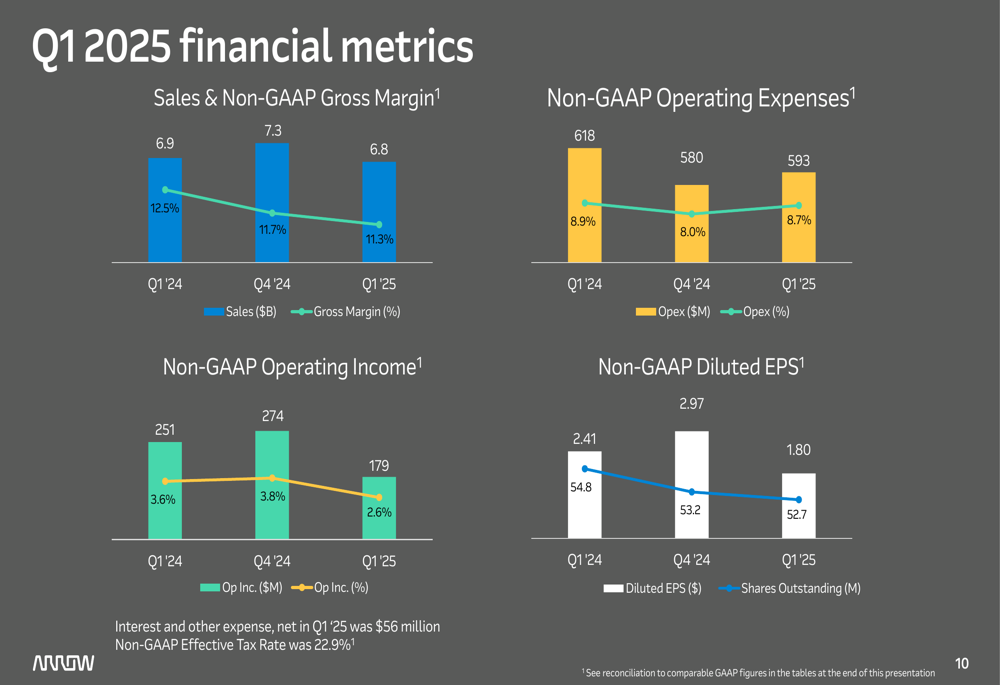

Arrow’s financial metrics for the quarter show year-over-year declines in several key areas, though sequential improvements in some metrics suggest potential stabilization:

