China’s Xi speaks with Trump by phone, discusses Taiwan and bilateral ties

Introduction & Market Context

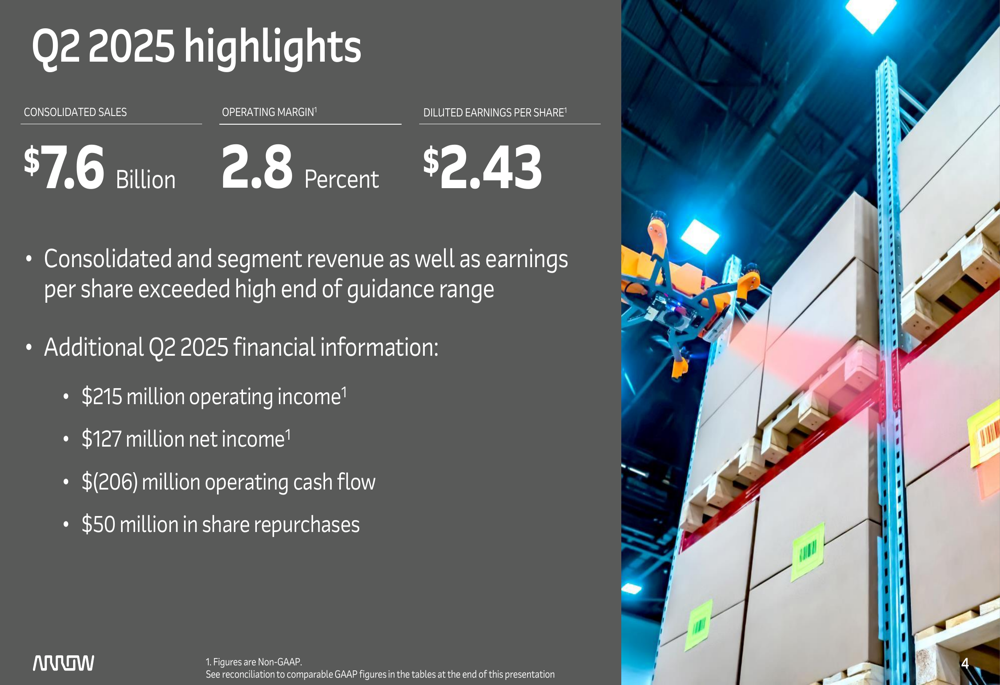

Arrow Electronics, Inc. (NYSE:ARW) released its second-quarter 2025 earnings presentation on July 31, 2025, reporting consolidated sales of $7.6 billion, a 10% increase year-over-year. The company's stock responded positively to the results, rising 1.94% to close at $113.65 following the announcement.

The electronic components distributor and enterprise computing solutions provider delivered solid growth across both business segments, with particularly strong performance in its Enterprise Computing Solutions (ECS) division. However, the company also faced margin pressure, with non-GAAP operating margin declining to 2.8% from 3.8% in the same period last year.

Quarterly Performance Highlights

Arrow's second-quarter results demonstrated resilience in a challenging market environment. The company reported consolidated sales of $7.6 billion, non-GAAP operating income of $215 million, and diluted earnings per share of $2.43 on a non-GAAP basis. While sales increased, the company experienced a decline in operating margin compared to the prior year.

As shown in the following financial highlights slide, Arrow generated $127 million in non-GAAP net income and repurchased $50 million in shares during the quarter:

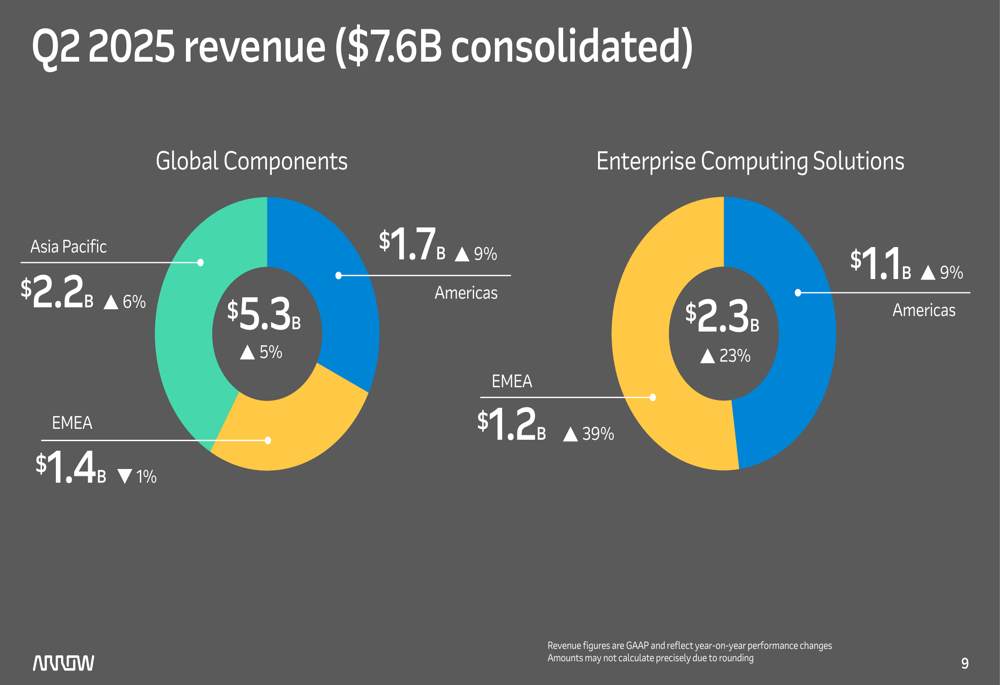

Breaking down the revenue by segment, Global Components accounted for $5.3 billion (70% of total revenue), while Enterprise Computing Solutions contributed $2.3 billion (30%). Geographically, Asia Pacific led the Global Components segment with $2.2 billion in sales, followed by Americas at $1.7 billion and EMEA at $1.4 billion.

The following revenue breakdown illustrates the distribution across segments and regions:

Detailed Financial Analysis

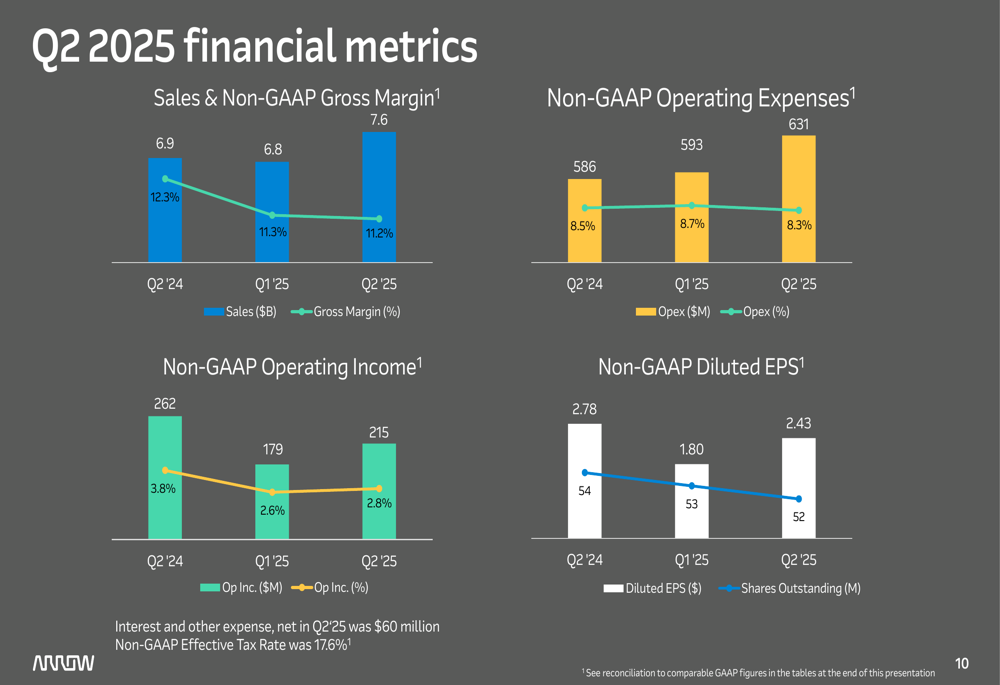

Arrow's financial metrics reveal a mixed performance picture. While sales increased by 10% year-over-year, the company experienced margin compression. Non-GAAP gross margin decreased to 11.2% from 12.3% in Q2 2024, a decline of 110 basis points. Non-GAAP operating margin also contracted to 2.8% from 3.8% in the prior-year period.