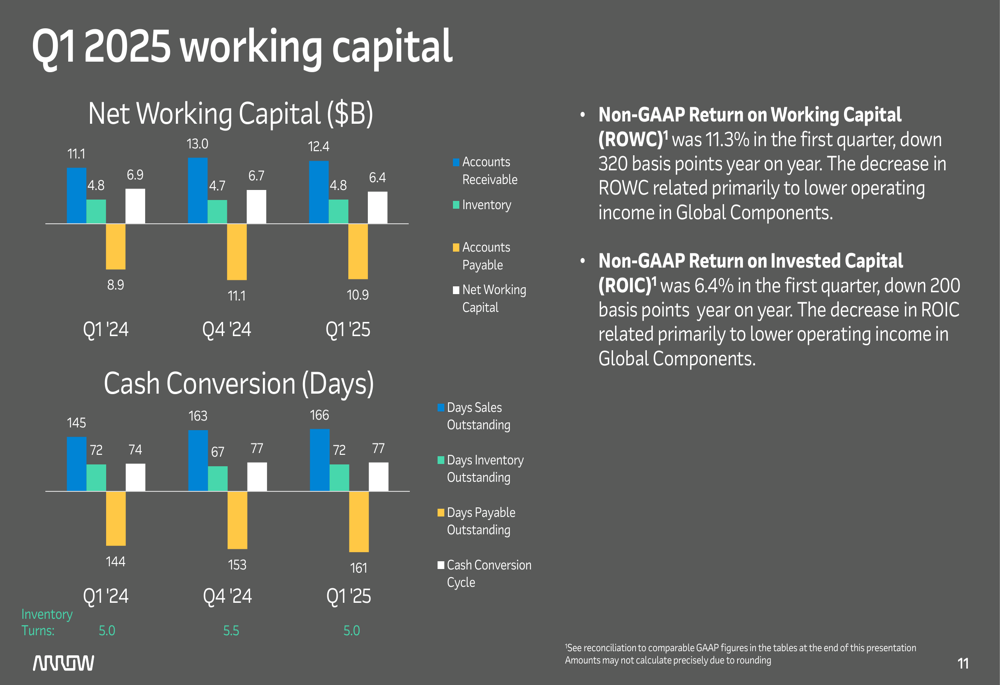

Working capital metrics reveal the operational challenges facing the company, particularly in the Global Components segment:

Non-GAAP Return on Working Capital (ROWC) was 11.3%, down 320 basis points year-over-year, while Non-GAAP Return on Invested Capital (ROIC) was 6.4%, down 200 basis points. Both decreases were primarily attributed to lower operating income in the Global Components segment.

Despite these challenges, Arrow maintained a strong balance sheet with $2.8 billion in gross debt and generated $352 million in operating cash flow during the quarter, continuing its track record of positive cash flow generation.

Forward Guidance

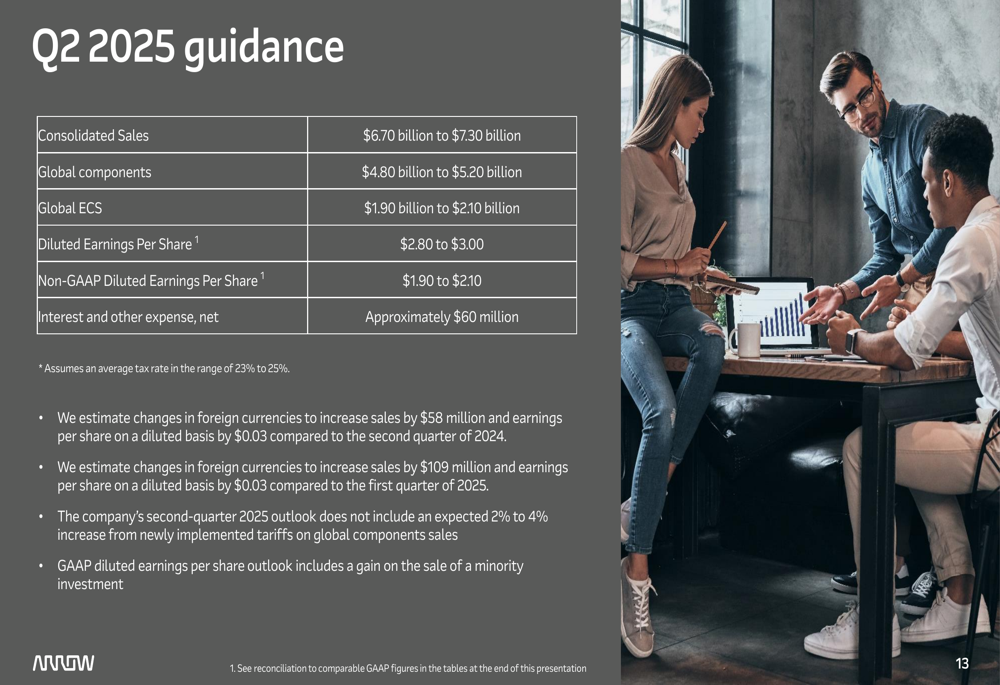

Looking ahead to Q2 2025, Arrow Electronics provided the following guidance:

The company expects consolidated sales between $6.70 and $7.30 billion, with Global Components sales of $4.80 to $5.20 billion and Global ECS sales of $1.90 to $2.10 billion. Non-GAAP diluted earnings per share are projected to be between $1.90 and $2.10.

Management noted that changes in foreign currencies are expected to increase sales by $58 million and earnings per share by $0.03 compared to Q2 2024. Additionally, the outlook does not include an expected 2% to 4% increase from newly implemented tariffs on global components sales.

Executive Commentary and Outlook

During the earnings presentation, CEO Sean Kerins expressed optimism about Arrow’s market position and future prospects. "We’re seeing positive momentum across both segments and improving demand trends," noted Kerins, while emphasizing the company’s focus on "factors within our control" and the resilience of Arrow teams globally.

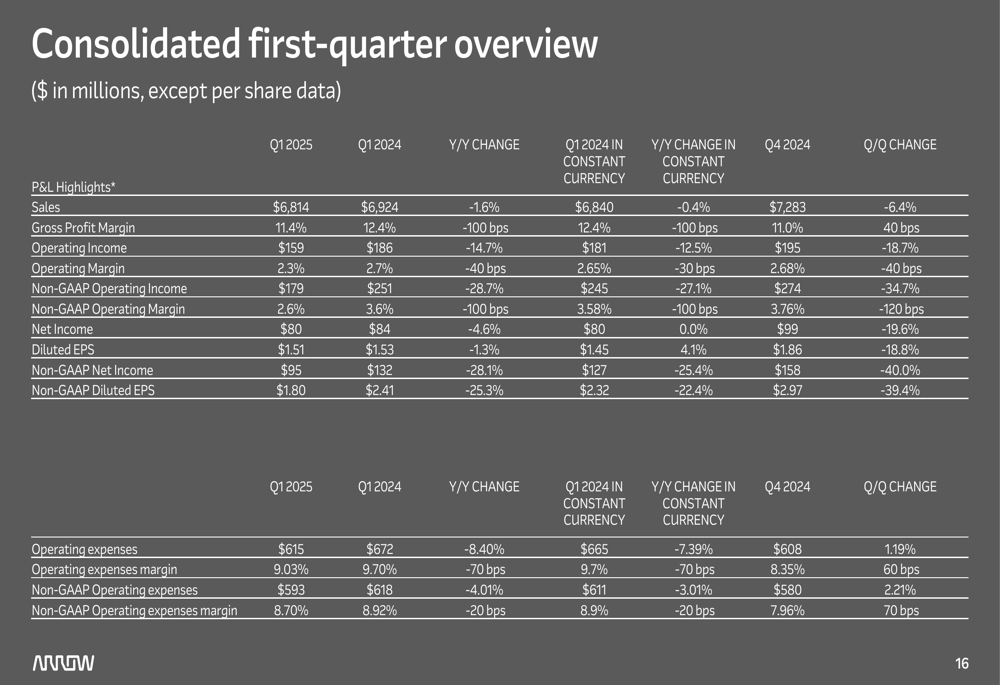

The company’s consolidated first-quarter overview provides additional context for its performance:

Management’s commentary during the earnings call suggested a potential cyclical turning point, with CEO Kerins stating, "We believe we’re at a modest turning point" and noting that "visibility is improving." These statements, combined with the improving book-to-bill ratios and growing backlog, indicate cautious optimism for the remainder of 2025.

Conclusion

Arrow Electronics’ Q1 2025 results demonstrate the company’s ability to navigate challenging market conditions while positioning itself for future growth. The strong performance in the Enterprise Computing Solutions segment, particularly in cloud and infrastructure software, helped offset ongoing challenges in the components business.

With improving demand indicators, a strong cash position, and strategic focus on high-growth areas, Arrow appears well-positioned to capitalize on potential market improvements in the coming quarters. However, investors should remain attentive to ongoing challenges in the components segment and potential impacts from newly implemented tariffs.

The company’s guidance for Q2 2025 suggests modest sequential improvement, with management expressing increasing confidence in the second half outlook. As Arrow continues to execute its strategy of balancing short-term performance with long-term growth initiatives, the divergent performance of its two main segments bears watching as a key indicator of overall company trajectory.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.