The following chart illustrates key financial metrics over the past three quarters, showing the trends in sales, gross margin, operating expenses, operating income, and diluted EPS:

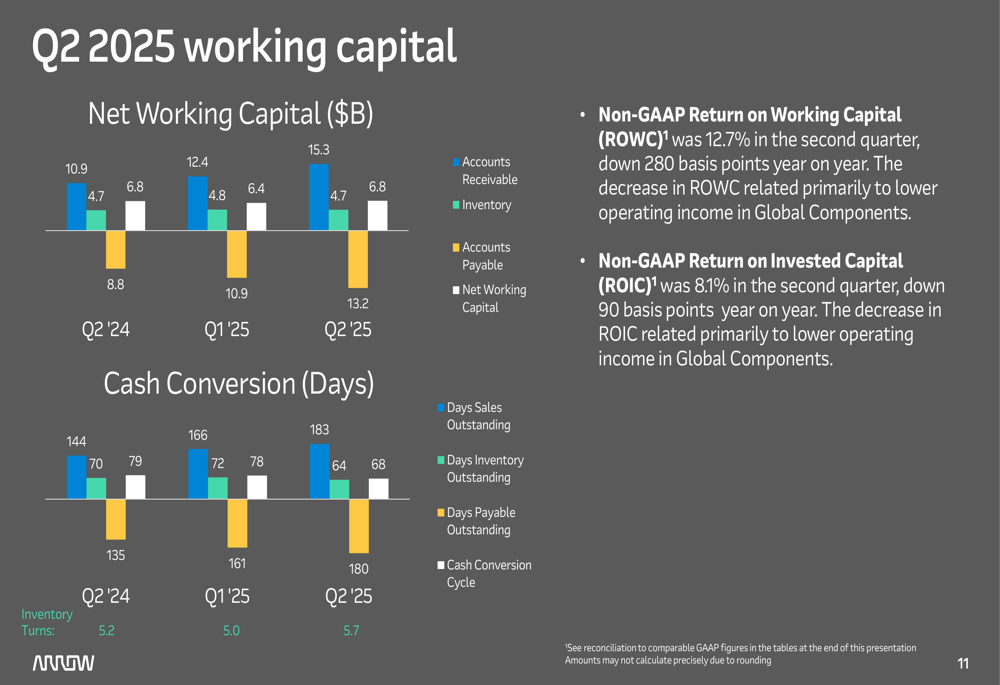

Working capital management showed improvement, with the cash conversion cycle decreasing to 68 days from 79 days in Q2 2024. However, net working capital increased to $13.2 billion from $8.8 billion in the same period last year, primarily due to higher inventory levels and accounts receivable, coupled with lower accounts payable.

The following slide details the company's working capital metrics and cash conversion cycle:

On the cash flow front, Arrow reported negative operating cash flow of $(206) million for the quarter. The company maintained a gross debt level of $2.8 billion and continued its share repurchase program, buying back $50 million in shares during the period.

Strategic Initiatives and Segment Performance

Arrow's Global Components segment, which represents approximately 70% of total revenue, showed improvement across all three regions. According to the presentation, all regions performed ahead of typical seasonal patterns, with industrial and transportation markets showing signs of recovery.

As illustrated in the following segment performance slide, the company is seeing positive indicators in its components business:

The Enterprise Computing Solutions segment delivered particularly strong results, with sales increasing 23.3% year-over-year to $2.3 billion. This growth was driven by strong performance in both Americas (up 9.2%) and EMEA (up 38.5%). The segment benefited from broad-based growth in EMEA and strength in cloud, infrastructure software, and data storage in the Americas.

The following slide details the performance of the Enterprise Computing Solutions segment:

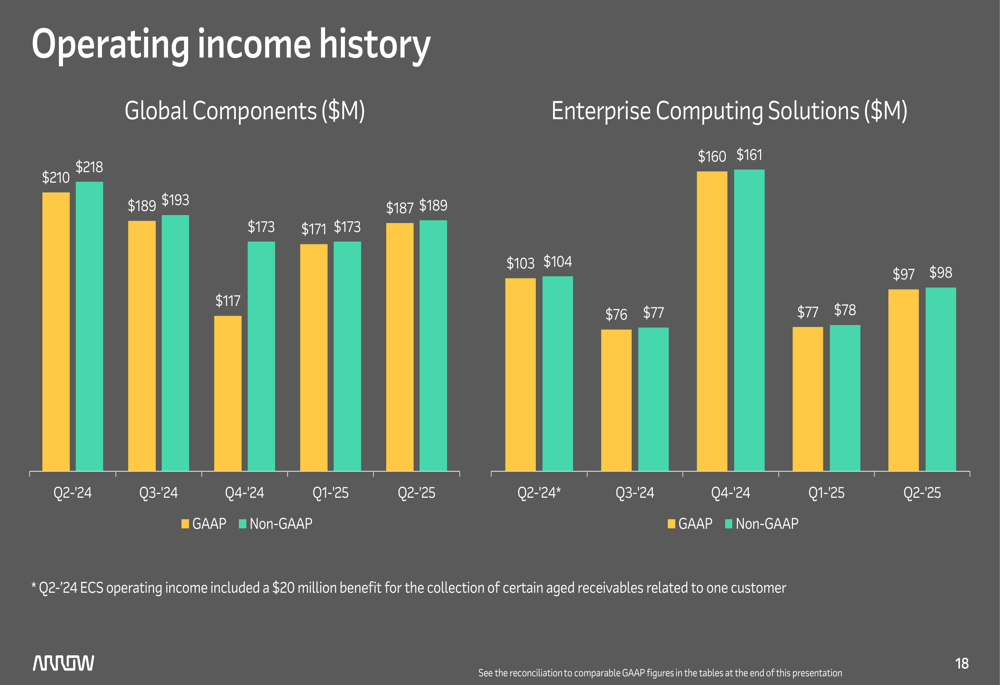

Arrow's operating income history shows the relative contribution of each segment to the company's overall profitability. While both segments have experienced fluctuations in operating income over the past five quarters, the Global Components segment has consistently generated higher operating income than the ECS segment.

The following chart illustrates the operating income history for both segments:

Forward-Looking Statements

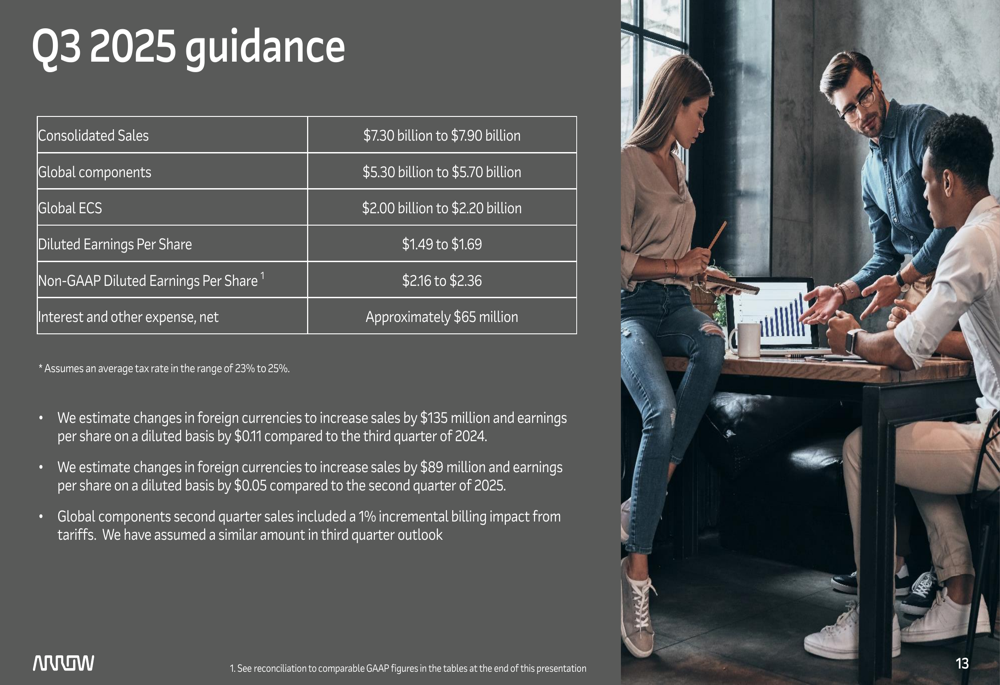

Looking ahead to the third quarter of 2025, Arrow provided guidance for consolidated sales between $7.30 billion and $7.90 billion. The company expects Global Components sales to range from $5.30 billion to $5.70 billion and Enterprise Computing Solutions sales between $2.00 billion and $2.20 billion.

For earnings, Arrow projects non-GAAP diluted EPS between $2.16 and $2.36 for Q3 2025, with interest and other expenses expected to be approximately $65 million.

The following guidance slide outlines the company's expectations for the upcoming quarter:

CEO Sean Kerins expressed optimism about the company's future in the earnings call, stating, "We are optimistic as we look to the near future." He emphasized the company's strategy to capitalize on market recovery, saying, "We want to be leaning in as the market recovers."

Despite the positive outlook, Arrow faces challenges including declining gross margins, ongoing destocking by mass market customers, and potential economic uncertainties that could affect demand in key markets like industrial and transportation.

With a current market capitalization of $5.96 billion and trading at a P/E ratio of 13.15, some analysts suggest the stock may be undervalued, presenting a potential opportunity for investors interested in the electronic equipment sector. The company's continued share repurchases also signal management's confidence in Arrow's long-term prospects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.